|

시장보고서

상품코드

2007118

도어 및 창 시장 예측(-2031년) : 제품별, 재료별, 구조 유형별, 용도별, 지역별Doors & Windows Market by Product (Doors and Windows), Material (Wood, Metal, Plastic), Construction Type (Swinging, Sliding, Folding, Revolving), End-use Industry (Residential, Commercial, and Industrial), and Region - Global Forecast To 2031 |

||||||

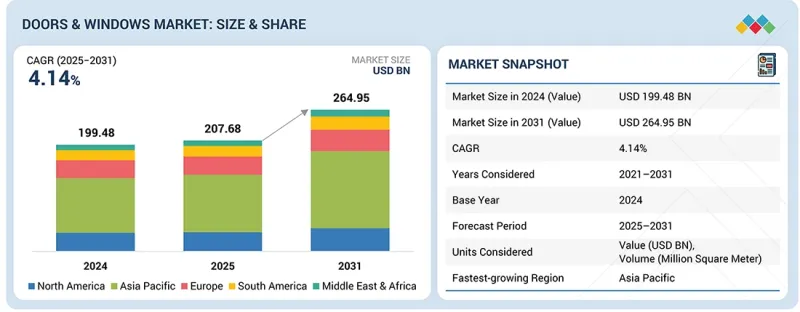

세계의 도어·창 시장 규모는 2025년 2,076억 8,000만 달러에서 2031년까지 2,649억 5,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 4.14%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 10억 달러, 100만 평방미터 |

| 부문 | 재료, 제품, 구조 유형, 최종 용도 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

세계 도어 및 창호 시장은 건설 활동의 활성화와 개보수 비용의 증가로 인해 꾸준히 성장하고 있습니다. 문과 창문은 건물의 필수적인 구성 요소일 뿐만 아니라 디자인에서도 중요한 역할을 합니다. 문과 창문은 통기성과 에너지 절약 측면에서 건물의 성능 향상에 기여합니다. 급속한 도시화, 주택 건설 프로젝트, 에너지 절약 제품에 대한 관심 증가 등이 글로벌 도어 및 창호 시장의 성장을 촉진하는 요인으로 작용하고 있습니다. 주택 소유자와 개발자가 건물의 성능, 단열 및 전반적인 디자인에 점점 더 많은 관심을 기울이면서 신축, 개보수 및 리노베이션 노력이 시장 수요를 크게 늘리고 있습니다. 예를 들어 미국에서는 National Association of Home Builders가 2026년 단독주택 착공 건수가 약 1% 증가한 약 94만 가구에 달하고, 2027년에는 약 5% 증가한 약 98만 4,000가구가 될 것으로 예측하고 있습니다. 협회는 주택 개보수 비용이 2007년 33% 이상에서 2025년 3분기에는 약 45%까지 증가했다고 강조하며, 이는 개보수 공사가 크게 확대되었음을 보여줍니다. 이러한 추세는 정교하고 에너지 절약형이며 내구성이 뛰어난 도어 및 창호 시스템에 대한 글로벌 수요를 더욱 증가시키고 있습니다.

"창호는 예측 기간 중 도어 및 창호 시장에서 가장 빠르게 성장하는 제품이 될 것으로 예상됩니다. "

이러한 성장은 주로 에너지 절약형 건물, 환기 및 자연 채광에 대한 수요 증가에 기인합니다. 현대의 창호 시스템은 단열성이 향상되고, 에너지 소비를 줄이고, 건물의 종합적인 성능을 향상시켜 창호는 에너지 절약과 지속가능한 건설에 필수적인 요소로 자리 잡고 있습니다. 도시 확장에 따라 신축이 증가하고 개보수 및 교체 공사도 증가 추세에 있으며, 첨단 창호 솔루션 부문의 성장이 더욱 가속화되고 있습니다. 또한 창틀에 비닐, 알루미늄, 유리섬유 및 복합재료의 사용이 증가함에 따라 창호 부문의 성장을 촉진하고 있습니다. 또한 에너지 절약형 유리와 스마트 창호 기술이 전 세계 건설 시장에서 창호 부문의 성장을 촉진하고 있습니다.

"슬라이딩 유형은 예측 기간 중 도어 및 창호 시장에서 가장 빠르게 성장하는 구조 유형이 될 것으로 예상됩니다. "

그 주요 원인은 슬라이딩 방식이 현재의 디자인 컨셉과 컴팩트한 공간에 더 적합하다는 점에 있습니다. 슬라이딩 도어와 창문은 수평 레일에 장착되어 개폐를 위한 공간을 필요로 하지 않는 것이 큰 장점입니다. 이들은 도시 주택, 발코니, 파티오, 고층 주택에서 볼 수 있는 컴팩트한 공간에 적합합니다. 또한 대형 유리 패널을 채택할 수 있으므로 더 많은 자연광을 받아들이고 야외를 선명하게 볼 수 있으며, 현대의 주거 및 상업 시설에서 유행하고 있습니다. 또한 슬라이딩 도어와 창문의 재료는 목재에서 알루미늄과 uPVC로 전환되고 있으며, 이중 또는 삼중 유리 패널이 채택되고 있습니다. 건축가들이 실내와 야외를 매끄럽게 연결하면서 현대적인 외관을 만들기 위해 고급 주택, 호텔, 사무실 공간에 다양한 슬라이딩 옵션을 도입한 것도 한 요인으로 작용하고 있습니다.

"플라스틱은 예측 기간 중 도어 및 창호 시장에서 가장 빠르게 성장하는 소재가 될 것으로 예상됩니다. "

이는 주로 주거 및 상업용 건축에서 uPVC 및 기타 폴리머 유래 프레임 시스템의 채택이 증가하고 있기 때문입니다. 플라스틱 프레임은 뛰어난 내구성, 내식성, 유지보수 용이성 및 우수한 단열성을 갖추고 있습니다. 이러한 요인으로 인해 플라스틱 프레임은 에너지 절약형 건축 설계를 실현하기 위한 현명한 선택이 되었습니다. 플라스틱 프레임은 습기, 화학물질, 환경 악화에 대한 저항력이 높아 극한의 기후 조건을 가진 지역에도 적합합니다. 이 소재는 유연한 설계와 비용 효율적인 생산이 가능하므로 신축 및 개보수 프로젝트에서 널리 채택되고 있습니다. 시장에서 지속가능하고 에너지 절약형 소재에 대한 수요가 증가함에 따라 플라스틱 문과 창문은 문과 창문 시장에서 더욱 탄력을 받을 가능성이 높다.

세계의 도어 및 창호 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 채택에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 도어·창 시장 : 제품별

제10장 도어·창 시장 : 구조 유형별

제11장 도어·창 시장 : 재료별

제12장 도어·창 시장 : 용도별

제13장 도어·창 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.04.29The doors & windows market is projected to reach USD 264.95 billion by 2031 from USD 207.68 billion in 2025, at a CAGR of 4.14% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD Billion) and Volume (Million Square Meter) |

| Segments | Material, Product, Construction Type, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The doors & windows market worldwide is growing steadily, driven by increased construction activity and rising renovation expenditure. Doors and windows are not only essential components of a building; they also play a vital role in its design. Doors and windows help improve a building's performance in terms of airflow and energy savings. Rapid urbanization, housing projects, and an increased emphasis on energy-efficient products are among the factors driving global growth in the doors and windows market. New construction, rehabilitation, and remodeling initiatives are substantially driving market demand, as homeowners and developers increasingly prioritize building performance, insulation, and overall design. For instance, in the US, the National Association of Home Builders projects that single-family housing starts will increase by about 1% in 2026, reaching approximately 940,000 units, and further grow by around 5% in 2027 to nearly 984,000 units. The group emphasizes that home improvement expenditures have increased from over 33% in 2007 to about 45% by the third quarter of 2025, signifying significant growth in renovation efforts. These trends continue to augment the global need for sophisticated, energy-efficient, and resilient door and window systems.

"Windows are projected to be the fastest-growing product in the doors & windows market during the forecast period."

Windows are projected to be the fastest-growing product segment in the doors & windows market during the forecast period. This growth is mainly due to increased demand for energy-efficient buildings, ventilation, and natural light. Modern window systems have improved thermal insulation, reduced energy consumption, and improved overall building performance, making windows an essential part of energy-efficient and sustainable construction. As cities expand, new construction is rising, and renovation and replacement activities are on the rise, thus propelling growth in the advanced window solutions segment at an even faster rate. Furthermore, an increase in the use of vinyl, aluminum, fiberglass, and composite materials in window frames is also propelling growth in the windows segment. Moreover, energy-efficient glazing and smart window technologies are driving growth in the windows segment across construction markets worldwide.

"Sliding is projected to be the fastest-growing construction type in the doors & markets market during the forecast period."

Sliding is projected to be the fastest-growing construction type in the doors & windows market during the forecast period. The major contributing factor is that it aligns better with current design concepts and compact spaces. The fact that sliding doors and windows are mounted on horizontal rails, requiring no clearance for swinging, is a major advantage. They are best suited for compact spaces found in urban homes, balconies, patios, and residential skyscrapers. They can support large glazed materials that allow for more natural light and provide a clear view of the outdoors, a trend becoming more popular in modern homes and commercial structures. In addition, there is a shift from wooden to aluminum and uPVC for sliding doors and windows, with double- or triple-glazed panels. The fact that architects are incorporating various sliding options into luxury homes, hotels, and office spaces to provide a seamless flow from indoors to outdoors while creating a modern look is also a contributing factor.

"Plastics are projected to be the fastest-growing material in the doors & windows market during the forecast period."

Plastics are projected to be the fastest-growing material segment in the doors & windows market during the forecast period, mainly due to the increasing adoption of uPVC and other polymer-based frame systems in residential and commercial construction. Plastic-based frames exhibit exceptional durability, corrosion resistance, ease of maintenance, and superior thermal insulation. These factors make plastic frames a wise choice for implementing energy-saving architectural designs. Plastic frames are highly resistant to moisture, chemicals, and environmental degradation, rendering them appropriate for regions with extreme climatic conditions. The material enables adaptable designs and cost-effective production, promoting widespread adoption in both new construction and renovation projects. With the increasing demand for sustainable and energy-saving materials in the market, plastic doors and windows are likely to gain momentum in the doors & windows market.

"Residential is projected to be the fastest-growing end-use industry in the doors & windows market during the forecast period."

The residential sector is projected to be the fastest-growing end-use industry in the doors & windows market during the forecast period, driven by rising housing construction, rapid urbanization, and a surge in global home renovation activity. The increasing demand for single-family homes, apartments, and multi-family housing complexes is substantially enhancing the installation of doors and windows in new residential projects. Moreover, homeowners are increasingly allocating resources to remodeling and replacement initiatives to enhance energy efficiency, security, and overall appeal. Contemporary residential structures are incorporating sophisticated door and window systems that offer enhanced thermal insulation, sound attenuation, and weather resistance. The growing trend towards expansive windows, sliding doors, and energy-efficient glazing solutions is further driving demand.

"Asia Pacific is projected to be the fastest-growing region in the doors & windows market during the forecast period."

Asia Pacific is projected to be the fastest-growing region in the doors & windows market during the forecast period. This is attributed to rapid urbanization, population growth, and massive development initiatives underway. It is recorded that the Asia-Pacific region is experiencing rapid urbanization. The United Nations Development Programme reported that the Asia Pacific region is likely to have a population of 4.84 billion by 2050. Of this figure, 64% are likely to reside in urban areas. This means that housing demand in the region will significantly drive demand for doors and windows. In India and China, massive development initiatives are underway. For instance, in India alone, the population living in urban areas is likely to reach 600 million by 2036. This means demand for doors and windows will increase significantly. The Smart Cities Mission and the Atal Mission for Rejuvenation and Urban Transformation are initiatives by the Indian government to finance the country's development. This move is likely to boost the demand for doors and windows.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Note: Others include sales, marketing, and product managers.

Tier 1: >USD 1 billion; Tier 2: USD 500 million-1 billion; and Tier 3: <USD 500 million.

Companies Covered: ASSA ABLOY (Sweden), LIXIL Corporation (Japan), Cornerstone Building Brands, Inc. (US), JELD-WEN, Inc. (US), YKK AP (Japan), Owens Corning (US), Pella Corporation (US), Schuco International KG (Germany), Andersen Corporation (US), MITER Brands (US), and Marvin (US) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the doors & windows market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the doors & windows market based on material (wood, metal, plastic, and other materials), product (doors and windows), construction type (swinging, sliding, folding, revolving, and other construction types), and end-use industry (residential, commercial, and industrial). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the doors & windows market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the doors & windows market. This report covers a competitive analysis of upcoming startups in the doors & windows market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall doors & windows market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (growth in residential construction activities, rapid urbanization and population growth fuel demand, and growing demand for energy-efficient and sustainable building components), restraints (environmental regulations and compliance pressure on PVC and other materials and high upfront and lifecycle costs of advanced and eco-friendly door & window systems), opportunities (rising demand in emerging economies, increasing demand for high-end residential units and multi-story buildings, integration of smart technologies and sustainable practices, and growing building retrofit and zero-carbon renovation initiatives), and challenges (compliance with evolving environmental regulations and energy efficiency standards and trade tariffs and supply chain disruptions).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the doors & windows market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the doors & windows market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the doors & windows market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as ASSA ABLOY (Sweden), LIXIL Corporation (Japan), Cornerstone Building Brands, Inc. (US), JELD-WEN, Inc. (US), YKK AP (Japan), Owens Corning (US), Pella Corporation (US), Schuco International KG (Germany), Andersen Corporation (US), MITER Brands (US), and Marvin (US), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DOORS & WINDOWS MARKET

- 3.2 ASIA PACIFIC: DOORS & WINDOWS MARKET, BY PRODUCT AND COUNTRY

- 3.3 DOORS & WINDOWS MARKET, BY PRODUCT

- 3.4 DOORS & WINDOWS MARKET, BY MATERIAL

- 3.5 DOORS & WINDOWS MARKET, BY CONSTRUCTION TYPE

- 3.6 DOORS & WINDOWS MARKET, BY END-USE INDUSTRY

- 3.7 DOORS & WINDOWS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in residential construction activities

- 4.2.1.2 Rapid urbanization and population growth

- 4.2.1.3 Growing demand for energy-efficient and sustainable building components

- 4.2.2 RESTRAINTS

- 4.2.2.1 Environmental regulations and compliance pressure on PVC and other materials

- 4.2.2.2 High upfront and lifecycle costs of advanced and eco-friendly door & window systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising demand in emerging economies

- 4.2.3.2 Increasing demand for high-end residential units and multi-story buildings

- 4.2.3.3 Integration of smart technologies and sustainable practices

- 4.2.3.4 Growing building retrofit and zero-carbon renovation initiatives

- 4.2.4 CHALLENGES

- 4.2.4.1 Compliance with evolving environmental regulations and energy efficiency standards

- 4.2.4.2 Trade tariffs and supply chain disruptions

- 4.2.4.3 Intense market competition and price sensitivity

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DOORS & WINDOWS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

- 4.5.1.1 ASSA ABLOY's acquisition of Metal Products Inc.

- 4.5.1.2 Cornerstone Building Brands' acquisition of Metal Sales Manufacturing Corp.

- 4.5.2 TIER 2 PLAYERS: REGIONAL INNOVATORS AND NICHE LEADERS

- 4.5.2.1 Andersen Corporation's expansion of the 100 series with double-hung window option

- 4.5.2.2 Marvin's expansion through a new manufacturing facility in Kansas City

- 4.5.3 TIER 3 PLAYERS: AGILE INNOVATORS AND SPECIALIZED PROVIDERS

- 4.5.3.1 Doma's redefinition of modern doors and smart home integration

- 4.5.3.2 GreenFortune Windows and Doors's USD 4.5 million funding to scale window & door manufacturing

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING CONSOLIDATION AND INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE SELLING PRICE, BY PRODUCT

- 5.5.2 AVERAGE SELLING PRICE, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 392520)

- 5.6.2 IMPORT SCENARIO (HS CODE 392520)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 MODERN ENERGY-EFFICIENT HOME INTEGRATION WITH ADVANCED WINDOW & DOOR SOLUTIONS

- 5.10.2 HERITAGE PROPERTY RESTORATION WITH HIGH-QUALITY TIMBER WINDOW & DOOR SOLUTIONS

- 5.10.3 MICHELLE ADAMS' MODERN MAKEOVER WITH ANDERSEN'S WINDOWS & DOORS

- 5.10.4 INNOVATIVE MULTI-SLIDE VINYL PATIO DOORS IN ORLANDO

- 5.11 IMPACT OF 2025 US TARIFF: DOORS & WINDOWS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Canada

- 5.11.4.3 China

- 5.11.4.4 Europe

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ENERGY-EFFICIENT GLAZING

- 6.1.2 SMART DOORS & WINDOWS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SMART HOME INTEGRATION

- 6.2.2 BUILDING INFORMATION MODELING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 INVISIBLE FRAME DOOR SYSTEMS WITH ULTRA-THIN, SUSTAINABLE PANELS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | PROCESS OPTIMIZATION AND EARLY DIGITAL INTEGRATION

- 6.4.2 MID-TERM (2027-2030) | ADVANCED MATERIAL INNOVATION AND SMART ECOSYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS BUILDING ENVELOPES AND NET-ZERO INNOVATION

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 DOORS & WINDOWS MARKET, PATENT ANALYSIS, 2016-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 SMART ADAPTIVE GLAZING & CLIMATE-RESPONSIVE WINDOWS

- 6.6.2 SELF-POWERED & ENERGY-GENERATING DOORS & WINDOWS IN FUTURE SMART CITIES

- 6.6.3 INVISIBLE & MINIMALIST FRAME SYSTEMS

- 6.7 IMPACT OF AI/GEN AI ON DOORS & WINDOWS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN DOORS & WINDOWS PROCESSING

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN DOORS & WINDOWS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DOORS & WINDOWS MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 CUSTOM DOOR SOLUTIONS ENHANCING INTERIOR EXPERIENCE IN IOWA, US

- 6.8.2 BI-FOLD DOORS TRANSFORMING SPACE AND AESTHETICS IN WILTSHIRE, UK

- 6.8.3 ALUMINUM SLIDING DOORS ENABLING INDOOR-OUTDOOR LIVING IN TEXAS, US

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 SUSTAINABILITY INITIATIVES

- 7.1.3.1 Low-carbon materials and eco-friendly sourcing

- 7.1.3.2 High-performance glazing and energy efficiency

- 7.1.3.3 Resource efficiency and waste minimization

- 7.1.3.4 Circular economy and product lifecycle management

- 7.1.3.5 Sustainable manufacturing and emission control

- 7.1.3.6 Smart and adaptive building integration

- 7.2 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 DOORS & WINDOWS MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 DOORS

- 9.2.1 RISING DEMAND FOR SMART, SECURE, AND ENERGY-EFFICIENT DOOR SYSTEMS DRIVING MARKET GROWTH

- 9.3 WINDOWS

- 9.3.1 INCREASING ADOPTION OF ENERGY-EFFICIENT AND SMART WINDOW TECHNOLOGIES FUELING MARKET EXPANSION

10 DOORS & WINDOWS MARKET, BY CONSTRUCTION TYPE

- 10.1 INTRODUCTION

- 10.2 SWINGING

- 10.2.1 INCREASING DEMAND FOR ENERGY-EFFICIENT AND HIGH-PERFORMANCE SWINGING SYSTEMS TO DRIVE MARKET

- 10.3 SLIDING

- 10.3.1 RISING DEMAND FOR SPACE-SAVING AND ENERGY-EFFICIENT SOLUTIONS DRIVING GROWTH

- 10.4 FOLDING

- 10.4.1 GROWING PREFERENCE FOR FLEXIBLE, SPACE-OPTIMIZING DESIGNS DRIVING SEGMENTAL GROWTH

- 10.5 REVOLVING

- 10.5.1 RISING ADOPTION OF ENERGY-EFFICIENT AND HIGH-TRAFFIC ENTRY SOLUTIONS DRIVING GROWTH

- 10.6 OTHER CONSTRUCTION TYPES

11 DOORS & WINDOWS MARKET, BY MATERIAL

- 11.1 INTRODUCTION

- 11.2 WOOD

- 11.2.1 RISING DEMAND FOR SUSTAINABLE, AESTHETIC, AND HIGH-PERFORMANCE MATERIALS DRIVING GROWTH

- 11.3 METAL

- 11.3.1 INCREASING DEMAND FOR DURABLE, SECURE, AND LOW-MAINTENANCE SOLUTIONS DRIVING GROWTH

- 11.4 PLASTIC

- 11.4.1 RISING DEMAND FOR COST-EFFECTIVE, LOW-MAINTENANCE, AND ENERGY-EFFICIENT SOLUTIONS TO DRIVE MARKET

- 11.5 OTHER MATERIALS

12 DOORS & WINDOWS MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 RESIDENTIAL

- 12.2.1 RISING RENOVATION ACTIVITIES AND DEMAND FOR SMART, ENERGY-EFFICIENT HOMES DRIVING GROWTH

- 12.3 COMMERCIAL

- 12.3.1 STRINGENT ENERGY REGULATIONS AND EXPANSION OF COMMERCIAL INFRASTRUCTURE DRIVING GROWTH

- 12.4 INDUSTRIAL

- 12.4.1 GROWTH IN INDUSTRIAL ACTIVITY AND ENHANCED SAFETY COMPLIANCE BOOSTING MARKET EXPANSION

13 DOORS & WINDOWS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Urban renewal and green building transition driving market

- 13.2.2 INDIA

- 13.2.2.1 Rapid urbanization, premium housing demand, and infrastructure push to fuel market growth

- 13.2.3 JAPAN

- 13.2.3.1 Large-scale redevelopment and aging population to boost market

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Smart construction adoption and housing initiatives driving doors & windows demand

- 13.2.5 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 NORTH AMERICA

- 13.3.1 US

- 13.3.1.1 Strong residential pipeline and energy efficiency trends driving doors & windows market

- 13.3.2 CANADA

- 13.3.2.1 Housing shortage, government programs, and sustainable construction driving demand

- 13.3.3 MEXICO

- 13.3.3.1 Infrastructure expansion, industrial growth, and housing programs driving market

- 13.3.1 US

- 13.4 EUROPE

- 13.4.1 GERMANY

- 13.4.1.1 Energy-efficient renovation and infrastructure investments driving growth

- 13.4.2 FRANCE

- 13.4.2.1 Housing stabilization and energy-efficient renovation driving demand

- 13.4.3 ITALY

- 13.4.3.1 Infrastructure-led growth and energy retrofit transition shaping market growth

- 13.4.4 UK

- 13.4.4.1 Need for greater security and convenience to drive market

- 13.4.5 POLAND

- 13.4.5.1 Regulatory reforms and housing supply constraints shaping doors & windows demand

- 13.4.6 REST OF EUROPE

- 13.4.1 GERMANY

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Government-led housing expansion & modular adoption driving demand

- 13.5.2 ARGENTINA

- 13.5.2.1 Infrastructure recovery and decentralized projects driving demand

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

- 13.6.1.1 Saudi Arabia

- 13.6.1.1.1 Giga projects & Vision 2030 investments driving demand

- 13.6.1.2 UAE

- 13.6.1.2.1 Mega infrastructure investments and real estate growth driving demand

- 13.6.1.3 Rest of GCC Countries

- 13.6.1.1 Saudi Arabia

- 13.6.2 SOUTH AFRICA

- 13.6.2.1 Urban infrastructure investment and housing demand to drive market growth

- 13.6.3 REST OF MIDDLE EAST & AFRICA

- 13.6.1 GCC COUNTRIES

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS

- 14.4 REVENUE ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.6 BRAND COMPARISON

- 14.6.1 ASSA ABLOY AB (ASSA ABLOY ENTRANCE SYSTEMS(R))

- 14.6.2 LIXIL CORPORATION (TOSTEM(R)/LIXIL WINDOWS & DOORS)

- 14.6.3 CORNERSTONE BUILDING BRANDS (PLY GEM(R)/ATRIUM(R) WINDOWS & DOORS)

- 14.6.4 JELD-WEN HOLDING, INC. (JELD-WEN(R) DOORS & WINDOWS)

- 14.6.5 OWENS CORNING (MASONITE(R) DOORS)

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Product footprint

- 14.7.5.4 Material footprint

- 14.7.5.5 Construction type footprint

- 14.7.5.6 End-use industry footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 ASSA ABLOY

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 LIXIL CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 CORNERSTONE BUILDING BRANDS, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 JELD-WEN, INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 YKK AP

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 OWENS CORNING

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.4 MnM view

- 15.1.7 PELLA CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.4 MnM view

- 15.1.8 SCHUCO INTERNATIONAL KG

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.4 MnM view

- 15.1.9 ANDERSEN CORPORATION

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Expansions

- 15.1.9.4 MnM view

- 15.1.10 MITER BRANDS

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.10.3.3 Expansions

- 15.1.10.4 MnM view

- 15.1.11 MARVIN

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.11.3.2 Expansions

- 15.1.11.4 MnM view

- 15.1.1 ASSA ABLOY

- 15.2 OTHER PLAYERS

- 15.2.1 REYNAERS GROUP

- 15.2.2 INTERNORM

- 15.2.3 NORDAN GROUP

- 15.2.4 APARNA ENTERPRISES LIMITED

- 15.2.5 KOLBE & KOLBE MILLWORK CO., INC.

- 15.2.6 PROVIA LLC

- 15.2.7 THERMA-TRU CORP.

- 15.2.8 NOVOFERM GMBH

- 15.2.9 SIMPSON DOOR COMPANY

- 15.2.10 LOEWEN WINDOWS

- 15.2.11 BG LEGNO

- 15.2.12 VINYLGUARD WINDOW & DOOR SYSTEMS LTD.

- 15.2.13 SGM WINDOW MANUFACTURING LIMITED

- 15.2.14 PROMINANCE UPVC WINDOW SYSTEMS

- 15.2.15 GREENFORTUNE WINDOWS AND DOORS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 DEMAND-SIDE APPROACH

- 16.3.2 SUPPLY-SIDE APPROACH

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS