|

시장보고서

상품코드

2061423

냉동절제 기기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Cryoablation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

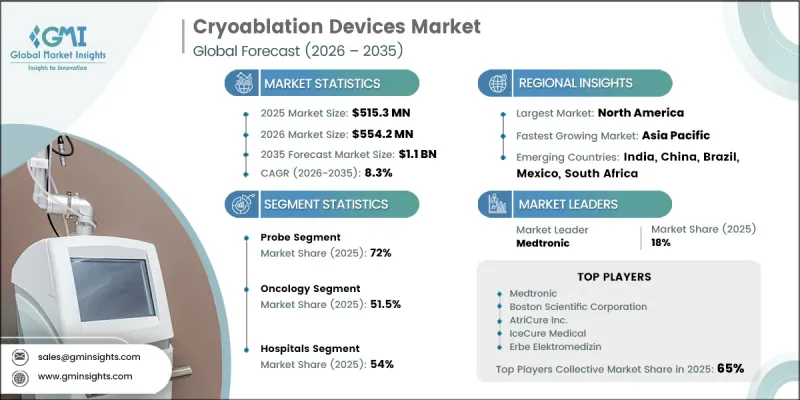

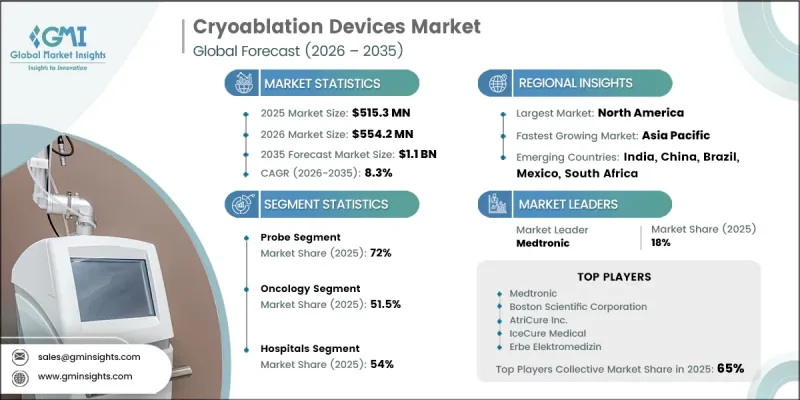

세계의 냉동절제 기기 시장은 2025년에 5억 1,530만 달러로 평가되고 CAGR 8.3%로 성장하며, 2035년까지 11억 달러에 달할 것으로 추정되고 있습니다.

이 시장의 성장은 암 및 심혈관 질환의 발병률 증가, 최소 침습 치료법에 대한 선호도 상승, 그리고 냉동 절제 시스템의 지속적인 기술 발전에 힘입어 이루어지고 있습니다. 고령화의 진행, 앉아 있는 시간이 많은 생활 습관, 비만이나 당뇨병 등의 위험 요인에 노출되는 경우가 늘어나면서 질환의 유병률과 치료 수요가 더욱 증가하고 있습니다. 동결 절제 장치는 전용 프로브나 카테터를 통해 극저온을 가함으로써 비정상 조직이나 병변 조직을 제거하도록 설계된 의료 기술입니다. 이러한 시스템은 주변의 건강한 조직을 보호하면서 종양이나 심장 조직을 정확하게 표적으로 삼는 제어된 동결 영역을 생성합니다. 안전성이 높고 회복 기간이 단축된 표적 치료를 제공할 수 있으므로 저침습적 종양학 및 심장학 수술에서 널리 사용되고 있습니다. 합병증 발생률이 낮고, 재현성이 뛰어나며, 환자 예후를 개선하는 등의 장점을 지닌 이 시술에 대한 임상 현장의 선호도가 높아지고 있는 것이 전 세계 의료 시스템에서의 도입을 크게 촉진하고 있습니다. 의료 제공자들이 점점 더 비침습적인 치료법으로 전환해 나가는 가운데, 동결 절제술 기술에 대한 수요는 전 세계 시장에서 계속해서 견고할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 5억 1,530만 달러 |

| 예측액 | 11억 달러 |

| CAGR | 8.3% |

2025년에는 프로브 부문이 72%의 점유율을 차지했습니다. 동결 절제용 프로브는 극저온을 전달하는 주요 기구로서, 심장 및 종양학 분야 모두에서 정밀하고 제어된 조직 파괴를 가능하게 합니다. 이러한 기기는 길이, 직경, 끝부분 구조 등이 서로 다른 여러 가지 구성으로 제공되므로, 의사는 특정 해부학적 및 임상적 요구 사항에 맞춰 시술을 조정할 수 있습니다. 열전도율 향상 및 동결 성능 최적화 등 프로브 설계 분야의 지속적인 발전으로 인해 시술의 정밀도, 일관성 및 전반적인 치료 성과가 향상되고 있으며, 이는 해당 부문의 지속적인 성장을 지원하고 있습니다.

2025년 기준으로 종양학 부문은 51.5%의 점유율을 차지했습니다. 이 부문은 간, 신장, 폐, 전립선, 유방에 영향을 미치는 종양을 포함한 다양한 암 치료에 냉동 절제 기술을 활용하는 데 중점을 두고 있습니다. 동결 절제술은 악성 조직을 표적으로 삼아 파괴하면서도 주변 정상 조직에 대한 손상을 최소화할 수 있으며, 기존의 외과적 시술이 적합하지 않은 환자에게 특히 유용합니다. 임상의들이 저침습적 종양 치료 옵션을 점점 더 많이 채택함에 따라 근치적 치료와 완화 치료 양 분야에서 그 적용 범위는 계속해서 확대되고 있습니다.

미국의 냉동 절제 기기 시장은 2025년에 1억 9,030만 달러로 평가되며, 2026-2035년 연평균 성장률(CAGR) 8%로 성장할 것으로 전망됩니다. 북미 전역에서 암 환자 수가 증가함에 따라 냉동 절제술 기술에 대한 수요가 확대되고 있습니다. 해당 지역에서는 연간 암 진단 건수가 여전히 높은 수준을 유지하고 있으며, 첨단이고 저침습적인 치료 솔루션에 대한 수요가 높아지고 있습니다. 또한 정밀한 종양 관리 기술에 대한 임상 현장의 선호도가 높아지고 있는 점도 시장 확대를 더욱 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 유형별, 2022-2035년

제6장 시장 추산·예측 : 용도별, 2022-2035년

제7장 시장 추산·예측 : 최종 사용별, 2022-2035년

제8장 시장 추산·예측 : 지역별, 2022-2035년

제9장 기업 개요

KSAThe Global Cryoablation Devices Market was valued at USD 515.3 million in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 1.1 billion by 2035.

The market growth is driven by the rising incidence of cancer and cardiovascular diseases, increasing preference for minimally invasive treatment procedures, and continuous technological advancements in cryoablation systems. Expanding aging populations, sedentary lifestyles, and higher exposure to risk factors such as obesity and diabetes are further contributing to disease prevalence and treatment demand. Cryoablation devices are medical technologies designed to eliminate abnormal or diseased tissue through the application of extremely low temperatures delivered via specialized probes or catheters. These systems generate controlled freezing zones that precisely target tumors or cardiac tissue while protecting surrounding healthy structures. They are widely used in minimally invasive oncology and cardiology procedures due to their ability to deliver targeted therapy with improved safety and reduced recovery time. Growing clinical preference for procedures that offer lower complication rates, repeatability, and enhanced patient outcomes is significantly strengthening adoption across healthcare systems worldwide. As healthcare providers continue to shift toward less invasive treatment alternatives, demand for cryoablation technologies is expected to remain strong across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $515.3 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 8.3% |

The probe segment accounted for a share of 72% in 2025. Cryoablation probes serve as the primary delivery instruments for extremely low temperatures, enabling precise and controlled tissue destruction in both cardiac and oncology applications. These devices are available in multiple configurations, including varying lengths, diameters, and tip structures, allowing physicians to tailor procedures to specific anatomical and clinical needs. Ongoing advancements in probe design, including improved thermal conductivity and optimized freezing performance, are enhancing procedural accuracy, consistency, and overall treatment outcomes, thereby supporting sustained segment growth.

The oncology segment held a share of 51.5% in 2025. This segment focuses on the use of cryoablation technologies for treating a range of cancers, including tumors affecting the liver, kidney, lung, prostate, and breast. Cryoablation enables targeted destruction of malignant tissues while minimizing damage to surrounding healthy structures, making it particularly valuable for patients who are not eligible for traditional surgical interventions. Its application across both curative and palliative care settings continues to expand as clinicians increasingly adopt minimally invasive oncology treatment options.

U.S. Cryoablation Devices Market was valued at USD 190.3 million in 2025 and is projected to grow at a CAGR of 8% from 2026 to 2035. The rising burden of cancer cases across North America is a major factor fueling demand for cryoablation technologies. The region continues to record a high volume of annual cancer diagnoses, reinforcing the need for advanced and minimally invasive treatment solutions. Increasing clinical preference for precise tumor management techniques is further supporting market expansion.

Key companies operating in the Global Cryoablation Devices Market include Medtronic, Boston Scientific, AtriCure Inc., Varian Medical Systems, IceCure Medical, Monteris Medical, Erbe Elektromedizin, Adagio Medical, CooperSurgical, CPSI Biotech, Endocare (HealthTronics), Hygea Medical, Inomed Medizintechnik, METRUM Cryoflex, and IceSense Medical. Companies in the cryoablation devices market are focusing on strengthening their market position through continuous technological innovation aimed at improving precision, safety, and procedural efficiency. A key strategy involves expanding product portfolios with next-generation cryoprobes and integrated ablation systems that offer enhanced thermal control and better clinical outcomes. Market players are also investing heavily in research and development to advance imaging-guided cryoablation and improve real-time procedural monitoring capabilities. Strategic collaborations with hospitals, oncology centers, and research institutions are helping accelerate clinical adoption and expand procedural applications. Additionally, companies are pursuing regulatory approvals in multiple regions to broaden geographic reach and increase commercialization opportunities. Strengthening distribution networks and expanding presence in emerging healthcare markets are also key priorities.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy and data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy and data integrity commitment

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.2.4 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cancer & cardiovascular disorders.

- 3.2.1.2 Growing demand for minimally invasive procedures.

- 3.2.1.3 Technological advancements in cryoablation devices.

- 3.2.1.4 Rising government initiatives and awareness campaigns.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with cryoablation devices.

- 3.2.2.2 Lack of awareness and expertise.

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding clinical evidence for cryoablation in pain management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.1.1 Advanced imaging integration

- 3.5.1.2 Multi-channel and temperature monitoring systems

- 3.5.2 Emerging technologies

- 3.5.2.1 Liquid nitrogen-based systems

- 3.5.2.2 Expansion into new clinical applications

- 3.5.1 Current technological trends

- 3.6 Future market trends (Driven by primary research)

- 3.7 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.8 Pricing trend analysis (Driven by primary research)

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Probe

- 5.2.1 Tissue contacts probe ablators

- 5.2.2 Epidermal and subcutaneous cryoablation systems

- 5.2.3 Tissue spray probe ablators

- 5.3 Systems

- 5.3.1 Generator

- 5.3.2 Accessories & consumables

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiology

- 6.3 Oncology

- 6.3.1 Lung cancer

- 6.3.2 Breast cancer

- 6.3.3 Liver cancer

- 6.3.4 Kidney cancer

- 6.3.5 Prostate cancer

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Adagio Medical

- 9.2 AtriCure Inc.

- 9.3 Boston Scientific

- 9.4 CooperSurgical

- 9.5 CPSI Biotech

- 9.6 Endocare (HealthTronics)

- 9.7 Erbe Elektromedizin

- 9.8 Hygea Medical

- 9.9 IceCure Medical

- 9.10 Inomed Medizintechnik

- 9.11 Medtronic

- 9.12 Monteris Medical

- 9.13 METRUM Cryoflex

- 9.14 Varian Medical Systems

- 9.15 IceSense Medical