|

시장보고서

상품코드

2061399

수의용 수술 기구 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Veterinary Surgical Instruments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

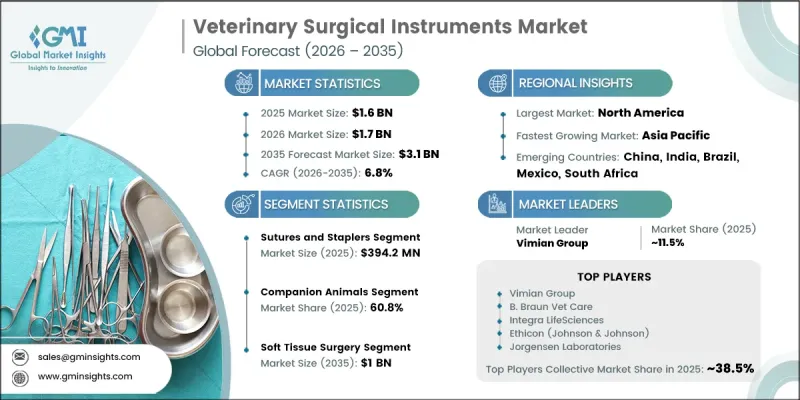

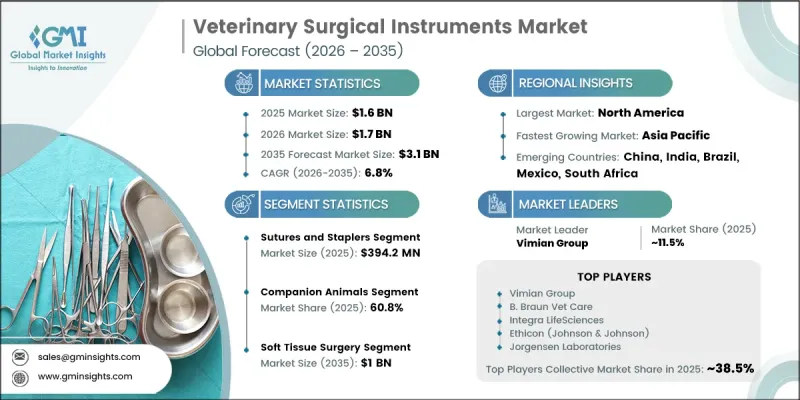

세계의 수의용 수술 기구 시장은 2025년에 16억 달러로 평가되고 CAGR 6.8%로 성장하며, 2035년까지 31억 달러에 달할 것으로 예측됩니다.

동물의 건강 상태에 대한 인식이 높아짐에 따라 시장 전체의 성장을 이끄는 데 중요한 역할을 하고 있습니다. 반려동물 사육 마릿수의 증가, 동물 관리에 대한 지출 확대, 그리고 수의학 기술의 급속한 발전이 수술 기구에 대한 수요를 더욱 높이고 있습니다. 또한 수의학적 시술 건수의 증가와 더불어 안과, 정형외과, 치과 등 전문 분야의 확대도 고도로 정교하고 용도에 특화된 수술 기구에 대한 수요를 지원하고 있습니다. 수의학용 수술 기구에는 집게, 메스 본체 및 날, 봉합 기구, 타월 클램프, 바늘 홀더 등 다양한 동물 외과 시술에 사용되는 필수 수기구가 포함됩니다. 동물병원, 진료소 및 의료기기 제조업체 간의 협력 강화로 인해 첨단 수술 솔루션에 대한 접근성이 개선되고 있습니다. 또한 선진국에서의 수의학 지출 증가, 인수공통감염병에 대한 우려 고조, 그리고 반려동물 비만증의 증가도 시장 성장에 더욱 기여하고 있습니다. 수술 기구의 지속적인 기술 발전은 정밀도, 안전성 및 시술 효율성을 높여 업계의 장기적인 성장을 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 16억 달러 |

| 예측액 | 31억 달러 |

| CAGR | 6.8% |

봉합사 및 스테이플러 시장은 2025년에 3억 9,420만 달러에 달했습니다. 이 부문은 일상적인 수의학적 치료부터 복잡한 시술에 이르기까지 상처 봉합 과정에서 매우 중요한 역할을 수행하고 있으며, 모든 임상 현장에서 안정적인 수요가 확보되어 있으며, 주도적인 위치를 유지하고 있습니다. 또한 연부조직 수술, 외상 치료, 불임 수술 등의 수술 건수가 많기 때문에 그 사용량은 더욱 증가하고 있습니다. 봉합 및 스테이플러 기술의 지속적인 혁신은 시술의 편의성, 안전 기준, 수술 후 치유 결과의 개선에도 기여하고 있으며, 이 부문의 지속적인 성장을 지원하고 있습니다.

2025년 기준으로 반려동물 부문은 60.8%의 점유율을 차지했습니다. 이 범주에는 개, 고양이, 말, 그 밖의 반려동물 등이 포함됩니다. 이 부문의 경쟁력은 반려동물 보유율의 상승과 반려인들이 첨단 수의학 치료에 대한 투자 의지가 높아짐에 따라 강력하게 지원되고 있습니다. 반려동물 보험이 점차 보급되고 있는 점도, 반려인들이 전문적인 외과적 치료나 첨단 의료 처치를 선택하는 데 한몫하고 있습니다. 이러한 요인들이 복합적으로 작용하여 반려동물의 의료에 사용되는 수의학용 수술 기구에 대한 수요를 높이고 있습니다.

북미의 수의학용 수술 기구 시장은 2025년에 40%의 점유율을 차지했습니다. 이 지역은 높은 반려동물 보유율, 수준 높은 수의학 인프라, 그리고 동물 의료 서비스에 대한 막대한 지출 덕분에 계속해서 선도적인 위치를 유지하고 있습니다. 확립된 동물병원 및 전문병원 네트워크에 더해, 저침습 수술과 첨단 외과 시술의 보급이 해당 지역의 성장을 더욱 지원하고 있습니다. 또한 반려동물 보험의 광범위한 보급, 동물 건강에 대한 의식의 향상, 그리고 업계를 선도하는 기업의 존재가 시장 발전을 지원하고 있습니다. 수의학 분야의 혁신에 대한 지속적인 투자와 애완동물 케어에 대한 관심 증가로 인해, 예측 기간 중 북미의 주도적 지위가 유지될 것으로 전망됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 제품별, 2022-2035년

제6장 시장 추산·예측 : 동물 유형별, 2022-2035년

제7장 시장 추산·예측 : 용도별, 2022-2035년

제8장 시장 추산·예측 : 최종 사용별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.24The Global Veterinary Surgical Instruments Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 3.1 billion by 2035.

Rising awareness regarding animal health conditions is playing a key role in driving overall market expansion. Growth in pet ownership, increased spending on animal care, and rapid advancements in veterinary medical technologies are further strengthening demand for surgical instruments. The rising number of veterinary procedures, along with the expansion of specialized veterinary disciplines such as ophthalmology, orthopedics, and dentistry, is also boosting the need for advanced and application-specific surgical tools. Veterinary surgical instruments include essential handheld devices such as forceps, scalpel handles and blades, suturing tools, towel clamps, and needle holders used in a wide range of animal surgical procedures. Increasing collaboration between veterinary hospitals, clinics, and instrument manufacturers is improving access to advanced surgical solutions. In addition, rising veterinary healthcare expenditure in developed economies, growing concerns over zoonotic diseases, and the increasing incidence of obesity in pets are further contributing to market growth. Continuous technological improvements in surgical tools are also enhancing precision, safety, and procedural efficiency, supporting long-term industry expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 6.8% |

The sutures and staplers segment reached USD 394.2 million in 2025. This segment maintains its leading position due to its critical importance in wound closure across both routine and complex veterinary procedures, ensuring consistent demand across clinical practices. Its strong usage is further supported by the high volume of surgeries such as soft tissue operations, trauma care procedures, and sterilization surgeries. Ongoing innovation in suturing and stapling technologies is also improving handling convenience, safety standards, and post-operative healing outcomes, contributing to sustained segment growth.

The companion animals segment accounted for 60.8% share in 2025. This category includes animals such as dogs, cats, horses, and other household pets. The segment's dominance is strongly supported by rising pet adoption rates and increasing willingness of owners to invest in advanced veterinary care. The growing penetration of pet insurance is also encouraging pet owners to opt for specialized surgical treatments and advanced medical procedures. These factors are collectively driving higher demand for veterinary surgical instruments used in companion animal healthcare.

North America Veterinary Surgical Instruments Market held a 40% share in 2025. The region continues to lead due to high rates of pet ownership, advanced veterinary healthcare infrastructure, and significant spending on animal health services. A well-established network of veterinary clinics and specialty hospitals, along with strong adoption of minimally invasive and advanced surgical procedures, further supports regional growth. In addition, widespread availability of pet insurance, rising awareness of animal health, and the presence of leading industry participants are strengthening market development. Continuous investments in veterinary innovation and increasing focus on companion animal care are expected to sustain North America's leadership over the forecast period.

Major companies operating in the Global Veterinary Surgical Instruments Industry include Arthrex, Avante Animal Health (Avante Health Solutions), B. Braun Vet Care, BMT Medizintechnik, Ethicon (Johnson & Johnson), Eickemeyer, GerMedUSA, Integra LifeSciences, Jorgensen Laboratories, Medtronic, Neogen Corporation, Sklar Surgical Instruments, STERIS, Smiths Medical, Surgical Holdings, Vimian Group, and World Precision Instruments. Companies operating in the veterinary surgical instruments market are implementing several strategic initiatives to strengthen their market position and expand global reach. Industry participants are focusing on continuous innovation in surgical tools to improve precision, safety, and procedural efficiency across veterinary applications. Many companies are expanding their product portfolios with advanced, ergonomically designed instruments suitable for complex and specialized procedures. Strategic collaborations with veterinary hospitals, clinics, and distribution partners are helping improve product availability and market penetration. In addition, manufacturers are investing heavily in research and development to introduce technologically advanced and cost-effective solutions aligned with evolving clinical needs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Animal type trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing animal healthcare expenditure in developed nations

- 3.2.1.2 Rising awareness about various animal health conditions

- 3.2.1.3 Escalating demand for pet health insurance

- 3.2.1.4 Growth in the number of veterinary practitioners in developed nations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled veterinary professionals in developing economies

- 3.2.2.2 High cost of veterinary surgeries

- 3.2.3 Market opportunities

- 3.2.3.1 Shift toward minimally invasive surgery (MIS)

- 3.2.3.2 Expansion of veterinary clinics & specialty hospitals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Pricing trend analysis (Driven by Primary Research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing analysis, by product

- 3.7 Investment & funding analysis

- 3.7.1 Venture capital & private equity activity

- 3.7.2 Strategic investments by key players

- 3.8 Future market trends

- 3.9 Pet population, by country, 2025

- 3.10 Impact of AI and Gen AI on the market

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Sutures and staplers

- 5.3 Forceps

- 5.4 Scalpels

- 5.5 Surgical scissors

- 5.6 Hooks and retractors

- 5.7 Trocars and cannulas

- 5.8 Electro-surgery instruments

- 5.9 Other products

Chapter 6 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Horses

- 6.2.4 Other companion animals

- 6.3 Livestock animals

- 6.3.1 Cattle

- 6.3.2 Sheep and goats

- 6.3.3 Swine

- 6.3.4 Poultry

- 6.4 Exotic and zoo animals

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Soft tissue surgery

- 7.3 Sterilization surgery

- 7.4 Dental surgery

- 7.5 Orthopedic surgery

- 7.6 Ophthalmic surgery

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals

- 8.3 Veterinary clinics

- 8.4 Academic and research institutes

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arthrex

- 10.2 Avante Animal Health (Avante Health Solutions)

- 10.3 B. Braun Vet Care

- 10.4 BMT Medizintechnik

- 10.5 Ethicon (Johnson & Johnson)

- 10.6 Eickemeyer

- 10.7 GerMedUSA

- 10.8 Integra LifeSciences

- 10.9 Jorgensen Laboratories

- 10.10 Medtronic

- 10.11 Neogen Corporation

- 10.12 Sklar Surgical Instruments

- 10.13 STERIS

- 10.14 Smiths Medical

- 10.15 Surgical Holdings

- 10.16 Vimian Group

- 10.17 World Precision Instruments