|

시장보고서

상품코드

2057473

반려동물 진단 시장 : 제품별, 기술별, 용도별, 동물 유형별, 최종사용자별, 지역별 - 예측(-2031년)Companion Animal Diagnostic Market by Product (Consumable, Instrument), Technology (Immunodiagnostic, ELISA, PCR Test, Urinalysis, Hematology), Animal Type (Dog, Cat), Application (Clinical Pathology, Virology), End User - Global Forecast to 2031 |

||||||

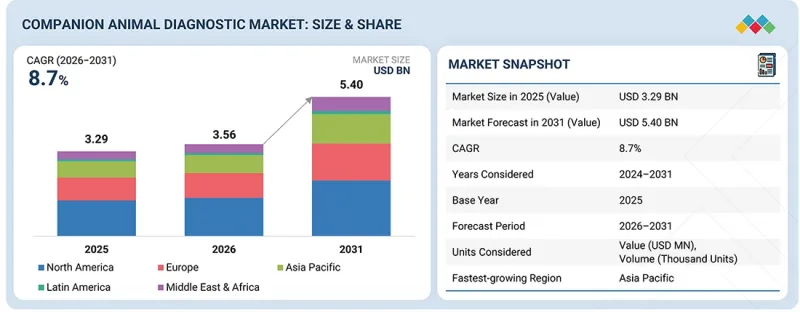

반려동물 진단 시장 규모는 2026년 35억 6,000만 달러에서 2031년까지 54억 달러로 성장하여 CAGR은 8.7%를 나타낼 것으로 예측됩니다.

이러한 성장은 진단 기술, 예방 의료, 그리고 정밀 수의학의 미래를 형성하는 몇 가지 주요 요인에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 기술별, 용도별, 동물 유형별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

주요 요인으로는 수의학 기관들이 현재의 진단 프로세스의 정확성, 속도, 효율성을 높이기 위해 노력하는 가운데, 고도화된 진단 플랫폼에 대한 수요가 증가하고 있다는 점을 들 수 있습니다. 반려동물 의료 분야에서 표적화된 데이터 중심 접근법에 대한 수요가 높아짐에 따라, 고품질 진단 플랫폼에 대한 수요도 증가하고 있습니다. 또한, 예방 의료 및 표적화된 질병 관리로의 전환 필요성은 혁신적인 진단 플랫폼에 대한 수요 증가에 힘입어 더욱 부각되고 있습니다. 이러한 추세는 AI를 활용한 데이터 분석과 클라우드 서비스로 인해 더욱 강화되고 있으며, 그 결과 GMP 기준을 준수하는 혁신적인 진단 플랫폼에 대한 수요가 발생하고 있습니다.

또한, 반려동물의 만성 질환, 감염증, 노화에 따른 질환의 발생률 증가로 인해 신속하고 효율적인 진단 수단에 대한 수요가 높아지고 있습니다. 수의사 및 수의학 검사실은 계속 증가하는 진료 건수에 대응하기 위해 고처리량 검사, 분자 검사 및 영상 진단 기능을 통해 전문 진단 기업의 지원을 점점 더 필요로 하고 있습니다. 실시간 모니터링 도구, 인공지능을 활용한 예측 분석, 그리고 클라우드 기반 시스템을 통해 추진되는 수의학 분야의 현대화 흐름 또한 새롭고 고품질의 진단 서비스에 대한 필요성을 뒷받침하고 있습니다.

자동 분석 장치, 현장 진단(POCT), AI 기반 판정 등의 기술 발전은 검사의 정확도와 결과 보고까지 걸리는 시간을 단축하고, 반려동물 분야에서 활용 가능한 검사 항목을 확대함으로써 시장을 주도하고 있습니다. 반려동물 진단 분야에서 복잡한 동물 진단 및 동물 조사에 대한 전문 지식의 아웃소싱이 증가함에 따라, 이러한 발전은 반려동물 진단 시장의 지속적인 진화에도 기여하고 있습니다.

“기술별로는 예측 기간 동안 분자진단 부문이 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. '

분자진단 부문은 반려동물의 감염성 질환, 유전성 질환 및 암에 대해 정확한 결과를 제공할 수 있어, 반려동물 진단 시장에서 가장 높은 성장세가 예상됩니다. PCR, 차세대 염기서열 분석 및 액체 생검 기술의 발전으로 분자진단 활용이 확대됨에 따라, 수의사들은 이전에는 진단이 어려웠던 복잡한 질환에 대해서도 환자를 손쉽게 검사할 수 있게 되었습니다. 또한, 반려동물에게 맞춤형 치료 계획을 제공하기 위해서는 정밀한 진단법이 필요하기 때문에 정밀 의학에 대한 수요가 높아지고 있습니다.

“제품별로는 2025년에 소모품 부문이 더 큰 시장 점유율을 차지했습니다.” '

2025년, 반려동물 진단 시장에서 소모품 부문이 주도적인 위치를 차지했습니다. 이는 시약, 검사 키트, 진단 스트립이 수의학 검사실이나 동물 의료 센터에서 수행되는 대부분의 검사에서 필수적인 구성 요소이기 때문입니다. 이러한 소모품은 혈액 검사나 소변 검사 등 반려동물에게 일상적으로 시행되는 검사에 사용됩니다. 또한 반려동물 업계에서는 현장 검사나 병원 내 검사가 널리 보급되어 있으며, 이러한 소모품들은 일상적으로 사용되고 있습니다. 또한, 동물 검사에 대한 수요가 증가하고 동물 병원이 예방적 검사로 전환함에 따라 소모품에 대한 수요가 늘어날 것이며, 그 결과 해당 시장에서 지배적인 입지를 유지하게 될 것입니다.

“예측 기간 동안 아시아태평양이 가장 높은 성장률을 나타낼 것으로 전망됩니다. '

아시아태평양은 반려동물에 막대한 비용을 지출하는 애호가들 증가에 힘입어, 예측 기간 동안 반려동물 진단 시장에서 가장 빠른 성장세를 보일 것으로 예측됩니다. 동물 건강에 대한 인식이 높아지고 반려동물 주인들의 구매력이 향상됨에 따라, 아시아태평양 시장은 급속히 성장하고 있습니다. 현장 검사 및 분자진단과 같은 첨단 동물용 진단 기기의 활용이 확대됨에 따라, 합리적인 가격으로 고품질의 진단을 받고자 하는 수요가 충족되고 있습니다. 또한, 동물 의료 인프라의 확충과 동물 보험의 보급이 확대되고 있는 점도 아시아태평양의 동물용 진단 시장을 견인하고 있습니다.

조사 범위

본 시장 조사는 반려동물 진단 시장의 다양한 부문을 대상으로 합니다. 제품, 기술, 용도, 동물 종, 최종 사용자, 지역별로 시장 규모 및 성장 가능성을 추정하는 것을 목적으로 합니다. 또한, 본 조사에는 시장의 주요 업체에 대한 상세한 경쟁 분석 외에도 각 기업프로파일, 제품 및 사업 내용에 대한 주요 분석 결과, 최근 동향, 주요 시장 전략도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유

본 보고서는 기존 기업 및 신생·중소기업이 시장 동향을 파악하고 시장 점유율을 확대하는 데 도움이 됩니다. 본 보고서를 입수한 기업은 아래에 개요를 제시한 5가지 전략 중 하나 이상을 실행할 수 있습니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(반려동물 증가, 반려동물 보험에 대한 수요 증가, 동물 의료비 지출 증가), 제약 요인(진단 장비의 높은 비용, 진단 제품에 대한 엄격한 규제 및 긴 승인 절차), 기회(POC(현장) 진단을 위한 신속 검사 및 휴대용 기기에 대한 수요 증가, 질병 진단의 고도화를 위한 AI 및 ML 통합), 그리고 과제(신흥 시장의 수의사 부족, 소규모 클리닉에서의 도입 장벽)에 대해 분석하여 반려동물 진단 시장의 성장에 영향을 미치는 요인을 밝힙니다.

- 제품 개발/혁신 : 반려동물 진단 시장의 향후 기술 동향 및 신제품 출시와 관련된 상세한 인사이트.

- 시장 개발: 수익성이 높은 신흥 시장에 대한 종합적인 정보. 본 보고서에서는 지역별로 다양한 유형의 반려동물 진단 제품 시장을 분석했습니다.

- 시장의 다각화 : 반려동물 진단 시장의 제품, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보.

- 경쟁사 분석 : 반려동물 진단 시장의 주요 기업들 시장 점유율, 전략, 제품, 유통망, 생산 능력에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성 이니셔티브

제8장 고객 현황과 구매 행동

제9장 반려동물 진단 시장(제품별)

제10장 반려동물 진단 시장(기술별)

제11장 반려동물 진단 시장(용도별)

제12장 반려동물 진단 시장(동물 유형별)

제13장 반려동물 진단 시장(최종사용자별)

제14장 반려동물 진단 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSH 26.06.23The companion animal diagnostics market is expected to grow from USD 3.56 billion in 2026 to USD 5.40 billion by 2031, at a CAGR of 8.7%. This growth is driven by several key factors shaping the future of diagnostic technology, preventive care, and precision veterinary medicine.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Product, Technology, Application, Animal Type, End User, Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

A key catalyst is the growing need for sophisticated diagnostic platforms as veterinary healthcare organizations seek to improve the accuracy, speed, and efficiency of current diagnostic processes. With the increasing need for a targeted, data-focused approach in companion animal healthcare, demand for high-quality diagnostic platforms is rising. Moreover, the need to shift focus to preventive healthcare and targeted disease management is being fueled by the growing demand for innovative diagnostic platforms. This trend is being augmented by AI-driven data analysis and cloud services, resulting in demand for innovative GMP-compliant diagnostic platforms.

Furthermore, the increasing incidence of chronic, infectious, and age-related diseases in domesticated pets is fueling the need for rapid, efficient diagnostic options. Veterinarians and veterinary labs are increasingly seeking support from specialty diagnostic companies to meet the ever-rising volume of cases through high-throughput testing, molecular testing, and imaging capabilities. The growing momentum toward modernizing the field of vet care, driven by real-time monitoring tools, artificial intelligence-powered predictive analytics, and cloud-based systems, is also fueling the need for new, high-quality diagnostic services.

Advances in technology, including automated analyzers, point-of-care testing, and AI interpretation, are fueling the market by improving test accuracy and turnaround times and expanding testing available in the companion animal space. With more of the companion animal diagnostics space outsourcing expertise in complex animal diagnoses or animal research, these advances also support the continued evolution of the companion animal diagnostics market.

"By technology, molecular diagnostics segment to register the highest CAGR during forecast period."

The molecular diagnostics segment is expected to see the highest growth in the companion animal diagnostics market due to its ability to deliver accurate results for infectious diseases, genetic disorders, and cancers in pet animals. Improvements in PCR, next-generation sequencing, and liquid biopsy have increased the use of molecular diagnostics, enabling veterinarians to easily test their patients for complex ailments that were previously hard to identify. Additionally, there is a growing need for precision medicine, which requires precise diagnostic methods to provide tailored treatment plans for pets.

"By product, consumables segment accounted for larger market share in 2025."

In 2025, the consumables segment dominated the companion animal diagnostics market, as reagents, test kits, and diagnostic strips are indispensable components of most tests performed in veterinary labs and animal health centers. Those consumables are used in everyday tests conducted for companion animals, including blood and urinalysis tests. Point-of-care and in-house testing are also widely adopted in the companion animal industry, and these consumables are used on a day-to-day basis. Furthermore, as the need to test animals increases and vet practices move toward preventive testing, there will be a growing demand for consumables, thereby maintaining their dominant market position.

"Asia Pacific to witness highest growth rate during forecast period."

The Asia Pacific region is expected to witness the fastest growth in the companion animal diagnostics market during the forecast period, driven by the growing number of pet lovers who are spending heavily on their pets. With greater awareness of animal health and higher spending capacity among pet owners, the Asia Pacific market is growing rapidly. The increased use of advanced animal diagnostic equipment, such as point-of-care testing and molecular diagnostics, is meeting the need for high-quality diagnostics at affordable prices. Moreover, advances in animal healthcare infrastructure and animal insurance coverage are driving the animal diagnostics market in the Asia Pacific region.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (45%), Europe (15%), Asia Pacific (25%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By End User: Diagnostic Laboratories (45%), Veterinary Hospitals & Clinics (30%), Veterinary Research Institutes & Universities (15%), and Home Care Settings (10%)

By Designation: Veterinary Clinicians (47%), Diagnostic Laboratory Directors/Managers (22%), R&D Directors/Product Development Heads (15%), and Others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the companion animal diagnostics market in various segments. It aims to estimate the market size and growth potential by product, technology, application, animal type, end user, and region. The study also includes an in-depth competitive analysis of the market's key players, along with their company profiles, key observations on their products and business offerings, recent developments, and key market strategies.

Reasons to Buy Report

The report can assist established companies and newer or smaller firms in understanding market trends, enabling them to capture a larger share of the market. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (growth in the companion animal population, rising demand for pet insurance, and increased spending on animal healthcare), restraints (high cost of diagnostic devices, stringent regulations and lengthy approval processes for diagnostic products), opportunities (growing demand for rapid tests and portable instruments for POC diagnostics, integration of AI and ML for enhanced disease diagnosis), and challenges (shortage of veterinary practitioners in emerging markets, barriers to adoption in small clinics) influencing the growth of the companion animal diagnostics market.

- Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the companion animal diagnostics market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of companion animal diagnostic products across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the companion animal diagnostics market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the companion animal diagnostics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN COMPANION ANIMAL DIAGNOSTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 COMPANION ANIMAL DIAGNOSTICS MARKET OVERVIEW

- 3.2 ASIA PACIFIC: COMPANION ANIMAL DIAGNOSTICS MARKET, BY PRODUCT & COUNTRY (2025)

- 3.3 COMPANION ANIMAL DIAGNOSTICS MARKET: REGIONAL MIX

- 3.4 COMPANION ANIMAL DIAGNOSTICS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.5 COMPANION ANIMAL DIAGNOSTICS MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in companion animal population

- 4.2.1.2 Increasing demand for pet insurance and growth in animal healthcare expenditure

- 4.2.1.3 Growing number of veterinary practitioners

- 4.2.1.4 Increasing prevalence of infectious, parasitic, and chronic diseases in pets

- 4.2.2 RESTRAINTS

- 4.2.2.1 Rising pet care costs

- 4.2.2.2 Limited access to advanced veterinary diagnostic services in developing regions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for rapid tests and portable instruments for POC diagnostics

- 4.2.3.2 Utilization of AI and ML for enhanced disease diagnosis

- 4.2.4 CHALLENGES

- 4.2.4.1 Low awareness regarding preventive diagnostics among pet owners in price-sensitive markets

- 4.2.4.2 Regulatory and reimbursement limitations in veterinary healthcare diagnostics

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN COMPANION ANIMAL DIAGNOSTICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ANIMAL HEALTH INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY KEY PLAYER, 2023-2025

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION, 2023-2025

- 5.5.2.1 Average selling price trend of rapid test kits, by region, 2023-2025

- 5.5.2.2 Average selling price trend of ELISA/immunodiagnostic test kits & reagents, by region, 2023-2025

- 5.5.2.3 Average selling price trend of clinical chemistry reagents, clips & cartridges, by region, 2023-2025

- 5.5.2.4 Average selling price trend of blood glucose strips, by region, 2023-2025

- 5.5.2.5 Average selling price trend of hematology analyzers, by region, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 TRADE DATA FOR HS CODE 9018

- 5.6.1.1 Import data for HS Code 9018

- 5.6.1.2 Export data for HS Code 9018

- 5.6.2 TRADE DATA FOR HS CODE 3822

- 5.6.2.1 Import data for HS Code 3822

- 5.6.2.2 Export data for HS Code 3822

- 5.6.1 TRADE DATA FOR HS CODE 9018

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 5.10.1 NGS-BASED LIQUID BIOPSY FOR CANINE CANCER DETECTION

- 5.10.2 ADOPTION OF AI-ENABLED POC DIAGNOSTIC PLATFORM FOR PARASITE DETECTION

- 5.10.3 DEVELOPMENT OF SNAP 4DX PLUS TEST FOR RAPID VECTOR-BORNE DISEASE DETECTION

- 5.11 IMPACT OF US TARIFFS-COMPANION ANIMAL DIAGNOSTICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Veterinary Hospitals & Clinics

- 5.11.5.2 Veterinary Reference Laboratories

- 5.11.5.3 Veterinary Research Institutes & Universities

- 5.11.5.4 Home Care Settings

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI-ENABLED DIAGNOSTICS

- 6.1.2 PORTABLE INSTRUMENTS FOR POC DIAGNOSTIC SERVICES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MICROFLUIDIC DEVICES FOR VETERINARY DIAGNOSTICS

- 6.2.2 CRISPR-BASED MOLECULAR DIAGNOSTICS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 WEARABLE BIOSENSORS & REMOTE MONITORING DEVICES

- 6.3.2 BREATH & SALIVA-BASED DIAGNOSTIC TOOLS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 NEAR TERM (2025-2027)

- 6.4.2 MID-TERM (2028-2030)

- 6.4.3 LONG TERM (2030+)

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR COMPANION ANIMAL DIAGNOSTIC KITS

- 6.5.2 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE DIAGNOSTICS

- 6.6.2 FULLY INTEGRATED DIGITAL VETERINARY ECOSYSTEMS

- 6.6.3 PRECISION & PERSONALIZED VETERINARY DIAGNOSTICS

- 6.6.4 REMOTE & HOME-BASED PET HEALTH MONITORING

- 6.6.5 AUTOMATED HIGH-THROUGHPUT VETERINARY LABORATORIES

- 6.7 IMPACT OF AI/GENERATIVE AI ON COMPANION ANIMAL DIAGNOSTICS MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL IN COMPANION ANIMAL DIAGNOSTIC ECOSYSTEM

- 6.7.3 AI USE CASES

- 6.7.4 KEY COMPANIES IMPLEMENTING AI IN COMPANION ANIMAL DIAGNOSTICS MARKET

7 REGULATORY LANDSCAPE & SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 Rest of the world

- 7.1.2 INDUSTRY STANDARDS

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 RECYCLED AND ECO-FRIENDLY MATERIALS FOR COMPANION ANIMAL DIAGNOSTIC PRODUCTS

- 7.2.2 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.2.1 DECISION-MAKING PROCESS

- 8.2.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.2.3 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.2.4 MARKET PROFITABILITY

9 COMPANION ANIMAL DIAGNOSTICS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 RECURRING NATURE TO BOOST DEMAND

- 9.3 INSTRUMENTS

- 9.3.1 INCREASING DEMAND FOR POC ANALYZERS TO DRIVE MARKET

10 COMPANION ANIMAL DIAGNOSTICS MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 IMMUNODIAGNOSTICS

- 10.2.1 LATERAL FLOW ASSAYS

- 10.2.1.1 Rapid tests

- 10.2.1.1.1 Growing prevalence of infectious diseases in pets to fuel demand

- 10.2.1.1.2 Global volume analysis of rapid tests, 2024-2031 (thousand units)

- 10.2.1.2 Strip readers

- 10.2.1.2.1 Advancements in digital and AI-enabled diagnostics to support adoption

- 10.2.1.2.2 Global volume analysis of strip readers, 2024-2031 (thousand units)

- 10.2.1.1 Rapid tests

- 10.2.2 ELISA TESTS

- 10.2.2.1 Higher sensitivity and specificity of ELISA testing to support market expansion

- 10.2.3 ALLERGEN-SPECIFIC IMMUNODIAGNOSTIC TESTS

- 10.2.3.1 Rising incidence of allergies and dermatological conditions to fuel market growth

- 10.2.4 IMMUNOASSAY ANALYZERS

- 10.2.4.1 Increasing automation in veterinary diagnostics to drive market growth

- 10.2.5 RADIOIMMUNOASSAYS

- 10.2.5.1 Growing demand for sensitive hormone and endocrine testing to fuel market

- 10.2.6 OTHER IMMUNODIAGNOSTICS PRODUCTS

- 10.2.1 LATERAL FLOW ASSAYS

- 10.3 CLINICAL BIOCHEMISTRY

- 10.3.1 CLINICAL CHEMISTRY ANALYSIS

- 10.3.1.1 Clinical chemistry reagents, clips, and cartridges

- 10.3.1.1.1 Increasing utilization of consumable-based diagnostic workflows to fuel market

- 10.3.1.1.2 Global volume analysis of clinical chemistry reagents, clips, and cartridges, 2024-2031 (thousand units)

- 10.3.1.2 Clinical chemistry analyzers

- 10.3.1.2.1 Growing adoption of in-house veterinary diagnostics to drive analyzer demand

- 10.3.1.2.2 Global volume analysis of clinical chemistry analyzers, 2024-2031 (thousand units)

- 10.3.1.1 Clinical chemistry reagents, clips, and cartridges

- 10.3.2 BLOOD GAS & ELECTROLYTE ANALYSIS

- 10.3.2.1 Blood gas and electrolyte reagents, clips, and cartridges

- 10.3.2.1.1 Rising demand for rapid point-of-care consumables to boost market

- 10.3.2.1.2 Global volume analysis of blood gas & electrolyte reagents, clips, and cartridges, 2024-2031 (thousand units)

- 10.3.2.2 Blood gas & electrolyte analyzers

- 10.3.2.2.1 Increasing adoption of compact critical-care analyzers in veterinary clinics to drive market

- 10.3.2.2.2 Global volume analysis of blood gas & electrolyte analyzers, 2024-2031 (thousand units)

- 10.3.2.1 Blood gas and electrolyte reagents, clips, and cartridges

- 10.3.3 GLUCOSE MONITORING

- 10.3.3.1 Blood glucose strips

- 10.3.3.1.1 Increasing home-based diabetes management to fuel market

- 10.3.3.1.2 Global volume analysis of blood glucose strips, 2024-2031 (thousand units)

- 10.3.3.2 Glucose monitors

- 10.3.3.2.1 Advancements in portable and continuous glucose monitoring technologies to drive market growth

- 10.3.3.2.2 Global volume analysis of glucose monitors, 2024-2031 (thousand units)

- 10.3.3.3 Urine glucose strips

- 10.3.3.3.1 Cost-effective and non-invasive diabetes screening to propel market

- 10.3.3.3.2 Global volume analysis of urine glucose strips, 2024-2031 (thousand units)

- 10.3.3.1 Blood glucose strips

- 10.3.1 CLINICAL CHEMISTRY ANALYSIS

- 10.4 MOLECULAR DIAGNOSTICS

- 10.4.1 PCR TESTS

- 10.4.1.1 Increasing prevalence of infectious diseases in companion animals to support growth

- 10.4.2 MICROARRAYS

- 10.4.2.1 Growing focus on genomic profiling and multiplex testing to drive market

- 10.4.3 NUCLEIC ACID SEQUENCING

- 10.4.3.1 Expanding applications of genomic analysis in veterinary medicine to drive demand

- 10.4.4 OTHER MOLECULAR DIAGNOSTICS PRODUCTS

- 10.4.1 PCR TESTS

- 10.5 URINALYSIS

- 10.5.1 URINALYSIS CLIPS & CARTRIDGES

- 10.5.1.1 Growing use of consumable-based urine testing workflows to drive growth

- 10.5.2 URINE ANALYZERS

- 10.5.2.1 Increasing automation in veterinary urinalysis testing to support market growth

- 10.5.3 URINE TEST STRIPS

- 10.5.3.1 Rising demand for rapid and cost-effective urine screening tests to drive market

- 10.5.1 URINALYSIS CLIPS & CARTRIDGES

- 10.6 HEMATOLOGY

- 10.6.1 HEMATOLOGY CARTRIDGES

- 10.6.1.1 Rising use of disposable consumables in automated hematology workflows to fuel demand

- 10.6.2 HEMATOLOGY ANALYZERS

- 10.6.2.1 Growing demand for rapid complete blood count testing to support market growth

- 10.6.1 HEMATOLOGY CARTRIDGES

- 10.7 OTHER TECHNOLOGIES

11 COMPANION ANIMAL DIAGNOSTICS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 CLINICAL PATHOLOGY

- 11.2.1 INCREASING PREVENTIVE HEALTH SCREENING AND CHRONIC DISEASE MONITORING DRIVES DEMAND

- 11.3 BACTERIOLOGY

- 11.3.1 RISING BACTERIAL INFECTIONS AND ANTIMICROBIAL RESISTANCE CONCERNS BOOST MARKET GROWTH

- 11.4 VIROLOGY

- 11.4.1 GROWING PREVALENCE OF COMPANION ANIMAL VIRAL DISEASES DRIVES GROWTH

- 11.5 PARASITOLOGY

- 11.5.1 INCREASING PARASITIC AND VECTOR-BORNE DISEASE BURDEN SUPPORTS DIAGNOSTIC ADOPTION

- 11.6 OTHER APPLICATIONS

12 COMPANION ANIMAL DIAGNOSTICS MARKET, BY ANIMAL TYPE

- 12.1 INTRODUCTION

- 12.2 DOGS

- 12.2.1 RISING PREVALENCE OF CANINE CHRONIC AND VECTOR-BORNE DISEASES DRIVES DIAGNOSTIC DEMAND

- 12.3 CATS

- 12.3.1 GROWING AWARENESS OF FELINE INFECTIOUS AND KIDNEY DISEASES BOOSTS MARKET GROWTH

- 12.4 HORSE

- 12.4.1 INCREASING EQUINE HEALTH MONITORING SUPPORTS DIAGNOSTIC ADOPTION

- 12.5 OTHER COMPANION ANIMALS

13 COMPANION ANIMAL DIAGNOSTICS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 VETERINARY HOSPITALS & CLINICS

- 13.2.1 EXPANDING ADOPTION OF IN-HOUSE POINT-OF-CARE DIAGNOSTIC SOLUTIONS TO DRIVE MARKET

- 13.3 VETERINARY REFERENCE LABORATORIES

- 13.3.1 RISING DEMAND FOR SPECIALIZED AND HIGH-COMPLEXITY VETERINARY DIAGNOSTIC TESTING TO PROPEL MARKET

- 13.4 VETERINARY RESEARCH INSTITUTES & UNIVERSITIES

- 13.4.1 INCREASING RESEARCH FOCUS ON PRECISION AND MOLECULAR VETERINARY DIAGNOSTICS TO SUPPORT GROWTH

- 13.5 HOME CARE SETTINGS

- 13.5.1 GROWING ADOPTION OF AT-HOME PET HEALTH MONITORING AND DIAGNOSTIC TECHNOLOGIES TO BOOST DEMAND

14 COMPANION ANIMAL DIAGNOSTICS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 14.2.2 NORTH AMERICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 14.2.3 US

- 14.2.3.1 Rising preventive pet healthcare spending to drive market

- 14.2.4 CANADA

- 14.2.4.1 Increasing veterinary visits and growing pet population to drive market

- 14.3 EUROPE

- 14.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 14.3.2 EUROPE: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 14.3.3 GERMANY

- 14.3.3.1 Large companion animal population and premium veterinary care fuel market growth

- 14.3.4 UK

- 14.3.4.1 High veterinary expenditure and rising chronic pet diseases support diagnostics demand

- 14.3.5 FRANCE

- 14.3.5.1 Willingness of pet owners to spend on pet health to drive market

- 14.3.6 ITALY

- 14.3.6.1 Expansion of veterinary services supports market growth

- 14.3.7 SPAIN

- 14.3.7.1 Growing pet care economy and animal welfare initiatives to fuel market

- 14.3.8 NETHERLANDS

- 14.3.8.1 Developments in veterinary diagnostic products to support market growth

- 14.3.9 SWEDEN

- 14.3.9.1 Growing companion animal care and advanced veterinary infrastructure supporting market growth

- 14.3.10 POLAND

- 14.3.10.1 Expanding veterinary infrastructure and rising pet ownership support market development

- 14.3.11 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 14.4.2 ASIA PACIFIC: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 14.4.3 CHINA

- 14.4.3.1 Growing urban pet population and rising adoption of pet insurance to propel market

- 14.4.4 JAPAN

- 14.4.4.1 Aging pet population and premium veterinary care to support market growth

- 14.4.5 INDIA

- 14.4.5.1 Expanding pet care industry and rising preventive healthcare awareness fuel market growth

- 14.4.6 AUSTRALIA

- 14.4.6.1 High veterinary expenditure and strong pet insurance penetration to support market growth

- 14.4.7 SOUTH KOREA

- 14.4.7.1 Digital veterinary healthcare expansion to drive market

- 14.4.8 THAILAND

- 14.4.8.1 Urban pet adoption and improving veterinary infrastructure to drive market

- 14.4.9 NEW ZEALAND

- 14.4.9.1 Strong animal welfare culture and preventive care trends support market expansion

- 14.4.10 REST OF ASIA PACIFIC

- 14.5 LATIN AMERICA

- 14.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 14.5.2 LATIN AMERICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 14.5.3 BRAZIL

- 14.5.3.1 Massive companion animal population to boost demand

- 14.5.4 MEXICO

- 14.5.4.1 High pet ownership and expanding veterinary services to support market growth

- 14.5.5 ARGENTINA

- 14.5.5.1 Strong pet humanization and preventive healthcare trends support market growth

- 14.5.6 REST OF LATIN AMERICA

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 14.6.2 MIDDLE EAST & AFRICA: VOLUME ANALYSIS, BY PRODUCT, 2024-2031

- 14.6.3 GCC COUNTRIES

- 14.6.3.1 Kingdom of Saudi Arabia (KSA)

- 14.6.3.1.1 Government initiatives to drive market growth

- 14.6.3.2 United Arab Emirates (UAE)

- 14.6.3.2.1 Premium veterinary services and rising pet ownership to drive market

- 14.6.3.3 Rest of GCC Countries

- 14.6.3.1 Kingdom of Saudi Arabia (KSA)

- 14.6.4 REST OF MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.4.1 RANKING OF KEY MARKET PLAYERS

- 15.4.2 US MARKET SHARE ANALYSIS, 2025

- 15.4.3 EUROPE MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Product footprint

- 15.5.5.4 Technology footprint

- 15.5.5.5 Animal type footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of key startups

- 15.7 BRAND/PRODUCT COMPARISON

- 15.8 R&D EXPENDITURE OF KEY PLAYERS

- 15.9 COMPANY VALUATION & FINANCIAL METRICS

- 15.9.1 FINANCIAL METRICS

- 15.9.2 COMPANY VALUATION

- 15.10 COMPETITIVE SCENARIO

- 15.10.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 15.10.2 DEALS

- 15.10.3 EXPANSIONS

- 15.10.4 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 IDEXX LABORATORIES, INC.

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches & enhancements

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 ANTECH DIAGNOSTICS, INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches & approvals

- 16.1.2.3.2 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses & competitive threats

- 16.1.3 ZOETIS SERVICES LLC

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches & enhancements

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.3.4 Other developments

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses & competitive threats

- 16.1.4 FUJIFILM CORPORATION

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 MnM view

- 16.1.4.3.1 Key strengths

- 16.1.4.3.2 Strategic choices

- 16.1.4.3.3 Weaknesses & competitive threats

- 16.1.5 THERMO FISHER SCIENTIFIC INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 MnM view

- 16.1.5.3.1 Key strengths

- 16.1.5.3.2 Strategic choices

- 16.1.5.3.3 Weaknesses & competitive threats

- 16.1.6 BIOMERIEUX

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches & approvals

- 16.1.7 BIONOTE

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches & enhancements

- 16.1.7.3.2 Deals

- 16.1.8 VIRBAC

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.8.3.2 Expansions

- 16.1.9 RANDOX LABORATORIES LTD.

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.9.3.2 Expansions

- 16.1.10 INDICAL BIOSCIENCE GMBH

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product enhancements

- 16.1.11 SHENZHEN MINDRAY ANIMAL MEDICAL TECHNOLOGY CO., LTD.

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.11.3.2 Expansions

- 16.1.12 BOULE

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches

- 16.1.12.3.2 Deals

- 16.1.13 INNOVATIVE DIAGNOSTICS

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Other developments

- 16.1.14 MEGACOR DIAGNOSTIK GMBH

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches & enhancements

- 16.1.15 BIOGAL

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.1 IDEXX LABORATORIES, INC.

- 16.2 OTHER PLAYERS

- 16.2.1 GOLD STANDARD DIAGNOSTICS

- 16.2.2 AGROLABO S.P.A.

- 16.2.3 PRECISION BIOSENSOR, INC.

- 16.2.4 SKYLA CORPORATION

- 16.2.5 FASSISI, GMBH

- 16.2.6 WOODLEY EQUIPMENT COMPANY LTD

- 16.2.7 BIOPANDA REAGENTS LTD

- 16.2.8 SKYER, INC.

- 16.2.9 RING BIOTECHNOLOGY CO., LTD.

- 16.2.10 SHENZHEN BIOEASY BIOTECHNOLOGY, INC.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.2 RESEARCH METHODOLOGY DESIGN

- 17.2.1 SECONDARY DATA

- 17.2.1.1 Key data from secondary sources

- 17.2.2 PRIMARY DATA

- 17.2.2.1 Key data from primary sources

- 17.2.2.2 Key industry insights

- 17.2.1 SECONDARY DATA

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 17.5 MARKET SHARE ANALYSIS

- 17.5.1 RESEARCH ASSUMPTIONS

- 17.5.2 GROWTH RATE ASSUMPTIONS

- 17.6 RISK ASSESSMENT

- 17.7 RESEARCH LIMITATIONS

- 17.7.1 METHODOLOGY-RELATED LIMITATIONS

- 17.7.2 SCOPE-RELATED LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.3.1 PRODUCT ANALYSIS

- 18.3.2 COMPANY INFORMATION

- 18.3.3 GEOGRAPHIC ANALYSIS

- 18.3.4 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 18.3.5 COUNTRY-LEVEL VOLUME ANALYSIS BY PRODUCT

- 18.3.6 BY PRODUCT MARKET SHARE ANALYSIS (TOP 5 PLAYERS)

- 18.3.7 ANY CONSULT/CUSTOM REQUIREMENTS AS PER CLIENT REQUESTS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS