|

시장보고서

상품코드

2083136

시비용 플라즈마 활성수 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Plasma-Activated Water (PAW) for Fertilization Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

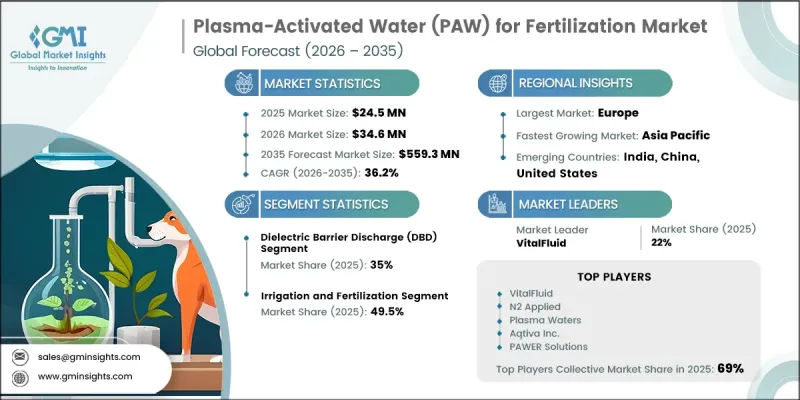

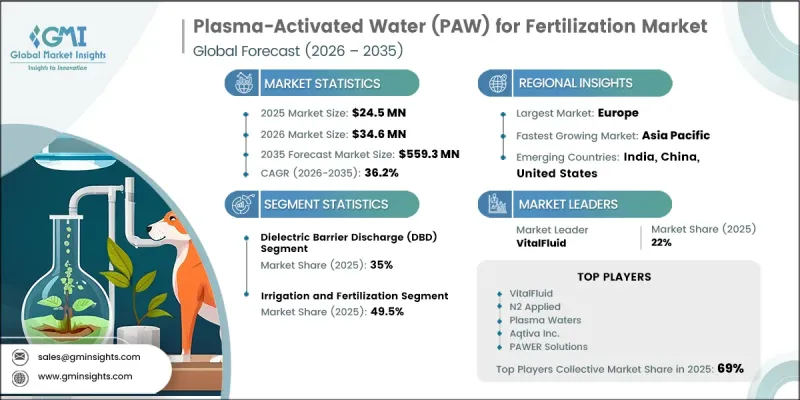

세계의 시비용 플라즈마 활성수 시장은 2025년에 2,450만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 36.2%로 성장하여 5억 5,930만 달러에 달할 것으로 추정되고 있습니다.

농업이 저탄소·자원 효율이 높은 정밀 영양분 공급 시스템으로 점점 더 전환되고 있는 가운데, 비료용 플라즈마 활성수 시장은 급속히 확대되고 있습니다. 이 기술이 주목받고 있는 이유는 대기압 하에서 작동하는 비열 플라즈마 반응을 이용하여 질산염(NO₂)이나 아질산염(NO₂)과 같은 식물이 흡수할 수 있는 질소 화합물을 생성함으로써, 기존의 질소 생산 방법에 대한 의존도를 낮출 수 있기 때문입니다. 이러한 전환은 농업 투입재에 대한 광범위한 탈탄소화 목표와 부합하며, 지속가능성을 중시하는 농업 관행을 뒷받침하고 있습니다. 온실 재배, 수경 재배, 수직 농업 시스템 등 제어 환경 농업의 도입이 확대되고 있는 점도, 일관된 양분 공급과 자원 효율 향상을 보장하는 정밀 시비 솔루션에 대한 수요를 더욱 가속화하고 있습니다. 추적 가능하고 잔류물이 없는 농업 자재에 대한 수요가 증가함에 따라, 특히 고부가가치 작물 생산 분야에서 플라즈마 활성수 시스템의 도입이 촉진되고 있습니다. 동시에, 물 부족, 토양 황폐화, 비료 가격 변동과 관련된 우려가 커짐에 따라 생산자들은 대체 영양소 생산 방법을 모색하고 있습니다. 플라즈마 발생 시스템의 기술적 발전과 최신 관개 인프라와의 통합을 통해 전 세계 농업 분야에서 시장 확대가 더욱 가속화될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 금액 | 2,450만 달러 |

| 예측 금액 | 5억 5,930만 달러 |

| CAGR | 36.2% |

2025년에는 유전체 배리어 방전(DBD) 시스템 부문이 35%의 점유율을 차지하며, 기술 부문 중 가장 높은 점유율을 유지했습니다. 이 부문이 선도적인 위치를 차지하고 있는 것은 안정적인 작동 성능, 확장성이 뛰어난 시스템 설계, 그리고 농업 분야에서의 폭넓은 실증 실적 덕분입니다. DBD 기반 플라즈마 시스템은 전극 사이에 배치된 유전체 층을 통해 비열 방전을 발생시켜, 반응성이 높은 질소 및 산소 종을 효율적으로 생성합니다. 이것들은 물에 용해되어 식물이 흡수할 수 있는 양액이 됩니다. 이러한 입증된 신뢰성과 다양한 농업 환경에 대한 적응성이 계속해서 해당 부문의 우위를 뒷받침하고 있습니다.

관개 및 비료 부문은 2025년에 49.5%의 점유율을 차지했습니다. 이러한 장점은 플라즈마 활성수를 기존 관개 시스템에 원활하게 통합할 수 있다는 점에 기인하며, 농업인은 농업 관행을 크게 변경하지 않고도 기존의 질소 시비를 강화하거나 대체할 수 있게 됩니다. 점적 관개, 스프링클러 및 순환식 비료 공급 시스템과의 호환성 덕분에, 관리 재배 환경과 노지 재배 환경 모두에서 널리 채택되고 있으며, 이것이 시장 수요의 주요 촉진요인이 되고 있습니다.

북미의 비료용 플라즈마 활성수 시장은 온타리오주와 브리티시컬럼비아주 등 지역의 캐나다 온실 원예 부문 확대에 힘입어 2025년에는 35%의 시장 점유율을 차지했습니다. 미국 시장은 지속 가능한 작물 생산에 초점을 맞춘 연구 주도형 노력과, 정밀한 영양분 공급 및 잔류물 없는 재배가 점점 더 중요시되는 고부가가치 농업 분야에서의 상업적 도입을 통해 진화를 거듭하고 있습니다. 첨단 농업 기술 및 제어 환경 농업에 대한 투자 확대가 계속해서 이 지역 시장 성장을 뒷받침하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 플라즈마 발생 기술별, 2022년-2035년

제6장 시장 추산 및 예측 : 용도별, 2022년-2035년

제7장 시장 추산 및 예측 : 최종사용자별, 2022년-2035년

제8장 시장 추산 및 예측 : 작물 유형별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSH 26.07.14The Global Plasma-Activated Water for Fertilization Market was valued at USD 24.5 million in 2025 and is estimated to grow at a CAGR of 36.2% to reach USD 559.3 million by 2035.

The plasma-activated water for fertilization market is witnessing rapid expansion as agriculture increasingly shifts toward low-carbon, resource-efficient, and precision nutrient delivery systems. The technology is gaining attention because it produces plant-available nitrogen compounds such as nitrate (NO2) and nitrite (NO2) using non-thermal plasma reactions that operate at atmospheric pressure, reducing reliance on conventional nitrogen production methods. This transition aligns with broader decarbonization goals in agricultural inputs and supports sustainability-focused farming practices. Rising adoption of controlled environment agriculture, including greenhouse cultivation, hydroponic production, and vertical farming systems, is further accelerating demand for precision fertilization solutions that ensure consistent nutrient delivery and improved resource efficiency. The growing need for traceable, residue-free agricultural inputs is also reinforcing the adoption of plasma-activated water systems, particularly in high-value crop production. At the same time, increasing concerns related to water scarcity, soil degradation, and fertilizer cost volatility are encouraging growers to explore alternative nutrient generation methods. Technological advancements in plasma generation systems and integration with modern irrigation infrastructure are expected to further strengthen market expansion across global agricultural applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.5 Million |

| Forecast Value | $559.3 Million |

| CAGR | 36.2% |

In 2025, the dielectric barrier discharge (DBD) systems segment accounted for 35% share, holding the largest share among technology categories. This segment leads due to its stable operating performance, scalable system design, and extensive validation in agricultural applications. DBD-based plasma systems generate non-thermal discharge through dielectric layers placed between electrodes, enabling efficient formation of reactive nitrogen and oxygen species that dissolve into water to create plant-available nutrient solutions. Its proven reliability and adaptability across different agricultural setups continue to support its dominant position.

The irrigation and fertilization segment held a 49.5% share in 2025. This dominance is driven by the seamless integration of plasma-activated water into existing irrigation systems, enabling growers to enhance or replace conventional nitrogen inputs without significant changes to agricultural practices. The compatibility with drip, sprinkler, and recirculating fertigation systems supports widespread adoption across controlled and open-field farming environments, making it a key driver of market demand.

North America Plasma-Activated Water for Fertilization Market accounted for 35% share in 2025, supported by Canada's expanding greenhouse horticulture sector in regions such as Ontario and British Columbia. The U.S. market is evolving through both research-led initiatives focused on sustainable crop production and commercial adoption in high-value agricultural segments where precision nutrient delivery and residue-free cultivation are increasingly prioritized. Growing investment in advanced agricultural technologies and controlled environment farming continues to support regional market expansion.

Major companies operating in the global plasma-activated water for fertilization industry include VitalFluid, N2 Applied, Plasma Waters, Aqtiva Inc., PAWER Solutions, HydroPlasma.Tech, cNTP AgriTech, Plasma Systems, Redhill Scientific, Greenpath Industries, Global Enviro, WIADAP Plasma Tech, US Plasma Engineering, AJ Plasmatech, and Eddaion. Companies operating in the plasma-activated water for fertilization market are strengthening their competitive position through continuous investment in plasma generation technology, system efficiency improvements, and integration with advanced irrigation infrastructure. Market participants are focusing on enhancing energy efficiency, scalability, and operational reliability to support broader adoption across commercial agriculture. Strategic collaborations with research institutions and agricultural technology providers enable faster validation and commercialization of new applications. Businesses are also expanding pilot projects and demonstration farms to increase awareness and build grower confidence in plasma-based fertilization systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Plasma Generation Technology

- 2.2.3 Application

- 2.2.4 End-User

- 2.2.5 Crop Type

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By crop type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Plasma Generation Technology, 2022-2035 (USD Million)

- 5.1 Key trends

- 5.2 Dielectric Barrier Discharge (DBD)

- 5.3 Corona Discharge

- 5.4 Atmospheric Pressure Plasma Jets (APPJ)

- 5.5 Microwave Discharge

- 5.6 Gliding Arc Discharge

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million)

- 6.1 Key trends

- 6.2 Irrigation & Fertilization

- 6.3 Seed Treatment & Priming

- 6.4 Foliar Application & Plant Protection

- 6.5 Post-Harvest Treatment

Chapter 7 Market Estimates and Forecast, By End-User, 2022-2035 (USD Million)

- 7.1 Key trends

- 7.2 Controlled Environment Agriculture (CEA)

- 7.3 Open-Field Agriculture

- 7.4 Organic Farms

- 7.5 Nurseries & Horticulture

- 7.6 Research Institutions

Chapter 8 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Million)

- 8.1 Key trends

- 8.2 Vegetables

- 8.3 Cereals & Grains

- 8.4 Fruits

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 VitalFluid

- 10.2 N2 Applied

- 10.3 Plasma Waters

- 10.4 Aqtiva Inc.

- 10.5 PAWER Solutions

- 10.6 HydroPlasma.Tech

- 10.7 cNTP AgriTech

- 10.8 Plasma Systems

- 10.9 Redhill Scientific

- 10.10 Greenpath Industries

- 10.11 Global Enviro

- 10.12 WIADAP Plasma Tech

- 10.13 US Plasma Engineering

- 10.14 AJ Plasmatech

- 10.15 Eddaion