|

시장보고서

상품코드

1934627

차량용 에어 필터 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Air Filter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

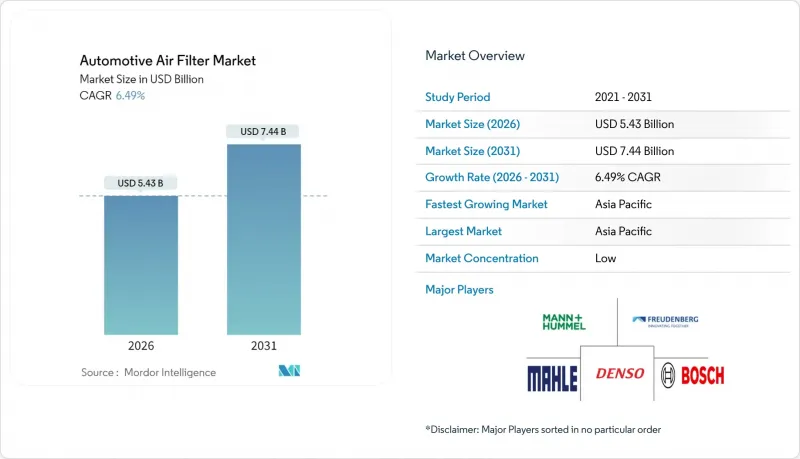

차량용 에어 필터 시장은 2025년에 51억 달러로 평가되었고, 2026년 54억 3,000만 달러에서 2031년까지 74억 4,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 6.49%로 예상됩니다.

유럽, 북미 및 주요 아시아 경제권에서 강화된 배출가스 규제와 더불어 차량 내 공기질에 대한 소비자의 관심이 높아지면서 견조한 수요가 지속되고 있습니다. 자동차 제조업체(OEM)는 유로 7, EPA 2027-2032 다오염물질 기준 및 Barato Stage VI 규제 준수를 위해 HEPA(고효율 입자 공기) 시스템 및 정전기 나노섬유 미디어의 채택을 확대하고 있습니다. 전기자동차(EV) 플랫폼은 배터리 열 관리 시스템과 정숙성이 높은 캐빈이 필터 성능의 차이를 두드러지게 하기 때문에 이 기회를 더욱 확대할 것입니다. 동시에 애프터마켓 유통업체들은 예측 유지보수 데이터를 활용하여 프리미엄 교체용 필터를 포지셔닝하고, 합성 매체로 인한 서비스 간격의 장기화에 대응하고 있습니다.

세계 자동차 에어필터 시장 동향과 인사이트

엄격한 배기가스 규제와 차량 실내 공기질 기준

주요 자동차 시장의 규제 수렴으로 엔진 보호와 실내 공기질을 동시에 충족시키는 첨단 여과 기술에 대한 수요가 그 어느 때보다 높아지고 있습니다. EU의 유로 7 규정은 타이어와 브레이크 마모로 인한 입자상 물질 배출량 상한을 처음으로 도입하여 기존의 배기가스 배출량을 초과하는 입자를 포집하는 여과 시스템을 요구하고 있습니다. 이번 규제 확대는 미국 환경보호청(EPA)이 휘발유 차량에 0.5mg/마일의 PM 배출량을 달성하는 미립자 필터를 의무화하는 Tier 4 기준과 시기가 일치하며, 필터의 가치 제안을 선택적 편의 장비에서 규제 준수를 위한 필수 요건으로 근본적으로 변화시키고 있습니다. 캄보디아가 2030년까지 유로 6/VI 표준을 채택한 것은 규제 조화가 선진국 시장을 넘어 확대되고 있음을 보여주며, 필터 공급업체에게 전 세계적인 기회를 창출하고 있습니다. 규제 일정이 단축됨에 따라 OEM 제조업체는 필터 기술 통합을 가속화해야 하며, 규정 준수 기한은 인위적인 수요 급증을 초래할 수 있습니다. 이를 통해 즉시 도입 가능한 솔루션을 보유한 공급업체가 혜택을 받을 수 있습니다. 캘리포니아주의 'Advanced Clean Car II Program'은 2035년까지 100% 무공해 자동차 판매를 의무화하고 있지만, 아이러니하게도 EV는 배터리의 열 효율을 유지하기 위해 고급 실내 공기 관리 시스템이 필요하기 때문에 필터 수요가 증가하고 있습니다.

늘어나는 세계 자동차 보유 대수와 서비스 간격 주행거리 확대

특히 신흥 시장에서의 세계 자동차 보유대수 확대는 신차 생산 증가율을 상회하는 지속적인 애프터마켓 수요를 창출하고 있습니다. 합성 윤활유 채택과 엔진 내구성 향상으로 인한 서비스 간격의 연장은 역설적으로 필터가 효율 기준을 유지하면서 교체 간격을 늘려야 하기 때문에 필터 시스템의 부하를 증가시킵니다. 이러한 추세는 OEM 사양을 충족하는 장수명 제품으로 높은 수익률을 확보할 수 있는 프리미엄 필터 제조업체에 유리하게 작용합니다. 차량 운영자들은 총소유비용(TCO)에서 프리미엄 필터의 이점을 점점 더 많이 인식하고 있으며, 예지보전 알고리즘을 통해 상태에 따른 교체 일정을 설정하여 필터 활용을 최적화하고 엔진의 조기 마모를 방지할 수 있습니다. 서비스형 모빌리티(Mobility as a Service, MaaS) 모델로의 전환은 상용차가 승용차보다 연간 주행거리가 길기 때문에 필터 교체 빈도를 높여 애프터마켓 공급업체에게 보다 예측 가능하고 수익성 높은 교체 주기를 만들어내고 있습니다.

장수명 합성 미디어로 교체 주기 연장

첨단 합성 필터 미디어 기술은 기존의 교체 주기를 넘어 서비스 주기를 연장하여 역설적으로 시장 성장을 억제합니다. Hollingsworth &Vose의 나노웹 시스템과 같은 나노섬유 코팅 기술은 심층 여과 및 펄스 세정 성능을 향상시켜 필터의 효율 유지 기간을 연장하는 동시에 교체 빈도를 줄여줍니다. 이러한 기술 발전은 우수한 제품 성능이 교체 빈도의 감소를 통해 잠재적 시장 규모를 감소시키는 전형적인 혁신가의 딜레마를 야기합니다. 고급 자동차 제조업체들은 유지보수 비용 절감과 고객 만족도 향상을 위해 장수명 여과 시스템을 표준으로 장착하는 추세가 강화되고 있으며, 그 결과 애프터마켓의 수익성을 제약하고 있습니다. 고급 전기자동차의 '평생 사용'형 밀폐형 캐빈 필터 모듈의 보급은 애프터마켓 교체 기회를 완전히 없애고, 공급업체는 정기적인 애프터마켓 판매에 의존하지 않고 OEM 공급 시 높은 마진율을 확보해야 합니다. 이란의 베할란 필터(Beharan Filter)는 나노기술을 적용한 자동차 에어필터로서는 최초로 '나노 나마드(Nano Namad)' 라이선스를 획득하며, 신흥 시장이 서비스 주기를 연장하는 첨단 필터 기술로 빠르게 전환하고 있는 실례를 보여주고 있습니다. 필터 제조업체는 기술 혁신과 비즈니스 모델의 지속가능성 사이의 균형을 맞추고, 물리적 필터 교체 빈도에 의존하지 않는 정기적인 수익원을 창출하고, 구독형 유지보수 서비스나 부가가치형 모니터링 시스템으로 전환해야할 것입니다.

부문 분석

흡기 필터는 2025년 54.78%의 시장 점유율을 차지할 것으로 예상되며, 이는 모든 차종에 대한 보편적 적용 가능성과 엔진 보호 요구 사항으로 인한 의무적 교체 주기를 반영합니다. 그러나 실내 공기 필터는 소비자의 건강 인식 증가와 차량 내 공기질 개선에 대한 규제 의무에 힘입어 2031년까지 연평균 8.94%의 성장세를 보이며 성장의 견인차 역할을 하고 있습니다.

보쉬가 바이러스, 박테리아, 알레르겐에 효과적인 항균층을 갖춘 'FILTER+pro' 캐빈 에어 필터를 도입한 사례는 기존 공급업체가 캐빈 필터 분야에서 프리미엄 가격을 얻기 위한 혁신적 자세를 보여주고 있습니다. 공기질 규제와 소비자의 건강 인식이 높아지면서 캐빈 필터 성능 향상에 대한 지속적인 수요가 창출되고 있으며, OEM 업체들은 고급차 부문에서 HEPA 등급 시스템을 표준으로 장착하는 추세가 강화되고 있습니다. 흡기 필터는 엔진 보호의 필요성으로 인해 안정적인 수요를 유지하고 있지만, 성숙한 기술과 확립된 교체 주기로 인해 성장률은 캐빈 필터보다 낮습니다. 정전기 및 나노섬유 부문은 업계의 기술적 최첨단을 달리고 있으며, 공급업체들은 기존 미디어 성능을 뛰어넘는 고급 입자 포집 능력으로 프리미엄 가격을 실현하고 있습니다.

셀룰로오스는 저렴한 비용과 제조업체의 높은 이해도로 인해 2025년 기준 43.75%의 점유율을 유지했습니다. 나노섬유 및 HEPA 미디어의 자동차 에어 필터 시장 규모는 CAGR 11.12%로 확대될 것으로 예상되며, 이는 프리미엄 고효율 미디어가 혁신의 속도를 결정하고 있음을 명확히 보여줍니다.

나노섬유층은 낮은 저항을 유지하면서 심층 집진 및 높은 먼지 보유 능력을 추가합니다. 이는 엔진 성능과 HVAC 에너지 효율에 있어 매우 중요한 이점입니다. 공급업체들은 기존 기판에 독자적인 나노 코팅을 통합하여 상당한 가격 프리미엄을 수반하는 차별화된 SKU를 창출하고 있습니다. 활성탄 제조업체들은 원자재 가격 변동에 대응하기 위해 재활용 기술에 투자하고 있으며, 자동차 제조업체와 규제 당국이 요구하는 성능과 지속가능성이라는 두 가지 가치 제안을 강화하고 있습니다.

지역별 분석

2025년 아시아태평양이 38.60%의 점유율을 차지하는 배경에는 중국의 전기차 급증과 인도의 Bharat Stage VI 규제가 있습니다. 이 지역은 예측 기간 동안 CAGR 6.28%로 확대될 것으로 예측됩니다. 현지 공급업체는 선진 미디어 기술 라이선스를 확보하기 위해 세계 브랜드와 제휴하고, 중국, 태국, 베트남의 비용 효율적인 생산기지가 세계 수요를 뒷받침합니다. 호주에서 유로6d에 상응하는 배기가스 규제 도입으로 규제 대상 시장이 더욱 확대될 것으로 보입니다.

유럽에서 유로 7 규제의 비배출 미립자 물질의 추가는 타이어 마모 입자 포집 장치 및 브레이크 먼지 필터와 같은 새로운 틈새 시장을 개척하고 있습니다. 독일 자동차 제조업체는 HEPA 필터와 센서의 통합을 주도하고 있으며, MANN+HUMMEL과 같은 공급업체와 자주 공동 개발을 하고 있습니다. Hengst의 루마니아 공장은 동유럽의 원가 경쟁력이 새로운 생산 능력을 유치하고 있음을 보여주고 있습니다. 소비자들은 고급 필터 기술을 건강 증진 및 환경적 책임과 연결하여 인식하고 있으며, 이는 프리미엄 가격 책정을 뒷받침하고 있습니다.

북미 EPA의 2027-2032년 규정은 고효율 엔진 에어 시스템 및 캐빈 시스템에 대한 지속적인 수요를 보장합니다. 캘리포니아주의 무공해 자동차 의무화는 EV 전용 열관리 필터에 대한 수요를 자극할 것입니다. 한온시스템의 온타리오주 EV 컴프레서 공장은 확대되는 지역 EV 생산에 대응하기 위한 공급업체 투자의 증거입니다. 잘 정비된 애프터마켓 물류망과 강력한 DIY 문화가 성능 향상 부품의 빠른 보급을 보장합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 : 달러/수량 : 대수)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

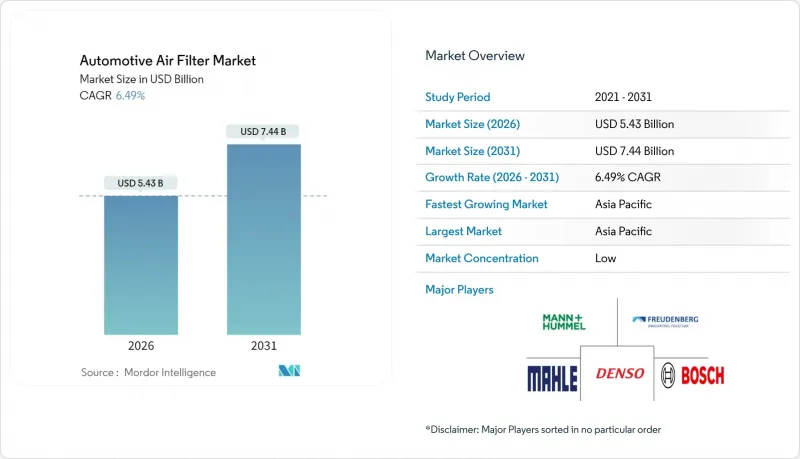

LSH 26.03.05The Automotive Air Filter Market was valued at USD 5.10 billion in 2025 and estimated to grow from USD 5.43 billion in 2026 to reach USD 7.44 billion by 2031, at a CAGR of 6.49% during the forecast period (2026-2031).

Tightening emission norms in Europe, North America, and key Asian economies, together with consumer attention to in-cabin air quality, sustain a robust demand pipeline. Original equipment manufacturers (OEMs) increasingly specify high-efficiency particulate air (HEPA) systems and electrostatic nano-fiber media to comply with Euro 7, EPA 2027-2032 multi-pollutant standards, and Bharat Stage VI rules. Electric-vehicle (EV) platforms amplify the opportunity because battery thermal systems and silent cabins highlight filtration performance differences. At the same time, aftermarket distributors leverage predictive maintenance data to position premium replacement filters, countering the lengthening service intervals delivered by synthetic media.

Global Automotive Air Filter Market Trends and Insights

Strict Emission & In-Cabin Air-Quality Mandates

Regulatory convergence across major automotive markets creates unprecedented demand for advanced filtration technologies that address engine protection and cabin air quality. The EU's Euro 7 regulation introduces particulate emissions limits from tire and brake wear for the first time, requiring filtration systems to capture particles beyond traditional exhaust emissions. This regulatory expansion coincides with the EPA's Tier 4 standards mandating gasoline particulate filters for vehicles achieving 0.5 mg/mi PM emissions, fundamentally altering the filtration value proposition from an optional comfort feature to a regulatory compliance necessity. Cambodia's adoption of Euro 6/VI standards by 2030 demonstrates regulatory harmonization extending beyond developed markets, creating global scale opportunities for filtration suppliers. The regulatory timeline compression forces OEMs to accelerate filtration technology integration, with compliance deadlines creating artificial demand spikes that benefit suppliers with ready-to-deploy solutions. California's Advanced Clean Cars II program mandating 100% zero-emission vehicle sales by 2035 paradoxically increases filtration demand as EVs require sophisticated cabin air management systems to maintain battery thermal efficiency.

Growing Global Vehicle Parc & Service-Interval Mileage

The expanding global vehicle fleet, particularly in emerging markets, creates sustained aftermarket demand that outpaces new vehicle production growth rates. Extended service intervals, driven by synthetic lubricant adoption and improved engine durability, paradoxically increase filtration system stress as filters must perform longer between replacements while maintaining efficiency standards. This dynamic benefits premium filter manufacturers who can command higher margins for extended-life products that meet OEM specifications. Fleet operators increasingly recognize the benefits of premium filtration for total cost of ownership, with predictive maintenance algorithms enabling condition-based replacement schedules that optimize filter utilization while preventing premature engine wear. The shift toward mobility-as-a-service models intensifies filter replacement frequency as commercial vehicles accumulate higher annual mileage than private passenger cars, creating a more predictable and lucrative replacement cycle for aftermarket suppliers.

Long-Life Synthetic Media Extending Replacement Intervals

Advanced synthetic filter media technologies paradoxically constrain market growth by extending service intervals beyond traditional replacement cycles. Nano-fiber coating technologies, such as Hollingsworth & Vose's NANOWEB system, enhance depth filtration and pulse-cleaning capabilities, enabling filters to maintain efficiency longer while reducing replacement frequency. This technological advancement creates a classic innovator's dilemma where superior product performance reduces total addressable market size by decreasing replacement frequency. Premium vehicle manufacturers increasingly specify long-life filtration systems as standard equipment to reduce maintenance costs and improve customer satisfaction scores, inadvertently constraining aftermarket revenue potential. The trend toward "lifetime" sealed cabin filter modules in luxury EVs eliminates aftermarket replacement opportunities entirely, forcing suppliers to capture higher margins during OEM fitment rather than relying on recurring aftermarket sales. Iran's Behran Filter Company, receiving the first "Nano Namad" license for nanotechnology-based car air filters, demonstrates how emerging markets are leapfrogging to advanced filtration technologies that extend service intervals. Filter manufacturers must balance technological advancement with business model sustainability, potentially requiring shift toward subscription-based maintenance services or value-added monitoring systems that generate recurring revenue streams independent of physical filter replacement frequency.

Other drivers and restraints analyzed in the detailed report include:

- Consumer Health Awareness in High-Pollution Megacities

- HEPA-Grade Filters Adopted by EV & Premium OEM Platforms

- Volatile Non-Woven & Activated-Carbon Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-intake filters command 54.78% market share in 2025, reflecting their universal application across all vehicle types and mandatory replacement cycles driven by engine protection requirements. However, cabin air filters emerge as the growth catalyst with 8.94% CAGR through 2031, propelled by consumer health awareness and regulatory mandates for in-cabin air quality improvement.

Bosch's introduction of FILTER+pro cabin air filters with antimicrobial layers effective against viruses, bacteria, and allergens demonstrates how traditional suppliers innovate to capture premium pricing in the cabin filtration segment. The convergence of air quality regulations and consumer health consciousness creates sustained demand for cabin filtration upgrades, with OEMs increasingly specifying HEPA-grade systems as standard equipment in premium vehicle segments. Air-intake filters maintain steady demand driven by engine protection requirements, though growth rates lag cabin filters due to mature technology and established replacement cycles. The electrostatic and nano-fiber segments represent the industry's technological frontier, where suppliers command premium pricing for advanced particle capture capabilities that exceed traditional media performance.

Cellulose retained a 43.75% share in 2025 because it is inexpensive and well-understood by manufacturers. The automotive air filtration market size for nano-fiber and HEPA media is projected to expand at 11.12% CAGR, a clear indicator that premium, high-efficiency media sets the innovation pace.

Nanofiber layers add depth loading and high dust-holding capacity while maintaining low restriction, a critical benefit for engine performance and HVAC energy efficiency. Suppliers integrate proprietary nano-coatings into traditional substrates to create differentiated SKUs with significant price premiums. Activated-carbon producers invest in recycling technology to combat feedstock price swings, reinforcing the dual performance and sustainability value proposition demanded by automakers and regulators.

The Automotive Air Filter Market Report is Segmented by Product Type (Air-Intake Filters, Cabin Air Filters, Hybrid Filters, and More), Filter Media (Cellulose, Synthetic, Activated-Carbon Composite, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM Fitment and Aftermarket) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific's 38.60% share in 2025 is backed by China's EV surge and India's Bharat Stage VI norms. The region is anticipated to grow with a 6.28% CAGR during the forecast period. Local suppliers collaborate with global brands to secure advanced media licenses, while cost-efficient manufacturing plants in China, Thailand, and Vietnam feed worldwide demand. Australia's adoption of Euro 6d-equivalent tailpipe limits further widens the regulatory addressable market.

Euro 7's inclusion of non-exhaust particles in Europe opens niches for tire-wear capture devices and brake-dust filters. German OEMs spearhead HEPA and sensor integration, often co-engineering with suppliers such as MANN+HUMMEL. Hengst's Romanian plant shows that Eastern Europe's cost base attracts new capacity. Consumers associate advanced filtration with wellness and environmental responsibility, supporting premium pricing.

The EPA's 2027-2032 rules in North America guarantee sustained demand for high-efficiency engine-air and cabin systems. California's zero-emission vehicle mandate stimulates demand for EV-specific thermal-management filters. Hanon Systems' Ontario EV compressor plant signals supplier investment to serve growing regional EV output. Well-developed aftermarket logistics and strong do-it-yourself cultures ensure rapid uptake of performance upgrades.

- MANN+HUMMEL GmbH

- MAHLE GmbH

- Donaldson Company Inc.

- Robert Bosch GmbH

- Sogefi SpA

- Cummins Inc.

- DENSO Corporation

- Parker-Hannifin Corp.

- Ahlstrom-Munksjo

- Freudenberg & Co. KG

- Hengst SE

- K&N Engineering Inc.

- Champion Laboratories Inc.

- Fram Group LLC

- Hollingsworth & Vose Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict emission & in-cabin air-quality mandates

- 4.2.2 Growing global vehicle parc & service-interval mileage

- 4.2.3 Consumer health awareness in high-pollution megacities

- 4.2.4 HEPA-grade filters adopted by EV & premium OEM platforms

- 4.2.5 Sensor-activated smart HVAC filtration modules

- 4.2.6 Predictive fleet-maintenance algorithms driving filter turnover

- 4.3 Market Restraints

- 4.3.1 Long-life synthetic media extending replacement intervals

- 4.3.2 Volatile non-woven & activated-carbon prices

- 4.3.3 Sealed "lifetime" cabin-filter modules in luxury EVs reduce aftermarket

- 4.3.4 Energy/weight penalty of ultra-high-efficiency media in BEVs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value in USD and Volume in Units)

- 5.1 By Product Type

- 5.1.1 Air-Intake Filters

- 5.1.2 Cabin Air Filters

- 5.1.3 Hybrid / Electrostatic Nano-fiber Filters

- 5.1.4 Electrically-enhanced (ePM1) Filters

- 5.2 By Filter Media

- 5.2.1 Cellulose

- 5.2.2 Synthetic/Melt-blown

- 5.2.3 Activated-Carbon Composite

- 5.2.4 Nano-fiber/HEPA Grade

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Sales Channel

- 5.4.1 OEM Fitment

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia & New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC Countries

- 5.5.5.2 Turkey

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, and Capacity)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 MANN+HUMMEL GmbH

- 6.4.2 MAHLE GmbH

- 6.4.3 Donaldson Company Inc.

- 6.4.4 Robert Bosch GmbH

- 6.4.5 Sogefi SpA

- 6.4.6 Cummins Inc.

- 6.4.7 DENSO Corporation

- 6.4.8 Parker-Hannifin Corp.

- 6.4.9 Ahlstrom-Munksjo

- 6.4.10 Freudenberg & Co. KG

- 6.4.11 Hengst SE

- 6.4.12 K&N Engineering Inc.

- 6.4.13 Champion Laboratories Inc.

- 6.4.14 Fram Group LLC

- 6.4.15 Hollingsworth & Vose Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment