|

시장보고서

상품코드

2061487

자동차 열관리 시스템용 펌프 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2026-2035년)Automotive Pump for Thermal System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

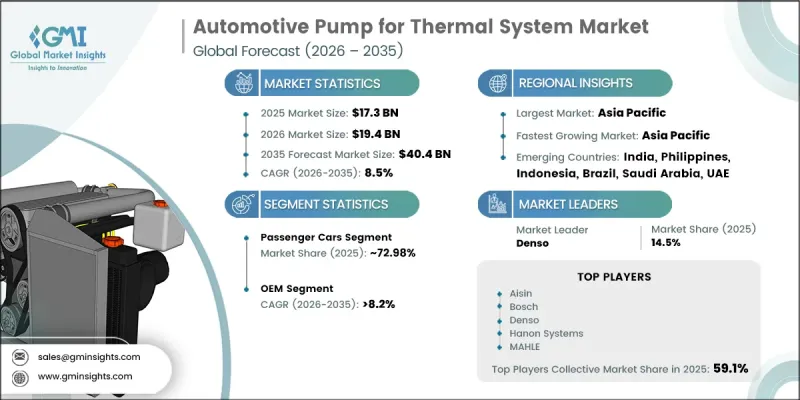

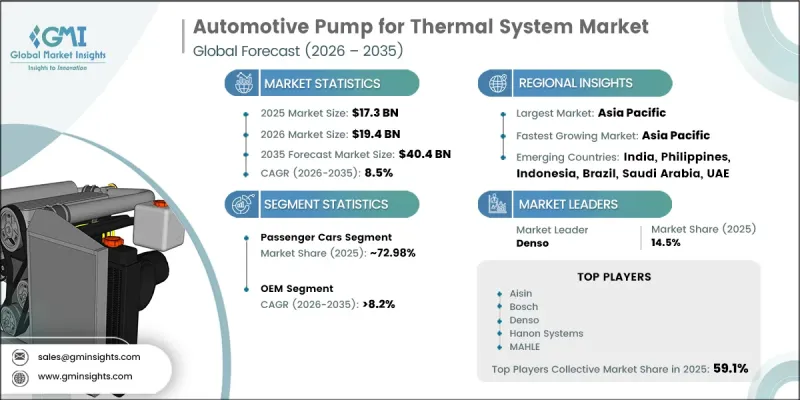

세계의 자동차 열관리 시스템용 펌프 시장은 2025년에 173억 달러로 평가되고 CAGR 8.5%로 성장하며, 2035년까지 404억 달러에 달할 것으로 예측됩니다.

자동차 업계가 기존의 내연기관 플랫폼에서 전동화 및 소프트웨어 주도형 차량 생태계로 급속히 전환되는 가운데, 자동차용 열관리 시스템용 펌프 업계는 큰 변화를 겪고 있습니다. 예전에는 주로 라디에이터의 순환 및 차량 내부 온도 조절에 사용되던 열 관리 펌프는 현재는 배터리 온도 유지, 인버터 성능 향상, 전력 전자 장치 보호, 그리고 주행 거리에 부정적인 영향을 주지 않으면서 차량 내부의 쾌적성을 확보하는 데 있으며, 필수적인 부품이 되었습니다. BEV, HEV, PHEV, FCEV 등의 전동 모빌리티 플랫폼에서 첨단 열펌프 시스템은 배터리 수명 연장, 급속 충전 효율 향상, 한랭 지역에서의 성능 향상, 그리고 차량 전체의 에너지 효율 최적화에 있으며, 매우 중요한 역할을 하고 있습니다. 세계 자동차 시장의 전동화 추세가 가속화됨에 따라 정밀한 열 관리 기능을 지원할 수 있는 지능형 냉각수 및 냉매 펌프 기술에 대한 수요도 증가하고 있습니다. 최신 전동 펌프는 효율을 높이는 동시에 불필요한 에너지 손실을 줄이기 위해 가변 속도 운전, 지능형 유량 제어, 그리고 차량 에너지 관리 시스템과의 원활한 통합 기능을 갖춘 설계가 점점 더 보편화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 173억 달러 |

| 예측액 | 404억 달러 |

| CAGR | 8.5% |

전 세계에서 전동 모빌리티로의 전환이 진행됨에 따라 첨단 자동차용 열펌프 기술에 대한 수요는 계속해서 증가하고 있습니다. 내연 기관차에 사용되는 기존의 벨트 구동식 기계 펌프와 달리, 전동식 냉각수 펌프는 수요에 맞춰 운전할 수 있도록 설계되어 있으며, 제조사는 열 제어 정밀도를 높이는 동시에 부수적인 에너지 소비를 줄일 수 있습니다. 자동차 제조사들은 전기자동차의 주행 거리를 늘리고, 전 세계에서 강화되고 있는 에너지 효율 기준을 충족하기 위해 첨단 열 관리 아키텍처에 점점 더 주력하고 있습니다. 멀티 루프 냉각 시스템과 지능형 열 제어 기술의 통합은 차세대 차량 플랫폼에서 중요한 차별화 요소로 부상하고 있으며, 시장 확대를 더욱 촉진하고 있습니다.

승용차 부문은 2025년에 72.98%의 점유율을 차지하며, 2035년까지 연평균 성장률(CAGR) 8.1%를 기록할 것으로 전망됩니다. 승용차 생산의 꾸준한 증가, 전기자동차의 보급 확대, 그리고 첨단 열 관리 시스템의 채택 증가가 이 부문의 성장에 크게 기여하고 있습니다. 승용차는 특히 주요 자동차 생산 거점에서, 전 세계 전기자동차 보급에서 가장 큰 점유율을 차지하고 있습니다. 전기자동차 및 하이브리드 승용차에는 고효율 배터리 냉각 시스템, 실내 공조 관리, 그리고 파워 일렉트로닉스의 열 관리가 요구되므로 첨단 전동 냉각수 펌프와 통합형 열 관리 시스템에 대한 수요는 계속해서 크게 증가하고 있습니다.

OEM 부문은 2025년에 84%의 시장 점유율을 차지하고 있으며, 2026-2035년 연평균 성장률(CAGR) 8.2%로 성장할 것으로 예상됩니다. 특히 전기자동차 및 하이브리드차 플랫폼 분야에서 첨단 열 관리 기술이 차량 생산 공정에 직접 통합되는 사례가 늘어나고 있으며, OEM 제조사들이 계속해서 시장을 독점하고 있습니다. 자동차 제조사들은 조립 공정에서 전동 냉각 펌프, HVAC 시스템, 배터리 냉각 모듈의 정밀한 동기화가 필요한 첨단 멀티루프 냉각 아키텍처를 개발하고 있습니다. 효율 향상, 안전성 강화, 차량 성능 최적화를 도모하기 위해 새로 출시되는 차량 플랫폼에는 맞춤형 열 관리 시스템이 탑재되어 있으며, 이는 OEM 부문의 성장을 더욱 촉진하고 있습니다.

아시아태평양의 자동차용 열 관리 시스템용 펌프 시장은 64.21%의 점유율을 차지했으며, 2025년에는 40억 달러 규모의 시장에 도달했습니다. 전기자동차 제조 및 배터리 생산 분야에서 중국이 차지하고 있는 확고한 입지가 계속해서 시장의 큰 성장을 이끌고 있습니다. 세계 최대 전기자동차 생산 거점으로서, 해당 국가에서는 배터리식 승용차, 전기 상용차, 전기버스의 도입이 확대되고 있습니다. 국내 자동차 제조사들은 충전 효율, 주행 거리 및 배터리의 장기 성능을 향상시키기 위해 첨단 액체 냉각 기술과 히트펌프 기반의 열 관리 아키텍처를 점점 더 많이 도입하고 있습니다. 고효율 열 관리 시스템으로의 이러한 지속적인 전환에 따라 중국 자동차 업계 전반에서 전기식 냉각수 및 냉매 펌프 솔루션에 대한 수요가 크게 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 개요

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산·예측 : 차량별, 2022-2035년

제6장 시장 추산·예측 : 추진력별, 2022-2035년

제7장 시장 추산·예측 : 판매 채널별, 2022-2035년

제8장 시장 추산·예측 : 용도별, 2022-2035년

제9장 시장 추산·예측 : 펌프 유형별, 2022-2035년

제10장 시장 추산·예측 : 출력 정격별, 2022-2035년

제11장 시장 추산·예측 : 지역별, 2022-2035년

제12장 기업 개요

KSA 26.06.24The Global Automotive Pump for Thermal System Market was valued at USD 17.3 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 40.4 billion by 2035.

The automotive pump for thermal system industry is witnessing a major transformation as the automotive sector rapidly shifts from conventional combustion-engine platforms toward electrified and software-driven vehicle ecosystems. Thermal pumps, which were previously used mainly for radiator circulation and cabin temperature regulation, have now become essential components responsible for maintaining battery temperature, improving inverter performance, protecting power electronics, and ensuring cabin comfort without negatively affecting vehicle range. In electric mobility platforms such as BEVs, HEVs, PHEVs, and FCEVs, advanced thermal pump systems play a vital role in extending battery life, improving fast-charging efficiency, enhancing cold-weather performance, and optimizing overall vehicle energy efficiency. Growing electrification across global automotive markets is also increasing demand for intelligent coolant and refrigerant pump technologies capable of supporting precise thermal management functions. Modern electric pumps are increasingly designed with variable-speed operation, intelligent flow control, and seamless integration with vehicle energy management systems to improve efficiency while reducing unnecessary energy loss.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.3 Billion |

| Forecast Value | $40.4 Billion |

| CAGR | 8.5% |

The growing transition toward electric mobility worldwide continues to strengthen demand for advanced automotive thermal pump technologies. Unlike traditional belt-driven mechanical pumps used in internal combustion vehicles, electrically powered coolant pumps are engineered for demand-based operation, allowing manufacturers to improve thermal accuracy while lowering parasitic energy consumption. Automakers are increasingly focusing on advanced thermal management architectures to extend electric vehicle driving range and comply with stricter global energy efficiency standards. The integration of multi-loop cooling systems and intelligent thermal regulation technologies is becoming a key differentiator in next-generation vehicle platforms, further supporting market expansion.

The passenger cars segment accounted for 72.98% share in 2025 and is projected to witness a CAGR of 8.1% through 2035. Strong growth in passenger vehicle production, rising penetration of electric passenger cars, and increasing adoption of sophisticated thermal management systems are contributing significantly to segment expansion. Passenger vehicles represent the largest share of electric vehicle deployment globally, particularly across major automotive manufacturing hubs. As electric and hybrid passenger vehicles require highly efficient battery cooling systems, cabin climate management, and thermal control of power electronics, the need for advanced electric coolant pumps and integrated thermal systems continues to increase substantially.

The OEM segment held a 84% share in 2025 and is expected to grow at a CAGR of 8.2% from 2026 to 2035. Original equipment manufacturers continue to dominate the market as advanced thermal management technologies are increasingly integrated directly into vehicle production processes, especially for electric and hybrid platforms. Automotive manufacturers are developing sophisticated multi-loop cooling architectures that require precise synchronization of electric coolant pumps, HVAC systems, and battery cooling modules during assembly. Customized thermal systems are being integrated into newly launched vehicle platforms to improve efficiency, enhance safety, and optimize vehicle performance, further supporting OEM segment growth.

Asia Pacific Automotive Pump for Thermal System Market held 64.21% share, generating USD 4 billion in 2025. China's strong position in electric vehicle manufacturing and battery production continues to drive substantial market growth. As the world's largest electric vehicle manufacturing hub, the country is witnessing rising deployment of battery electric passenger vehicles, electric commercial fleets, and electric buses. Domestic vehicle manufacturers are increasingly incorporating advanced liquid cooling technologies and heat pump-based thermal architectures to improve charging efficiency, vehicle range, and long-term battery performance. This ongoing transition toward high-efficiency thermal management systems is significantly increasing demand for electric coolant and refrigerant pump solutions across the Chinese automotive industry.

Leading companies operating in the Global Automotive Pump for Thermal System Market include Aisin, Denso, Magna International, Hanon Systems, Bosch, MAHLE, Valeo, Hitachi, Gates, and Eberspacher Group. Companies operating in the Automotive Pump for Thermal System Market are focusing heavily on technological innovation, strategic collaborations, and expansion of electrification-focused product portfolios to strengthen their market position. Major manufacturers are investing in advanced electric coolant pumps, intelligent thermal management systems, and energy-efficient refrigerant technologies to support growing electric vehicle adoption. Businesses are also prioritizing partnerships with automotive OEMs to secure long-term supply agreements and improve integration capabilities within next-generation vehicle platforms. In addition, companies are expanding manufacturing capacity across key automotive hubs to meet rising global demand. Research and development investments are accelerating to improve thermal efficiency, reduce power consumption, and enhance system reliability. Several market participants are also leveraging digital engineering, software-based thermal controls, and smart energy management technologies to differentiate their offerings and strengthen competitiveness in the rapidly evolving automotive ecosystem.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power Rating

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Propulsion

- 2.2.6 Sales Channel

- 2.2.7 Pump Type

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in electric vehicle production volumes

- 3.2.1.2 Growth in electrified commercial and fleet vehicle deployments

- 3.2.1.3 Increase in fast-charging infrastructure installations

- 3.2.1.4 Expansion of 800V high-voltage vehicle platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced pump technologies

- 3.2.2.2 Complexity in retrofitting advanced thermal pumps

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of battery immersion cooling technologies

- 3.2.3.2 Growth in EV aftermarket thermal component replacement

- 3.2.3.3 Development of ultra-fast charging compatible cooling systems

- 3.2.3.4 Electrification of public transportation networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory guideline

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA Vehicle Emission & Fuel Efficiency Standards

- 3.4.1.2 Canada: Transport Canada Safety & Thermal Performance Standards

- 3.4.2 Europe

- 3.4.2.1 Germany: End-of-Life Vehicle (ELV) Directive

- 3.4.2.2 UK: Zero Emission Vehicle (ZEV) Mandate

- 3.4.2.3 France: Energy Transition Law

- 3.4.2.4 Italy: National Energy & Climate Plan (PNIEC) Alignment

- 3.4.3 Asia Pacific

- 3.4.3.1 China: NEV Mandate & Dual Credit Policy

- 3.4.3.2 India: FAME II & PLI Scheme for Auto Components

- 3.4.3.3 Japan: Green Growth Strategy & JEVS Standards

- 3.4.3.4 Australia: National Electric Vehicle Strategy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: Rota 2030 Program

- 3.4.4.2 Mexico: USMCA Localization Requirements

- 3.4.4.3 Argentina: National Sustainable Mobility Policies

- 3.4.5 MEA

- 3.4.5.1 UAE: Net Zero 2050 Strategy & EV Infrastructure Expansion

- 3.4.5.2 Saudi Arabia: Vision 2030 & EV Localization Strategy

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Trade statistics (Driven by Paid Database)

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Future outlook & opportunities

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.14.3 Risks, Limitations & Regulatory Considerations

- 3.15 Capacity & Production Landscape (Driven by Primary Research)

- 3.15.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.15.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

- 3.15.3 Regional Manufacturing Footprint

- 3.15.4 Production Technology & Automation Levels

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light-duty

- 5.3.2 Medium-duty

- 5.3.3 Heavy-duty

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 BEV (battery electric vehicle)

- 6.4 PHEV (plug-in hybrid electric vehicle)

- 6.5 HEV (hybrid electric vehicle)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Engine cooling

- 8.3 Battery thermal management

- 8.4 Power electronics & motor cooling

- 8.5 Turbocharger cooling

- 8.6 Cabin HVAC

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Pump Type, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Centrifugal pumps

- 9.3 Positive displacement pumps

- 9.4 Variable displacement pumps

Chapter 10 Market Estimates & Forecast, By Power Rating, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Below 50w

- 10.3 50w - 100w

- 10.4 100w - 500w

- 10.5 Above 500w

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Belgium

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aisin

- 12.1.2 Bosch

- 12.1.3 Continental

- 12.1.4 Denso

- 12.1.5 Hanon Systems

- 12.1.6 Mahle

- 12.1.7 Schaeffler

- 12.1.8 Valeo

- 12.2 Regional Players

- 12.2.1 Eberspaecher

- 12.2.2 Gates

- 12.2.3 Hitachi Astemo

- 12.2.4 Magna International

- 12.2.5 Nidec / GPM

- 12.2.6 Rheinmetall / Pierburg

- 12.2.7 Sanhua Automotive