|

시장보고서

상품코드

2071197

LFP 및 LMFP 캐소드 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)LFP and LMFP Cathode Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

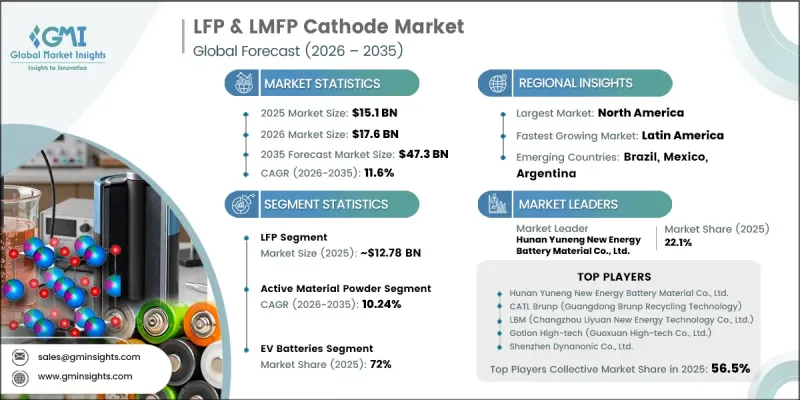

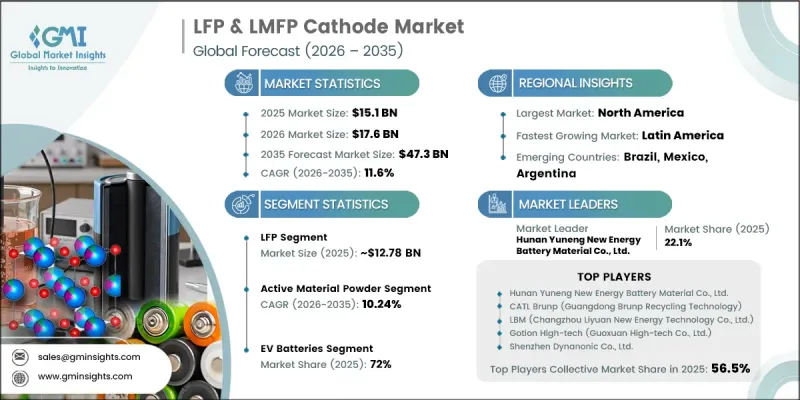

세계의 LFP 및 LMFP 캐소드 시장은 2025년에 151억 달러 규모가 되어, CAGR 11.6%로 성장하여 2035년까지 473억 달러에 이를 것으로 추정되고 있습니다.

LFP 및 LMFP 캐소드 업계의 성장은 비용 최적화에 대한 압박, 공급망 취약성에 대한 우려, 그리고 배터리 안전성에 대한 더욱 엄격해진 기대의 영향을 받아, 코발트 의존형 화학 조성에서 벗어나는 구조적 전환에 힘입어 이루어지고 있습니다. 리튬 철 인산염(LFP) 및 망간이 강화된 리튬 망간 철 인산염(LMFP)의 화학 조성은 대형 에너지 저장 및 전동 모빌리티 분야에서 점점 더 선호되는 솔루션으로 자리매김하고 있습니다. 이러한 채용 경향은 장기적인 조달 전략에 힘입어 더욱 가속화되고 있으며, OEM 및 배터리 제조업체들은 인산철계 캐소드를 중심으로 수년에 걸친 공급 계약을 체결하는 사례가 늘고 있습니다. 이는 안정적인 원자재 비용을 확보하고, 코발트 조달에 수반되는 지정학적 위험에 대한 노출을 줄이려는 보다 광범위한 노력을 반영한 것입니다. 수요 증가는 LFP 생산 생태계의 확장성에 의해서도 형성되고 있습니다. 특히 아시아에서는 확립된 제조 클러스터와 성숙한 가공 노하우가 대량 생산을 뒷받침하고 있습니다. 운송 및 에너지 인프라 분야 전반에서 전동화 추세가 계속해서 가속화되는 가운데, LFP 및 LMFP 계열 배터리는 앞으로도 세계 배터리 공급망의 핵심적인 위치를 유지할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 151억 달러 |

| 예측 금액 | 473억 달러 |

| CAGR | 11.6% |

2025년에는 LFP 기술이 시장 점유율의 82.2%를 차지하며 약 127억 8,000만 달러에 달했습니다. 이는 조기 상용화, 확립된 제조 공정, 그리고 대규모 배터리 제조 생태계 전반에 걸친 광범위한 통합 덕분입니다. 이러한 화학 조성은 성숙한 산업 기반과 확립된 배터리 공급망 전반에 걸친 광범위한 채택이라는 장점을 활용하여 안정적인 대량 생산을 가능하게 하고 있습니다. 높은 작동 신뢰성과 긴 수명은 전 세계 캐소드 시장의 다양한 최종 용도 분야에서 이 제품의 우위를 더욱 공고히 하고 있습니다.

2025년에는 전기차용 배터리 부문이 72%의 점유율을 차지했습니다. LFP 및 LMFP 캐소드는 안전성, 비용 효율성, 긴 수명이 중요한 고려 사항인 전동 모빌리티 분야에서 널리 사용되고 있습니다. 특히 대중용 전기차, 상용 운송 차량 및 보급형 모빌리티 솔루션 분야에서 그 도입이 두드러지며, 이러한 분야에서는 에너지 밀도의 단점이 합리적인 가격과 내구성의 장점으로 상쇄되고 있습니다.

북미의 LFP 및 LMFP 캐소드 시장은 2026년부터 2035년까지 연평균 성장률(CAGR) 11.37%를 나타낼 것으로 예측됩니다. 미국의 성장은 국내 배터리 생산 능력을 확대하고 공급망의 현지화를 강화하기 위한 정책 주도형 제조 인센티브의 영향을 받고 있습니다. 이러한 규제 체계는 캐소드 생산에 대한 투자를 촉진하고, 지역 전체에 걸쳐 현지화된 배터리 밸류체인의 확장을 지원하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035년

제6장 시장 추산 및 예측 : 형태별, 2022-2035년

제7장 시장 추산 및 예측 : 용도별, 2022-2035년

제8장 시장 추산 및 예측 : 지역별, 2022-2035년

제9장 기업 개요

JHS 26.07.01The Global LFP & LMFP Cathode Market was valued at USD 15.1 billion in 2025 and is estimated to grow at a CAGR of 11.6% to reach USD 47.3 billion by 2035.

Growth across the LFP & LMFP cathode industry is driven by a structural shift away from cobalt-dependent chemistries, influenced by cost optimization pressures, supply chain vulnerability concerns, and stricter battery safety expectations. Lithium iron phosphate (LFP) and manganese-enhanced lithium manganese iron phosphate (LMFP) chemistries are increasingly positioned as preferred solutions for large-format energy storage and electric mobility applications. Adoption is further reinforced by long-term procurement strategies, with OEMs and battery manufacturers increasingly locking in multi-year supply agreements centered on iron-phosphate-based cathode materials. This reflects a broader effort to secure stable input costs and reduce exposure to geopolitical risks associated with cobalt sourcing. Demand growth is also being shaped by the scalability of LFP production ecosystems, particularly in Asia, where established manufacturing clusters and mature processing expertise support high-volume output. As electrification trends continue to accelerate across transportation and energy infrastructure sectors, LFP and LMFP chemistries are expected to remain central to global battery supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.1 Billion |

| Forecast Value | $47.3 Billion |

| CAGR | 11.6% |

LFP technology accounted for 82.2% share in 2025, representing about USD 12.78 billion, attributed to its early commercialization, well-established production processes, and extensive integration across large-scale battery manufacturing ecosystems. Chemistry benefits from mature industrial capabilities and widespread adoption across established battery supply networks, enabling consistent large-volume production. Strong operational reliability and long cycle life further reinforce its dominance across multiple end-use applications within the global cathode market.

The EV batteries segment held a 72% share in 2025. LFP and LMFP cathodes are widely utilized in electric mobility applications where safety performance, cost efficiency, and long operational life are critical considerations. Their deployment is particularly strong in mass-market electric vehicles, commercial transportation fleets, and entry-level mobility solutions, where energy density trade-offs are balanced by affordability and durability advantages.

North America LFP & LMFP Cathode Market is expected to grow at a CAGR of 11.37% from 2026 to 2035. Growth in the United States is influenced by policy-driven manufacturing incentives designed to accelerate domestic battery production capacity and strengthen supply chain localization. These regulatory frameworks encourage investments in cathode material production and support the expansion of localized battery value chains across the region.

Major companies operating in the Global LFP & LMFP cathode market include CATL Brunp (Guangdong Brunp Recycling Technology), Hunan Yuneng New Energy Battery Material Co., Ltd., Gotion High-tech (Guoxuan High-tech Co., Ltd.), LBM (Changzhou Liyuan New Energy Technology Co., Ltd.), Shenzhen Dynanonic Co., Ltd., Chongqing Terui Battery Materials Co., Ltd., Epsilon Advanced Materials Pvt. Ltd., IBU-tec Advanced Materials AG, IBUvolt Battery Materials GmbH, Mitra Chem, Sparkz Inc., HCM, Integrals Power Ltd., and Western CAM. Companies operating in the LFP & LMFP cathode market are focusing on strengthening their competitive position through capacity expansion, vertical integration, and long-term supply agreements with battery manufacturers and automotive OEMs. Significant investments are being directed toward scaling production facilities to meet rising demand from electric vehicle and energy storage applications. Firms are also prioritizing technological advancements aimed at improving energy density, cycle life, and material efficiency to enhance product performance. Strategic partnerships and joint ventures are increasingly being used to secure raw material supply chains and reduce exposure to price volatility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising electric vehicle adoption worldwide

- 3.2.1.2 Increasing demand for energy storage solutions

- 3.2.1.3 Cost advantages over nickel-based chemistries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lower energy density than alternative chemistries

- 3.2.2.2 Raw material price fluctuations and volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of LMFP for higher energy density

- 3.2.3.2 Growth in stationary energy storage installations

- 3.2.3.3 Localization of battery material supply chains

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 LFP

- 5.3 LMFP

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Active material powder

- 6.3 Coated electrode

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 EV batteries

- 7.3 ESS

- 7.4 Consumer electronics

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Hunan Yuneng New Energy Battery Material Co., Ltd.

- 9.2 CATL Brunp (Guangdong Brunp Recycling Technology)

- 9.3 LBM (Changzhou Liyuan New Energy Technology Co. Ltd.)

- 9.4 Gotion High-tech (Guoxuan High-tech Co., Ltd.)

- 9.5 Shenzhen Dynanonic Co., Ltd.

- 9.6 Chongqing Terui Battery Materials Co., Ltd.

- 9.7 Epsilon Advanced Materials Pvt. Ltd.

- 9.8 IBUvolt Battery Materials GmbH

- 9.9 IBU-tec Advanced Materials AG

- 9.10 HCM

- 9.11 Mitra Chem

- 9.12 Sparkz Inc.

- 9.13 Integrals Power Ltd.

- 9.14 Western CAM