|

시장보고서

상품코드

2061396

화물 드론 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cargo Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

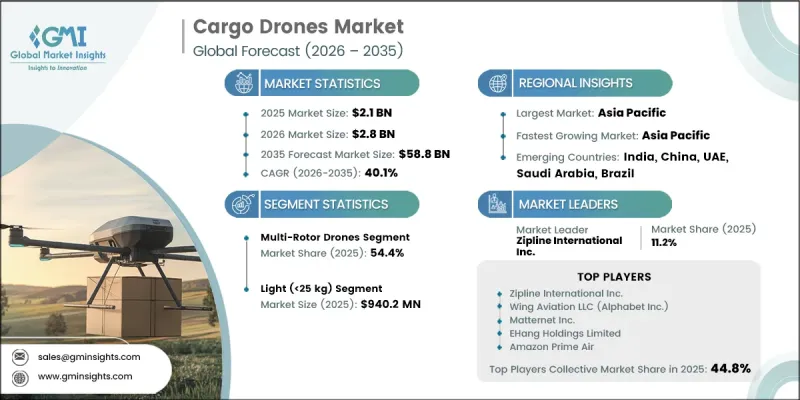

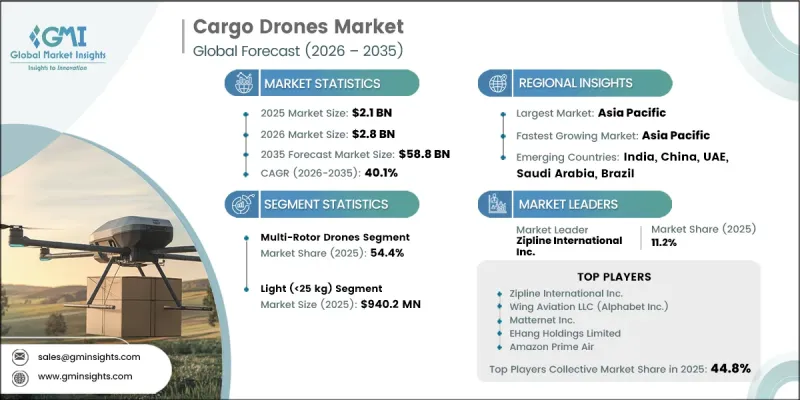

세계의 화물 드론 시장은 2025년에 21억 달러로 평가되며, 2035년까지 CAGR 40.1%로 성장하며, 588억 달러에 달할 것으로 추정되고 있습니다.

장거리 드론 운항을 지원하는 규제 체계가 마련되고 있으며, 또한 다양한 산업 분야에서 무인 항공기를 활용한 배송 시스템의 도입이 확대됨에 따라 해당 시장은 급속한 성장을 달성하고 있습니다. 특히 의료 물류 분야에서는 필수품의 신속하고 효율적인 운송이 점점 더 중요시되는 가운데, 화물 드론의 도입이 가속화되고 있습니다. 또한 국방 기관에서도 혹독한 환경이나 외딴 지역에서의 자재 및 장비 수송에 화물 드론의 활용을 확대하고 있으며, 시장 수요를 지원하고 있습니다. 자동화된 물류 생태계로의 전환이 진행되고 있는 데다, 적재 능력과 비행 효율의 지속적인 향상이 더해지면서 화물 드론 도입의 상업적 실현 가능성은 더욱 높아지고 있습니다. 첨단 항공 모빌리티 인프라와 자율주행 운송 기술에 대한 투자 확대 역시 대규모 시장의 발전을 지원하고 있습니다. 또한 지능형 내비게이션 시스템, AI를 활용한 경로 최적화, 그리고 배터리 기술의 발전에 따른 통합이 진전되면서 운영 효율성과 신뢰성이 향상됨에 따라 화물 드론은 전 세계의 현대적인 물류·수송 네트워크에 있으며, 점점 더 매력적인 솔루션으로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 21억 달러 |

| 예측액 | 588억 달러 |

| CAGR | 40.1% |

화물 드론 시장은 시야 외 비행(BVLOS) 운영의 추가적인 발전에 힘입어 더욱 성장하고 있습니다. 이를 통해 드론은 직접적인 시각적 감시 없이도 장거리 임무를 수행할 수 있게 됩니다. 이러한 기능들은 드론을 활용한 물류 네트워크의 확장성과 효율성을 대폭 향상시킵니다. 또한 항공로와 드론 착륙 시설을 포함한 도시 전용 드론 인프라의 개발을 통해 운영상의 연계가 개선되고, 도시 공역 내의 혼잡이 완화되고 있습니다. 정부와 민간 기관의 통합형 항공 모빌리티 시스템에 대한 투자 확대에 힘입어, 향후 10년 동안 대도시권 및 지방의 물류 네트워크에서 상업적 도입이 가속화될 것으로 예상됩니다.

하이브리드 VTOL 드론 시장은 2026-2035년 연평균 성장률(CAGR) 41.3%로 성장할 것으로 전망됩니다. 이러한 성장은 수직 이착륙 기능과 장거리 비행 능력, 그리고 뛰어난 적재 성능을 겸비한 하이브리드 VTOL 플랫폼의 능력 덕분입니다. 이러한 시스템은 장거리 배송의 효율성이 매우 중요한 도시 간 운송이나 외딴 지역의 물류 업무에서 점점 더 널리 도입되고 있습니다. 운영상의 유연성과 비용 효율성이 높은 물류 솔루션에 대한 수요가 증가함에 따라 상업 분야 전반에 걸쳐 이러한 솔루션의 도입이 지속적으로 확대되고 있습니다.

25kg 미만의 드론으로 구성된 경량 페이로드 부문은 2025년에 9억 4,020만 달러에 달했습니다. 이 부문은 단거리 배송 용도로 적합할 뿐만 아니라 운영 및 규제 측면에서의 복잡성이 낮아, 시장에서 강력한 주도적 위치를 유지하고 있습니다. 이러한 드론은 제조, 도입, 유지보수가 비교적 용이하므로 라스트 마일 배송이나 상업 물류 업무에서 매우 매력적입니다. 저렴한 가격과 도시 지역 배송 시스템과의 손쉬운 통합 덕분에, 이 제품은 시장에서 계속해서 널리 보급되고 있습니다.

2025년, 북미 화물 드론 시장은 43.4%의 점유율을 차지했습니다. 해당 지역 시장은 지원적인 규제 체계의 구축과 상용 드론 운용을 촉진하는 체계적인 공역 통합 프로그램의 시행에 힘입어 급속히 확대되고 있습니다. 정부 기관은 첨단 항공 모빌리티(AAM) 사업과 BVLOS(시야 외 비행) 도입 프로그램에 대한 지원을 강화하고 있으며, 이로 인해 물류 및 공공 서비스 분야에서의 화물용 드론 도입이 가속화되고 있습니다. 해당 지역의 항공우주 제조업체와 드론 기술 제공업체들이 보여주는 강력한 입지는 상용화 및 대규모 도입 활동을 더욱 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 플랫폼 유형별, 2022-2035년

제6장 시장 추산·예측 : 페이로드 용량별, 2022-2035년

제7장 시장 추산·예측 : 범위별, 2022-2035년

제8장 시장 추산·예측 : 추진 유형별, 2022-2035년

제9장 시장 추산·예측 : 자율주행 레벨별, 2022-2035년

제10장 시장 추산·예측 : 최종 용도 산업별, 2022-2035년

제11장 시장 추산·예측 : 지역별, 2022-2035년

제12장 기업 개요

KSA 26.06.24The Global Cargo Drones Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 40.1% to reach USD 58.8 billion by 2035.

The market is witnessing rapid growth due to the increasing development of regulatory frameworks supporting long-distance drone operations and the rising adoption of unmanned aerial delivery systems across multiple industries. Cargo drones are gaining strong momentum in healthcare logistics, where fast and efficient transportation of essential supplies is becoming increasingly important. In addition, defense organizations are expanding the use of cargo drones for transporting materials and equipment in difficult and remote environments, strengthening market demand. The growing transition toward automated logistics ecosystems, combined with continuous improvements in payload capabilities and flight efficiency, is further increasing the commercial viability of cargo drone deployment. Expanding investments in advanced air mobility infrastructure and autonomous transportation technologies are also supporting large-scale market development. Furthermore, the integration of intelligent navigation systems, AI-driven route optimization, and enhanced battery technologies is improving operational efficiency and reliability, making cargo drones an increasingly attractive solution for modern logistics and transportation networks worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $58.8 Billion |

| CAGR | 40.1% |

The cargo drones market is further supported by the increasing advancement of Beyond Visual Line of Sight (BVLOS) operations, which enable drones to perform long-distance missions without direct visual supervision. These capabilities significantly improve the scalability and efficiency of drone-based logistics networks. In addition, the development of dedicated urban drone infrastructure, including air corridors and drone landing facilities, is improving operational coordination and reducing congestion within urban airspaces. Growing investments by governments and private organizations in integrated air mobility systems are expected to accelerate commercial deployment across metropolitan and regional logistics networks through the coming decade.

The hybrid VTOL drones segment is expected to grow at a CAGR of 41.3% during 2026-2035. This growth is attributed to the capability of hybrid VTOL platforms to combine vertical takeoff functionality with extended flight range and higher payload performance. These systems are increasingly being adopted for intercity transportation and remote-area logistics operations where long-distance delivery efficiency is critical. Rising demand for operational flexibility and cost-efficient logistics solutions continues to strengthen adoption across commercial sectors.

The light payload segment, consisting of drones carrying less than 25 kg reached USD 940.2 million in 2025. The segment maintains strong market leadership due to its suitability for short-range delivery applications and lower operational and regulatory complexities. These drones are comparatively easier to manufacture, deploy, and maintain, making them highly attractive for last-mile delivery and commercial logistics operations. Their affordability and ease of integration into urban delivery systems continue to support widespread market adoption.

North America Cargo Drones Market accounted for 43.4% share in 2025. The regional market is expanding rapidly due to supportive regulatory developments and the implementation of structured airspace integration programs that facilitate commercial drone operations. Government agencies are increasingly supporting advanced air mobility initiatives and BVLOS deployment programs, which are accelerating cargo drone adoption across logistics and public service sectors. The strong presence of aerospace manufacturers and drone technology providers in the region further supports commercialization and large-scale deployment activities.

Major companies operating in the Global Cargo Drones Market include Zipline International Inc., Wing Aviation LLC (Alphabet Inc.), Matternet Inc., Volocopter GmbH, EHang Holdings Limited, Dronamics Ltd., Amazon Prime Air, Elroy Air Inc., VastArrive, Skyports Infrastructure, Swoop Aero, Wingcopter GmbH, Natilus Inc., Pipistrel VTOL, Valqari, Manna Aero, Volans-i, Airspace Link, Skyward (Verizon), and Flyte Systems. Companies operating in the cargo drones market are focusing on expanding their technological capabilities through continuous investments in autonomous flight systems, advanced navigation technologies, and AI-powered fleet management platforms. Strategic collaborations with logistics providers, healthcare organizations, and government agencies are helping companies accelerate commercial deployment and strengthen operational networks. Manufacturers are also prioritizing the development of hybrid VTOL systems and long-range drones to improve payload efficiency and operational flexibility. Investments in urban air mobility infrastructure, including drone ports and air traffic integration systems, are further supporting scalability. In addition, companies are working on enhancing battery performance, flight safety systems, and real-time communication technologies to improve reliability and reduce operational risks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Payload capacity trends

- 2.2.3 Range trends

- 2.2.4 Propulsion type trends

- 2.2.5 Autonomy level trends

- 2.2.6 End-use industry trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of beyond visual line of sight (BVLOS) operations enabling long range cargo delivery

- 3.2.1.2 Integration into healthcare supply chains for critical medical deliveries

- 3.2.1.3 Growing deployment in defense and tactical logistics operations

- 3.2.1.4 Shift toward autonomous and digitized connected logistics networks

- 3.2.1.5 Development of high-payload and long-endurance cargo drone platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory fragmentation across regions

- 3.2.2.2 High operational cost of large-scale drone logistics deployment

- 3.2.3 Market opportunities

- 3.2.3.1 Development of dedicated drone logistics hubs and infrastructure

- 3.2.3.2 Expansion into commercial middle-mile and intercity logistics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Multi-rotor drones

- 5.3 Fixed-wing drones

- 5.4 Hybrid VTOL drones

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Light (<25 kg)

- 6.3 Medium (25-100 kg)

- 6.4 Heavy (>100 kg)

Chapter 7 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Close-range (<50 km)

- 7.3 Short-range (50-149 km)

- 7.4 Mid-range (150-650 km)

- 7.5 Long-range (>650 km)

Chapter 8 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Battery-electric

- 8.3 Hydrogen/fuel cell

- 8.4 Hybrid

Chapter 9 Market Estimates and Forecast, By Autonomy Level, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Fully autonomous

- 9.3 Semi-autonomous

- 9.4 Remotely piloted

Chapter 10 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 Healthcare and emergency services

- 10.2.1 Medical supply delivery

- 10.2.2 Blood and organ transport

- 10.2.3 Emergency response and disaster relief

- 10.2.4 Others

- 10.3 Retail and e-commerce

- 10.3.1 Last-mile delivery

- 10.3.2 Inter-hub cargo transport

- 10.3.3 Warehouse transfer operations

- 10.3.4 Others

- 10.4 Defense and security

- 10.4.1 Field resupply

- 10.4.2 Border patrol logistics

- 10.4.3 Disaster evacuation support

- 10.4.4 Others

- 10.5 Agriculture

- 10.6 Infrastructure and construction

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Zipline International Inc.

- 12.1.2 Wing Aviation LLC (Alphabet Inc.)

- 12.1.3 Matternet Inc.

- 12.1.4 EHang Holdings Limited

- 12.1.5 Amazon Prime Air

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Elroy Air Inc.

- 12.2.1.2 Natilus Inc.

- 12.2.1.3 Valqari

- 12.2.1.4 Airspace Link

- 12.2.1.5 Skyward (Verizon)

- 12.2.1.6 Flyte Systems

- 12.2.2 Asia Pacific

- 12.2.2.1 VastArrive

- 12.2.3 Europe

- 12.2.3.1 Volocopter GmbH

- 12.2.3.2 Dronamics Ltd.

- 12.2.3.3 Wingcopter GmbH

- 12.2.3.4 Skyports Infrastructure

- 12.2.3.5 Pipistrel VTOL

- 12.2.3.6 Manna Aero

- 12.2.4 Middle East & Africa

- 12.2.4.1 Swoop Aero

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Volans-i.