|

시장보고서

상품코드

2071228

차세대 자동차 커넥티비티 솔루션 시장 : 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Next-Generation Automotive Connectivity Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

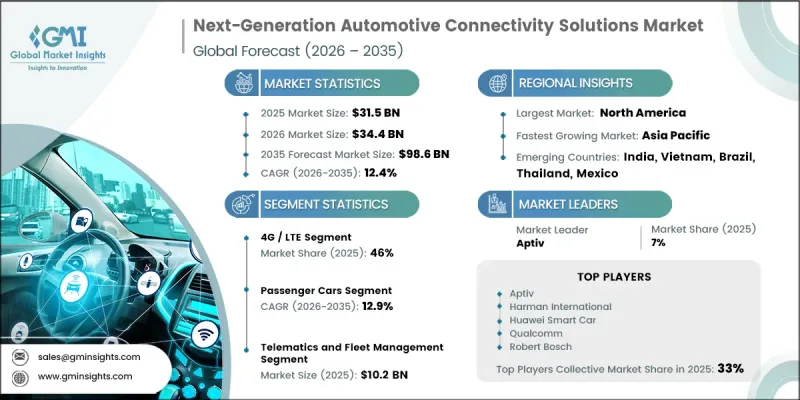

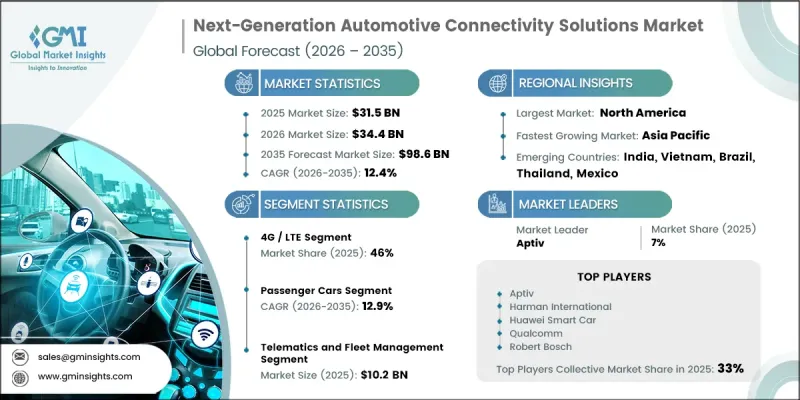

세계 차세대 자동차 커넥티비티 솔루션 시장은 2025년에 315억 달러로 평가되었고 CAGR 12.4%로 성장하여 2035년까지 986억 달러에 이를 것으로 추정되고 있습니다.

이 시장의 성장은 5G 연결, 셀룰러 V2X(C-V2X) 통신, 위성 지원형 네트워크, 엣지 컴퓨팅 기능, 소프트웨어 정의 차량 플랫폼 등 커넥티드카 기술의 급속한 발전에 힘입어 이루어지고 있습니다. 커넥티드 모빌리티 생태계가 지속적으로 성숙해감에 따라, 수익 창출 기회는 기존의 커넥티비티 하드웨어의 범위를 훨씬 뛰어넘어 확대되고 있습니다. 자동차 제조업체, 반도체 공급업체, 통신 사업자, 클라우드 기술 기업 및 차량 관리 기술 공급업체들은 차량 데이터 서비스, 무선 소프트웨어 업데이트, 커넥티드 인포테인먼트 서비스, 첨단 안전 기능, 디지털 차량 관리 운영을 통해 창출되는 장기적인 수익원을 확보하는 데 점점 더 주력하고 있습니다. 차량이 점점 더 소프트웨어 중심으로 변모함에 따라 시장은 지속적으로 진화하고 있으며, 이는 정기적인 서비스 기반의 비즈니스 모델에 새로운 기회를 창출하는 동시에 커넥티드 모빌리티 분야 전반의 혁신을 가속화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 연도 시장 규모 | 315억 달러 |

| 예측 금액 | 986억 달러 |

| CAGR | 12.4% |

현재 이 시장은 여전히 4G/LTE 기술의 광범위한 보급에 큰 영향을 받고 있습니다. 안정적인 네트워크 가용성, 비용 효율성이 뛰어난 모듈의 도입, 그리고 신뢰할 수 있는 성능이 커넥티드카 생태계 전반에 걸친 광범위한 도입을 지속적으로 뒷받침하고 있습니다. COVID-19 팬데믹 기간 동안 차세대 자동차 커넥티비티 솔루션 시장은 과제와 기회 모두에 직면했습니다. 당초 제조 부진, 공급망 혼란, 반도체 부족, 그리고 자동차 생산 대수 감소로 인해 시장 성장이 제약을 받았으며, 그 결과 첨단 커넥티드카 기술의 도입이 주춤했습니다. 이러한 역풍에도 불구하고, 커넥티드 모빌리티 솔루션에 대한 장기적인 수요는 견조한 모습을 유지했습니다. V2X(Vehicle-to-Everything) 통신은 협력형 지능형 교통 시스템(ITS) 개발에서 계속해서 중요한 역할을 수행하고 있으며, 차량과 주변 교통 인프라 간의 원활한 상호작용을 가능하게 하고 있습니다.

4G/LTE 부문은 2025년에 46%의 시장 점유율을 차지하고, 2026년부터 2035년까지 연평균 성장률(CAGR) 10.7%로 성장할 것으로 전망됩니다. LTE 기반 기술이 이미 입증된 신뢰성과 합리적인 가격을 갖추고 있다는 점이, 이 기술의 지속적인 채택을 뒷받침하고 있습니다. LTE-Advanced, LTE Cat-M1 및 NB-IoT 솔루션은 확립된 인프라와 유리한 비용 구조 덕분에 커넥티드카 용도 전반에 걸쳐 지속적으로 널리 도입되고 있습니다.

승용차 부문은 2025년에 67%의 시장 점유율을 차지했습니다. 디지털 기술로 강화된 운전 경험에 대한 강력한 수요가 이 부문 전체의 성장을 지속적으로 뒷받침하고 있습니다. 첨단 연결 기술, 내장형 5G 기능, 무선 소프트웨어 업데이트(OTA), ADAS(첨단 운전자 지원 시스템), 전기차(EV) 최적화 기능, 원격 차량 제어, 그리고 구독형 디지털 서비스의 통합이 진행됨에 따라 승용차 제조업체와 소비자들의 도입이 가속화되고 있습니다.

2025년, 미국의 차세대 자동차 커넥티비티 솔루션 시장은 89억 달러 규모에 달했습니다. 해당 국가 시장 성장은 연결형 교통 인프라 구축을 추진하기 위한 정부의 이니셔티브에 힘입어 이루어지고 있습니다. ‘초당파 인프라법’에 따른 자금 배분으로 V2X 기술 개발이 촉진되고 있는 한편, 5.9GHz 대역에 대한 규제가 명확해짐에 따라 C-V2X 통신 도입 전망이 밝아지고 있습니다. 차량 통신 프레임워크 및 자동차 사이버 보안 기준에 대한 지속적인 노력이 미국 내 커넥티드카 생태계의 확장을 계속해서 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 연결 아키텍처별, 2022-2035년

제6장 시장 추산 및 예측 : 커뮤니케이션 기술별, 2022-2035년

제7장 시장 추산 및 예측 : 차량별, 2022-2035년

제8장 시장 추산 및 예측 : 추진력별, 2022-2035년

제9장 시장 추산 및 예측 : 용도별, 2022-2035년

제10장 시장 추산 및 예측 : 최종 용도별, 2022-2035년

제11장 시장 추산 및 예측 : 지역별, 2022-2035년

제12장 기업 개요

JHS 26.07.01The Global Next-Generation Automotive Connectivity Solutions Market was valued at USD 31.5 billion in 2025 and is estimated to grow at a CAGR of 12.4% to reach USD 98.6 billion by 2035.

Industry expansion is driven by the rapid evolution of connected vehicle technologies, including 5G connectivity, cellular vehicle-to-everything (C-V2X) communications, satellite-supported networking, edge computing capabilities, and software-defined vehicle platforms. As connected mobility ecosystems continue to mature, revenue opportunities are extending far beyond traditional connectivity hardware. Automotive manufacturers, semiconductor suppliers, telecommunications providers, cloud technology companies, and fleet technology vendors are increasingly focused on capturing long-term revenue streams generated through vehicle data services, over-the-air software updates, connected infotainment offerings, advanced safety functionalities, and digital fleet operations. The market continues to evolve as vehicles become more software-centric, creating new opportunities for recurring service-based business models while accelerating innovation across the connected transportation landscape.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.5 Billion |

| Forecast Value | $98.6 Billion |

| CAGR | 12.4% |

The market currently remains heavily influenced by the widespread adoption of 4G/LTE technologies. Strong network availability, cost-efficient module deployment, and dependable performance continue to support extensive implementation across connected vehicle ecosystems. During the COVID-19 pandemic, the next-generation automotive connectivity solutions market experienced both challenges and opportunities. Initial market growth was constrained by manufacturing disruptions, supply chain disruptions, semiconductor shortages, and reduced vehicle output, thereby slowing the deployment of advanced connected vehicle technologies. Despite these setbacks, long-term demand for connected mobility solutions remained resilient. Vehicle-to-everything (V2X) communication continues to play a critical role in the development of cooperative intelligent transportation systems, enabling seamless interaction between vehicles and surrounding transportation infrastructure.

The 4G/LTE segment accounted for a 46% share in 2025 and is forecast to grow at a 10.7% CAGR from 2026 through 2035. Continued adoption is supported by the proven reliability and affordability of LTE-based technologies. LTE-Advanced, LTE Cat-M1, and NB-IoT solutions remain widely deployed across connected vehicle applications due to their established infrastructure and favorable cost structures.

The passenger cars segment held a 67% share in 2025. Strong demand for digitally enhanced driving experiences continues to support growth across this category. Increasing integration of advanced connectivity technologies, embedded 5G capabilities, over-the-air software delivery, advanced driver assistance systems, electric vehicle optimization functions, remote vehicle controls, and subscription-based digital services is accelerating adoption among passenger vehicle manufacturers and consumers.

United States Next-Generation Automotive Connectivity Solutions Market generated USD 8.9 billion in 2025. Market growth in the country is supported by government initiatives designed to advance connected transportation infrastructure. Funding allocations under the Bipartisan Infrastructure Law have encouraged the development of V2X technologies, while regulatory clarity surrounding the 5.9 GHz spectrum has strengthened the deployment outlook for C-V2X communications. Ongoing efforts related to vehicle communication frameworks and automotive cybersecurity standards continue to support the expansion of connected vehicle ecosystems throughout the U.S.

Major companies operating in the global next-generation automotive connectivity solutions market include Aptiv, Continental (ANS), Harman International, Huawei Smart Car, NXP Semiconductors, Qualcomm, Robert Bosch, TE Connectivity, Texas Instruments, and Thales. Companies operating in the next-generation automotive connectivity solutions market are focusing on several strategic initiatives to strengthen their competitive position and expand market share. Industry participants are investing heavily in research and development to accelerate innovation in 5G connectivity, C-V2X technologies, software-defined vehicle platforms, and advanced telematics systems. Strategic partnerships between automotive manufacturers, semiconductor companies, cloud service providers, and telecommunications operators are becoming increasingly common to build integrated connected mobility ecosystems. Many companies are also expanding their product portfolios through technology acquisitions and collaborative development agreements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Connectivity Architecture

- 2.2.2 Communication Technology

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Technology installers

- 3.1.1.4 Service providers

- 3.1.1.5 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising deployment of 5G & C-V2X infrastructure

- 3.2.1.2 Increasing demand for advanced driver assistance & autonomous connectivity

- 3.2.1.3 Expansion of connected vehicle ecosystems

- 3.2.1.4 Growing adoption of edge computing & ai-enabled connectivity

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Rising cybersecurity vulnerabilities in connected vehicles

- 3.2.2.2 High infrastructure deployment & integration costs

- 3.2.3 Market opportunities

- 3.2.3.1 Transition toward software-defined & connected vehicles

- 3.2.3.2 Rising integration of satellite & hybrid connectivity solutions

- 3.2.3.3 Growth of vehicle-to-everything (V2X) communication platforms

- 3.2.3.4 Expansion of connected infotainment & personalized mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 FCC Spectrum Allocation for C-V2X & 5G Automotive Communications

- 3.5.1.2 NHTSA Vehicle Cybersecurity & Connected Vehicle Safety Guidelines

- 3.5.2 Europe

- 3.5.2.1 EU Connected and Automated Mobility (CAM) Framework

- 3.5.2.2 General Safety Regulation (GSR) for Intelligent Vehicle Systems

- 3.5.2.3 UNECE WP.29 Cybersecurity Regulation (R155)

- 3.5.2.4 UNECE Software Update Management System (SUMS) Regulation (R156)

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Intelligent Connected Vehicle (ICV) Development Strategy

- 3.5.3.2 China C-V2X Commercialization & Smart Highway Initiatives

- 3.5.3.3 Japan Connected Mobility & ITS Roadmap

- 3.5.3.4 South Korea 5G-V2X and Autonomous Vehicle Policy Framework

- 3.5.4 Latin America

- 3.5.4.1 Brazil Connected Mobility & Smart Transportation Programs

- 3.5.4.2 Mexico Automotive Telematics and Digital Infrastructure Expansion Policies

- 3.5.5 MEA

- 3.5.5.1 UAE Smart Mobility & Autonomous Transport Strategy

- 3.5.5.2 Saudi Arabia Intelligent Transportation & Smart City Connectivity Initiatives

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Use cases

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 Automated design optimization

- 3.11.3 Supply chain AI for demand forecasting

- 3.11.4 GenAI use cases & adoption roadmap by segment

- 3.11.5 Risks, Limitations & Regulatory Considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Connectivity Architecture, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Embedded

- 5.3 Integrated

- 5.4 Tethered

Chapter 6 Market Estimates & Forecast, By Communication Technology, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 5G / C-V2X (Cellular Vehicle-to-Everything)

- 6.3 4G / LTE

- 6.4 DSRC / Wi-Fi

- 6.5 Bluetooth / Ultra-Wideband (UWB)

- 6.6 Satellite Connectivity

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 SUV

- 7.2.2 Sedan

- 7.2.3 Hatchback

- 7.3 Commercial Vehicle

- 7.3.1 Light Commercial Vehicle (LCV)

- 7.3.2 Medium Commercial Vehicle (MCV)

- 7.3.3 Heavy Commercial Vehicle (HCV)

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 ICE Vehicles

- 8.3 Battery Electric Vehicles (BEV)

- 8.4 Plug-in Hybrid Electric Vehicles (PHEV)

- 8.5 Hybrid Electric Vehicles (HEV)

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 9.1 ADAS & Autonomous Driving Support

- 9.2 Telematics & Fleet Management

- 9.3 Safety & Emergency Response

- 9.4 Remote Diagnostics & OTA Updates

- 9.5 V2X Communication

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 10.1 OEM/Tier 1

- 10.2 Fleet Operators

- 10.3 Aftermarket & Service Providers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 North America

- 11.1.1 US

- 11.1.2 Canada

- 11.2 Europe

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Italy

- 11.2.5 Spain

- 11.2.6 Belgium

- 11.2.7 Netherlands

- 11.2.8 Sweden

- 11.2.9 Russia

- 11.3 Asia Pacific

- 11.3.1 China

- 11.3.2 India

- 11.3.3 Japan

- 11.3.4 Australia

- 11.3.5 Singapore

- 11.3.6 South Korea

- 11.3.7 Vietnam

- 11.3.8 Indonesia

- 11.3.9 Thailand

- 11.4 Latin America

- 11.4.1 Brazil

- 11.4.2 Mexico

- 11.4.3 Argentina

- 11.5 MEA

- 11.5.1 South Africa

- 11.5.2 Saudi Arabia

- 11.5.3 UAE

- 11.5.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Aptiv

- 12.1.2 Continental

- 12.1.3 Denso

- 12.1.4 Harman International

- 12.1.5 NXP Semiconductors

- 12.1.6 Qualcomm Technologies

- 12.1.7 Robert Bosch

- 12.1.8 TE Connectivity

- 12.1.9 Texas Instruments

- 12.1.10 Thales

- 12.2 Regional Players

- 12.2.1 BlackBerry

- 12.2.2 Ericsson

- 12.2.3 Geotab

- 12.2.4 Huawei Technologies

- 12.2.5 LG Electronics Vehicle Component Solutions

- 12.2.6 Octo Group

- 12.2.7 Sierra Wireless

- 12.2.8 Verizon Connect

- 12.3 Emerging players

- 12.3.1 Mojio

- 12.3.2 Molex