|

시장보고서

상품코드

2071397

코발트 프리 캐소드 재료 시장 : 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Cobalt-Free Cathode Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

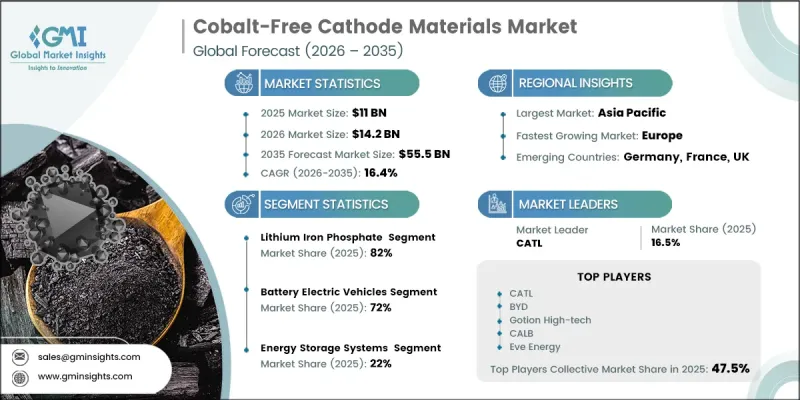

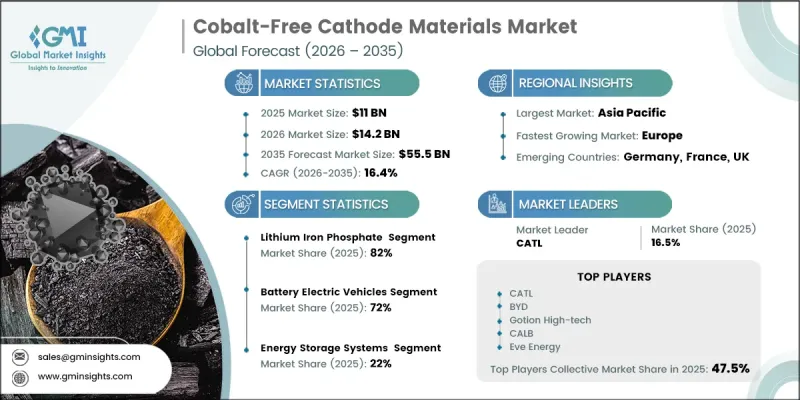

세계의 코발트 프리 캐소드 재료 시장은 2025년에 110억 달러 규모로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 16.4%로 성장하여 555억 달러에 이를 것으로 추정되고 있습니다.

이러한 성장 추세는 코발트를 많이 사용하는 화학 조성에서 비롯된 공급망 리스크를 제거하고, 소재 비용을 절감하는 대체재로 결정적으로 전환함에 따라 주도되고 있습니다. 책임 있는 조달에 대한 규제 당국의 감독 강화와 더불어, 배터리 밸류체인 전반에 걸친 대규모 투자가 맞물리면서 그 도입은 계속해서 가속화되고 있습니다. 동시에, 재료 공학의 발전으로 인해 코발트계와 코발트 프리 솔루션 간의 성능 격차가 줄어들면서, 후자는 더 폭넓은 용도로 실용화될 수 있게 되었습니다. 비용 측면에서의 우위는 여전히 중요한 요소이며, 코발트가 포함되지 않은 화학 조성은 높은 안전성과 내구성을 유지하면서도 kWh당 비용을 대폭 절감하고 있습니다. 업계 전반의 협력 강화, 제조 효율 향상, 그리고 유리한 정책 지원이 맞물려 장기적인 시장 확대를 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 110억 달러 |

| 예측 금액 | 555억 달러 |

| CAGR | 16.4% |

이 시장은 기존의 양극재 조성에서 코발트에 대한 의존도를 완전히 배제한 인산철 리튬이나 망간 함량을 높인 대체재로 구조적으로 전환됨에 따라 형성되었습니다. 이러한 전환은 규제 요건의 강화와 변동이 심한 원자재 공급망에 대한 의존도를 낮추기 위한 지속적인 노력에 힘입어 더욱 가속화되고 있습니다. 비용 경쟁력은 지속적으로 향상되고 있으며, 리튬철인산염은 기존 화학 조성에 비해 kWh당 비용을 약 30% 절감하고 있습니다. 망간을 풍부하게 함유한 제품은 제조 공정이 복잡하여 가격이 다소 비싸긴 하지만, 코발트 함유 소재와 비교했을 때 여전히 전반적인 비용 면에서 우위를 유지하고 있습니다.

2025년에는 리튬인산철 부문이 시장 점유율의 82%를 차지했으며, 이는 이 부문의 강력한 상용화 및 확장성 우위를 반영한 것입니다. 이러한 우위는 높은 열 안정성, 안전성 및 성능 향상, 그리고 널리 구할 수 있는 원자재를 기반으로 한 확립된 공급 생태계에 의해 뒷받침되고 있습니다. 이러한 특성 덕분에, 특히 안전성, 긴 수명, 비용 효율성이 중요한 고려 사항이 되는 용도에서 대규모 도입을 위한 최적의 선택지로 자리매김하고 있습니다.

2025년, 배터리식 전기차(BEV) 부문은 72%의 시장 점유율을 차지했습니다. 이 부문 수요는 지속적으로 진화하고 있으며, 표준 주행 거리의 배터리 시스템과 첨단 급속 충전 솔루션 간에 뚜렷한 차별화가 나타나고 있습니다. 재료 밀도와 충전 성능이 향상됨에 따라 더욱 폭넓은 활용 사례가 가능해졌으며, 시스템 전체의 효율도 향상되고 있습니다.

2025년, 북미의 코발트 프리 양극재 시장은 11%의 점유율을 기록했으나, 배터리 제조 및 에너지 저장 인프라에 대한 국내 투자가 증가함에 따라 그 전략적 중요성은 계속해서 높아지고 있습니다. 미국은 대규모 에너지 저장 시스템의 도입이 급속히 확대되고, 전기 이동 수단 솔루션의 채택이 진전되고 있는 것을 배경으로, 여전히 주요 수요 거점으로 자리 잡고 있습니다. 지속적인 정책 지원과 공급망 현지화 노력을 통해 해당 지역 시장에서의 입지가 더욱 공고해질 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 재료 화학 유형별(2022-2035년)

제6장 시장 추정 및 예측 : 용도별(2022-2035년)

제7장 시장 추정 및 예측 : 최종 사용자별(2022-2035년)

제8장 시장 추정 및 예측 : 지역별(2022-2035년)

제9장 기업 개요

KTHThe Global Cobalt-Free Cathode Materials Market was valued at USD 11 billion in 2025 and is estimated to grow at a CAGR of 16.4% to reach USD 55.5 billion by 2035.

The growth trajectory is driven by a decisive transition away from cobalt-intensive chemistries toward alternatives that eliminate supply chain risk and reduce material costs. Increasing regulatory scrutiny around responsible sourcing, combined with large-scale investments across the battery value chain, continues to accelerate adoption. At the same time, advancements in material engineering have narrowed the performance gap between cobalt-based and cobalt-free solutions, making the latter viable across a wider range of applications. Cost advantages remain a central factor, as cobalt-free chemistries deliver significantly lower cost per kWh while maintaining strong safety and durability characteristics. Growing industrial alignment, improved manufacturing efficiencies, and favorable policy support are collectively reinforcing long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11 Billion |

| Forecast Value | $55.5 Billion |

| CAGR | 16.4% |

The market is shaped by a structural migration away from traditional cathode compositions toward lithium iron phosphate and manganese-enhanced alternatives that completely remove cobalt dependency. This shift is further supported by tightening compliance requirements and ongoing efforts to reduce exposure to volatile raw material supply chains. Cost competitiveness continues to improve, with lithium iron phosphate offering nearly a 30% lower cost-per-kWh compared to conventional chemistries. Manganese-enriched variants, while slightly more expensive due to processing complexity, still maintain an overall cost advantage when compared to cobalt-containing materials.

The lithium iron phosphate segment accounted for 82% share in 2025, reflecting its strong commercialization and scalability advantages. Its dominance is supported by high thermal stability, improved safety performance, and a well-established supply ecosystem based on widely available raw materials. These characteristics have positioned it as the preferred choice for large-scale adoption, particularly in applications where safety, longevity, and cost efficiency are critical considerations.

The battery electric vehicles segment held 72% share in 2025. Demand within this segment continues to evolve, with clear differentiation emerging between standard-range battery systems and advanced fast-charging solutions. Improvements in material density and charging performance are enabling broader use cases and enhancing overall system efficiency.

North America Cobalt-Free Cathode Materials Market held a 11% share in 2025, yet its strategic importance continues to rise due to increasing domestic investments in battery manufacturing and energy storage infrastructure. The United States remains a key demand hub, supported by rapid growth in large-scale energy storage deployments and rising adoption of electric mobility solutions. Continued policy backing and supply chain localization efforts are expected to further strengthen regional market positioning.

Key participants in the Global Cobalt-Free Cathode Materials Market include BTR New Material Group, Dynanonic Ltd., Nano One Materials Corp., Integrals Power Pte. Ltd., IBU-tec Advanced Materials AG, Mitra Chem Inc., Redoxion Ltd., Sparkz Inc., CATL (Contemporary Amperex Technology Co., Ltd.), BYD Company Limited, and Epsilon Advanced Materials. Companies operating in the cobalt-free cathode materials market are focusing on capacity expansion, vertical integration, and advanced material innovation to strengthen their competitive position. Strategic collaborations across the battery value chain are enabling firms to secure raw material supply and enhance production efficiency. Investments in research and development are driving improvements in energy density, cycle life, and fast-charging capabilities, helping companies differentiate their offerings. Many players are also prioritizing regional manufacturing footprints to align with local policy incentives and reduce supply chain risks. In addition, partnerships with automotive and energy storage stakeholders are supporting long-term demand visibility while accelerating the commercialization of next-generation cathode technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material chemistry

- 2.2.3 Application

- 2.2.4 End user industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Chemistry Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Lithium iron phosphate (LFP)

- 5.3 Lithium manganese iron phosphate (LMFP)

- 5.4 Nickel-manganese-aluminum oxide (NMA)

- 5.5 High-nickel layered oxides (LNO-based)

- 5.6 Lithium-rich layered oxides (LMR)

- 5.7 Manganese-based spinels (LMO)

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Battery electric vehicles (BEV)

- 6.2.1 Passenger BEV

- 6.2.2 Commercial BEV (Trucks, Buses)

- 6.3 Plug-in hybrid electric vehicles (PHEV)

- 6.4 Stationary energy storage systems (ESS)

- 6.4.1 Grid-scale ESS

- 6.4.2 Commercial & industrial ESS

- 6.4.3 Residential ESS

- 6.5 Consumer electronics

- 6.5.1 Smartphones & tablets

- 6.5.2 Laptops & wearables

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive OEMs

- 7.3 Battery cell manufacturers

- 7.4 Energy storage system integrators

- 7.5 Consumer electronics manufacturers

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BTR New Material Group

- 9.2 BYD Company Limited

- 9.3 CATL (Contemporary Amperex Technology)

- 9.4 Dynanonic Ltd.

- 9.5 Epsilon Advanced Materials

- 9.6 IBU-tec Advanced Materials AG

- 9.7 IBUvolt Battery Materials GmbH

- 9.8 Integrals Power Pte. Ltd.

- 9.9 Mitra Chem Inc.

- 9.10 Nano One Materials Corp.

- 9.11 Redoxion Ltd.

- 9.12 Sparkz Inc.

- 9.13 Sumitomo Metal Mining Co., Ltd.

- 9.14 Targray Technology International

- 9.15 Umicore N.V.

- 9.16 Western CAM Inc.