|

시장보고서

상품코드

2061420

전기 오토바이 및 스쿠터 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Electric Motorcycle and Scooters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

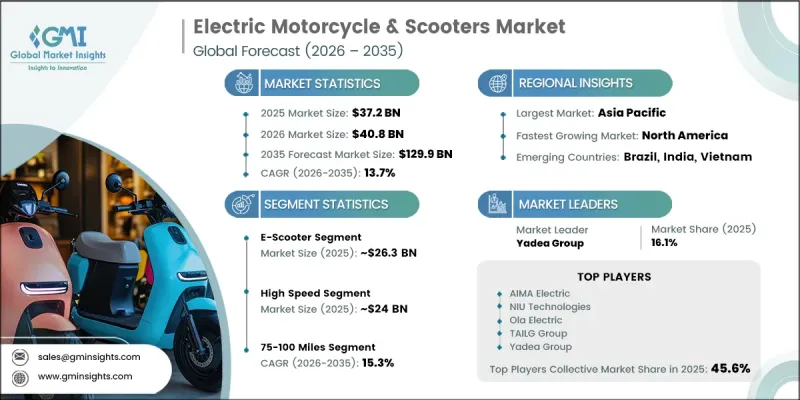

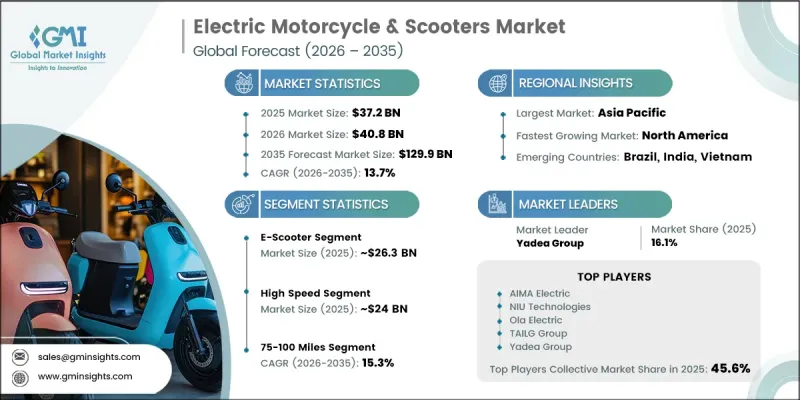

세계의 전기 오토바이·스쿠터 시장은 2025년에 372억 달러로 평가되고 CAGR 13.7%로 성장하며, 2035년까지 1,299억 달러에 달할 것으로 추정되고 있습니다.

시장 구조는 여전히 아시아태평양에 크게 집중되어 있으며, 2025년에는 시장 총액의 96.5%를 차지했습니다. 한편, 북미와 유럽은 현재 시장 점유율이 낮긴 하지만, 충전 인프라, 판매점 네트워크 및 소비자 인식이 지속적으로 개선됨에 따라 꾸준히 성장하고 있습니다. 시장의 성장은 정책 체계의 영향을 크게 받고 있으며, 인센티브 제도, 세제 혜택, 그리고 규제 측면에서의 접근성 이점이 초기 소유 비용을 대폭 낮추고 보급률을 가속화하고 있습니다. 경제적 요인도 중요한 역할을 하고 있으며, 내연기관 차량에 비해 1킬로미터당 운영 비용이 낮고, 장기적인 유지보수 요구 사항도 적기 때문에 총 소유 비용(TCO) 측면에서 우위가 더욱 커지고 있습니다. 이러한 요인들이 복합적으로 작용하여, 특히 이용률이 높은 밀집된 도시 환경에서 개인용 이동 수단 및 상업용 차량 모두에 있으며, 전동 이륜차의 매력이 높아지고 있습니다. 배터리 교체형 모델과 공유 충전 생태계는 운영 효율을 한층 더 높이고, 가동률을 향상시키며, 고정식 충전 인프라에 대한 의존도를 낮추고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025 |

| 예측 기간 | 2026-2035 |

| 개시 금액 | 372억 달러 |

| 예측액 | 1,299억 달러 |

| CAGR | 13.7% |

전동 스쿠터 부문은 70.8%의 시장 점유율을 차지했으며, 2025년에는 263억 달러 규모의 시장을 형성했습니다. 이 카테고리는 도시내 단거리 통근 및 배송 용도와 높은 친화성을 보이기 때문에 계속해서 주도적인 위치를 유지하고 있습니다. 한편, 전기 오토바이는 주행 거리 연장, 고속 주행 능력, 고속도로 주행 적합성 등이 필수적인, 보다 고성능의 사용 사례로 그 위상이 점차 변화하고 있습니다. 배터리의 에너지 밀도와 비용 효율성이 향상됨에 따라 전기 오토바이는 점차 주행 거리를 늘릴 수 있게 되었으며, 기존 대체 수단과의 경쟁력을 높이고 있습니다.

고속 부문은 2025년에 64.4%의 점유율을 차지했으며, 시장 규모는 240억 달러에 달했습니다. 기술의 발전으로 가속 성능, 내구성 및 전반적인 주행 성능이 향상됨에 따라 고속 전기 이륜차의 인기가 높아지고 있습니다. 이러한 차량들은 고속도로 주행 요건을 충족하게 되었으며, 일상적인 출퇴근이나 장거리 이동에 사용되는 내연기관 모델을 대체할 유력한 선택지로 떠오르고 있습니다.

미국의 전기 오토바이 및 스쿠터 시장은 2025년에 1억 470만 달러에 달하며, 2026-2035년 연평균 성장률(CAGR) 15.6%로 성장할 것으로 전망됩니다. 이 국가는 지역 시장 가치의 약 83%를 차지하고 있으며, 이는 대도시권에서의 조기 기술 도입과 소비자들의 높은 관심에 힘입은 것입니다. 인구 밀도가 높고, 환경 의식이 높으며, 기술 지향적인 소비자가 많은 도시 지역이 계속해서 보급을 주도하며, 꾸준한 시장 확대를 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 차량별, 2022-2035년

제6장 시장 추산·예측 : 속도별, 2022-2035년

제7장 시장 추산·예측 : 범위별, 2022-2035년

제8장 시장 추산·예측 : 배터리별, 2022-2035년

제9장 시장 추산·예측 : 출력별, 2022-2035년

제10장 시장 추산·예측 : 전압별, 2022-2035년

제11장 시장 추산·예측 : 최종 사용별, 2022-2035년

제12장 시장 추산·예측 : 판매 채널별, 2022-2035년

제13장 시장 추산·예측 : 지역별, 2022-2035년

제14장 기업 개요

KSA 26.06.24The Global Electric Motorcycle &Scooters Market was valued at USD 37.2 billion in 2025 and is estimated to grow at a CAGR of 13.7% to reach USD 129.9 billion by 2035.

The market structure remains heavily concentrated in Asia Pacific, which accounted for 96.5% of total value in 2025, while North America and Europe currently represent smaller shares but are steadily expanding as charging infrastructure, dealership networks, and consumer awareness continue to improve. Market growth is strongly influenced by policy frameworks, where incentive schemes, tax benefits, and regulatory access advantages significantly lower upfront ownership costs and accelerate adoption rates. Economic fundamentals also play a central role, as lower per-kilometer operating costs compared to internal combustion vehicles and reduced long-term maintenance requirements strengthen the total cost of ownership advantage. These combined factors are increasing the attractiveness of electric two-wheelers for both personal mobility and commercial fleet applications, particularly in dense urban environments where utilization rates are high. Battery swapping models and shared charging ecosystems are further improving operational efficiency, enabling higher uptime and reducing dependency on fixed charging infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $37.2 Billion |

| Forecast Value | $129.9 Billion |

| CAGR | 13.7% |

The e-scooter segment held a 70.8% share, generating USD 26.3 billion in 2025. This category continues to lead due to its strong alignment with short-distance urban commuting and delivery applications. Electric motorcycles, on the other hand, are increasingly positioned toward higher performance use cases where extended range, higher speed capability, and highway suitability are essential. Growing improvements in battery density and cost efficiency are gradually enabling electric motorcycles to achieve longer travel ranges, making them more competitive with conventional alternatives.

The high-speed segment accounted for 64.4% share in 2025, valued at USD 24 billion. High-speed electric two-wheelers are gaining momentum as technological improvements enhance acceleration, endurance, and overall riding performance. These vehicles are increasingly meeting highway-grade requirements, making them viable substitutes for internal combustion engine models used in daily commuting and long-distance travel.

U.S. Electric Motorcycle and Scooters Market reached USD 104.7 million in 2025 and is expected to grow at a CAGR of 15.6% from 2026 to 2035. The country represents approximately 83% of the regional market value, supported by early technology adoption and strong consumer interest in metropolitan areas. Urban centers characterized by dense populations, environmental awareness, and tech-oriented consumers continue to drive adoption, reinforcing steady market expansion.

Key players operating in the Global Electric Motorcycle &Scooters Industry include Yadea Group, TVS Motor, Hero MotoCorp, NIU Technologies, Gogoro, Ola Electric, AIMA Electric, Luyuan Electric, TAILG Group, and Zero Motorcycles. Companies in the electric motorcycle & scooters market are focusing heavily on battery innovation and cost optimization to improve driving range and reduce vehicle prices. They are expanding battery swapping and charging infrastructure partnerships to enhance convenience and increase adoption speed in urban areas. Strategic collaboration with energy providers, mobility platforms, and logistics operators is strengthening fleet deployment opportunities. Manufacturers are also investing in lightweight materials and advanced powertrain systems to improve vehicle efficiency and performance. In addition, digital integration through connected vehicle platforms, app-based fleet management, and predictive maintenance solutions is enhancing user experience. Expansion into emerging markets, coupled with localized production strategies and aggressive dealership growth, is further helping companies strengthen competitive positioning and capture long-term demand growth in both personal and commercial mobility segments.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Speed

- 2.2.4 Range

- 2.2.5 Battery

- 2.2.6 Power Output

- 2.2.7 Voltage

- 2.2.8 End-Use

- 2.2.9 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent Emission Regulations & Climate Action Commitments

- 3.2.1.2 Rising Fuel Prices & Total Cost of Ownership Benefits

- 3.2.1.3 Government Incentives, Subsidies & Tax Benefits

- 3.2.1.4 Advancement in Battery Technology & Declining Battery Costs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Upfront Purchase Cost vs ICE Alternatives

- 3.2.2.2 Limited Charging Infrastructure & Range Anxiety

- 3.2.3 Market opportunities

- 3.2.3.1 Fleet Electrification in Logistics & Delivery Sectors

- 3.2.3.2 Battery Swapping Business Models & Infrastructure Plays

- 3.2.3.3 Export Opportunities from Low-Cost Manufacturing Hubs

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.1.1 Lithium-ion Battery Systems (NMC / LFP)

- 3.3.1.2 BLDC (Brushless DC) Hub Motors

- 3.3.2 Emerging technologies

- 3.3.2.1 Solid-State Batteries

- 3.3.2.2 Swappable Battery Ecosystems

- 3.3.2.3 Wireless Inductive Charging

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - Environmental Protection Agency (EPA)

- 3.6.1.2 US - National Highway Traffic Safety Administration (NHTSA)

- 3.6.1.3 Canada - Transport Canada

- 3.6.2 Europe

- 3.6.2.1 EU - European Commission (Mobility and Transport/Green Deal framework)

- 3.6.2.2 Germany - Kraftfahrt-Bundesamt (KBA)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - Ministry of Industry and Information Technology (MIIT)

- 3.6.3.2 India - Ministry of Road Transport and Highways (MoRTH)

- 3.6.4 LATAM

- 3.6.4.1 Brazil - CONTRAN

- 3.6.4.2 Brazil - Secretaria Nacional de Transito (SENATRAN)

- 3.6.5 MEA

- 3.6.5.1 Saudi Arabia - SASO

- 3.6.5.2 UAE - Ministry of Industry and Advanced Technology (MoIAT)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Trade Data Analysis (Driven by Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.11.1 Battery Pack Cost

- 3.11.2 Electric Powertrain Cost

- 3.11.3 Chassis & Mechanical Components Cost

- 3.11.4 Electronics Cost

- 3.11.5 Manufacturing & Assembly Cost

- 3.12 Patent analysis (Driven by Primary Research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Charging infrastructure readiness

- 3.15.1 Public charging station density & geographic coverage

- 3.15.2 Charging standards & compatibility issues

- 3.15.3 Fast charging vs home charging economics

- 3.15.4 Battery swapping network development

- 3.15.5 Infrastructure investment gaps & future roadmap

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.16.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Vehicle, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 E-Motorcycle

- 5.2.1 Dirt Bikes

- 5.2.2 Sports Motorcycles

- 5.2.3 Standard Motorcycles

- 5.2.3.1 Cruiser

- 5.2.3.2 Touring

- 5.2.3.3 Street/Naked

- 5.2.3.4 Adventure/Dual-Sport

- 5.2.3.5 Commuter

- 5.3 E-Scooter

- 5.3.1 Folding Scooters

- 5.3.2 Three-Wheeled Scooters

- 5.3.3 Standard Scooters

- 5.3.4 Mopeds

Chapter 6 Market Estimates and Forecast, By Speed, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Low Speed

- 6.3 High Speed

Chapter 7 Market Estimates and Forecast, By Range, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Below 75 Miles

- 7.3 75-100 Miles

- 7.4 Above 100 Miles

Chapter 8 Market Estimates and Forecast, By Battery, 2022 - 2035 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Lead Acid

- 8.3 Lithium-ion

- 8.3.1 Lithium Iron Phosphate (LFP)

- 8.3.2 Nickel Manganese Cobalt (NMC)

Chapter 9 Market Estimates and Forecast, By Power Output, 2022 - 2035 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Below 3 kW

- 9.3 3-10 kW

- 9.4 Above 10 kW

Chapter 10 Market Estimates and Forecast, By Voltage, 2022 - 2035 ($ Mn, Units)

- 10.1 Key trends

- 10.2 36V

- 10.3 48V

- 10.4 60V

- 10.5 72V

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By End-Use, 2022 - 2035 ($ Mn, Units)

- 11.1 Key trends

- 11.2 Private/Individual

- 11.3 Commercial

- 11.3.1 Logistics & Delivery

- 11.3.2 Shared Mobility/Ride-sharing

- 11.3.3 Law Enforcement & Municipal Services

Chapter 12 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Mn, Units)

- 12.1 Key trends

- 12.2 Online

- 12.3 Offline

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Netherlands

- 13.3.7 Norway

- 13.3.8 Sweden

- 13.3.9 Belgium

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Vietnam

- 13.4.6 Indonesia

- 13.4.7 Thailand

- 13.4.8 Philippines

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.5.4 Colombia

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global players

- 14.1.1 Yadea Group

- 14.1.2 NIU Technologies

- 14.1.3 Hero MotoCorp

- 14.1.4 Ola Electric

- 14.1.5 TAILG Group

- 14.1.6 Gogoro

- 14.1.7 TVS Motor

- 14.1.8 Yamaha Motor

- 14.1.9 Zero Motorcycles

- 14.1.10 Ather Energy

- 14.1.11 AIMA Electric

- 14.1.12 Honda

- 14.2 Regional players

- 14.2.1 Bajaj Auto

- 14.2.2 TORROT Electric

- 14.2.3 Oben Electric

- 14.2.4 Maeving

- 14.2.5 Mohenic Motors

- 14.2.6 Savic Motorcycles

- 14.3 Emerging players

- 14.3.1 Matter Motors

- 14.3.2 Ryvid