|

시장보고서

상품코드

1910884

광업용 덤프 트럭 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mining Dump Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

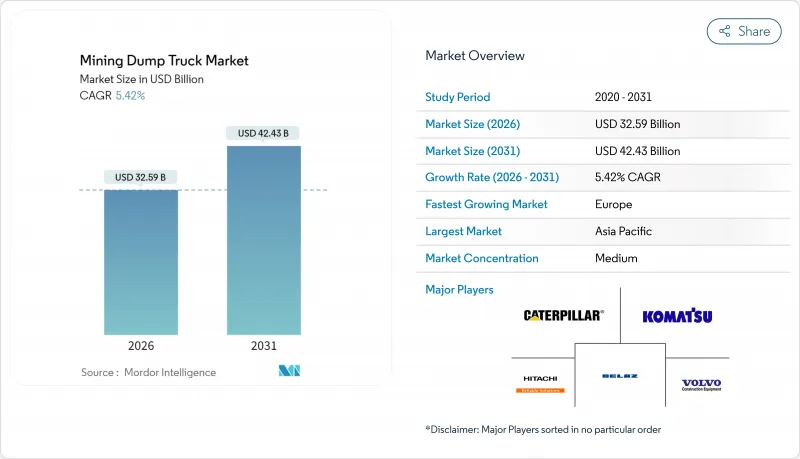

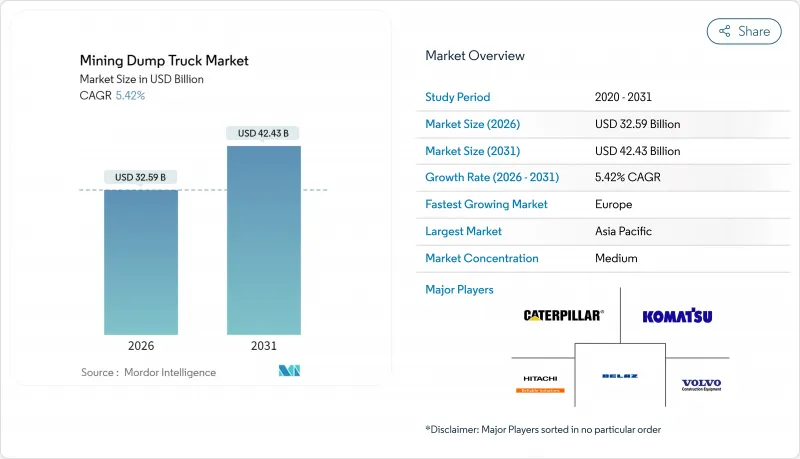

세계의 광업용 덤프 트럭 시장은 2025년에 309억 1,000만 달러로 평가되었으며, 2026년 325억 9,000만 달러에서 2031년까지 424억 3,000만 달러에 이를 것으로 예상됩니다. 예측 기간(2026-2031년)의 CAGR은 5.42%를 나타낼 것으로 전망됩니다.

자율주행 기술에 대한 투자 확대, 배터리 전기 구동으로의 이행, 그리고 보다 엄격한 스테이지 V 및 티어 5 규제의 시행이 수요 증가를 견인하는 3개의 기둥이 되고 있습니다. 아시아태평양은 중국·인도·인도네시아에서 노천굴굴 광산의 생산 확대에 의해 압도적인 우위성을 유지하는 한편, 유럽에서는 배출가스 규제에 따른 차량 갱신을 배경으로 가장 급속한 성장을 기록하고 있습니다. 장비 제조업체는 적재 킬로미터 생산성을 향상시키고 연료 소비를 줄이는 통합 디지털 플랫폼 개발에 주력하고 있습니다. 톤당 비용 연동형 리스 모델과 채굴에서 제련까지의 최적화 툴은 자본 장벽을 줄여 중견 생산자에게도 최신 기술에 대한 액세스를 가능하게 하고 있습니다. Komatsu의 GHH 그룹 인수로 대표되는 M&A 활동은 풀 라인 지하 및 지상 설비 제공으로의 전환을 보여 주며 가격 주도형 경쟁에서 서비스 충실형 솔루션으로의 이행을 강조하고 있습니다.

세계의 광업용 덤프 트럭 시장 동향과 전망

Tier-4 및 Stage-V 배출 가스 규제 강화가 차량 갱신을 촉진

EU 산업 배출 지침은 오프로드 엔진의 미립자 배출을 줄이고 캘리포니아의 Tier 5 규정은 유사한 기준을 미국 광산으로 확대합니다. 구형 트럭의 개조는 단가가 높고 비용 효과의 관점에서 완전한 갱신이 유리합니다. 리오 틴트와 같은 사업자는 충전 네트워크가 성숙할 때까지의 잠정 규칙에 대응하기 위해 듀얼 연료 시스템과 하이브리드 시스템을 추가 도입하고 있습니다. 벌칙이 다가오는 가운데 규제 준수 타임라인은 구매 사이클을 단축하고 클린텍 트럭의 단기 주문을 밀어 올리고 있습니다. 배출 감축과 생산성 향상의 양립을 목표로 하는 차량 갱신의 움직임이 광업용 덤프 트럭 시장에 직접적인 수요를 가져오고 있습니다.

자율주행에 의한 적재 킬로 생산성 향상 실증

고마츠의 AHS(자동 운반 시스템)는 23광산에서 700대 이상이 가동되어 리오틴트의 필바라 네트워크에서는 1대당 생산성 향상과 유지 보수 비용 절감이 보고되었습니다. 24시간 가동에 의해 오퍼레이터의 피로 제약이 해소되어 사고 발생률이 대폭 저하. 캐터필러의 "Command for Hauling"은 실시간 광석 품위에 따라 덤프 트럭을 굴삭기 작업에 할당하여 대기 시간을 단축하고 제련소의 처리 능력을 향상시킵니다. 고생산 광산에서는 도입 비용을 2년 이내에 회수할 수 있어 자율 기능은 시험 운용 단계에서 주류 사양으로 이행하고 있습니다. 안전성, 가동률, 단위 비용의 향상에 의해 자율 기능은 신규 입찰 서류에 있어서 필수 요건으로서 확고한 지위를 구축하고 있습니다.

초기설비투자액의 높이와 회수기간의 길이

초대형 트럭에는 연료, 타이어, 유지 보수를 포함한 초기 투자로 300만-600만 달러, 10년간 1,500만-2,000만 달러의 비용이 듭니다. 타이어만으로도 연간 많은 투자가 발생합니다. 배터리식 전기로의 전환에는 충전기나 축전 설비의 추가 비용이 듭니다만, 에너지 절약 효과에 의해 회수 기간은 4-6년으로 단축됩니다. 재무기반이 취약한 중소광산업체는 업그레이드를 앞당기는 경향이 있어 조기 도입률을 억제하고 있습니다. 현재 대출액은 광산 운영 총 비용의 15-20%를 차지하고 있으며, 자본 조달 여부는 광업용 덤프 트럭 시장의 성장 곡선을 좌우하는 결정적 요인이 되고 있습니다.

부문 분석

2025년 시점에서 리지드 후방 덤프 트럭은 광업용 덤프 트럭 시장 점유율의 48.70%를 차지했으며, 석탄·철광석·채석장 등 폭넓은 용도로의 유용성을 반영했습니다. 자율주행 하위 부문은 현시점에서는 규모가 작은 것, 호주·칠레·캐나다의 광산에서 24시간 무인 운전으로의 전환이 진행되는 가운데, CAGR 11.05%를 나타낼 전망입니다. 자율주행 차량의 광업용 덤프 트럭 시장 규모는 트럭 가동률 향상과 유지 보수 비용 절감을 배경으로 2030년대 초반까지 리지드 후방 덤프의 수익 규모에 필적할 것으로 예측됩니다.

생산성 향상 효과는 Komatsu AHS 및 캐터필러 명령과 같은 시스템에서 파생됩니다. 이들은 운반 사이클의 배차, 타이어 감시, 충돌 회피를 자동화합니다. 운영자는 이러한 장점을 최대한 활용하기 위해 고대역폭의 전체 사이트 네트워크와 원격 운영 센터의 도입에 주력하고 있습니다. 리지드 측면 덤프 및 굴절식 형식은 적재량보다 기동성이 우선되는 협맥광상 및 연약지반 용도를 위한 틈새 시장으로 존속합니다. 인프라 비용에도 불구하고 자율운전의 투자회수 효과는 충분히 설득력이 있어, 신규 입찰 서류에서는 표준 장비로 지정되는 케이스가 증가. 이를 통해 광업용 덤프 트럭 시장은 자동화 옵션으로 더욱 기울어지고 있습니다.

2025년 성숙한 공급망과 높은 에너지 밀도를 바탕으로 내연기관 디젤 유닛이 광업용 덤프 트럭 시장의 68.73%를 차지했습니다. 배터리 전기식 대체기는 CAGR 9.88%로 확대되고 있으며 탄소가격 설정의 진전에 따라 2031년까지 광업용 덤프 트럭 시장 규모에 현저한 공헌을 할 것으로 예측되고 있습니다.

초기 전동화 도입은 연간 가동시간이 4,000시간을 넘는 구리·금광산에 집중하고 있어 총소유비용이 디젤차를 밑돌게 됩니다. XCMG사가 포트에스크사와 체결한 240톤급 배터리 트럭 12억 달러 규모의 계약은 경제성이 입증되는 대로 주요 광산 기업이 주문 규모를 확대하는 실례를 보여줍니다. 하이브리드 자동차와 수소차는 과도기를 채우는 옵션이 되어 심방전 충전 네트워크를 필요로 하지 않고 단계적인 연료비 절감을 실현합니다. EU 및 캘리포니아 주 규제 기한은 강제력으로 작용하여 전기식 및 하이브리드식의 보급이 광업용 덤프 트럭 시장의 구조적 추진력으로 지속되도록 합니다.

지역별 분석

2025년 시점에서 아시아태평양은 광업용 덤프 트럭 시장의 57.76%를 차지해 중국의 설비 제조 에코시스템, 인도의 석탄 생산 증가, 인도네시아의 전지 금속 수요 증가가 기반이 되었습니다. XCMG나 Sany 등 국내 브랜드는 규모와 지리적 우위성을 살려 수주를 획득. 한편, 호주는 자율주행차대의 세계적 도입을 주도하고, 다른 지역에서 채용되는 모범 사례를 형성하고 있습니다.

유럽은 2031년까지 6.26%라는 최고 CAGR을 나타낼 전망입니다. 스테이지 V 규제 타임라인은 디젤 차량의 급격한 교체를 촉진하고 탄소 크레딧의 현금화는 배터리 구동 트럭의 수익성을 높이고 있습니다. 스웨덴과 핀란드의 광산 회사는 완전 배터리 전기화로의 길을 선도. 볼리덴은 2030년까지 탄소 중립 트럭 도입을 목표로 하여 지역의 깊은 헌신을 보여주고 있습니다.

북미에서는 특히 네바다주의 금광산과 애리조나주의 구리광산 거점에서 꾸준한 대체 수요가 보이며, 광산에서 제련소까지의 소프트웨어 도입률로 선두를 차지하고 있습니다. 남미에서는 칠레와 페루를 중심으로 비용 곡선을 보호하기 위해 초대형 차량의 플릿 규모를 확대하고 있습니다. 한편 중동 및 아프리카에서는 신규 파이프라인 개발 가능성이 열려 있지만, 송전망 인프라의 지연으로 인해 이들 지역에서의 광업용 덤프 트럭 시장의 단기적인 성장은 억제되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- Tier-4 및 Stage-V 배출 가스 규제의 강화가 차량 갱신을 촉진

- 자율 주행 운반 기술이 적재 킬로 생산성의 향상을 실증

- 아시아태평양에서의 노천굴굴 광산 생산량 확대

- 광산에서 제련소까지의 최적화/적재량 데이터와 제련소 처리 능력의 연동

- 초대형 트럭용 톤당 리스 모델에 의한 설비 투자 삭감

- 배터리식 전기 덤프 트럭용 탄소배출권의 현금화

- 시장 성장 억제요인

- 초기 투자액의 높이와 회수 기간의 길이

- 상품 가격의 변동이 신규 광산 개발을 지연

- 원격지에서의 취약한 송전망 용량이 전화를 지연

- 500kWh 초배터리 팩용 리튬 이온 배터리 공급망 위험

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(단위))

- 트럭 유형별

- 리지드 후방 덤프 트럭

- 리지드 측면 덤프 트럭

- 굴절식 덤프 트럭

- 하부 및 배면 덤프 트럭

- 자율 주행 덤프 트럭(AHS 지원)

- 연료 및 추진 방식별

- 내연기관(디젤)

- 하이브리드(디젤-전기)

- 배터리식 전기자동차

- 수소 연료전지

- 적재량별

- 150메트릭톤 미만

- 150-200메트릭톤

- 201-330메트릭톤

- 330메트릭톤 이상

- 용도별

- 노천 금속 채굴

- 석탄 및 갈탄 채굴

- 채석 및 골재

- 주요 인프라 건설

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 호주

- 인도네시아

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Liebherr Group

- BelAZ

- Volvo Construction Equipment

- SANY Heavy Industry Co., Ltd.

- Epiroc AB

- Sandvik AB

- HD Hyundai Infracore Co., Ltd.

- Xuzhou Construction Machinery Group Co., Ltd.

- Bell Equipment

- Shaanxi Tonly Heavy Industries Co., Ltd.

- Ashok Leyland Limited

- Guangxi LiuGong Machinery Co., Ltd.

- Daimler Truck AG

제7장 시장 기회와 향후 전망

KTH 26.01.26The global mining dump truck market was valued at USD 30.91 billion in 2025 and estimated to grow from USD 32.59 billion in 2026 to reach USD 42.43 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031).

Surging investments in autonomous haulage, the switch to battery-electric propulsion, and stricter Stage V and Tier 5 rules are the three pillars pushing demand higher. Asia-Pacific keeps a commanding lead because surface mines in China, India, and Indonesia scale output, while Europe registers the quickest gains on the back of emission-related fleet renewal. Equipment makers focus on integrated digital platforms that raise payload-kilometer productivity and trim fuel burn. Leasing models tied to cost-per-ton and mine-to-mill optimization tools lower capital hurdles and make the latest technology accessible to mid-tier producers. M&A activity, highlighted by Komatsu's purchase of GHH Group, signals a turn toward full-line underground and surface offerings and underscores the shift from price-led competition toward service-rich solutions.

Global Mining Dump Truck Market Trends and Insights

Tightening Tier-4 and Stage-V Emission Norms Drive Fleet Renewal

The EU Industrial Emissions Directive cuts particulate output from off-road engines, while California's Tier 5 package extends similar thresholds to mines in the United States . Retrofitting older trucks has high costs per unit, tilting the cost-benefit equation toward full replacement. Operators such as Rio Tinto add dual-fuel and hybrid systems to meet interim rules as charging networks mature. With penalties looming ahead, the compliance timetable tightens purchasing cycles and lifts near-term order books for clean-tech trucks. The replacement wave directly feeds the mining dump truck market as fleets look to pair emission cuts with productivity upgrades.

Autonomous Haulage Proven to Raise Payload-km Productivity

Komatsu's AHS has over 700 units running across 23 mines, and Rio Tinto's Pilbara network reports extra productivity and lower maintenance per truck . Around-the-clock operation removes operator fatigue constraints and cuts incident rates significantly. Caterpillar's Command for Hauling allocates trucks to shovel assignments based on real-time ore grade, shrinking idle time, and improving mill throughput. High-volume mines recoup conversion costs within two years, propelling autonomous functionality from pilot stage to mainstream specification. Gains in safety, utilization, and unit cost cement autonomy as a non-negotiable feature in new tender documents.

High Upfront Capex and Long Payback Cycles

An ultra-class truck demands USD 3-6 million in capital and USD 15-20 million over a decade once fuel, tires, and maintenance are folded in. Tires alone can incur high investments annually. Battery-electric conversions tack on significant cost for chargers and storage but promise energy savings, stretching payback to 4-6 years. Smaller miners with thin balance sheets often defer upgrades, limiting early adoption rates. Financing now measures 15-20% of total mine operating cost, making capital availability a decisive factor in the mining dump truck market's growth slope.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Surface-Mine Output in Asia-Pacific

- Mine-to-Mill Optimization Linking Payload Data to Mill Throughput

- Commodity-Price Volatility Delaying Green-Field Mines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid rear-dump trucks commanded 48.70% of the mining dump truck market share in 2025, reflecting their broad utility across coal, iron ore, and quarry operations. The autonomous sub-segment, while smaller today, is scaling at an 11.05% CAGR as sites in Australia, Chile, and Canada convert fleets to 24-hour driverless operation. The mining dump truck market size for autonomous fleets is projected to match rigid rear-dump revenue by the early 2030s, driven by higher truck utilization and lower maintenance.

Productivity benefits stem from systems such as Komatsu AHS and Caterpillar Command that automate haul cycle dispatch, tire monitoring, and collision avoidance. Operators commit to high-bandwidth sitewide networks and remote-operation centers to unlock these gains. Rigid side-dump and articulated formats remain niche, serving narrow-vein or soft-ground applications where maneuverability overrides payload. Despite infrastructure costs, the payback for autonomy proves compelling enough that new tender documents increasingly specify the feature as standard, further tilting the mining dump truck market toward automated options.

Internal-combustion diesel units held 68.73% of the mining dump truck market share in 2025, supported by mature supply chains and high energy density. Battery-electric alternatives are expanding at a 9.88% CAGR and are forecast to account for a notable contribution to the mining dump truck market size by 2031 as carbon pricing lifts.

Early electric deployments focus on copper and gold pits where high utilization surpasses 4,000 hours annually, pushing total cost of ownership below that of diesel. XCMG's USD 1.2 billion agreement with Fortescue for 240-t battery trucks illustrates how major miners scale orders once economics prove viable. Hybrid and hydrogen pathways fill the transition gap, offering incremental fuel savings without deep-cycle charging networks. Regulatory deadlines in the EU and California act as forcing functions, ensuring electric and hybrid penetration remains a structural, rather than cyclical, driver of the mining dump truck market.

The Global Mining Dump Truck Market Report is Segmented by Truck Type (Rigid Rear-Dump, Rigid Side-Dump, and More), Fuel/Propulsion Type (Internal-Combustion (Diesel), Hybrid (Diesel-Electric), and More), Payload Capacity (Below 150 Metric Tons, 150-200 Metric Tons, and More), Application (Open-Pit Metal Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific held 57.76% of the mining dump truck market share in 2025, anchored by China's equipment manufacturing ecosystem, India's rising coal output, and Indonesia's battery-metal growth. Domestic brands such as XCMG and Sany exploit scale and proximity to win contracts, while Australia leads global deployment of autonomous fleets, shaping best practices taken up elsewhere.

Europe records the highest 6.26% CAGR to 2031 as Stage V timelines compel rapid diesel replacement and carbon-credit monetization sweetens returns on battery trucks. Miners in Sweden and Finland pioneer full battery-electric pathways; Boliden targets carbon-neutral trucks by 2030, signaling deep regional commitment.

North America shows steady replacement demand, especially in Nevada gold and Arizona copper hubs, and ranks first in mine-to-mill software adoption. South America, centered on Chile and Peru, scales ultra-class fleets to protect cost curves, while the Middle East and Africa unlock greenfield pipeline potential but lag on grid infrastructure, tempering short-term mining dump truck market growth in those regions.

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Liebherr Group

- BelAZ

- Volvo Construction Equipment

- SANY Heavy Industry Co., Ltd.

- Epiroc AB

- Sandvik AB

- HD Hyundai Infracore Co., Ltd.

- Xuzhou Construction Machinery Group Co., Ltd.

- Bell Equipment

- Shaanxi Tonly Heavy Industries Co., Ltd.

- Ashok Leyland Limited

- Guangxi LiuGong Machinery Co., Ltd.

- Daimler Truck AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Tier-4 and Stage-V Emission Norms Drive Fleet Renewal

- 4.2.2 Autonomous Haulage Proven to Raise Payload-km Productivity

- 4.2.3 Expansion of Surface-Mine Output in Asia-Pacific

- 4.2.4 Mine-to-Mill Optimization Linking Payload Data to Mill Throughput

- 4.2.5 Pay-per-Ton Leasing Models for Ultra-Class Trucks Cut Capex

- 4.2.6 Carbon-Credit Monetization for Battery-Electric Dump Trucks

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex and Long Payback Cycles

- 4.3.2 Commodity-Price Volatility Delaying Green-Field Mines

- 4.3.3 Weak Grid Capacity in Remote Sites Slows Electrification

- 4.3.4 Li-ion Supply-Chain Risk for Above 500 kWh Battery Packs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Truck Type

- 5.1.1 Rigid Rear-Dump Trucks

- 5.1.2 Rigid Side-Dump Trucks

- 5.1.3 Articulated Dump Trucks

- 5.1.4 Bottom/Belly Dump Trucks

- 5.1.5 Autonomous Dump Trucks (AHS-ready)

- 5.2 By Fuel/Propulsion Type

- 5.2.1 Internal-Combustion (Diesel)

- 5.2.2 Hybrid (Diesel-Electric)

- 5.2.3 Battery-Electric

- 5.2.4 Hydrogen Fuel-Cell

- 5.3 By Payload Capacity

- 5.3.1 Below 150 metric tons

- 5.3.2 150-200 metric tons

- 5.3.3 201-330 metric tons

- 5.3.4 Above 330 metric tons

- 5.4 By Application

- 5.4.1 Open-pit Metal Mining

- 5.4.2 Coal and Lignite Mining

- 5.4.3 Quarrying and Aggregates

- 5.4.4 Major Infrastructure Construction

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Chile

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Indonesia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Hitachi Construction Machinery Co., Ltd.

- 6.4.4 Liebherr Group

- 6.4.5 BelAZ

- 6.4.6 Volvo Construction Equipment

- 6.4.7 SANY Heavy Industry Co., Ltd.

- 6.4.8 Epiroc AB

- 6.4.9 Sandvik AB

- 6.4.10 HD Hyundai Infracore Co., Ltd.

- 6.4.11 Xuzhou Construction Machinery Group Co., Ltd.

- 6.4.12 Bell Equipment

- 6.4.13 Shaanxi Tonly Heavy Industries Co., Ltd.

- 6.4.14 Ashok Leyland Limited

- 6.4.15 Guangxi LiuGong Machinery Co., Ltd.

- 6.4.16 Daimler Truck AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment