|

시장보고서

상품코드

2061482

수소 발전기 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Hydrogen Powered Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

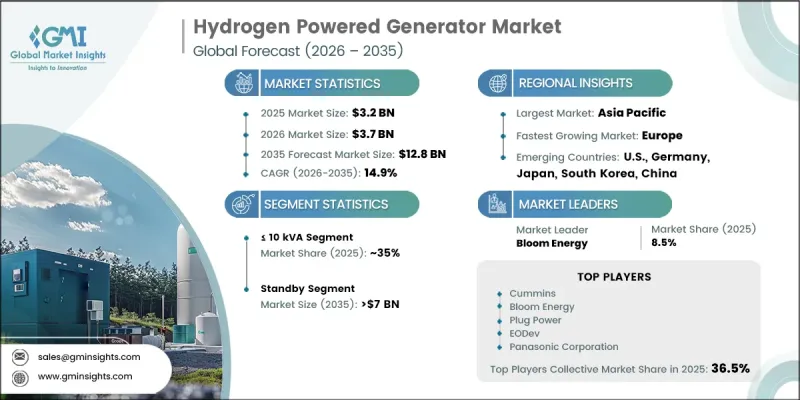

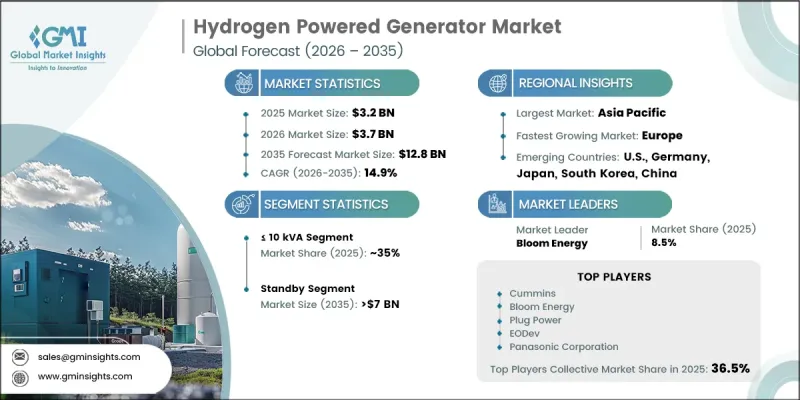

세계의 수소 발전기 시장은 2025년에 32억 달러로 평가되며, 2035년까지 CAGR 14.9%로 성장하며, 128억 달러에 달할 것으로 추정되고 있습니다.

전 세계에서 청정 에너지 도입과 환경의 지속가능성에 대한 관심이 높아지고 있는 것이 시장 확대를 크게 지원하고 있습니다. 이산화탄소 배출량에 대한 우려가 커지고 대체 에너지 기술로의 전환이 맞물리면서, 수소를 기반으로 한 전력 시스템에 대한 적극적인 투자가 촉진되고 있습니다. 정부와 민간 단체는 기존 연료에 대한 의존도를 낮추기 위한 노력을 적극적으로 추진하고 있으며, 이는 산업의 장기적인 성장에 유리한 환경을 조성하고 있습니다. 수소 발전기는 수소 연료를 사용하여 주택, 상업, 산업 및 비연속 전원 용도에 필요한 전력을 생산하는 첨단 에너지 시스템입니다. 이러한 발전기는 연소 과정을 통해 수소에 저장된 화학 에너지를 전기로 변환하며, 기존 연료 발전기를 대체할 수 있는 보다 친환경적인 대안을 제시합니다. 친환경 전력 솔루션에 대한 수요가 증가하는 데다, 배기가스 저감 및 가동시 소음 감소와 같은 장점이 더해지면서 제품의 보급이 더욱 가속화되고 있습니다. 또한 에너지 신뢰성, 무정전 전원, 지속가능한 운영 관행에 대한 인식이 높아짐에 따라 기업과 기관들은 수소 발전 기술에 대한 투자를 적극적으로 추진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 32억 달러 |

| 예측액 | 128억 달러 |

| CAGR | 14.9% |

정격 출력 10kVA 이하 부문은 2025년에 35%의 시장 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 14.5%로 성장할 것으로 전망됩니다. 컴팩트하고 효율적이며 친환경적인 백업 전원 시스템에 대한 수요가 꾸준히 증가하고 있으며, 이는 해당 부문의 성장에 기여하고 있습니다. 이러한 발전기는 조용한 운전, 낮은 탄소 배출, 신뢰성 높은 전력 공급 덕분에 널리 받아들여지고 있습니다. 소규모 용도나 분산형 전력 수요에 대한 적합성이 시장 수요를 더욱 부추기고 있습니다. 또한 지속가능한 에너지 인프라 및 청정 에너지 기술에 대한 투자 확대 역시 이 부문에서 수소 발전 시스템의 도입을 가속화하고 있습니다.

스탠바이 부문은 2025년에 55.8%의 시장 점유율을 차지하며, 2035년까지 70억 달러에 달할 것으로 전망됩니다. 신뢰성이 높은 비연속 및 백업 전원 솔루션에 대한 수요가 증가함에 따라 다양한 산업 분야에서 대기용 수소 발전기에 대한 수요가 크게 늘어나고 있습니다. 이러한 시스템은 정전시 저배출이며 신뢰성이 매우 높은 전력을 공급하는 동시에, 보다 광범위한 지속가능성 목표를 지원한다는 점에서도 널리 인정받고 있습니다. 탄력적인 에너지 시스템과 더욱 친환경적인 발전 기술에 대한 관심이 높아지고 있는 것이 대기 모드 용도 시장의 성장을 더욱 지원하고 있습니다.

북미 수소 발전기 시장은 2025년에 84%의 점유율을 차지하며 4억 9,600만 달러의 시장 규모를 기록했습니다. 청정 에너지 기술에 대한 투자 확대와 저배출형 백업 전원 시스템의 도입 증가가 맞물리면서, 전미에서 유망한 비즈니스 기회가 지속적으로 창출되고 있습니다. 지속가능한 에너지 구상에 대한 정부의 지원과 수소 발전 기술의 도입 확대가 산업 성장에 기여하고 있습니다. 중요 인프라 및 상업 시설에서의 수소 발전기 활용 확대 역시 미국내 시장 개발의 급속한 진전을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 개요

제3장 산업 인사이트

제4장 경쟁 구도

제5장 시장 규모·예측 : 정격 출력별, 2022-2035년

제6장 시장 규모·예측 : 용도별, 2022-2035년

제7장 시장 규모·예측 : 설치 형태별, 2022-2035년

제8장 시장 규모·예측 : 최종 용도별, 2022-2035년

제9장 시장 규모·예측 : 지역별, 2022-2035년

제10장 기업 개요

KSA 26.06.24The Global Hydrogen Powered Generator Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 14.9% to reach USD 12.8 billion by 2035.

The growing worldwide emphasis on clean energy adoption and environmental sustainability is significantly supporting market expansion. Rising concerns regarding carbon emissions, along with the transition toward alternative energy technologies, are encouraging strong investments in hydrogen-based power systems. Governments and private organizations are actively promoting initiatives aimed at reducing dependence on conventional fuels, creating favorable conditions for long-term industry growth. Hydrogen-powered generators are advanced energy systems that use hydrogen fuel to generate electricity for residential, commercial, industrial, and backup power applications. These generators convert the chemical energy stored in hydrogen into electrical power through combustion-based processes, offering a cleaner alternative to traditional fuel-powered generators. Increasing preference for environmentally friendly power solutions, combined with lower emissions and reduced operational noise, continues to strengthen product adoption. In addition, growing awareness regarding energy reliability, uninterrupted power supply, and sustainable operational practices is encouraging businesses and institutions to invest in hydrogen powered generation technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $12.8 Billion |

| CAGR | 14.9% |

The <= 10 kVA rated segment accounted for 35% share in 2025 and is anticipated to grow at 14.5% through 2035. Demand for compact, efficient, and environmentally sustainable backup power systems is steadily increasing, contributing to the segment's expansion. These generators are gaining wider acceptance due to their quiet operation, low carbon emissions, and reliable energy output. Their suitability for small-scale applications and decentralized power requirements is further supports market demand. Rising investments in sustainable energy infrastructure and clean power technologies are also accelerating the deployment of hydrogen-powered systems within this segment.

The standby segment held a 55.8% share in 2025 and is projected to reach USD 7 billion by 2035. The increasing need for dependable emergency and backup power solutions is driving strong demand for standby hydrogen-powered generators across multiple industries. These systems are widely recognized for delivering low-emission and highly reliable power during outages while supporting broader sustainability objectives. Growing emphasis on resilient energy systems and cleaner electricity generation technologies is further strengthening market growth for standby applications.

North America Hydrogen Powered Generator Market held an 84% share in 2025 and generated USD 496 million. Rising investments in clean energy technologies, combined with increasing adoption of low-emission backup power systems, continue to create favorable business opportunities across the country. Government support for sustainable energy initiatives and the growing deployment of hydrogen-based power generation technologies are contributing to industry expansion. Increasing use of hydrogen powered generators across critical infrastructure and commercial operations is also supporting the rapid pace of market development in the U.S.

Key participants operating in the Global Hydrogen Powered Generator Industry include 2G Energy, AFC Energy, Bloom Energy, Caterpillar, Cummins, EODev, GenCell, GeoPura, H2 Power System, H2SYS, H2X Global, HYGEN Technologies, Inocel, Mitsubishi Heavy Industries, Nuvera Fuel Cells, Panasonic Corporation, Plug Power, PowerCell Sweden, SFC Energy, and TOSHIBA CORPORATION. Companies operating in the hydrogen powered generator market are adopting multiple strategic initiatives to strengthen their competitive position and expand their market presence. Industry participants are heavily investing in research and development activities to improve fuel efficiency, system durability, and operational performance of hydrogen-powered technologies. Strategic collaborations with energy providers, technology developers, and infrastructure companies are also becoming increasingly common to accelerate product commercialization and deployment. Many manufacturers are expanding their production capacities and focusing on advanced hydrogen storage and fuel cell technologies to enhance system reliability. In addition, companies are strengthening their regional distribution networks and increasing investments in sustainable energy projects to improve customer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 Application trends

- 2.1.4 Installation trends

- 2.1.5 End use trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of hydrogen powered generators

- 3.8 Emerging opportunities & trends

- 3.9 Clean energy incentives & subsidies

- 3.10 Environmental compliance & emissions standards

- 3.11 Investment analysis & future prospects

- 3.12 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.12.1 By region (Driven by Primary Research)

- 3.12.2 By power rating (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 10 kVA

- 5.3 > 10 kVA - 100 kVA

- 5.4 > 100 kVA - 200 kVA

- 5.5 > 200 kVA

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Standby

- 6.3 Peak shaving

- 6.4 Prime power

Chapter 7 Market Size and Forecast, By Installation, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Portable

- 7.3 Stationary

Chapter 8 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Austria

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 South Korea

- 9.4.3 China

- 9.4.4 India

- 9.4.5 Philippines

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Iran

- 9.5.4 Iraq

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Peru

- 9.6.3 Mexico

Chapter 10 Company Profiles

- 10.1 2G Energy

- 10.2 AFC Energy

- 10.3 Bloom Energy

- 10.4 Caterpillar

- 10.5 Cummins

- 10.6 EODev

- 10.7 GenCell

- 10.8 GeoPura

- 10.9 H2 Power System

- 10.10 H2SYS

- 10.11 H2X Global

- 10.12 HYGEN Technologies

- 10.13 Inocel

- 10.14 Mitsubishi Heavy Industries

- 10.15 Nuvera Fuel Cells

- 10.16 Panasonic Corporation

- 10.17 Plug Power

- 10.18 PowerCell Sweden

- 10.19 SFC Energy

- 10.20 TOSHIBA CORPORATION