|

시장보고서

상품코드

2061393

창 및 도어 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Windows and Doors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

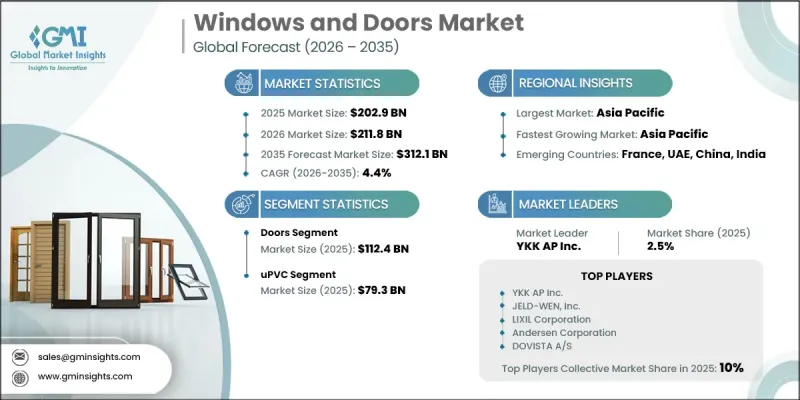

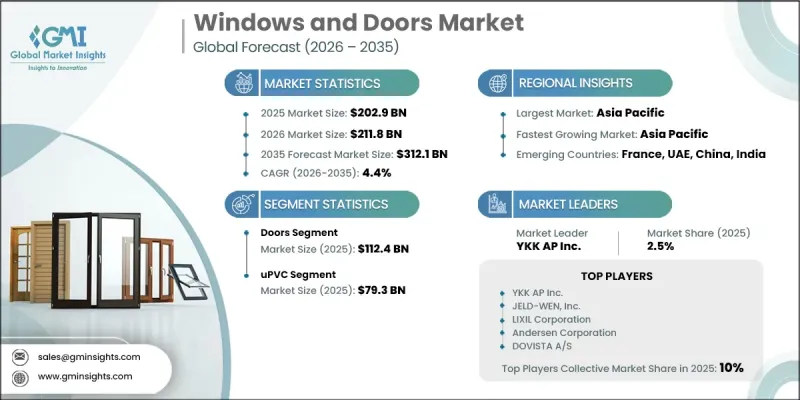

세계의 창·도어 시장은 2025년에 2,029억 달러로 평가되며, 2035년까지 CAGR 4.4%로 성장하며, 3,121억 달러에 달할 것으로 예측됩니다.

시장의 확대는 건축 동향의 진화와 더불어, 주거용·상업용 건축을 불문하고 고성능이면서 미관이 뛰어난 건축자재에 대한 수요 증가에 힘입어 이루어지고 있습니다. 에너지 절약형 건축 외피에 대한 관심이 높아지는 가운데, 첨단 유리, 단열 기술 및 정밀하게 설계된 프레임 시스템의 도입이 확산되고 있습니다. 건설업체 및 도급업체를 포함한 건설 업계 관계자들은 맞춤형 신속 설치 솔루션에 대한 수요 증가에 대응하기 위해 조립식 시설 및 지역 밀착형 생산 거점에 대한 의존도를 높이고 있습니다. 이러한 변화에 따라 대규모 맞춤형 생산을 지원하기 위해 자동 절단 시스템, 로봇 조립 라인 및 CNC 기반 제조 설비에 대한 의존도도 높아지고 있습니다. 생산 현장에서 설치 현장으로의 모듈식 창문·문 시스템의 신속한 납품은 중요한 경쟁 요소로 부상하고 있으며, 첨단 제조와 물류의 통합 역할을 강화하고 있습니다. 또한 저복사율 코팅, 열단절 시스템, 고성능 단열재 등 단열 솔루션에 대한 관심이 높아짐에 따라 업계 전반에서 제품 혁신과 전문 자재에 대한 수요가 더욱 촉진되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 2,029억 달러 |

| 예측액 | 3,121억 달러 |

| CAGR | 4.4% |

2025년, 도어 부문은 1,124억 달러를 차지했습니다. 이러한 우위는 주택, 상업 및 산업 시설의 주요 출입구로서 건물의 기능성에 없어서는 안 될 역할을 수행하고 있다는 점에 기인합니다. 잦은 사용과 지속적인 마모 및 손상에 노출되는 것도 안정적인 교체 수요를 창출하여 해당 부문의 성장을 더욱 지원하고 있습니다. 안전성, 보안, 구조 설계에서 그 중요성은 현대 건축의 핵심 구성 요소로서의 위상을 확고히 하고 있습니다.

2025년, uPVC 부문은 시장에서 주도적인 점유율을 차지하며 793억 달러의 매출을 기록했고, 39.1%의 점유율을 차지했습니다. 이러한 높은 보급률은 비용 효율성, 단열 성능, 그리고 다양한 기후 조건에서의 내구성에 힘입어 이루어지고 있습니다. uPVC 소재의 다중 챔버 구조는 에너지 효율을 높이는 동시에 유지보수 필요성을 줄여주므로, 대규모 주거 및 상업용 건축물에 매우 적합합니다. 대규모 주택 및 공동주택 개발로 인한 수요 확대가 uPVC 창호 시스템의 보급을 지속적으로 지원하고 있습니다.

중국의 창호 시장은 2025년에 50.6%의 점유율을 차지하며, 해당 지역은 2026-2035년 연평균 성장률(CAGR) 5.3%를 기록할 것으로 전망됩니다. 급속한 도시화, 강력한 산업 발전, 그리고 대규모 인프라 확장이 지역 수요를 견인하는 주요 요인이 되고 있습니다. 중국은 강력한 제조 역량과 합리적인 가격의 주택 및 에너지 절약형 건축을 장려하는 정부의 노력에 힘입어, 창문 및 문 제품의 최대 생산국이자 소비국으로서의 위상을 계속해서 유지하고 있습니다. 인도 및 일본 역시 주택 및 상업 인프라 프로젝트에서 전통적 및 현대적 건축 시스템에 대한 수요가 증가함에 따라 지역 성장에 크게 기여하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 창·도어 업계의 동향

제4장 경쟁 구도

제5장 창·도어 시장 : 제품 유형별

제6장 창·도어 시장 : 소재별

제7장 창·도어 시장 : 용도별

제8장 창·도어 시장 : 판매 채널별

제9장 창·도어 시장 : 지역별

제10장 기업 개요

KSA 26.06.24The Global Windows and Doors Market was valued at USD 202.9 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 312.1 billion by 2035.

Market expansion is driven by evolving architectural trends and increasing demand for high-performance, aesthetically advanced building components across residential and commercial construction. The growing emphasis on energy-efficient building envelopes is encouraging wider adoption of advanced glazing, insulation technologies, and precision-engineered frame systems. Construction stakeholders, including builders and contractors, are increasingly relying on prefabrication facilities and localized production units to meet rising demand for customized and quick-installation solutions. This shift is also increasing reliance on automated cutting systems, robotic assembly lines, and CNC-based manufacturing equipment to support large-scale customized production. Faster delivery of modular window and door systems from production sites to installation locations is becoming a key competitive factor, strengthening the role of advanced manufacturing and logistics integration. In addition, rising focus on thermal efficiency solutions such as low-emissivity coatings, thermal break systems, and high-performance insulation materials is further driving product innovation and specialized component demand across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $202.9 Billion |

| Forecast Value | $312.1 Billion |

| CAGR | 4.4% |

The doors segment accounted for USD 112.4 billion in 2025. This dominance is attributed to the essential role doors play in building functionality, serving as primary access points across residential, commercial, and industrial structures. Frequent usage and exposure to continuous wear and tear have also led to consistent replacement demand, further supporting segment growth. Their importance in safety, security, and structural design continues to reinforce their position as a core component of modern construction.

The uPVC segment held a leading share of the market in 2025, generating USD 79.3 billion and accounting for 39.1% share. Its strong adoption is driven by cost efficiency, thermal insulation performance, and durability across varying climatic conditions. The multi-chamber structure of uPVC materials enhances energy efficiency while reducing maintenance requirements, making them highly suitable for large-scale residential and commercial construction. Growing demand from mass housing and multi-unit developments continues to support the widespread use of uPVC-based window and door systems.

China Windows and Doors Market held a 50.6% share in 2025 and the region expected to register a CAGR of 5.3% from 2026 to 2035. Rapid urbanization, strong industrial development, and large-scale infrastructure expansion are key factors driving regional demand. China continues to serve as the largest producer and consumer of fenestration products, supported by strong manufacturing capabilities and government initiatives promoting affordable housing and energy-efficient construction. India and Japan are also contributing significantly to regional growth, with increasing demand for both traditional and modern building systems across residential and commercial infrastructure projects.

Major companies operating in the Global Windows and Doors Industry include JELD-WEN, Inc., LIXIL Corporation, Andersen Corporation, Pella Corporation, DOVISTA A/S, Marvin (The Marvin Companies), YKK AP Inc., SAYYAS Windows Co., Ltd, DCM Shriram Ltd (Fenesta), OPPEIN Home Group Inc., Neuffer Windows + Doors GmbH, TAMCO Gulf Ltd, SGM Windows Manufacturing Limited, Hotian, B.G. Legno, Vinylguard Window & Door Systems Ltd, Century Plyboards (India) Limited, Performance Doorset Solutions Ltd (PDS), Garador Limited, Rogenilan, and Paiya. Companies in the windows and doors market are focusing on advanced manufacturing automation, including CNC machining, robotic assembly, and precision fabrication systems to improve production efficiency and customization capabilities. Many players are expanding prefabrication and modular construction solutions to meet rising demand for faster installation and reduced on-site labor requirements. Strategic investments in energy-efficient product innovations, such as thermal insulation technologies and advanced glazing systems, are strengthening product competitiveness. Firms are also expanding regional manufacturing networks to reduce logistics costs and improve delivery timelines. Partnerships with construction firms and real estate developers are enhancing project integration and supply chain coordination.

Table of Contents

Chapter 1 Methodology And Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022-2035

- 2.2 Key Trends

- 2.3 Product Type

- 2.4 Material

- 2.5 Application

- 2.6 Distribution Channel

Chapter 3 Windows & Doors Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape (raw materials, components, hardware)

- 3.1.2 Manufacturing & fabrication layer

- 3.1.3 Distribution & channel partners

- 3.1.4 Installation & after-sales services

- 3.1.5 Value addition at each stage

- 3.1.6 Profit margin analysis by value chain stage

- 3.2 Supply chain analysis

- 3.2.1 Raw material sourcing dynamics

- 3.2.2 Manufacturing footprint across Europe

- 3.2.3 Distribution network structure

- 3.2.4 Logistics and transportation considerations

- 3.2.5 Supply chain disruptions and risk factors

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising Construction and Urban Development Activities

- 3.3.1.2 Growing Preference for Energy-Efficient Building Solutions

- 3.3.1.3 Increasing Demand for Home Renovation and Upgrades

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Fluctuating Raw Material Costs

- 3.3.2.2 Intense Market Competition and Price Sensitivity

- 3.3.3 Opportunities

- 3.3.3.1 Sustainable & Circular Economy Materials (Recycled uPVC, FSC-Certified Wood)

- 3.3.3.2 Automated & Smart Door/Window Systems for Luxury & Commercial Segments

- 3.3.1 Growth drivers

- 3.4 Technology & innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies (smart windows, electrochromic glass, self-cleaning coatings)

- 3.4.3 Material science advancements

- 3.4.4 Digital manufacturing & automation

- 3.5 Regulatory framework

- 3.5.1 Standards & compliance requirements

- 3.5.2 Regional regulatory frameworks

- 3.5.3 Energy efficiency standards (Energy Star 7.0, EU energy labels)

- 3.5.4 Building codes & safety regulations

- 3.5.5 Certification standards (NFRC, CE marking, ASTM)

- 3.6 Growth potential analysis

- 3.7 Investment & funding analysis

- 3.7.1 M&A activity & consolidation trends

- 3.7.2 Private equity & venture capital investments

- 3.7.3 Strategic investments in smart & sustainable technologies

- 3.7.4 Regional investment hotspots

- 3.8 Pricing analysis (driven by primary research)

- 3.8.1 Historical price trend analysis (2022-2025)

- 3.8.2 Pricing strategy by player type

- 3.8.3 Price variation by material and product type

- 3.8.4 Regional price benchmarking

- 3.8.5 Material cost pass-through dynamics

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Trade data analysis (driven by paid database)

- 3.11.1 Import & export volume & value trends (HS code 392520, 441820, 761010) (driven by primary research)

- 3.11.2 Key trade corridors & tariff impact (driven by primary research)

- 3.11.3 Trade flow analysis by material & product type

- 3.12 Impact of AI and generative AI

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment (design automation, predictive maintenance, demand forecasting)

- 3.12.3 Risks, limitations & regulatory considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Company market share analysis

- 4.1.1 By region

- 4.1.1.1 North America

- 4.1.1.2 Europe

- 4.1.1.3 Asia Pacific

- 4.1.1.4 Latin America

- 4.1.1.5 Middle East & Africa

- 4.1.1 By region

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plan

Chapter 5 Windows & Doors Market, By Product Type (USD Billion) (Million Units)

- 5.1 Window

- 5.1.1 Casement Windows

- 5.1.2 Sliding Windows

- 5.1.3 Double-Hung Windows

- 5.1.4 Awning Windows

- 5.1.5 Fixed Windows

- 5.1.6 Bay & Bow Windows

- 5.1.7 Others

- 5.2 Doors

- 5.2.1 Entry Doors

- 5.2.2 Interior Doors

- 5.2.3 Sliding Doors (Patio Doors)

- 5.2.4 Folding Doors (Bi fold)

- 5.2.5 Revolving Doors

- 5.2.6 Overhead Doors (Garage Doors)

- 5.2.7 Others

Chapter 6 Windows & Doors Market, By Material (USD Billion) (Million Units)

- 6.1 uPVC

- 6.2 Wood

- 6.3 Metal

- 6.4 Others

Chapter 7 Windows & Doors Market, By Application (USD Billion) (Million Units)

- 7.1 Residential

- 7.2 Residential

- 7.2.1 News Construction

- 7.2.2 Improvement & Repair

- 7.3 Commercial

- 7.3.1 News Construction

- 7.3.2 Improvement & Repair

- 7.4 Industrial

- 7.4.1 News Construction

- 7.4.2 Improvement & Repair

Chapter 8 Windows & Doors Market, By Distribution Channel (USD Billion) (Million Units)

- 8.1 Online

- 8.2 Offline

Chapter 9 Windows & Doors Market, By Region

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 Germany

- 9.2.2 UK

- 9.2.3 Italy

- 9.2.4 France

- 9.2.5 Spain

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 Japan

- 9.3.3 India

- 9.3.4 South Korea

- 9.3.5 Australia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 JELD-WEN, Inc.

- 10.1.2 LIXIL Corporation

- 10.1.3 Andersen Corporation

- 10.1.4 Pella Corporation

- 10.1.5 DOVISTA A/S

- 10.1.6 Marvin (The Marvin Companies)

- 10.1.7 SAYYAS Windows Co., Ltd

- 10.2 Regional Champions

- 10.2.1 YKK AP Inc.

- 10.2.2 DCM Shriram Ltd (Fenesta)

- 10.2.3 OPPEIN Home Group Inc.

- 10.2.4 Hotian

- 10.2.5 SGM Windows Manufacturing Limited

- 10.2.6 TAMCO Gulf Ltd

- 10.2.7 Neuffer Windows + Doors GmbH

- 10.3 Niche/Specialist players

- 10.3.1 B.G. Legno

- 10.3.2 Vinylguard Window & Door Systems Ltd

- 10.3.3 Century Plyboards (India) Limited

- 10.3.4 Performance Doorset Solutions Ltd (PDS)

- 10.3.5 Rogenilan

- 10.3.6 Paiya

- 10.3.7 Garador Limited