|

시장보고서

상품코드

2061330

UAV용 프로펠러 추진 시스템 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)UAV Propulsion Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

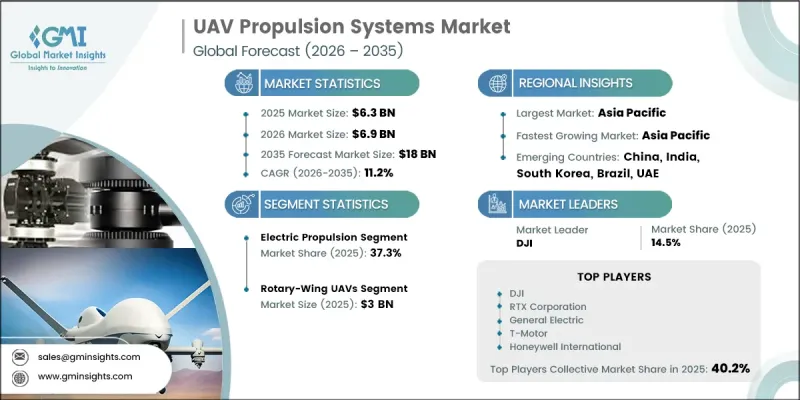

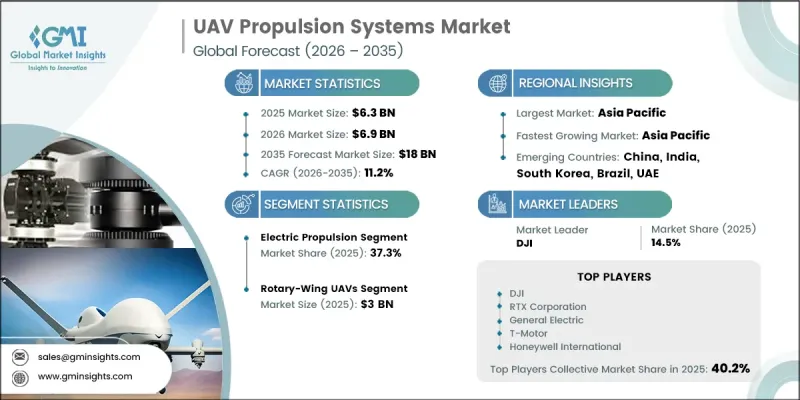

세계의 UAV용 프로펠러 추진 시스템 시장은 2025년에 63억 달러로 평가되고 CAGR 11.2%로 성장하며, 2035년까지 180억 달러에 달할 것으로 추정되고 있습니다.

전 세계 무인항공기(UAV)용 프로펠러 추진 시스템 산업의 성장은 방위 및 상업 분야에서의 무인 항공 플랫폼 도입 확대, 고효율 추진 기술에 대한 수요 증가, 그리고 방위 현대화 구상에 대한 투자 증가에 힘입어 이루어지고 있습니다. 첨단 운용 능력을 확보하기 위해 무인항공기(UAV)에 대한 의존도가 높아지는 가운데, 비행 시간 연장 및 임무 성능 향상을 지원할 수 있는 소형·경량이며 연료 효율이 뛰어난 추진 시스템의 개발이 활발히 진행되고 있습니다. 추진 아키텍처, 에너지 관리 및 전력 최적화 분야의 기술 혁신 또한 시장 확대를 지원하고 있습니다. 산업, 물류, 감시 및 보안 업무에 무인 시스템의 통합이 진행됨에 따라 신뢰성, 운영 효율성 및 내구성을 향상시키는 첨단 추진 기술에 대한 안정적인 수요가 발생하고 있습니다. 동시에, 무인항공기(UAV)의 설계 및 에너지 효율이 높은 추진 플랫폼의 급속한 발전으로 인해 항공기 전반의 성능이 향상되었으며, 이는 더 광범위한 상업적 도입을 촉진하고 있습니다. 차세대 무인항공기(UAV) 기술 및 자율 시스템에 대한 지속적인 투자는 무인항공기용 프로펠러 추진 시스템 시장의 장기적인 성장 가능성을 더욱 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 63억 달러 |

| 예측액 | 180억 달러 |

| CAGR | 11.2% |

무인항공기(UAV)용 프로펠러 추진 시스템 업계는 군사 및 민간 부문 모두에서 무인 항공 시스템의 도입이 확대됨에 따라 강력한 성장세를 보이고 있습니다. 항공 감시, 화물 운송, 산업용 검사, 농업 분야에서의 무인항공기(UAV) 활용이 확대됨에 따라 더 긴 운용 지속 시간과 효율적인 비행 성능을 실현할 수 있는 추진 기술에 대한 수요가 높아지고 있습니다. 또한 자율 기능 및 차세대 운용 능력 향상에 초점을 맞춘 군용 무인항공기(UAV) 현대화 프로그램에 대한 정부 지출 증가 역시 시장 확대를 지원하고 있습니다. 이 기간 중 산업, 감시, 물류 등 각 분야에서 무인항공기(UAV) 도입이 대폭 확대된 한편, 기술의 발전과 투자 증가가 시장 전반의 혁신을 가속화했습니다. 동시에, 첨단 추진 기술과 에너지 효율이 높은 무인항공기(UAV) 구성의 도입으로 운용 능력이 향상되어, 여러 응용 분야에서 보급이 촉진되고 있습니다.

2025년에는 전기 추진 부문이 37.3%의 점유율을 차지했습니다. 전기 시스템의 시장 침투가 확대되고 있는 것은 상업 및 국방 분야의 중소형 무인항공기(UAV) 플랫폼에서 광범위하게 활용되고 있기 때문입니다. 전기 추진 기술은 운용시 소음 저감, 배기가스 감축, 에너지 효율 향상을 실현하여 감시, 수송 및 검사 관련 용도에 매우 적합합니다. 이러한 간소화된 기계 구조, 유지보수 요구 사항의 감소, 그리고 진화하는 배터리 기술과의 호환성은 대규모 도입과 시장 수요를 계속해서 더욱 공고히 하고 있습니다.

하이브리드 방식의 무인항공기(UAV) 부문은 2035년까지 연평균 성장률(CAGR) 13.1%를 기록할 것으로 전망됩니다. 이 부문의 성장은 주로 장시간 비행 지속 능력과 뛰어난 운용 적응성을 겸비한 무인항공기(UAV) 플랫폼에 대한 수요 증가에 힘입어 이루어지고 있습니다. 하이브리드 추진 방식은 수직 이륙 능력과 효율적인 전진 비행 성능을 모두 지원하므로 장거리 작전 임무에서 큰 주목을 받고 있습니다. 이러한 운영상 이점은 상용화를 가속화하고, 첨단 무인항공기(UAV) 배치 시나리오 전반에 걸쳐 더 광범위한 도입을 촉진하고 있습니다.

북미의 무인항공기(UAV)용 프로펠러 추진 시스템 시장은 2025년에 36.7%의 점유율을 차지했습니다. 지역 시장의 성장은 막대한 국방 지출과 군사, 감시, 국토 안보 분야의 각 작전에 무인 시스템이 빠르게 통합됨에 따라 지원되고 있습니다. 이 지역은 성숙한 무인항공기(UAV) 생태계와 차세대 항공우주·방위 프로그램에 첨단 추진 기술이 지속적으로 도입되는 혜택을 누리고 있습니다. 이러한 추세에 따라 장시간 임무 및 다양한 용도에 걸친 중요한 운용 요건을 충족할 수 있는 고성능 추진 시스템에 대한 수요가 높아지고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 추진 유형별, 2022-2035년

제6장 시장 추산·예측 : 컴포넌트별, 2022-2035년

제7장 시장 추산·예측 : UAV 유형별, 2022-2035년

제8장 시장 추산·예측 : 페이로드 용량별, 2022-2035년

제9장 시장 추산·예측 : 최종 용도별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.23The Global UAV Propulsion Systems Market was valued at USD 6.3 billion in 2025 and is estimated to grow at a CAGR of 11.2% to reach USD 18 billion by 2035.

The growth of the global UAV propulsion systems industry is driven by the rising deployment of unmanned aerial platforms across defense and commercial operations, growing demand for high-efficiency propulsion technologies, and increasing investments in defense modernization initiatives. Expanding reliance on UAVs for advanced operational capabilities is encouraging the development of compact, lightweight, and fuel-efficient propulsion systems capable of supporting extended flight durations and enhanced mission performance. Technological innovations in propulsion architecture, energy management, and power optimization are also strengthening market expansion. Increasing integration of unmanned systems into industrial, logistics, monitoring, and security operations is creating consistent demand for advanced propulsion technologies that deliver reliability, operational efficiency, and improved endurance. At the same time, rapid advancements in UAV design and energy-efficient propulsion platforms are improving overall aircraft performance and supporting broader commercial adoption. Continuous investments in next-generation UAV technologies and autonomous systems are further contributing to the long-term growth potential of the UAV propulsion systems market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.3 Billion |

| Forecast Value | $18 Billion |

| CAGR | 11.2% |

The UAV propulsion systems industry is witnessing strong momentum due to the increasing adoption of unmanned aerial systems across both military and commercial sectors. Rising utilization of UAVs for aerial monitoring, cargo transportation, industrial inspections, and agricultural applications is increasing the requirement for propulsion technologies capable of delivering longer operational endurance and efficient flight performance. Market expansion is also being supported by growing government spending on military UAV modernization programs focused on improving autonomous functionality and next-generation operational capabilities. During this period, the deployment of UAVs expanded significantly across industrial, surveillance, and logistics applications, while technological advancements and rising investments accelerated innovation throughout the market. Simultaneously, the introduction of advanced propulsion technologies and energy-efficient UAV configurations is improving operational capabilities and supporting wider adoption across multiple application areas.

The electric propulsion segment accounted for a 37.3% share in 2025. Strong market penetration of electric systems is attributed to their extensive use in small and medium-sized UAV platforms across commercial and defense operations. Electric propulsion technologies provide reduced operational noise, lower emissions, and improved energy efficiency, making them highly suitable for monitoring, transportation, and inspection-related applications. Their simplified mechanical structure, lower maintenance requirements, and compatibility with evolving battery technologies continue to strengthen large-scale deployment and market demand.

The hybrid configuration UAVs segment is anticipated to register a CAGR of 13.1% during 2035. Growth within this segment is primarily driven by increasing demand for UAV platforms capable of combining extended flight endurance with enhanced operational adaptability. Hybrid propulsion configurations are gaining significant traction in long-range operational missions because they support both vertical takeoff capability and efficient forward-flight performance. These operational advantages are accelerating commercialization and encouraging wider adoption across advanced UAV deployment scenarios.

North America UAV Propulsion Systems Market held a 36.7% share in 2025. Regional market growth is supported by substantial defense expenditures and the rapid integration of unmanned systems across military, surveillance, and homeland security operations. The region benefits from a mature UAV ecosystem and continuous incorporation of advanced propulsion technologies into next-generation aerospace and defense programs. These developments are increasing demand for high-performance propulsion systems capable of supporting long-endurance missions and critical operational requirements across multiple applications.

Major companies operating in the Global UAV Propulsion Systems Market include DJI, RTX Corporation, Honeywell International Inc., Rolls-Royce plc, General Electric Company, T-Motor, Maxon, BRP-Rotax GmbH & Co KG, Orbital UAV, Hirth Engines GmbH, Sky Power GmbH, General Atomics, Hobbywing Technology Co., Ltd., H3 Dynamics, Amprius Technologies, Yuneec, KDE Direct, and Rotron Power Ltd. Companies participating in the UAV propulsion systems industry are focusing on product innovation, strategic collaborations, and advanced propulsion technology development to strengthen their competitive position. Market players are investing heavily in lightweight propulsion architectures, energy-efficient systems, and hybrid-electric technologies to improve flight endurance and operational efficiency. Many manufacturers are also prioritizing research and development activities aimed at enhancing power density, reducing emissions, and supporting autonomous UAV operations. Partnerships with defense organizations, aerospace manufacturers, and technology providers are helping companies expand their technological capabilities and accelerate commercialization.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Propulsion type trends

- 2.2.2 Component trends

- 2.2.3 UAV type trends

- 2.2.4 Payload capacity trends

- 2.2.5 End-use application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global adoption of UAVs across defense and commercial applications

- 3.2.1.2 Rising demand for long-endurance and high-efficiency UAV operations

- 3.2.1.3 Increasing defense investments and military UAV modernization programs

- 3.2.1.4 Advancements in electric and hybrid propulsion technologies

- 3.2.1.5 Increasing demand for miniaturized and specialized UAV propulsion systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs of advanced propulsion systems

- 3.2.2.2 Limited battery capacity and energy density constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of propulsion systems in Urban Air Mobility (UAM) and drone delivery networks

- 3.2.3.2 Expansion of UAV-as-a-Service (UaaS) business models across industries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Electric propulsion

- 5.2.1 Brushless DC motors

- 5.2.2 Electronic speed controllers

- 5.2.3 Others

- 5.3 Hybrid propulsion

- 5.3.1 Hybrid-electric architectures

- 5.3.2 Generator-motor systems

- 5.3.3 Others

- 5.4 Internal combustion engines

- 5.4.1 Gasoline engines

- 5.4.2 Heavy fuel engines

- 5.4.3 Piston engines

- 5.4.4 Others

- 5.5 Turbine & jet propulsion

- 5.5.1 Turbojet systems

- 5.5.2 Turbofan systems

- 5.5.3 Turboprop systems

- 5.5.4 Others

- 5.6 Fuel Cell propulsion

- 5.6.1 Hydrogen fuel cells

- 5.6.2 PEM (proton exchange membrane) fuel cells

- 5.6.3 Hybrid fuel cell-battery systems

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Motors & engines

- 6.2.1 Brushless motors

- 6.2.2 Brushed motors

- 6.2.3 IC engines (piston, rotary, turbine)

- 6.3 Battery & energy storage systems

- 6.3.1 Lithium-ion batteries

- 6.3.2 Solid-state batteries

- 6.3.3 Fuel storage systems

- 6.3.4 Others

- 6.4 Propellers & rotor systems

- 6.4.1 Fixed-pitch propellers

- 6.4.2 Variable-pitch propellers

- 6.4.3 Rotor assemblies

- 6.4.4 Others

- 6.5 Accessories & supporting components

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By UAV Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fixed-wing UAVs

- 7.2.1 Short-range fixed-wing

- 7.2.2 Medium-range fixed-wing

- 7.2.3 Long-range fixed-wing

- 7.3 Rotary-wing UAVs

- 7.3.1 Quadcopters & multirotors

- 7.3.2 Helicopter configuration UAVs

- 7.3.3 Others

- 7.4 Hybrid configuration UAVs

- 7.4.1 VTOL fixed-wing systems

- 7.4.2 Tilt-rotor UAVs

- 7.4.3 Others

Chapter 8 Market Estimates and Forecast, By Payload Capacity, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Less than 2 kg

- 8.3 2-25 kg

- 8.4 25-150 kg

- 8.5 150-600 kg

- 8.6 More than 600 kg

Chapter 9 Market Estimates and Forecast, By End-use Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Military & defense

- 9.2.1 Combat UAVs & loitering munitions

- 9.2.2 Surveillance & reconnaissance (ISR)

- 9.2.3 Target drones & training systems

- 9.2.4 Others

- 9.3 Commercial

- 9.3.1 Agriculture & precision farming

- 9.3.2 Logistics & package delivery

- 9.3.3 Media & entertainment

- 9.3.4 Others

- 9.4 Civil government

- 9.4.1 Law enforcement & border patrol

- 9.4.2 Emergency response & disaster management

- 9.4.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 DJI

- 11.1.2 RTX Corporation

- 11.1.3 General Electric

- 11.1.4 T-Motor

- 11.1.5 Honeywell International

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 General Atomics

- 11.2.1.2 Amprius Technologies

- 11.2.1.3 KDE Direct

- 11.2.2 Asia Pacific

- 11.2.2.1 Hobbywing Technology Co., Ltd.

- 11.2.2.2 Yuneec

- 11.2.3 Europe

- 11.2.3.1 Rolls-Royce plc

- 11.2.3.2 Maxon

- 11.2.3.3 BRP-Rotax GmbH & Co KG

- 11.2.3.4 Hirth Engines GmbH

- 11.2.3.5 Sky Power GmbH

- 11.2.3.6 Rotron Power Ltd.

- 11.2.4 Middle East & Africa

- 11.2.4.1 H3 Dynamics

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Orbital UAV