|

시장보고서

상품코드

2061425

전기 덤프트럭 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Electric Dump Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

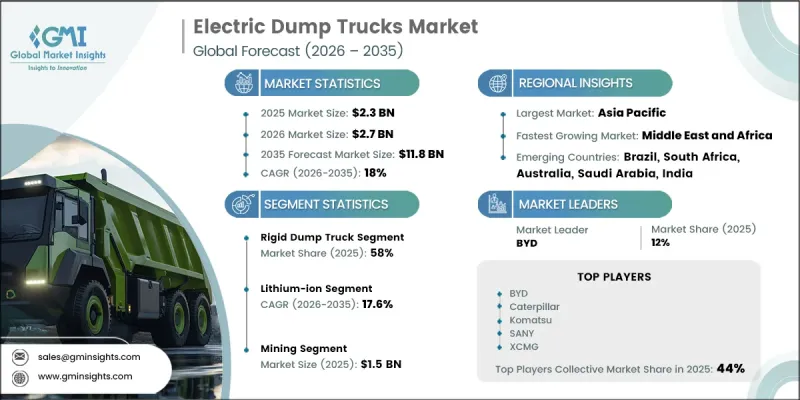

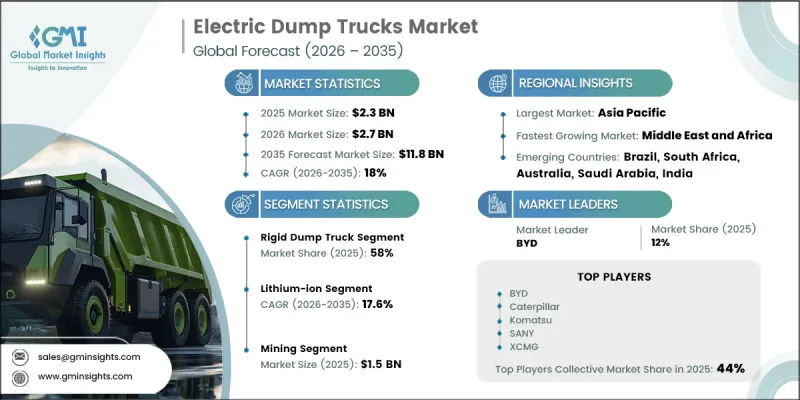

세계의 전동 덤프트럭 시장은 2025년에 23억 달러로 평가되고 CAGR 18%로 성장하며, 2035년까지 118억 달러에 달할 것으로 예측됩니다.

대형 비도로용 차량 전반에 걸쳐 전동화가 가속화되면서 시장은 급속한 변화를 겪고 있습니다. 에너지 밀도 향상 및 제조 비용 절감 등 배터리 성능의 개선으로 인해 전기 덤프트럭의 상업적 실현 가능성이 크게 높아지고 있습니다. 이러한 발전 덕분에 차량의 주행 거리, 내구성 및 운영 효율성이 향상되어, 전기자동차 모델이 기존 디젤 차량과 더욱 효과적으로 경쟁할 수 있게 되었습니다. 또한 내연기관 차량에 비해 운용 및 유지보수 요건이 낮기 때문에 광업 및 건설 업계 전반에서 도입이 가속화되고 있습니다. 환경 규제 강화, 연료비 급등, 수명 주기 전반에 걸친 운영 비용 절감에 대한 압박이 커지면서 배터리식 대형 전기 트럭으로의 전환이 가속화되고 있습니다. 충전 인프라 구축이 진전되고 있는 점도 중요한 역할을 하고 있으며, 특히 지속적인 전력 공급이 필수적인 대규모 광업이나 건설 현장에서 그 효과가 두드러집니다. 차량 보유 사업자, 에너지 공급 사업자, 충전 인프라 개발 사업자 간의 협력은 산업용 분야 전반에 걸쳐 신뢰성 높은 차량 운영과 에너지 관리의 향상을 가능하게 하는 통합된 전동화 생태계 구축을 더욱 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 23억 달러 |

| 예측액 | 118억 달러 |

| CAGR | 18% |

리지드 덤프트럭 부문은 2025년에 58%의 시장 점유율을 차지하며, 2026-2035년 연평균 성장률(CAGR) 19%로 성장할 것으로 전망됩니다. 이 부문은 제조사들이 첨단 배터리 기술을 탑재한 완전 전기식 및 트롤리 보조 시스템으로 전환함에 따라 급속히 확산되고 있습니다. 광산 사업자들이 고부하 실제 운영 환경에서 그 성능을 입증함에 따라 배터리식 리지드 덤프트럭에 대한 신뢰도가 높아지고 있습니다. 대형 운송 솔루션의 전동화 전환이 진행되는 가운데, 대규모 자재 운송 용도에 적합하다는 점 때문에 리지드형에 대한 수요가 증가하고 있습니다.

리튬이온 배터리 부문은 2025년에 88%의 시장 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 17.6%로 성장할 것으로 전망됩니다. 리튬이온 기술은 기존의 대체 기술에 비해 에너지 밀도가 높고, 충전 속도가 빠르며, 수명 주기 성능이 향상되었으므로 계속해서 시장을 독점하고 있습니다. 이러한 장점 덕분에, 가혹한 환경에서 운행되는 전동 덤프트럭에 있으며, 리튬이온 배터리는 최적의 동력원이 되고 있습니다. 그 결과, 각 제조사들은 광업 및 건설 현장의 가혹한 가동 조건에서도 안전하고 효율적인 성능을 확보하기 위해 첨단 배터리 열 관리 시스템의 도입을 가속화하고 있습니다.

2025년, 중국의 전기 덤프트럭 시장 규모는 6억 6,300만 달러에 달했습니다. 이 국가의 선도적 지위는 강력한 국내 제조 능력과 정부의 지원에 힘입어, 전동 및 자율주행형 광산 차량의 대규모 도입에 의해 주도되고 있습니다. BYD, XCMG, SANY 등 주요 기업은 통합된 배터리 공급망과 규모의 경제의 혜택을 누리고 있으며, 비용 경쟁력이 있는 제품을 제공할 수 있게 되었습니다. 또한 중국은 인프라 관련 산업 구상을 통해 동남아시아, 중앙아시아, 아프리카의 국제 광업 시장에서 영향력을 확대하고 있으며, 전기식 대형 차량 솔루션 분야에서 전 세계적인 입지를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 트럭별, 2022-2035년

제6장 시장 추산·예측 : 용량별, 2022-2035년

제7장 시장 추산·예측 : 배터리별, 2022-2035년

제8장 시장 추산·예측 : 추진력별, 2022-2035년

제9장 시장 추산·예측 : 용도별, 2022-2035년

제10장 시장 추산·예측 : 지역별, 2022-2035년

제11장 기업 개요

KSA 26.06.24The Global Electric Dump Trucks Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 18% to reach USD 11.8 billion by 2035.

The market is undergoing rapid transformation as electrification gains momentum across heavy-duty off-highway vehicles. Improvements in battery performance, including higher energy density and lower production costs, are significantly improving the commercial viability of electric dump trucks. These advancements are enhancing vehicle range, durability, and operational efficiency, allowing electric models to compete more effectively with conventional diesel-powered alternatives. In addition, lower operating and maintenance requirements compared to internal combustion engine vehicles are accelerating adoption across the mining and construction industries. The shift toward battery electric heavy-duty trucks is being reinforced by tightening environmental regulations, rising fuel costs, and increasing pressure to reduce lifecycle operating expenses. The growing development of charging infrastructure is also playing a critical role, particularly in large-scale mining and construction operations where continuous power availability is essential. Collaboration among fleet operators, energy providers, and charging infrastructure developers is further supporting the creation of integrated electrification ecosystems that enable reliable fleet operations and improved energy management across industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $11.8 Billion |

| CAGR | 18% |

The rigid dump truck segment accounted for 58% share in 2025 and is projected to grow at a CAGR of 19% from 2026 to 2035. This segment is witnessing strong adoption as manufacturers transition toward fully electric and trolley-assisted systems powered by advanced battery technologies. Confidence in battery electric rigid dump trucks is increasing as mining operators validate their performance in high-load, real-world operational environments. The ongoing shift toward electrified heavy-duty hauling solutions is strengthening demand for rigid configurations due to their suitability for large-scale material transport applications.

The lithium-ion battery segment held 88% share in 2025 and is expected to grow at a CAGR of 17.6% through 2035. Lithium-ion technology continues to dominate due to its superior energy density, faster charging capability, and improved lifecycle performance compared to conventional alternatives. These advantages make it the preferred power source for electric dump trucks operating in demanding environments. As a result, manufacturers are increasingly integrating advanced battery thermal management systems to ensure safe and efficient performance under extreme operating conditions in mining and construction applications.

China Electric Dump Trucks Market generated USD 663 million in 2025. The country's leadership is driven by large-scale deployments of electric and autonomous mining vehicles, supported by strong domestic manufacturing capabilities and government backing. Leading manufacturers such as BYD Company, XCMG, and SANY benefit from integrated battery supply chains and economies of scale, enabling cost-competitive product offerings. China is also expanding its influence in international mining markets across Southeast Asia, Central Asia, and Africa through infrastructure-linked industrial initiatives, further strengthening its global footprint in electric heavy-duty vehicle solutions.

Key companies operating in the Global Electric Dump Trucks Industry include AB Volvo, BYD Company, Caterpillar, Hitachi Construction Machinery, Komatsu, Liebherr, Mercedes-Benz, SANY, Scania, and XCMG. Companies operating in the electric dump trucks market are adopting a range of strategic initiatives to strengthen their competitive positioning and expand global reach. Leading players are investing heavily in battery innovation, vehicle electrification platforms, and high-efficiency powertrain systems to improve operational performance and reduce total cost of ownership. Strategic collaborations with mining operators, energy providers, and infrastructure developers are helping accelerate the deployment of integrated charging ecosystems. Manufacturers are also expanding production capabilities and enhancing supply chain integration to improve cost efficiency and scalability. In addition, firms are focusing on product validation through real-world testing in harsh mining and construction environments to build market confidence. Continuous innovation in battery thermal management, autonomous integration, and fleet optimization technologies is further reinforcing long-term market competitiveness and adoption of electric dump truck solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Truck

- 2.2.2 Capacity

- 2.2.3 Battery

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for low-emission heavy-duty mining and construction operations

- 3.2.1.2 Increasing fuel cost volatility and diesel operating expenses

- 3.2.1.3 Government regulations targeting decarbonization of off-highway vehicles

- 3.2.1.4 Advancements in high-capacity battery and fast-changing technologies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront cost of electric dump trucks

- 3.2.2.2 Limited charging infrastructure in mining and remote sites

- 3.2.3 Market opportunities

- 3.2.3.1 Shift toward fully battery electric dump trucks in mining operations

- 3.2.3.2 Integration of autonomous and connected fleet systems

- 3.2.3.3 Development of battery swapping and modular charging infrastructure

- 3.2.3.4 Increasing deployment of smart energy management systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 ACT Regulation

- 3.5.1.2 EPA Phase 3

- 3.5.2 Europe

- 3.5.2.1 CO2 Emission Standards

- 3.5.2.2 Euro 6/Next Generation Standards

- 3.5.3 Asia-Pacific

- 3.5.3.1 Emission Reduction Targets

- 3.5.3.2 China-6 Standard

- 3.5.4 Latin America

- 3.5.4.1 Brazil Proconve P8

- 3.5.4.2 Mexico EPA-Aligned Standards

- 3.5.5 MEA

- 3.5.5.1 Saudi Vision 2030 Green Initiatives

- 3.5.5.2 South Africa EV Tax Rebates

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Capacity & production landscape (Driven by Primary Research)

- 3.10.1 Installed capacity by region & key producer

- 3.10.2 Capacity utilization rates & expansion pipelines

- 3.11 Trade data analysis (Driven by Paid Research)

- 3.11.1 Intra Trade Flows - Volume & Value Trends

- 3.11.2 Import/Export Corridor Analysis

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 Automated design optimization

- 3.12.3 Supply chain AI for demand forecasting

- 3.12.4 GenAI use cases & adoption roadmap by segment

- 3.12.5 Risks, Limitations & Regulatory Considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Truck, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Rigid Dump Trucks

- 5.3 Articulated Dump Trucks

Chapter 6 Market Estimates & Forecast, By Capacity, 2022 - 2035 ($Mn, units)

- 6.1 Key trends

- 6.2 Below 50 Tons

- 6.3 50-100 Tons

- 6.4 Above 100 Tons

Chapter 7 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Lithium-ion

- 7.3 Lead-acid

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Battery Electric

- 8.3 Hybrid Electric

- 8.4 Fuel Cell Electric

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Mining

- 9.3 Construction

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 AB Volvo

- 11.1.2 BYD Company

- 11.1.3 Caterpillar

- 11.1.4 Hitachi Construction Machinery

- 11.1.5 Komatsu

- 11.1.6 Liebherr

- 11.1.7 Mercedes-Benz

- 11.1.8 PACCAR

- 11.1.9 SANY

- 11.1.10 Scania CV

- 11.1.11 XCMG

- 11.2 Regional players

- 11.2.1 Edison

- 11.2.2 Inner Mongolia North Hauler

- 11.2.3 LiuGong Machinery

- 11.2.4 Xiangtan Electric Manufacturing

- 11.2.5 Yutong Heavy Industries

- 11.2.6 Zoomlion

- 11.3 Emerging players

- 11.3.1 International Motors

- 11.3.2 Rivian

- 11.3.3 Shaanxi Tonly Heavy Industries