|

시장보고서

상품코드

2061388

요검사 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Urinalysis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

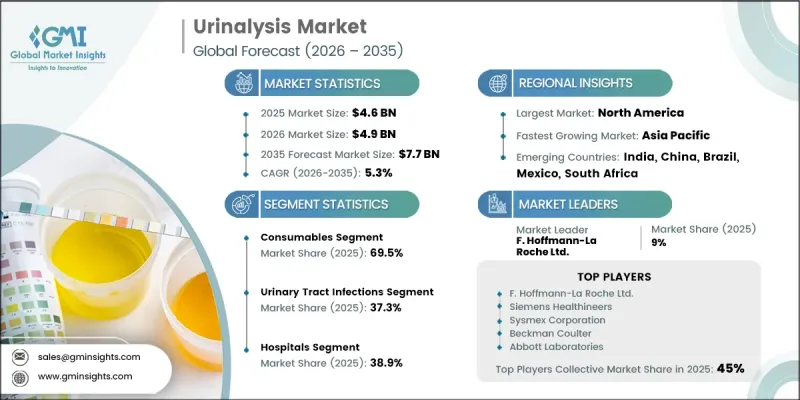

세계의 요검사 시장은 2025년에 46억 달러로 평가되고 CAGR 5.3%로 성장하며, 2035년까지 77억 달러에 달할 것으로 추정되고 있습니다.

시장 확대는 개발도상 지역에서 요로감염증의 부담이 증가하고, 전 세계에서 만성 신장병 유병률이 상승하며, 고령 인구가 급속히 증가함에 따라 지원되고 있습니다. 이러한 요인들이 복합적으로 작용하여, 정기적인 진단 검진 및 질병의 조기 발견에 대한 수요가 높아지고 있습니다. 소변의 물리적, 화학적, 현미경적 특성을 평가하는 소변 검사는 요로 감염, 신장 질환, 당뇨병 및 다양한 대사이상을 확인·모니터링하기 위한 기본적인 진단 방법으로 계속해서 활용되고 있습니다. 개발도상국에서 위생 환경의 악화, 깨끗한 식수에 대한 접근 제한, 의료 인프라의 미비 등 위험 요인에 노출되는 경우가 늘어나고 있으며, 감염률이 더욱 높아지고 있습니다. 동시에, 당뇨병 등 만성질환의 유병률 증가로 인해 감염병에 대한 감수성이 높아지면서, 그 결과 환자층이 확대되고 있습니다. 의료 시스템에서는 조기 진단과 예방 의학이 점점 더 중요시되면서, 소변 검사는 핵심적인 진단 툴로서의 위상을 공고히 하고 있습니다. 또한 전 세계에서 만성 신장 질환의 부담이 증가하고 있는 점도 소변 검사를 기반으로 한 검사 솔루션에 대한 장기적인 수요를 더욱 부추기고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 46억 달러 |

| 예측 시장 규모 | 77억 달러 |

| CAGR | 5.3% |

2025년에는 소모품 부문이 시장 점유율의 69.5%를 차지했습니다. 이 부문에는 일상적인 소변 검사 절차에 사용되는 테스트 스트립, 시약, 딥스틱 및 기타 일회용 검사 용품이 포함됩니다. 병원, 임상검사실 및 현장진단(Point-of-Care) 환경에서 이루어지는 진단 검사는 반복적으로 수행되는 특성을 가지고 있으므로 수요는 지속적으로 높은 수준을 유지하고 있습니다. 질환 모니터링 요건과 광범위한 선별 검사의 시행에 힘입어 지속적인 사용 주기가 형성됨에 따라 안정적이고 반복적인 소비가 보장되고 있습니다. 요로 감염증, 신장 관련 질환 및 만성질환의 발생률 증가는 이러한 소모품에 대한 지속적인 수요를 더욱 강화하고 있습니다.

2025년 기준으로 요로감염 부문은 37.3%의 시장 점유율을 차지했습니다. 이 응용 분야는 다양한 인구 집단에 감염병이 널리 퍼져 있으므로 소변 검사의 가장 중요한 용도 중 하나가 되고 있습니다. 소변 검사는 세균의 활동 및 관련 감염 지표를 검출하기 위한 주요 진단법으로 기능하며, 요로 감염을 신속하고 확실하게 확인하는 데 도움이 됩니다. 특히 여성, 고령자 및 기저질환이 있는 환자들 사이에서 감염률이 상승하고 있는 것이 전 세계에서 높은 검사 건수를 지속적으로 이끌고 있습니다.

2025년, 북미 소변 검사 시장은 35.7%의 점유율을 차지했습니다. 이 지역은 첨단 의료 인프라, 높은 진단 의식, 그리고 확립된 질병 선별 검진 관행에 힘입어 계속해서 강력한 성장세를 보이고 있습니다. 만성 신장 질환 및 기타 장기적인 건강 문제의 유병률 증가가 진단 검사 수요 증가에 크게 기여하고 있습니다. 지속적인 모니터링이 필요한 환자층이 확대됨에 따라 일상적인 의료 업무 흐름에서 소변 검사의 중요성이 더욱 커지고 있습니다. 자동화·고처리량형 진단 시스템의 보급은 검사의 효율과 정확도를 높이고, 임상 판단의 개선을 지원하는 동시에 해당 지역 전체의 시장 성장을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035년

제6장 시장 추산·예측 : 테스트 유형별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 최종 사용별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

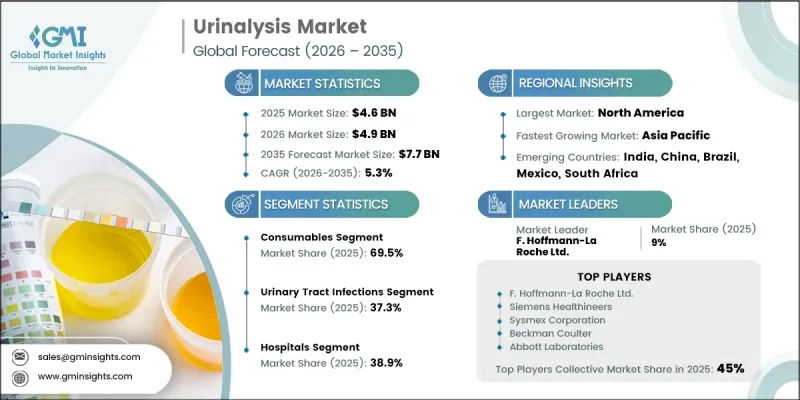

KSA 26.06.24The Global Urinalysis Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 7.7 billion by 2035.

Market expansion is supported by a rising burden of urinary tract infections across developing regions, increasing global prevalence of chronic kidney disease, and a rapidly growing elderly population. These factors are collectively strengthening the demand for routine diagnostic screening and early disease detection. Urinalysis, which evaluates the physical, chemical, and microscopic properties of urine, remains a fundamental diagnostic approach for identifying and monitoring urinary tract infections, kidney disorders, diabetes, and various metabolic abnormalities. Growing exposure to risk factors such as poor sanitation, limited access to clean drinking water, and inadequate healthcare infrastructure in developing economies is further increasing infection rates. At the same time, rising incidence of chronic diseases such as diabetes is contributing to higher susceptibility to infections, thereby expanding the patient pool. Healthcare systems are increasingly prioritizing early diagnosis and preventive care, positioning urinalysis as a core diagnostic tool. In addition, the rising global burden of chronic kidney disease is further reinforcing long-term demand for urinalysis-based testing solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.7 Billion |

| CAGR | 5.3% |

The consumables segment accounted for 69.5% share in 2025. This segment includes test strips, reagents, dipsticks, and other disposable testing materials used in routine urine analysis procedures. Demand remains consistently high due to the repetitive nature of diagnostic testing in hospitals, clinical laboratories, and point-of-care environments. Continuous usage cycles, driven by disease monitoring requirements and widespread screening practices, ensure stable and recurring consumption. The growing incidence of urinary tract infections, kidney-related disorders, and chronic illnesses further strengthens sustained demand for these consumable products.

The urinary tract infections segment held a share of 37.3% in 2025. This application area represents one of the most significant uses of urinalysis due to the widespread prevalence of infections across diverse population groups. Urinalysis serves as a primary diagnostic method for detecting bacterial activity and related infection markers, enabling fast and reliable identification of urinary tract infections. Rising infection rates, particularly among women, elderly individuals, and patients with underlying health conditions, continue to drive high testing volumes globally.

North America Urinalysis Market accounted for 35.7% share in 2025. The region continues to exhibit strong growth, supported by advanced healthcare infrastructure, high diagnostic awareness, and well-established disease screening practices. The growing prevalence of chronic kidney disease and other long-term health conditions is significantly contributing to increased diagnostic testing demand. A large patient base requiring continuous monitoring further reinforces the importance of urinalysis in routine healthcare workflows. The widespread availability of automated and high-throughput diagnostic systems enhances testing efficiency and accuracy, supporting improved clinical decision-making and strengthening market growth across the region.

Key players operating in the Global Urinalysis Industry include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, Beckman Coulter, Bio-Rad Laboratories, Becton, Dickinson and Company (BD), Sysmex Corporation, QuidelOrtho Corporation, ARKRAY Inc., ACON Laboratories, Cardinal Health, DIRUI Industrial, URIT Medical, and 77 Elektronika. Companies in the urinalysis market are focusing on the development of automated and high-throughput diagnostic systems to improve testing speed, accuracy, and workflow efficiency in clinical settings. They are investing in advanced reagent technologies and digital integration to enhance result interpretation and laboratory connectivity. Expansion of point-of-care testing solutions is another key strategy, enabling faster diagnostics outside traditional laboratory environments. Strategic partnerships with healthcare providers and diagnostic laboratories are strengthening product adoption and distribution reach. Manufacturers are also emphasizing cost-effective consumable innovations to support high-volume testing requirements. In addition, continuous research and development efforts are being directed toward improving sensitivity, reducing turnaround time, and expanding test menus to cover a wider range of diseases and metabolic conditions, thereby reinforcing competitive positioning in the global market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy and data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy and data integrity commitment

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Test type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.2.5 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of urinary tract infection in developing regions

- 3.2.1.2 Increasing prevalence of chronic kidney disease worldwide

- 3.2.1.3 Increasing geriatric population

- 3.2.1.4 High pregnancy rates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Low awareness about routine check-ups

- 3.2.2.2 High R&D cost of developing instruments

- 3.2.3 Market opportunities

- 3.2.3.1 Development of multiparametric & biomarker-rich tests

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing trend analysis (Driven by primary research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.2.1 Dipsticks

- 5.2.2 Reagents

- 5.2.3 Disposables

- 5.2.4 Pregnancy & fertility kits

- 5.3 Instruments

- 5.3.1 Biochemical urine analyzer

- 5.3.2 Automated urine sediment analyzer

Chapter 6 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Biochemical urinalysis

- 6.3 Sediment urinalysis

- 6.4 Pregnancy & fertility testing

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Urinary tract infections

- 7.3 Kidney disease

- 7.4 Pregnancy

- 7.5 Diabetes

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Clinical laboratories

- 8.3 Hospitals

- 8.4 Home healthcare

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ACON Laboratories

- 10.3 ARKRAY Inc.

- 10.4 Beckman Coulter

- 10.5 Bio-Rad Laboratories

- 10.6 Becton, Dickinson and Company (BD)

- 10.7 Cardinal Health

- 10.8 DIRUI Industrial

- 10.9 QuidelOrtho Corporation

- 10.10 Roche Diagnostics

- 10.11 Siemens Healthineers

- 10.12 Sysmex Corporation

- 10.13 Thermo Fisher Scientific

- 10.14 URIT Medical

- 10.15 77 Elektronika