|

시장보고서

상품코드

2061465

다층형 C-UAS 아키텍처 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Layered C-UAS Architecture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

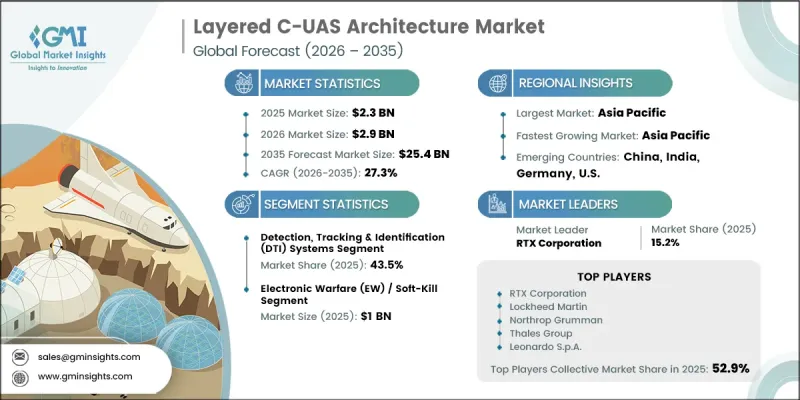

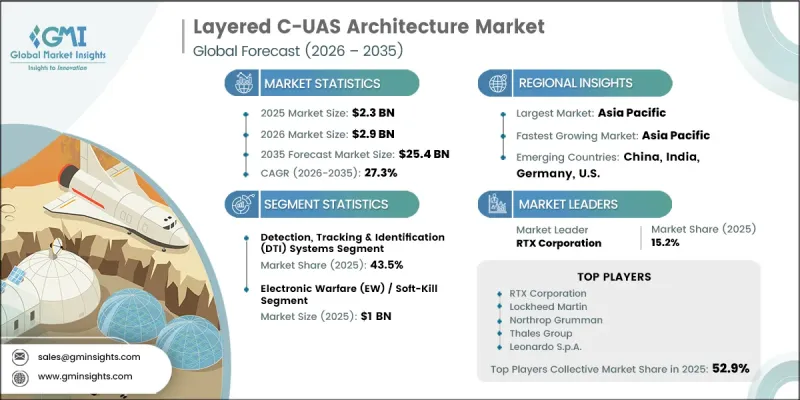

세계의 다층형 C-UAS 아키텍처 시장은 2025년에 23억 달러로 평가되며, 2035년까지 CAGR 27.3%로 성장하며, 254억 달러에 달할 것으로 추정되고 있습니다.

다층형 C-UAS 아키텍처 산업의 확대는 단일 대책이 아닌 포괄적인 방어 전략이 필요한 무인 항공기에 의한 위협의 고도화, 빈발화, 다양화에 의해 주도되고 있습니다. 기밀 자산을 보호하는 조직들은 탐지, 추적, 식별 및 대응 기능의 전 범위를 지원할 수 있는 통합 시스템의 도입을 점점 더 확대하고 있습니다. 방위 기관, 중요 인프라 시설 및 공공 부문 전반의 업무에 대한 보안 요구 사항이 높아짐에 따라 시장 성장이 더욱 가속화되고 있습니다. 또한 국토안보 프로그램과 국방 현대화 구상에 대한 지속적인 투자가 첨단 드론 대응 기술에 대한 강력한 수요를 창출하고 있습니다. 센서 네트워크, 지휘통제 플랫폼 및 데이터 처리 능력 분야의 기술적 진보 또한 다층 방어 아키텍처의 유효성과 신뢰성을 높이고 있습니다. 위협 환경이 점점 더 복잡해지는 가운데, 조직들은 운영 효율성을 유지하면서 여러 위협 시나리오에 대응할 수 있는 확장성과 상호 운용성을 갖춘 솔루션을 우선적으로 선택하고 있습니다. 정부와 보안 기관들이 영공 보호 역량을 지속적으로 강화함에 따라 이러한 요인들로 인해 다층형 C-UAS 아키텍처 시장은 장기적으로 상당한 성장이 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 23억 달러 |

| 예측액 | 254억 달러 |

| CAGR | 27.3% |

다층형 대-UAS(C-UAS) 아키텍처 시장은 진화하는 무인항공기로 인한 위협이 광범위한 운영상 과제를 해결할 수 있는 통합 방어 프레임워크에 대한 수요를 높이고 있으며, 성장세를 보이고 있습니다. 첨단 드론 기술의 활용이 확대됨에 따라 고립된 대응 시스템의 한계가 부각되면서, 상황 인식을 향상시키고 위협에 대한 협력적 대응을 목적으로 하는 다층형 아키텍처의 도입이 진행되고 있습니다. 국가 안보에 대한 정부의 관심이 높아지고, 국방비가 증가하며, 치안 기관 간의 협력이 강화됨에 따라 포괄적인 대무인항공기(UAS) 솔루션이 광범위하게 도입되고 있습니다. 동시에, 센서 기술, 지휘통제시스템 및 상호운용 능력의 발전으로 인해 작전 수행 능력이 향상되고, 다층 방어 네트워크의 효과성이 강화되고 있습니다.

지휘·통제 및 데이터 융합(C2/DF) 플랫폼 부문은 예측 기간 중 연평균 성장률(CAGR) 29.3%로 성장할 것으로 전망됩니다. 이 부문의 성장은 현대의 무인항공기(UAS) 대응 환경이 점점 더 복잡해지고 있으며, 여러 탐지 및 대응 시스템에서 얻은 정보를 통합해야 할 필요성이 커지고 있기 때문입니다. 다층 방어 아키텍처가 고도화됨에 따라 조직들은 실시간 정보 처리, 자동화된 의사결정 지원, 그리고 여러 운영 계층에 걸친 협력적 대응을 지원하는 중앙 집중형 플랫폼에 대한 투자를 확대하고 있습니다. 이러한 기능들은 상황 인식 능력을 향상시키고 시스템 전반의 성능을 강화하는 데 필수적인 요소로 자리 잡고 있습니다.

하이브리드 및 통합 시스템 부문은 2026-2035년 연평균 성장률(CAGR) 28.1%를 기록할 것으로 전망됩니다. 이 부문의 성장은 다양한 환경에서 운용 가능한, 유연하고 적응성이 뛰어난 대드론(UAS) 솔루션에 대한 수요 증가에 힘입고 있습니다. 점점 더 고도화되는 공중 위협 시나리오에 따라 통합된 운용 프레임워크 하에서 여러 방어 계층을 통합하는 아키텍처의 도입이 확대되고 있습니다. 집중 관리 시스템을 통해 고정 자산과 배치 가능한 자산을 조정할 수 있는 능력은 대응의 효율성을 높여, 국방 및 보안 분야에서 더 광범위한 도입을 촉진하고 있습니다.

북미의 다층형 대 UAS 아키텍처 시장은 2025년에 31.4%의 점유율을 차지했습니다. 이 지역의 성장은 국토 안보, 영공 보호, 국경 감시 및 중요 인프라 방어에 대한 우선순위가 높아짐에 따라 주도되고 있습니다. 무허가 항공 활동에 대한 우려가 커짐에 따라 다양한 운용 환경에서 포괄적인 보호를 제공할 수 있는 첨단 대UAS 솔루션에 대한 수요가 증가하고 있습니다. 정부의 막대한 투자, 대규모 국방 현대화 프로그램, 그리고 연방 기관 간의 협력 강화가 해당 지역 전체에 걸쳐 다층형 대무인항공기(UAS) 아키텍처의 도입을 더욱 촉진하고 있습니다. 이러한 요인들로 인해 북미는 첨단 공역 보안 기술의 주요 시장으로서의 입지를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 컴포넌트 유형별, 2022-2035년

제6장 시장 추산·예측 : 완화 기술 유형별, 2022-2035년

제7장 시장 추산·예측 : 도입 아키텍처별, 2022-2035년

제8장 시장 추산·예측 : 최종사용자별, 2022-2035년

제9장 시장 추산·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.24The Global Layered C-UAS Architecture Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 27.3% to reach USD 25.4 billion by 2035.

Expansion of the layered C-UAS architecture industry is driven by the growing sophistication, frequency, and diversity of unmanned aerial threats that require comprehensive defense strategies rather than standalone countermeasures. Organizations responsible for protecting sensitive assets are increasingly adopting integrated systems capable of supporting the full spectrum of detection, tracking, identification, and mitigation functions. Rising security requirements across defense establishments, critical infrastructure facilities, and public-sector operations are further accelerating market growth. In addition, continued investments in homeland security programs and defense modernization initiatives are creating strong demand for advanced counter-drone technologies. Technological advancements in sensor networks, command-and-control platforms, and data processing capabilities are also improving the effectiveness and reliability of layered defense architectures. As threat environments become more complex, organizations are prioritizing scalable and interoperable solutions that can respond to multiple threat scenarios while maintaining operational efficiency. These factors are positioning the layered C-UAS architecture market for substantial long-term expansion as governments and security organizations continue strengthening airspace protection capabilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $25.4 Billion |

| CAGR | 27.3% |

The layered C-UAS architecture market is gaining momentum as evolving unmanned aerial threats create increasing demand for integrated defense frameworks capable of addressing a broad range of operational challenges. The growing use of advanced drone technologies has highlighted the limitations of isolated countermeasure systems, prompting greater adoption of multi-layered architectures designed to provide enhanced situational awareness and coordinated threat response. Increased government focus on national security, rising defense expenditures, and stronger collaboration among security agencies are contributing to the broader implementation of comprehensive counter-UAS solutions. At the same time, advancements in sensor technologies, command-and-control systems, and interoperability capabilities are improving operational performance and strengthening the effectiveness of layered defense networks.

The command, control, and data fusion (C2/DF) platforms segment is projected to grow at a CAGR of 29.3% throughout the forecast period. Growth within this segment is driven by the increasing complexity of modern counter-UAS environments and the growing requirement to integrate information from multiple detection and mitigation systems. As layered defense architectures become more sophisticated, organizations are investing in centralized platforms that support real-time information processing, automated decision support, and coordinated responses across multiple operational layers. These capabilities are becoming essential for improving situational awareness and enhancing overall system performance.

The hybrid and integrated systems segment is anticipated to register a CAGR of 28.1% during 2026-2035. Segment growth is supported by the rising need for flexible and adaptive counter-UAS solutions capable of operating across diverse environments. Increasingly advanced aerial threat scenarios are encouraging adoption of integrated architectures that combine multiple defense layers under a unified operational framework. The ability to coordinate fixed and deployable assets through centralized management systems is improving response effectiveness and supporting wider adoption across defense and security applications.

North America Layered C-UAS Architecture Market accounted for 31.4% share in 2025. Regional growth is driven by heightened priorities surrounding homeland security, airspace protection, border monitoring, and critical infrastructure defense. Growing concerns related to unauthorized aerial activity have increased demand for advanced counter-UAS solutions capable of providing comprehensive protection across a range of operational environments. Significant government investments, large-scale defense modernization programs, and enhanced coordination among federal agencies are further supporting the adoption of layered counter-UAS architectures throughout the region. These factors continue to strengthen North America's position as a key market for advanced airspace security technologies.

Major companies operating in the Global Layered C-UAS Architecture Industry include RTX Corporation, Lockheed Martin, Northrop Grumman, Thales Group, Leonardo S.p.A., Israel Aerospace Industries, Rafael Advanced Defense Systems, BAE Systems, Saab AB, Elbit Systems, Rheinmetall AG, L3Harris Technologies, Anduril Industries, DroneShield, and Dedrone. Companies competing in the layered C-UAS architecture market are implementing a variety of strategies to strengthen their market position and expand their competitive advantage. Significant investments in research and development are enabling organizations to enhance threat detection accuracy, improve sensor integration capabilities, and develop more advanced command-and-control platforms. Strategic collaborations with defense agencies, technology providers, and security organizations are accelerating innovation and expanding deployment opportunities. Market participants are also focusing on developing scalable and interoperable solutions capable of addressing evolving aerial threat environments. Portfolio expansion through acquisitions, technology partnerships, and product diversification remains a key growth strategy. In addition, companies are emphasizing artificial intelligence integration, real-time data analytics, and autonomous response capabilities to improve operational effectiveness, strengthen customer value propositions, and secure a stronger foothold within the rapidly growing layered C-UAS architecture market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 Mitigation technology type trends

- 2.2.3 Deployment architecture trends

- 2.2.4 End-User trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising frequency and complexity of drone threats

- 3.2.1.2 Shift toward integrated and networked defense systems

- 3.2.1.3 Growing protection requirements for critical infrastructure

- 3.2.1.4 Increased defense and homeland security spending

- 3.2.1.5 Advancements in sensor fusion and command-and-control technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory complexity and operational restrictions

- 3.2.2.2 High system integration cost and technical complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Commercial and civilian airspace security adoption

- 3.2.3.2 Export potential and allied defense collaboration programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Detection, tracking & identification (DTI) systems

- 5.3 Command, control & data fusion (C2/DF) platforms

- 5.4 Mitigation & neutralization systems

Chapter 6 Market Estimates and Forecast, By Mitigation Technology Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Kinetic/physical neutralization

- 6.3 Electronic warfare (EW) / soft-kill

- 6.4 Directed energy (DE) / hard-kill

Chapter 7 Market Estimates and Forecast, By Deployment Architecture, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Fixed / static systems

- 7.3 Mobile / portable systems

- 7.4 Hybrid / integrated systems

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Military & defense forces

- 8.3 Government security & border agencies

- 8.4 Critical infrastructure operators

- 8.5 Airport & aviation authorities

- 8.6 Commercial & private sector

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 RTX Corporation

- 10.1.2 Lockheed Martin

- 10.1.3 Northrop Grumman

- 10.1.4 Thales Group

- 10.1.5 Leonardo S.p.A.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 L3Harris Technologies

- 10.2.1.2 Anduril Industries

- 10.2.2 Europe

- 10.2.2.1 BAE Systems

- 10.2.2.2 Saab AB

- 10.2.2.3 Rheinmetall AG

- 10.2.3 Middle East & Africa

- 10.2.3.1 Israel Aerospace Industries

- 10.2.3.2 Rafael Advanced Defense Systems

- 10.2.3.3 Elbit Systems

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 DroneShield

- 10.3.2 Dedrone