|

시장보고서

상품코드

2061403

VRL(Veterinary Reference Laboratory) 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Veterinary Reference Laboratory Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

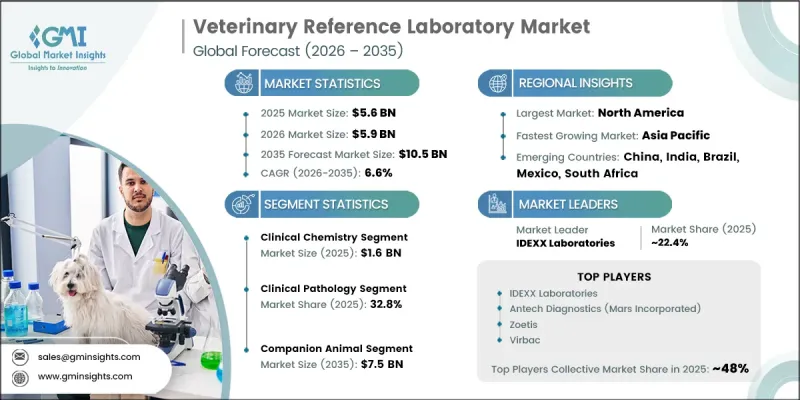

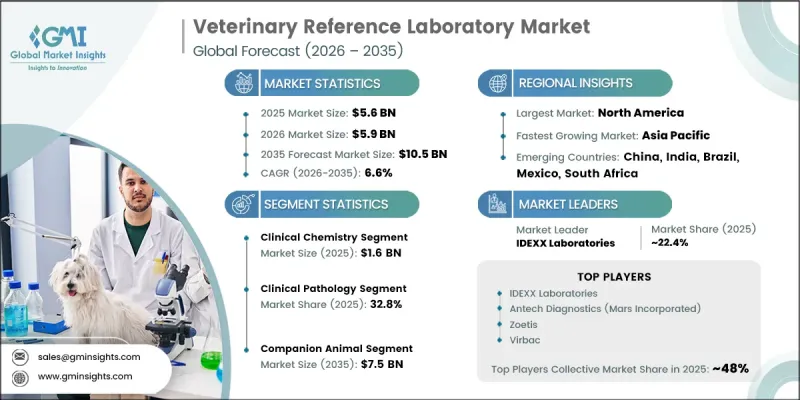

세계의 VRL(Veterinary Reference Laboratory) 시장은 2025년에 56억 달러로 평가되고 CAGR 6.6%로 성장하며, 2035년까지 105억 달러에 달할 것으로 추정되고 있습니다.

수의학 검사 기관은 가축 및 반려동물에 영향을 미치는 인수공통감염병의 규명 및 감시에서 매우 중요한 역할을 수행하고 있습니다. 이 기관들은 세균학, 임상병리학, 바이러스학, 독물학, 생식 검사 등 폭넓은 진단 서비스를 제공하고 있습니다. 또한 분자 진단, 혈액학, 면역 진단 검사 등의 첨단 기술을 통해 수의학을 지원하고 있습니다. 전 세계 반려동물 사육 마릿수가 증가함에 따라 동물 의료 및 진단 서비스에 대한 수요가 크게 증가하고 있습니다. 질병의 조기 발견과 예방 의료의 중요성에 대한 반려동물 주인들의 인식이 높아지면서, 전문적인 검사의 도입이 더욱 가속화되고 있습니다. 반려동물의 만성질환, 대사성 질환, 감염증과 관련된 정밀진단에 대한 수요는 꾸준히 증가하고 있습니다. 가축 분야에서도 동물의 건강 모니터링 및 식품 안전 기준 준수에 대한 관심이 높아짐에 따라 첨단 수의학적 진단에 대한 필요성이 대두되고 있습니다. 동물 질병 관리 및 수의의료 인프라 개선을 목적으로 한 정부의 지원책은 시장 전반에 걸쳐 관민 양측의 투자를 촉진하고 있습니다. 또한 동물병원과 검사 기관 간의 제휴 확대는 물론, 대기업의 네트워크 확장 전략에 힘입어 개발도상 지역의 진단 서비스 접근성이 개선되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 56억 달러 |

| 예측 시장 규모 | 105억 달러 |

| CAGR | 6.6% |

임상화학 부문은 2025년에 16억 달러에 달했습니다. 임상화학 검사는 혈액 및 기타 생체 시료를 분석함으로써 장기 기능, 대사 상태, 전해질 균형을 평가하는 데 있으며, 매우 중요한 역할을 하고 있습니다. 이러한 진단 절차는 반려동물과 가축 모두에서 간 기능, 신장 건강, 내분비계, 대사 상태와 관련된 질환을 확인하는 데 널리 활용되고 있습니다. 반려동물의 만성질환 유병률 증가는 임상화학 진단에 대한 수요를 크게 증가시키고 있으며, 이는 수의학 의료 시설 전반에 걸친 해당 부문의 성장에 기여하고 있습니다.

임상병리학 부문은 2025년에 32.8%의 시장 점유율을 차지했습니다. 이 부문은 정기적인 선별 검사, 질환 진단 및 장기적인 치료 관리에서 차지하는 중요성 덕분에 시장에서 여전히 강력한 입지를 유지하고 있습니다. 임상병리학에는 혈액학, 세포학, 소변 검사, 임상화학 등 주요 진단 분야가 포함되어 있으며, 이 모든 분야는 동물의 건강 상태를 정확하게 평가하기 위한 기초가 됩니다. 수의학 전문가들은 적시의 진단, 치료 계획 수립 및 지속적인 환자 모니터링을 위해 이러한 검사 기법에 대한 의존도를 높이고 있으며, 이로 인해 수의학 검사실 전반에 걸친 임상병리학 서비스에 대한 수요가 더욱 증가하고 있습니다.

2025년, 북미 수의학 검사 기관 시장은 44.6%의 점유율을 차지했습니다. 이 지역은 첨단인 수의학 인프라, 높은 반려동물 보유율, 그리고 동물 의료 서비스에 대한 막대한 지출 덕분에 계속해서 업계를 선도하고 있습니다. 인수공통감염병 예방에 대한 의식의 향상, 반려동물 보험 가입률 증가, 그리고 예방 수의학에 대한 관심 증대 역시 해당 지역의 시장 성장에 기여하고 있습니다. 또한 수의학 진단 및 동물 의료 기술에 대한 적극적인 투자가 북미 수의학 검사 기관 업계의 지속적인 성장을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 기술별, 2022-2035년

제6장 시장 추산·예측 : 용도별, 2022-2035년

제7장 시장 추산·예측 : 동물 유형별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

KSAThe Global Veterinary Reference Laboratory Market was valued at USD 5.6 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 10.5 billion by 2035.

Veterinary reference laboratories play a vital role in identifying and monitoring zoonotic diseases affecting both domestic and farm animals. These laboratories provide a broad range of diagnostic services, including bacteriology, clinical pathology, virology, toxicology, and reproductive testing. In addition, they support veterinary healthcare through advanced technologies such as molecular diagnostics, hematology, and immunodiagnostic testing. Rising pet ownership worldwide is significantly increasing demand for animal healthcare and diagnostic services. Growing awareness among pet owners regarding the importance of early disease detection and preventive healthcare is further accelerating the adoption of specialized laboratory testing. Demand for advanced diagnostics related to chronic conditions, metabolic disorders, and infectious diseases in companion animals continues to rise steadily. In the livestock sector, increasing focus on animal health monitoring and food safety compliance is also driving the need for advanced veterinary diagnostics. Supportive government initiatives aimed at improving animal disease management and veterinary healthcare infrastructure are encouraging both public and private investments across the market. Furthermore, expanding partnerships between veterinary clinics and reference laboratories, along with network expansion strategies adopted by major companies, are improving accessibility to diagnostic services in developing regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.6 Billion |

| Forecast Value | $10.5 Billion |

| CAGR | 6.6% |

The clinical chemistry segment reached USD 1.6 billion in 2025. Clinical chemistry testing plays a crucial role in evaluating organ functionality, metabolic conditions, and electrolyte balance through the analysis of blood and other biological samples. These diagnostic procedures are widely used for identifying disorders related to liver function, kidney health, endocrine systems, and metabolic conditions in both companion and livestock animals. The rising prevalence of chronic health conditions among pets is significantly increasing demand for clinical chemistry diagnostics, contributing to segment growth across veterinary healthcare facilities.

The clinical pathology segment accounted for 32.8% share in 2025. The segment continues to maintain strong market presence due to its importance in routine screening, disease diagnosis, and long-term treatment management. Clinical pathology includes key diagnostic disciplines such as hematology, cytology, urinalysis, and clinical chemistry, all of which support accurate evaluation of animal health conditions. Veterinary professionals increasingly rely on these testing methods for timely diagnosis, treatment planning, and continuous patient monitoring, which continues to strengthen demand for clinical pathology services across veterinary laboratories.

North America Veterinary Reference Laboratory Market held a 44.6% share in 2025. The region continues to lead the industry due to its advanced veterinary healthcare infrastructure, high rate of pet ownership, and substantial spending on animal healthcare services. Growing awareness regarding zoonotic disease prevention, rising adoption of pet insurance, and increasing emphasis on preventive veterinary care are also contributing to regional market growth. In addition, strong investments in veterinary diagnostics and animal healthcare technologies are supporting the continued expansion of the North American veterinary reference laboratory industry.

Key companies operating in the Global Veterinary Reference Laboratory Market include Antech Diagnostics (Mars), APHA Scientific, Colorado State University, Cornell University College of Veterinary Medicine, Friedrich-Loeffler-Institut, GD Animal Health, IDEXX Laboratories, Laboklin, Neogen Corporation, Texas A&M Veterinary Medical Diagnostic Laboratory, Virbac, and Zoetis. Companies operating in the veterinary reference laboratory market are implementing multiple strategies to strengthen their competitive position and expand their global footprint. Industry participants are investing heavily in advanced diagnostic technologies, including molecular diagnostics, digital pathology, and automated testing systems, to improve testing accuracy and turnaround times. Many organizations are also focusing on expanding laboratory networks and forming strategic partnerships with veterinary clinics and healthcare providers to improve service accessibility. Acquisitions, collaborations, and geographic expansion initiatives are helping companies strengthen their presence in emerging markets. In addition, market players are emphasizing research and development activities to introduce innovative diagnostic solutions for infectious diseases and chronic animal health conditions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 Animal type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing pet adoption for companionship

- 3.2.1.2 Rising adoption of pet insurance and increasing animal health expenditure

- 3.2.1.3 Increasing outbreaks of animal diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with diagnostic services

- 3.2.2.2 Growing adoption of POC portable instruments

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Increasing demand for livestock and food safety testing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Pricing analysis, 2025

- 3.7 Future market trends

- 3.8 Impact of AI and Gen AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Clinical chemistry

- 5.3 Immunodiagnostics

- 5.3.1 ELISA

- 5.3.2 Lateral flow assays

- 5.3.3 Other immunodiagnostics assays

- 5.4 Molecular diagnostics

- 5.4.1 PCR tests

- 5.4.2 Microarray

- 5.4.3 Other molecular diagnostic services

- 5.5 Hematology

- 5.6 Urinalysis

- 5.7 Other technologies

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical pathology

- 6.3 Bacteriology

- 6.4 Virology

- 6.5 Parasitology

- 6.6 Productivity testing

- 6.7 Pregnancy testing

- 6.8 Toxicology testing

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Sheep and goats

- 7.3.5 Other livestock animals

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Antech Diagnostics (Mars)

- 9.2 APHA Scientific

- 9.3 Colorado State University

- 9.4 Cornell University College of Veterinary Medicine

- 9.5 Friedrich-Loeffler-Institut

- 9.6 GD Animal Health

- 9.7 IDEXX Laboratories

- 9.8 Laboklin

- 9.9 Neogen Corporation

- 9.10 Texas A&M Veterinary Medical Diagnostic Laboratory

- 9.11 Virbac

- 9.12 Zoetis