|

시장보고서

상품코드

2083355

테스트 및 측정 장비 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Test and Measurement Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

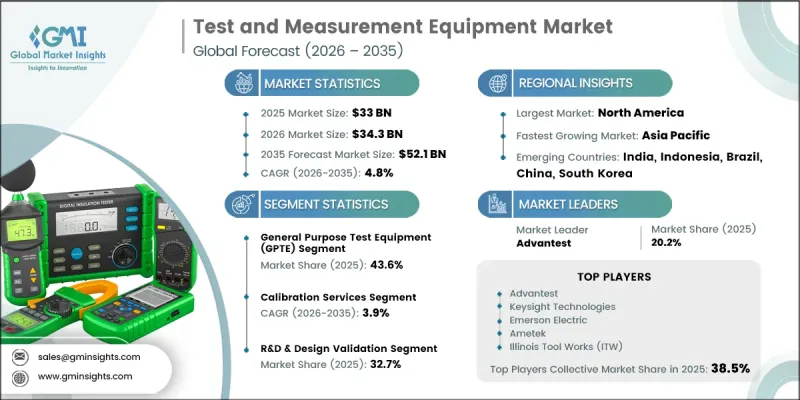

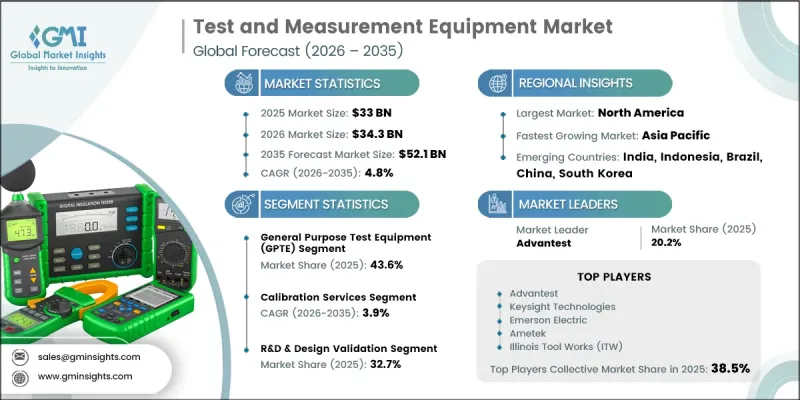

세계의 테스트 및 측정 장비 시장은 2025년에 330억 달러로 평가되었고, CAGR 4.8%로 성장하여 2035년까지 521억 달러에 달할 것으로 추정되고 있습니다.

시장 확대는 특히 첨단 전자 및 반도체 제조를 비롯한 여러 산업 분야에서 기술이 점점 더 복잡해짐에 따라 가속화되고 있습니다. 현대 기기가 점점 더 고도화되고 성능 요구 사항이 지속적으로 높아짐에 따라, 고정밀 시험, 검증 및 계측 솔루션에 대한 수요가 크게 증가하고 있습니다. 첨단 반도체 기술, 차세대 통신 네트워크, 지능형 자동차 시스템 및 산업용 자동화 플랫폼의 발전에 따라, 제품 개발 및 생산 공정 전반에 걸쳐 고정밀 측정 장비에 대한 수요가 증가하고 있습니다. 또한, 규제 요건과 품질 보증 기준 역시 주요 산업 전반에 걸쳐 테스트 및 측정 솔루션의 보다 광범위한 도입을 촉진하고 있습니다. 각 조직은 제품의 신뢰성, 운영상의 안전성, 그리고 끊임없이 진화하는 기술 기준을 준수하기 위해 첨단 장비에 대한 투자를 점점 더 늘리고 있습니다. 또한, 고속 디지털 기술, 첨단 무선 통신 시스템 및 복잡한 전자 아키텍처의 도입 확대가 혁신적인 테스트 기능에 대한 수요를 이끌고 있습니다. 각 업계가 성능 최적화, 제품 품질 및 시스템 검증을 지속적으로 우선시하는 가운데, 시험·측정 장비는 전 세계의 연구개발, 제조 및 유지보수 활동에서 점점 더 중요한 요소로 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 330억 달러 |

| 예측액 | 521억 달러 |

| CAGR | 4.8% |

범용 시험 장비(GPTE) 부문은 43.6%의 시장 점유율을 차지했으며, 2026년부터 2035년까지 연평균 성장률(CAGR) 2.8%로 성장할 것으로 전망됩니다. 이 부문에는 다양한 산업 분야에서 제품 개발, 엔지니어링 검증, 문제 해결 및 성능 평가에 사용되는 광범위한 장비가 포함됩니다. 시스템이 점점 더 복잡해짐에 따라 정확한 신호 분석, 전자 테스트 및 측정 기능에 대한 수요가 높아지고 있는 것이 지속적인 도입을 뒷받침하고 있습니다. 또한, 이 부문은 효율성과 시험 정밀도 향상을 목표로 소프트웨어 기반 기능, 모듈식 아키텍처, 그리고 지능형 측정 기술의 통합을 통해 진화하고 있습니다.

교정 서비스 부문은 2025년에 37%의 시장 점유율을 차지했습니다. 이 부문은 2035년까지 연평균 성장률(CAGR) 3.9%를 나타낼 것으로 예측됩니다. 교정 서비스는 측정 정밀도의 유지, 추적성의 확보, 그리고 업계 표준 준수를 지원하는 데 있어 매우 중요한 역할을 하고 있습니다. 다양한 산업 및 기술 중심의 응용 분야에서 시험 시스템이 점점 더 고도화되고 정밀도 요구 사항이 엄격해짐에 따라, 수요는 계속해서 증가하고 있습니다. 디지털 교정 프로세스, 자동 검증 시스템 및 원격 서비스 기능의 발전으로 인해 교정 서비스의 가치 제안은 더욱 높아졌으며, 이는 장기적인 시장 성장을 뒷받침하고 있습니다.

2025년, 중국의 테스트 및 측정 장비 시장은 56%의 점유율을 차지하며 57억 달러 시장 규모를 기록했습니다. 중국의 압도적인 위상은 광범위한 제조 생태계, 지속적으로 성장하는 반도체 산업, 그리고 첨단 디지털 인프라에 대한 지속적인 투자에 의해 뒷받침되고 있습니다. 시험 및 계측 솔루션에 대한 활발한 수요는 지속적인 기술 개발, 산업 현대화 노력, 그리고 다양한 분야에서 첨단 전자 시스템의 도입 확대에 힘입어 견인되고 있습니다. 이러한 요인들로 인해, 아시아태평양 전체 시장 성장에 있어 중국의 주요 기여자로서의 역할은 계속해서 강화되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품 유형별, 2022년-2035년

제6장 시장 추산 및 예측 : 서비스 유형별, 2022년-2035년

제7장 시장 추산 및 예측 : 용도별, 2022년-2035년

제8장 시장 추산 및 예측 : 최종 사용 산업별, 2022년-2035년

제9장 시장 추산 및 예측 : 지역별, 2022년-2035년

제10장 기업 개요

LSH 26.07.14The Global Test and Measurement Equipment Market was valued at USD 33 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 52.1 billion by 2035.

Market expansion is fueled by increasing technological complexity across multiple industries, particularly within advanced electronics and semiconductor manufacturing. As modern devices become more sophisticated and performance requirements continue to rise, the demand for highly accurate testing, validation, and measurement solutions is growing significantly. The evolution of advanced semiconductor technologies, next-generation communication networks, intelligent automotive systems, and industrial automation platforms is creating a greater need for precision instrumentation throughout product development and production processes. Regulatory requirements and quality assurance standards are also encouraging broader adoption of test and measurement solutions across critical industries. Organizations are increasingly investing in advanced equipment to ensure product reliability, operational safety, and compliance with evolving technical standards. Furthermore, growing adoption of high-speed digital technologies, advanced wireless communication systems, and complex electronic architectures is driving demand for innovative testing capabilities. As industries continue to prioritize performance optimization, product quality, and system validation, test and measurement equipment is becoming an increasingly important component of research, development, manufacturing, and maintenance activities worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $33 Billion |

| Forecast Value | $52.1 Billion |

| CAGR | 4.8% |

The general-purpose test equipment (GPTE) segment accounted for 43.6% share and is anticipated to grow at a CAGR of 2.8% from 2026 to 2035. This segment encompasses a broad range of instruments used for product development, engineering validation, troubleshooting, and performance evaluation across diverse industries. Growing system complexity and increasing demand for accurate signal analysis, electronic testing, and measurement capabilities are supporting continued adoption. The segment is also evolving through the integration of software-driven functionality, modular architectures, and intelligent measurement technologies designed to improve efficiency and testing accuracy.

The calibration services segment held a 37% share in 2025. The segment is expected to expand at a CAGR of 3.9% through 2035. Calibration services play a critical role in maintaining measurement accuracy, ensuring traceability, and supporting compliance with industry standards. Demand continues to rise as testing systems become increasingly sophisticated and precision requirements become more stringent across a variety of industrial and technology-focused applications. Advancements in digital calibration processes, automated verification systems, and remote service capabilities are further enhancing the value proposition of calibration services and supporting long-term market growth.

China Test and Measurement Equipment Market held a 56% share in 2025, generating USD 5.7 billion. The country's dominant position is supported by its extensive manufacturing ecosystem, expanding semiconductor industry, and ongoing investments in advanced digital infrastructure. Strong demand for testing and measurement solutions is being driven by continued technological development, industrial modernization efforts, and growing adoption of advanced electronic systems across multiple sectors. These factors continue to reinforce China's role as a major contributor to market growth throughout the Asia Pacific region.

Major companies operating in the global test and measurement equipment market include Advantest, Rohde & Schwarz, Keysight Technologies, Teledyne Technologies, Yokogawa Electric, Emerson Electric, Fortive, Anritsu, Illinois Tool Works (ITW), and Ametek. Companies operating in the test and measurement equipment market are implementing a variety of strategic initiatives to strengthen their competitive position and expand their global footprint. Research and development investments remain a key priority, enabling manufacturers to introduce advanced testing solutions that address increasingly complex technological requirements. Many organizations are enhancing their product portfolios through software integration, automation capabilities, and data analytics features that improve testing efficiency and measurement accuracy. Strategic acquisitions, partnerships, and collaborations are also helping companies expand market reach and accelerate innovation. Additionally, businesses are investing in cloud-enabled platforms, digital service offerings, and customer support infrastructure to improve user experiences and strengthen long-term customer relationships.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Service Type

- 2.2.4 Application

- 2.2.5 End-Use Industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerating 5G/6G Infrastructure Rollout Driving RF & Signal Test Demand

- 3.2.1.2 Rising EV & ADAS Adoption Creating New Powertrain & Radar Validation Requirements

- 3.2.1.3 Semiconductor Complexity Growth (Advanced Nodes, 3D ICs, Chiplets) Expanding ATE Addressable Market

- 3.2.1.4 Industry 4.0 & IIoT Adoption Increasing In-Line & Predictive Maintenance Testing Needs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Capital Expenditure & Extended Procurement Cycles for Advanced ATE & Modular Platforms

- 3.2.2.2 Shortage of Qualified T&M Application Engineers Limiting Equipment Utilization

- 3.2.3 Market opportunities

- 3.2.3.1 T&M-as-a-Service & Rental Models Unlocking Budget-Constrained End-Users

- 3.2.3.2 AI/ML Integration in Automated Test Workflows Reducing Test Time & False Failures

- 3.2.3.3 Expansion of Space, Satellite & Defense Electronics Creating Specialized Test Demand

- 3.2.3.4 Growing Medical Device & Wearable Diagnostics Market Expanding Healthcare T&M Segment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 National Institute of Standards and Technology (Measurement Standards & Traceability)

- 3.6.1.2 Federal Communications Commission Equipment Authorization & EMC Regulations

- 3.6.1.3 Occupational Safety and Health Administration Laboratory & Workplace Safety Standards

- 3.6.1.4 American National Standards Institute Testing & Measurement Standards

- 3.6.1.5 ISO/IEC 17025 Accreditation Requirements

- 3.6.2 Europe

- 3.6.2.1 European Committee for Electrotechnical Standardization EMC & Electrical Testing Standards

- 3.6.2.2 Electromagnetic Compatibility Directive

- 3.6.2.3 Low Voltage Directive

- 3.6.2.4 Radio Equipment Directive

- 3.6.2.5 ISO/IEC 17025 Accreditation Framework

- 3.6.3 Asia Pacific

- 3.6.3.1 State Administration for Market Regulation Measurement & Metrology Regulations

- 3.6.3.2 China National Accreditation Service for Conformity Assessment Laboratory Accreditation Standards

- 3.6.3.3 Japanese Industrial Standards Committee Testing & Measurement Standards

- 3.6.3.4 National Accreditation Board for Testing and Calibration Laboratories Accreditation Requirements

- 3.6.3.5 Bureau of Indian Standards Electronics Testing & Certification Standards

- 3.6.4 Latin America

- 3.6.4.1 National Institute of Metrology, Quality and Technology Metrology & Calibration Regulations

- 3.6.4.2 Directorate General of Standards Testing & Certification Standards

- 3.6.4.3 Inter-American Metrology System Regional Metrology Cooperation Framework

- 3.6.4.4 ISO/IEC 17025 Laboratory Accreditation Requirements

- 3.6.5 Middle East & Africa

- 3.6.5.1 Emirates Authority for Standardization and Metrology Testing & Calibration Standards

- 3.6.5.2 Saudi Standards, Metrology and Quality Organization Product Testing & Compliance Regulations

- 3.6.5.3 Gulf Standardization Organization Regional Testing & Certification Standards

- 3.6.5.4 African Organisation for Standardisation Regional Standardization Framework

- 3.6.5.5 ISO/IEC 17025 Laboratory Accreditation Framework

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI and Generative AI on the Market

- 3.12.1 AI Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.12.3 Risks Limitations and Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Bn, Units)

- 5.1 Key trends

- 5.2 General Purpose Test Equipment (GPTE)

- 5.3 Mechanical Test Equipment (MTE)

- 5.4 Environmental Test Equipment (ETE)

- 5.5 Automated Test Equipment (ATE)

Chapter 6 Market Estimates & Forecast, By Service Type, 2022 - 2035 (USD Bn, Units)

- 6.1 Key trends

- 6.2 Calibration Services

- 6.3 Repair & After-Sales Services

- 6.4 Asset Management & Leasing Services

- 6.5 Training & Technical Support Services

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Bn, Units)

- 7.1 Key trends

- 7.2 R&D & Design Validation

- 7.3 Manufacturing & Production Testing

- 7.4 Quality Assurance & Compliance Testing

- 7.5 Field Service & Maintenance Testing

- 7.6 Environmental & Safety Certification Testing

Chapter 8 Market Estimates & Forecast, By End-Use Industry, 2022 - 2035 (USD Bn, Units)

- 8.1 Key trends

- 8.2 Semiconductor & Electronics

- 8.3 Aerospace & Defense

- 8.4 Automotive & Transportation

- 8.5 IT & Telecommunications

- 8.6 Healthcare & Medical Devices

- 8.7 Industrial & Manufacturing

- 8.8 Energy & Utilities

- 8.9 Education & Government

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Qualcomm

- 10.1.2 Keysight Technologies

- 10.1.3 Rohde & Schwarz

- 10.1.4 Anritsu

- 10.1.5 Yokogawa Electric

- 10.1.6 Teradyne

- 10.1.7 Advantest

- 10.1.8 VIAVI Solutions

- 10.1.9 Fortive

- 10.1.10 Ametek

- 10.1.11 Teledyne Technologies

- 10.1.12 Emerson Electric

- 10.1.13 Spectris

- 10.1.14 Illinois Tool Works

- 10.1.15 Shimadzu

- 10.1.16 EXFO

- 10.2 Regional Players

- 10.2.1 ESPEC

- 10.2.2 ZwickRoell

- 10.2.3 Hioki E.E.

- 10.2.4 Good Will Instrument (GW Instek)

- 10.2.5 Chroma ATE