|

시장보고서

상품코드

2083038

식품 및 음료용 에어 필터 시장 : 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Food and Beverages Air Filters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

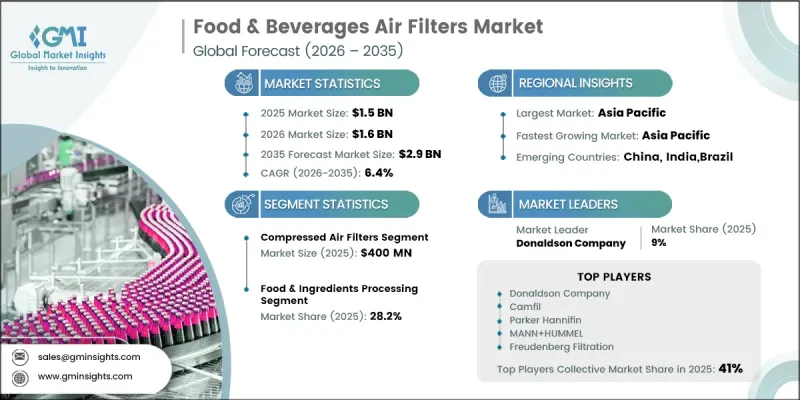

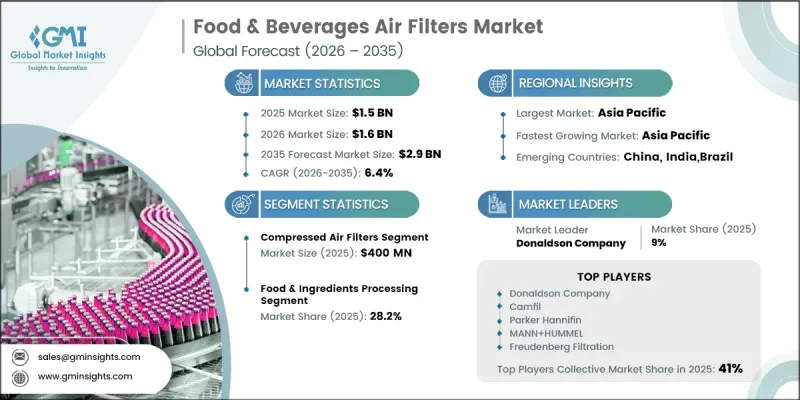

세계의 식품 및 음료용 에어 필터 시장은 2025년에 15억 달러로 평가되었고, CAGR 6.4%로 성장하여 2035년까지 29억 달러에 달할 것으로 예측됩니다.

식품 및 음료 제조업체들이 제품 품질, 업무 효율성 및 위생적인 생산 환경을 높은 수준으로 유지하는 데 점점 더 중점을 두면서, 이 시장은 계속해서 성장세를 보이고 있습니다. 가공 시설의 자동화가 진행되고 생산량이 지속적으로 증가하는 가운데, 깨끗하고 관리가 잘 된 공기를 유지하는 것은 단순한 보조적 기능이 아니라 필수적인 요건이 되었습니다. 효과적인 공기 여과 시스템은 제조의 일관성을 높이고, 오염 위험을 최소화하며, 생산의 신뢰성을 높이고, 중단 없는 가공 작업을 뒷받침하는 데 도움이 됩니다. 식품 안전에 대한 인식이 높아지고 규제 감독이 강화됨에 따라, 각 제조업체들은 가공 시설 전반에 걸쳐 첨단 공기 여과 기술을 도입하고 있습니다. 또한 기업들은 운용 성과를 향상시키는 동시에 끊임없이 진화하는 업계 표준을 더욱 철저히 준수하기 위해 최신 여과 시스템에 투자하고 있습니다. 또한, 제품의 품질과 제조 과정의 투명성에 대한 소비자의 기대가 높아지고 있는 점도 고성능 공기 여과 솔루션에 대한 수요를 지속적으로 뒷받침하고 있습니다. 여과 기술의 지속적인 발전과 식품 가공 시설의 끊임없는 현대화로 인해, 예측 기간 동안 전 세계 식품 및 음료용 공기 필터 시장에 유리한 성장 기회가 창출될 것으로 전망됩니다.

| 시장 범위 | |

|---|---|

| 개시연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 초기 시장 규모 | 15억 달러 |

| 예측액 | 29억 달러 |

| CAGR | 6.4% |

규제 감독이 강화되고 소비자의 기대가 높아짐에 따라, 식품 및 음료 제조업체들은 첨단 공기 여과 시스템에 대한 투자를 확대되고 있습니다. 각 기업은 제품 품질 향상, 제조 공정의 보호, 그리고 안정적인 근무 환경 유지를 위해 보다 청결한 생산 환경을 우선시하고 있습니다. 또한, 최신 여과 기술은 점점 더 엄격해지는 규제 요건을 준수하면서도 시설이 더 높은 생산 기준을 달성할 수 있도록 지원함으로써 업무 효율 향상에도 기여하고 있습니다. 제조업체들이 가공 시설을 현대화해 나가는 가운데, 공기 여과 시스템은 업무 효율성을 높이고 식품의 안전성과 품질에 대한 소비자의 신뢰를 강화하기 위한 필수적인 투자로 자리 잡고 있습니다.

2025년, 압축 공기 필터 부문 시장 규모는 4억 달러에 달했습니다. 압축 공기는 식품 및 음료 제조 공정 전반에 걸쳐 여전히 필수적인 유틸리티이므로, 이 부문은 계속해서 시장을 주도하고 있습니다. 엄격한 공기 청정도 기준과 높아지는 품질 요건으로 인해, 고성능 압축 공기 여과 시스템에 대한 수요는 더욱 증가하고 있습니다. 깨끗한 공기공급을 유지하고, 공정의 신뢰성을 높이며, 일관된 생산 품질을 뒷받침하는 이러한 시스템의 역량이 전 세계 식품 및 음료 업계 전반에 걸쳐 광범위한 도입을 지속적으로 촉진하고 있습니다.

식품·원료 가공 분야는 2025년에 28.2%의 점유율을 기록했습니다. 이 부문이 주도적인 위치를 유지하고 있는 이유는 식품 가공 환경에 따른 광범위한 공기 여과 요건이 있기 때문입니다. 제조업체들은 관리된 생산 조건을 유지하고, 제품 품질을 향상시키며, 업계 표준 준수를 보장하기 위해 첨단 여과 기술이 필요합니다. 전 세계 식품 제조 시설 증가와 생산 현대화를 위한 지속적인 투자가 맞물리면서, 이 용도 부문 전체에서 공기 여과 시스템에 대한 꾸준한 수요를 뒷받침하고 있습니다.

미국의 식품 및 음료용 에어 필터 시장은 2025년에 80%의 점유율을 차지하며 2억 7,600만 달러 시장 규모를 기록했습니다. 북미 전체 시장의 성장은 제조업체들이 첨단 여과 기술에 투자하도록 유도하는 엄격한 규제 준수 요건과 식품 안전 기준에 의해 계속해서 뒷받침되고 있습니다. 개정된 규제 요건이 지속적으로 도입됨에 따라, 특히 높은 수준의 공기 품질 성능이 요구되는 압축 공기 여과 시스템 분야에서 단기적인 수요가 유지될 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 용도별, 2022년-2035년

제7장 시장 추산 및 예측 : 유통 채널별, 2022년-2035년

제8장 시장 추산 및 예측 : 지역별, 2022년-2035년

제9장 기업 개요

LSH 26.07.13The Global Food & Beverages Air Filters Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 2.9 billion by 2035.

The market continues to gain momentum as food and beverage manufacturers place greater emphasis on maintaining high standards of product quality, operational efficiency, and hygienic production environments. As processing facilities become increasingly automated and production volumes continue to rise, maintaining clean and controlled air has become an essential requirement rather than a supporting function. Effective air filtration systems help improve manufacturing consistency, minimize contamination risks, enhance production reliability, and support uninterrupted processing operations. Rising awareness of food safety, coupled with stricter regulatory oversight, is encouraging manufacturers to adopt advanced air filtration technologies across processing facilities. Companies are also investing in modern filtration systems to improve operational performance while strengthening compliance with evolving industry standards. In addition, increasing consumer expectations regarding product quality and manufacturing transparency continue to support demand for high-performance air filtration solutions. Continuous advancements in filtration technologies and ongoing modernization of food processing facilities are expected to create favorable growth opportunities for the global food & beverages air filters market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.4% |

Growing regulatory oversight and heightened consumer expectations are encouraging food and beverage manufacturers to increase investments in advanced air filtration systems. Companies are prioritizing cleaner production environments to improve product quality, protect manufacturing operations, and maintain consistent workplace conditions. Modern filtration technologies also support greater operational efficiency by helping facilities achieve higher production standards while complying with increasingly stringent regulatory requirements. As manufacturers continue upgrading processing facilities, air filtration systems are becoming an essential investment for strengthening operational performance and reinforcing consumer confidence in food safety and quality.

The compressed air filters segment accounted for USD 400 million in 2025. The segment continues to lead the market because compressed air remains a critical utility throughout food and beverage manufacturing operations. Strict air purity standards and increasing quality requirements have further strengthened demand for high-performance compressed air filtration systems. Their ability to maintain clean air supplies, improve process reliability, and support consistent production quality continues to drive widespread adoption across the global food and beverage industry.

The food & ingredients processing reached 28.2% share in 2025. This segment maintains its leading position due to the broad range of air filtration requirements associated with food processing environments. Manufacturers require advanced filtration technologies to maintain controlled production conditions, improve product quality, and ensure compliance with industry standards. The increasing number of food manufacturing facilities worldwide, combined with continued investments in production modernization, continues to support strong demand for air filtration systems across this application segment.

United States Food & Beverages Air Filters Market held an 80% share, generating USD 276 million in 2025. Market growth across North America continues to be supported by strong regulatory compliance requirements and strict food safety standards that encourage manufacturers to invest in advanced filtration technologies. Ongoing implementation of updated regulatory requirements is expected to sustain short-term demand, particularly for compressed air filtration systems requiring enhanced air quality performance.

Major companies operating in the global food & beverages air filters market include Solventum (formerly 3M Purification), Pall Corporation (Danaher), Camfil Group, Parker Hannifin Corporation, Donaldson Company, Inc., MANN+HUMMEL Group, Freudenberg Filtration Technologies, AAF International (American Air Filter), Porvair Filtration Group Ltd., Spirax-Sarco Engineering Plc., Nederman Holding AB, Koch Filter Corporation (Atmus), APC Filtration, Inc., Hengst Filtration, Micronics Engineered Filtration Group (Cleanova), Nano Purification Solutions Ltd., Air Filters, Inc., Permatron Corporation, Intensiv-Filter Himenviro GmbH, TROX Group, and GVS Group S.p.A. Companies operating in the food & beverages air filters market are strengthening their market position by investing in advanced filtration technologies that improve efficiency, durability, and compliance with evolving food safety regulations. Manufacturers are expanding research and development activities to introduce high-performance filtration systems capable of supporting increasingly automated production environments. Strategic collaborations with food processing companies and equipment manufacturers are helping suppliers broaden their customer base and strengthen long-term business relationships. Businesses are also enhancing manufacturing capabilities, optimizing supply chains, and expanding their global distribution networks to improve product availability and market reach.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Business trends

- 2.3 Product type trends

- 2.4 Application trends

- 2.5 Distribution channel trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem and value chain analysis

- 3.1.1 Raw material suppliers (filter media, frames, activated carbon)

- 3.1.2 Filter manufacturers & OEMs

- 3.1.3 Distribution channels (direct, distributors, system integrators)

- 3.1.4 End-use food & beverage processors

- 3.2 Industry impact forces

- 3.2.1 Market Driver

- 3.2.2 Market challenges/pitfalls

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Industry ecosystem analysis

- 3.5 Regulatory framework

- 3.5.1 U.S.: FDA food safety modernization act (FSMA), OSHA air quality standards

- 3.5.2 European Union: EC 1935/2004, EN 1822 HEPA classification, ATEX directives

- 3.5.3 Asia Pacific: China GB standards, India FSSAI guidelines

- 3.5.4 Global ISO 8573 compressed air quality standards

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7 Technology and innovation landscape

- 3.7.1 Advances in filter media (nanofiber, ePTFE, electrospun media)

- 3.7.2 Smart & IoT-enabled air filter monitoring systems

- 3.7.3 Energy-efficient & low-pressure-drop filter designs

- 3.8 Porter’s Analysis

- 3.9 PESTEL Analysis

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import/export volume & value trends: air filtration equipment (HS code 8421)

- 3.10.2 Key trade corridors & tariff impact on F&B air filter markets

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption: predictive maintenance & filter lifecycle optimization

- 3.11.2 GenAI use cases & adoption roadmap by F&B segment

- 3.11.3 Risks, limitations & regulatory considerations for AI in food-grade environments

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region & key filter producer (driven by primary research)

- 3.12.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 APAC

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Billion)(Thousand Units)

- 5.1 Key trends

- 5.2 Dust collectors

- 5.2.1 Cartridge collectors

- 5.2.2 Baghouse filters

- 5.2.3 Cyclone / inertial separators

- 5.3 Mist collectors

- 5.4 EPA / HEPA / ULPA filters

- 5.4.1 EPA filters (E10-E12)

- 5.4.2 HEPA filters (H13-H14)

- 5.4.3 ULPA filters (U15-U17)

- 5.5 Activated carbon / odor & VOC control filters

- 5.6 Compressed air filters

- 5.6.1 Particulate filters

- 5.6.2 Coalescing filters

- 5.6.3 Sterile / membrane filters

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Dairy

- 6.2.1 Food & ingredients processing

- 6.2.2 Bakery & confectionery

- 6.2.3 Flour milling & grain processing

- 6.2.4 Spices & seasonings processing

- 6.3 Bottled water

- 6.4 Non-alcoholic beverages

- 6.5 Brewery & alcoholic beverages

- 6.6 Meat & poultry processing

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Indirect sales

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Solventum

- 9.1.2 Pall Corporation (Danaher)

- 9.1.3 Camfil Group

- 9.1.4 Parker Hannifin Corporation

- 9.1.5 Donaldson Company, Inc.

- 9.1.6 MANN+HUMMEL Group

- 9.1.7 Freudenberg Filtration Technologies

- 9.1.8 AAF International

- 9.2 Regional Champions

- 9.2.1 Porvair Filtration Group Ltd.

- 9.2.2 Spirax-Sarco Engineering Plc.

- 9.2.3 Nederman Holding AB

- 9.2.4 Koch Filter Corporation (Atmus)

- 9.2.5 APC Filtration, Inc.

- 9.2.6 Hengst Filtration

- 9.2.7 Micronics Engineered Filtration Group

- 9.3 Niche/Specialist Players

- 9.3.1 Nano Purification Solutions Ltd.

- 9.3.2 Air Filters, Inc.

- 9.3.3 Permatron Corporation

- 9.3.4 Intensiv-Filter Himenviro GmbH

- 9.3.5 TROX Group

- 9.3.6 GVS Group S.p.A.

- 9.3.7 Oerlikon AM