|

시장보고서

상품코드

2061642

UAV 추진 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)UAV Propulsion Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

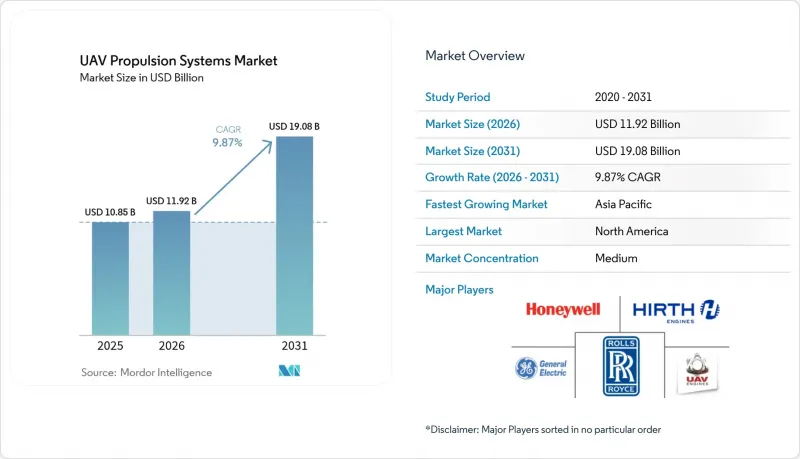

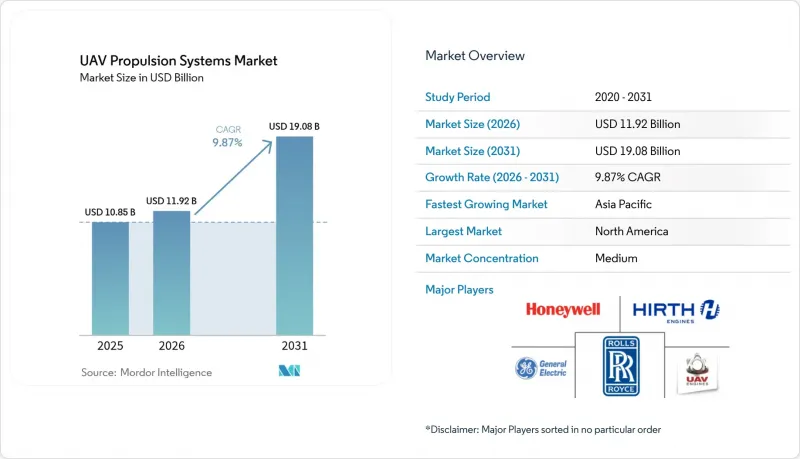

Mordor Intelligence에 의하면, 무인항공기(UAV) 추진 시스템 시장 규모는 2025년에 108억 5,000만 달러로 평가되었고, 2026년 119억 2,000만 달러로 추정되고, 2031년까지 190억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.87%를 나타낼 전망입니다.

본 보고서는 엔진 유형별(기존, 하이브리드, 순전기식), 연료 유형별(가솔린, 중유, 수소 등), 비행 시간 등급별(1시간 미만, 1-3시간, 기타), UAV 유형별(마이크로 UAV, 미니 UAV, 전술용 UAV 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 UAV 추진 시스템 시장 동향 및 분석

전기차 및 하이브리드 전기차에 대한 수요 급증

전기 및 하이브리드 전기 추진 시스템은 음향 및 적외선 신호를 줄이고, 열악한 환경에 위치한 기지에서의 유지보수를 간소화하며, 부피가 큰 액체 연료를 모듈식 배터리 팩으로 대체함으로써 공급망의 무게를 줄여줍니다. 노스롭 그루먼사의 1,250파운드 시스템을 탑재한 DARPA의 XRQ-73 셰퍼드(SHEPARD) 하이브리드기는 직렬 구성이 스텔스 성능을 저해하지 않으면서도 수 시간에 걸친 체공을 실현하는 방법을 보여주고 있습니다. 하네웰의 1MW 터보 발전기는 이러한 장점을 대형 화물 드론에 적용하여 기존 출력 수준을 3배로 높이고, 더 큰 주익에 분산 배치된 전동 모터의 구현을 가능하게 합니다. 각국의 국방부는 현재 국경 대치 구역에서 음향 감지를 회피할 수 있는 소음이 적은 침투형 드론에 대한 예산을 편성하고 있습니다. 조달 부서는 평균 수리 시간을 단축할 수 있는 간소화된 라인 교체 가능 유닛을 중시하고 있으며, 이에 따라 전기 하이브리드 추진 시스템이 향후 입찰의 핵심이 되고 있습니다. 그 결과, 무인항공기(UAV) 추진 시스템 시장에서는 기존 기업들이 인버터, 배터리, 열 관리 전문 기업들과 제휴하여 출력 대 중량 비율 목표와 전장 내구성의 균형을 맞추고 있습니다.

군용 스웜 드론 운용 및 자율 전투 시스템

스웜(군집) 개념에서는 수십 대에서 수백 대의 소형 네트워크 드론을 전개하여 적의 방어망을 포화시키고, 신속한 대응을 유도하며, 높은 소모율을 감수합니다. 미 육군의 '런치드 이펙츠(Launched Effects)' 실험에서는 양산 및 비행 전 자가 진단을 목적으로 설계된 소형 엔진과 전동 팬이 공개되었습니다. 독일의 1,000억 유로(1,177억 달러) 규모 재군비 계획에서 로탈링 무니션과 자율형 윙맨이 주요 지출 분야로 부상하면서, 일회용 기체에 장착 가능한 동일 사양의 추진 포드에 대한 대량 생산 기회가 생겨나고 있습니다. AI 미션 컨트롤러가 무리 전체의 스로틀, 상태, 비상 정지를 관리할 수 있도록 추진 장치에는 공통 디지털 인터페이스가 필요합니다. 표준화를 통해 정비 공장의 조립 라인이 효율화되고, 수명 주기 비용이 절감됩니다. 이는 한 번의 임무에서 수십 대의 기체가 소모될 가능성이 있는 경우, 중요한 지표가 됩니다. 따라서, 군집 전술의 도입은 소형 모터 분야의 혁신을 가속화하고, 무인항공기(UAV) 추진 시스템 시장의 생산 능력을 확대할 것입니다.

배터리 에너지 밀도의 한계에 도달

리튬 이온 배터리의 에너지 밀도는 여전히 300 Wh/kg 수준에서 정체되어 있습니다. 10-60℃의 환경에서 전술용 eVTOL을 운용하면 급속한 성능 저하가 발생하여 배터리 수명이 100회 전투 주기 미만으로 단축됩니다. 그 결과, 비행 시간이 20-30분으로 제한됨에 따라 군은 예비 배터리를 비축하거나 하이브리드 부스터를 추가할 수밖에 없게 되어 물류 부담이 가중됩니다. 온도 상승에 대처하려면 액체 냉각식 케이스가 필요하며, 이로 인해 무게가 증가하여 탑재량이 감소합니다. 전고체 전지나 리튬-황 전지의 시제품에는 기대가 모아지고 있지만, NATO의 안전 기준을 충족시키려면 양산화가 필요합니다. 그 전까지는 배터리의 한계로 인해 순수 전기 방식의 도입이 제약을 받게 되며, 이는 무인항공기(UAV) 추진 시스템 시장의 각 부문에서 성장 속도가 둔화되는 결과를 초래할 것입니다.

부문별 분석

2025년 기준으로, UAV 추진 시스템 시장의 39.35%를 기존 엔진이 차지했으며, 고온 및 고열 환경이나 모래먼지가 많은 환경에서도 확고한 신뢰성을 입증하고 있습니다. 그러나 은밀성, 유지보수 용이성, 모듈성의 장점이 현대 군사 전략에 부합하기 때문에 전전기식 유닛 시장은 연평균 성장률(CAGR) 12.68%로 성장하고 있습니다. 하이브리드 발전 시스템은 순항 시 부하를 중유 터빈에 맡기면서도 배터리를 통해 조용한 접근을 가능하게 함으로써, 탑재량 격차를 해소하고 있습니다. '프린트 투 플라이(Print-to-Fly)' 방식의 마이크로터빈은 일회용 탄약에 제트 엔진의 성능을 적용함으로써, 내연 기관과 전기 구동 방식 간의 경쟁을 더욱 치열하게 만들고 있습니다. 투자자들은 예상치 못한 가동 중단 시간을 줄이기 위한 공통 코어 인버터 및 디지털 트윈에 대한 연구 개발을 추진하고 있으며, 이는 UAV 추진 시스템 시장 전반의 도입 곡선을 가속화하고 있습니다.

플랫폼 통합 업체들은 기체 전체의 분석 데이터에 반영되는 상태 모니터링 기능이 내장된, 밀폐형 서브시스템으로 제공되는 엔진을 선호합니다. 전기 모터는 순항 시 98%의 효율을 달성하며, 적외선 흔적을 대폭 줄입니다. 반면, kW급 발전기가 기내 히터나 제빙 키트에 전력을 공급하는 북극권이나 사막의 전초기지에서는 중유를 연료로 사용하는 2행정 엔진이 여전히 필수적입니다. 따라서 조달 기관은 전력 모드를 전환할 수 있는 플러그 앤 플레이형 아키텍처를 요구하고 있으며, 이를 통해 부품 재사용이 촉진되고 예비 부품 재고 리스크가 감소합니다. 이러한 모듈화 개념이 무인항공기(UAV) 추진 시스템 시장에서 하이브리드 대응 설계가 우위를 점할 것으로 예상되는 배경이 되고 있습니다.

휘발유는 전 세계적인 공급 안정성과 입증된 저온 시동 신뢰성에 힘입어, 2025년 무인항공기(UAV) 추진 시스템 시장 규모에서 43.05%의 점유율을 차지했습니다. 수소 솔루션은 출력 밀도 향상과 그린 수소 인프라 확장이 맞물려, 거의 소음이 없는 비행 환경에서 장시간 비행을 가능하게 함에 따라 13.08%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 중유인 JP-8의 다양한 유형은 병참적 측면의 공통성과 함상에서의 안전성을 우선시하는 방위 분야 사용자에게 여전히 중요한 선택지로 남아 있습니다. 배터리만 사용하는 구성은 임무 시간이 1시간 미만이고 탑재 하중이 10kg 미만인 등급에서 주류를 이룹니다. 중국의 액체 수소 고정익 시제기 등 실증 기체들은 저장 및 배기 관련 기준이 아직 발전 단계에 있음에도 불구하고, 극저온 연료가 대형 무인항공기(UAV)를 구동할 수 있음을 입증하고 있습니다.

태양광 발전을 보조 전원으로 사용하는 기체는 여전히 틈새 시장에 머물러 있지만, 수소를 이용한 항속 거리 연장 장치와 결합이 가능한 초박형 태양전지 소재 연구를 주도하고 있습니다. 압축 가스의 충전 시간은 배터리 충전 주기보다 짧기 때문에 출격 빈도가 높은 모델의 경우 수소가 가용성 측면에서 우위를 점하고 있습니다. 연료 선택은 냉각 전략, 임무 계획 및 탄소 배출량 산정 지표에 영향을 미치며, 이러한 요소들은 현재 유럽과 아시아의 공공 입찰에도 반영되고 있습니다. 따라서 공급업체들은 다양한 기체 크기에 대응할 수 있는 모듈식 탱크와 퀵 디스커넥트 밸브를 개발하고 있으며, 무인항공기(UAV) 추진 시스템 시장의 기술 선택 변화에 발맞추어 잔존 가치를 확보하고 있습니다.

지역별 분석

북미는 2025년에 33.40%의 점유율을 유지했습니다. 이는 미국 국방부의 프로그램, FAA의 시험 비행 노선, 그리고 실리콘밸리의 자본이 결합되어 견실한 수요와 신속한 인증 절차를 만들어내고 있기 때문입니다. DARPA와 AFWERX의 지원금은 초기 단계 엔진의 위험을 완화하는 한편, 미 해군의 함상 시험에서는 해상에서의 수소 연료 보급이 평가되고 있습니다. 정책 측면에서는 주 정부의 에너지 크레딧 제도와 기지의 마이크로그리드 현대화 사업이 연계되어 하이브리드 방식의 도입을 촉진하고 있습니다.

아시아태평양은 중국의 1조 위안 규모 저탄소 경제 구상이 국내 추진 시스템 개발을 촉진하고 연료전지 시험 차량에 대한 지원을 실시하고 있어, 11.32%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 인도의 '아트마니르바르(Atmanirbhar)' 이니셔티브는 수입 전자 부품에 대한 의존도를 낮추기 위해, 오프셋 자금을 중유 피스톤 엔진 및 하이브리드 기술 연구 개발에 투입하고 있습니다. 일본은 도시형 eVTOL을 위해 가스터빈·전기 하이브리드 기술을 선도적으로 개발하고 있으며, 한국은 방위 수출 마스터플랜에 수소 드론을 포함시켰습니다. 다양한 규제 기준은 수출 사양의 복잡성을 초래하는 한편, 병행된 혁신을 촉진하여 UAV 추진 시스템 시장의 전반적인 기회를 확대되고 있습니다.

유럽에서는 EASA가 소음 및 CO2 배출량 상한선을 시행하고, 투자가 전기 및 수소 기술로 전환됨에 따라 시장이 꾸준히 성장하고 있습니다. 프랑스와 독일은 국경을 넘는 수소 화물 운송 회랑을 시범 운영하는 'HyPoTraDe' 프로젝트에 공동 투자하고 있습니다. 영국은 Loyal Wingman 프로그램용 중유 엔진의 형식 인증 실증을 가속화하기 위해 적층 가공 터빈 센터를 지원하고 있습니다. 탄소 가격 책정은 제로 배출 동력 장치의 투자 수익률(ROI)을 높이고, 공동 연구 네트워크는 지식 공유를 공고히 하며, UAV 추진 시스템 시장 전반에서 유럽의 입지를 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the uAV propulsion systems market size was valued at USD 10.85 billion in 2025 and estimated to grow from USD 11.92 billion in 2026 to reach USD 19.08 billion by 2031, at a CAGR of 9.87% during the forecast period (2026-2031).

This report is Segmented by Engine Type (Conventional, Hybrid, Full-Electric), Fuel Type (Gasoline, Heavy Fuel, Hydrogen, and More), Endurance Class (Less Than 1 Hour, 1-3 Hours, and More), UAV Type (Micro UAV, Mini UAV, Tactical UAV, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global UAV Propulsion Systems Market Trends and Insights

Surge in E- and Hybrid-Electric Demand

Electric and hybrid-electric propulsion lowers acoustic and infrared signatures, simplifies maintenance at austere bases, and trims supply-chain weight by replacing bulk liquid fuel with modular battery packs. DARPA's XRQ-73 SHEPARD hybrid, powered by Northrop Grumman's 1,250-lb system, illustrates how series configurations deliver multi-hour loiter without compromising stealth. Honeywell's 1 MW turbogenerator scales these gains for heavy cargo drones, tripling earlier power levels and enabling distributed electric motors on larger wings. Defence ministries now budget for silent ingress drones that avoid acoustic detection at border standoff ranges. Procurement offices highlight simplified line-replaceable units that cut mean-time-to-repair, making electric-hybrid propulsion central to future tenders. In turn, the UAV propulsion system market sees incumbents partner with inverter, battery, and thermal-management specialists to balance power-to-weight targets with battlefield durability.

Military Swarm Drone Operations and Autonomous Combat Systems

Swarm concepts deploy dozens to hundreds of small, networked drones that saturate defenses, demand rapid thrust response, and accept higher attrition. US Army "launched effects" experiments showcase miniature engines and electric fans engineered for mass production and pre-flight self-diagnostics. Germany's EUR 100 billion (USD 117.7 billion) rearmament makes loitering munitions and autonomous wingmen core spending areas, creating large-volume opportunities for identical propulsion pods that clip into disposable airframes. Powerplants need common digital interfaces so AI mission controllers can manage throttle, health, and emergency shutdown across the swarm. Standardization accelerates depot assembly lines and lowers life-cycle cost, a key metric when each mission may consume dozens of vehicles. Swarm adoption, therefore, accelerates mini-motor innovation and stretches production capacity within the UAV propulsion system market.

Battery Energy-Density Plateau

Lithium-ion chemistries remain locked near 300 Wh/kg; tactical eVTOL sorties at 10-60 °C discharge trigger fast degradation and shorten battery life to under 100 combat cycles. Resulting 20-30 minute flight times force armies to stock spare packs or add hybrid boosters, raising the logistical burden. Thermal spikes require liquid-cooled enclosures that add weight and lower payload. Solid-state and lithium-sulfur prototypes show promise but need scale to meet NATO safety rules. Until then, battery limits cap pure-electric adoption, moderating the expansion pace in segments of the UAV propulsion system market.

Other drivers and restraints analyzed in the detailed report include:

- Defense Modernization Budgets for MALE/HALE UAVs

- Hydrogen Fuel-Cell Range-Extender Breakthroughs

- Rare-Earth Magnet Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional engines held 39.35% of the UAV propulsion system market 2025, signaling entrenched reliability for high-hot and sandy environments. Yet full-electric units expand at a 12.68% CAGR thanks to stealth, maintenance, and modular benefits that resonate with modern doctrines. Hybrid generators bridge payload gaps by handing cruise loads to heavy-fuel turbines while batteries power silent ingress. Print-to-fly micro-turbines democratize jet performance for expendable munitions, tightening competition between combustion and electric lines. Investors steer R&D toward common-core inverters and digital twins that cut unplanned downtime, reinforcing adoption curves across the UAV propulsion system market.

Platform integrators prefer engines delivered as sealed sub-systems with embedded health-monitoring that feed fleet-wide analytics. Electric motors achieve 98% efficiency at cruise, slashing infrared traces. Conversely, heavy-fuel two-strokes remain essential for Arctic and desert outposts where kilowatt-class generators power onboard heaters and de-icing kits. Procurement agencies thus request plug-and-play architecture that toggles between power modes, accelerating component reuse and lowering spares inventory exposure. This modular philosophy underpins forecast dominance of hybrid-ready designs in the UAV propulsion system market.

Gasoline held a 43.05% share of the UAV propulsion systems market size in 2025, supported by global availability and proven cold-start reliability. Hydrogen solutions register the highest 13.08% CAGR as power density gains and green-hydrogen infrastructure scale converge to unlock extended sorties at near-silent acoustic profiles. Heavy-fuel JP-8 variants maintain relevance for defense users who prioritize logistics commonality and shipboard safety. Battery-only configurations dominate sub-10 kg payload classes where missions last under one hour. Demonstrators such as China's liquid-hydrogen fixed-wing prototype prove that cryogenic fuel can support large UAVs, although storage and venting standards are still evolving.

Solar-assisted craft remains a narrow niche yet drives material research for ultrathin photovoltaics that could pair with hydrogen range extenders. Refueling times for compressed gas undercut battery recharge cycles, giving hydrogen an edge in availability for high sortie frequency models. Fuel selection influences cooling strategy, mission planning, and carbon accounting metrics, which now appear in European and Asian public tenders. Suppliers therefore engineer modular tanks and quick-disconnect valves that integrate with multiple airframe sizes, safeguarding residual value as technology choices shift through the UAV propulsion systems market.

Geography Analysis

North America sustained 33.40% share in 2025 because Pentagon programs, FAA test corridors, and Silicon Valley capital coalesce into robust demand and swift certification pipelines. DARPA and AFWERX grants de-risk early-stage engines, while US Navy shipboard tests evaluate hydrogen refueling at sea. Policy aligns state energy credits with base microgrid upgrades, incentivizing hybrid adoption.

Asia-Pacific posts the strongest 11.32% CAGR as China's trillion-yuan low-altitude economy charter encourages domestic propulsion lines and subsidizes fuel-cell trial fleets. India's Atmanirbhar initiative channels offset funds into heavy-fuel piston and hybrid labs to cut reliance on imported electronics. Japan pioneers gas-turbine electric hybrids for urban eVTOL, and South Korea includes hydrogen drones in its defence-export masterplan. Diverse regulatory codes create export-variant complexity yet drive parallel innovation, expanding overall opportunity within the UAV propulsion system market.

Europe grows steadily as EASA enforces noise and CO2 caps that tilt spending toward electric and hydrogen. France and Germany co-finance HyPoTraDe to validate cross-border hydrogen cargo corridors. The UK backs additive turbine centers that accelerate Type-Cert demonstrations for heavy-fuel engines destined for Loyal Wingman programs. Carbon pricing boosts ROI for zero-emission powerplants, and collective research networks ensure shared lessons, reinforcing continental momentum across the UAV propulsion system market.

- Honeywell International Inc.

- Rolls-Royce plc

- General Electric Company

- Sky Power GmbH

- UAV Engines Limited

- Hirth Engines GmbH (UMS SKELDAR)

- Orbital Corporation Ltd

- Intelligent Energy Limited

- H3 Dynamics Holdings Pte. Ltd.

- VerdeGo Aero, Inc.

- Rotron Power Ltd.

- Electra.Aero.

- PBS AEROSPACE

- DeltaHawk Engines, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e- and hybrid-electric demand

- 4.2.2 Military swarm drone operations and autonomous combat systems

- 4.2.3 Defence modernisation budgets for MALE/HALE UAVs

- 4.2.4 Drone-as-a-service retrofit kits

- 4.2.5 Hydrogen fuel-cell range-extender breakthroughs

- 4.2.6 Additive-manufactured micro-turbine cost deflation

- 4.3 Market Restraints

- 4.3.1 Battery energy-density plateau

- 4.3.2 Rare-earth magnet supply constraints

- 4.3.3 Export-control (ITAR/MTCR) restrictions

- 4.3.4 Ultra-low thermal-/acoustic-signature thresholds for contested airspace

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Engine Type

- 5.1.1 Conventional

- 5.1.2 Hybrid

- 5.1.3 Full-Electric

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Heavy Fuel

- 5.2.3 Hydrogen

- 5.2.4 Battery (Li-ion, Li-S)

- 5.2.5 Solar-Augmented

- 5.3 By Endurance Class

- 5.3.1 Less than 1 hour

- 5.3.2 1 - 3 hours

- 5.3.3 3 - 6 hours

- 5.3.4 Greater than 6 hours

- 5.4 By UAV Type

- 5.4.1 Micro UAV

- 5.4.2 Mini UAV

- 5.4.3 Tactical UAV

- 5.4.4 MALE UAV

- 5.4.5 HALE UAV

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 France

- 5.5.3.3 Germany

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Rolls-Royce plc

- 6.4.3 General Electric Company

- 6.4.4 Sky Power GmbH

- 6.4.5 UAV Engines Limited

- 6.4.6 Hirth Engines GmbH (UMS SKELDAR)

- 6.4.7 Orbital Corporation Ltd

- 6.4.8 Intelligent Energy Limited

- 6.4.9 H3 Dynamics Holdings Pte. Ltd.

- 6.4.10 VerdeGo Aero, Inc.

- 6.4.11 Rotron Power Ltd.

- 6.4.12 Electra.Aero.

- 6.4.13 PBS AEROSPACE

- 6.4.14 DeltaHawk Engines, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment