|

시장보고서

상품코드

2048955

탄소섬유 시장 : 원재료별, 계수별, 제품 유형별, 섬유 유형별, 용도별, 최종 이용 산업별, 지역별 - 세계 예측(-2031년)Carbon Fiber Market by Raw Material Type, By Fiber Type, By Modulus, By Product Type, By Application, By End-use Industry, By Region - Forecast to 2031 |

||||||

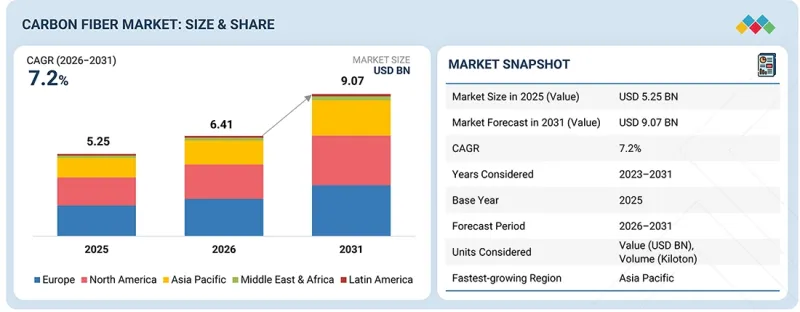

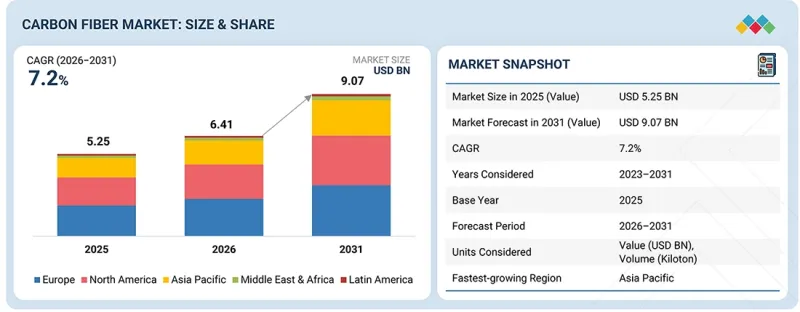

탄소섬유 시장 규모는 2026년에 64억 1,000만 달러로 추정되며, 2026년부터 2031년까지 CAGR 7.2%를 기록하며 2031년에는 90억 7,000만 달러에 달할 것으로 예측됩니다.

석유에서 추출한 피치를 원료로 하는 피치계 탄소섬유는 우수한 기계적 특성과 높은 열 안정성을 가지고 있습니다. 이 섬유는 5GPa 이상의 우수한 인장 강도를 가지고 있으며, 이는 강철에 필적하는 수준입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만 달러) 및 킬로톤 |

| 부문 | 원재료별, 계수별, 제품 유형별, 섬유 유형별, 용도별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

또한, 비강성이 알루미늄의 2배에 달해 경량화 용도에 적합합니다. 피치계 탄소섬유는 부식, 화학제품 및 극한의 온도에 대한 탁월한 내성을 보여 가혹한 환경에서도 사용할 수 있습니다. 높은 열전도율로 효율적인 방열이 가능하여 열에 민감한 용도에 적합합니다. 피치계 탄소섬유는 PAN계 섬유에 비해 피로 저항성이 향상되어 특정 용도에서 더 높은 정밀도로 제조할 수 있습니다.

"금액 기준으로 볼 때, 버진 탄소섬유가 전체 탄소섬유 시장에서 가장 큰 점유율을 차지했습니다."

버진 탄소섬유 부문은 고강도, 경량성, 강성, 내화학성 등 우수한 기계적 특성으로 인해 세계 탄소섬유 시장에서 가장 큰 점유율을 차지했습니다. 이러한 특성으로 인해 버진 탄소섬유는 항공우주 및 방위, 자동차, 풍력발전, 스포츠 용품, 압력 용기 등의 산업에서 가혹한 용도에 매우 적합합니다. 항공기, 자동차, 재생에너지 시스템 등 최종 사용 산업에서 연비 향상, 구조적 성능 강화 및 전반적인 배출량 감소를 위해 경량 소재에 대한 의존도가 높아지고 있습니다. 버진 탄소섬유는 안정적인 품질, 안정적인 성능 및 확립된 제조 공정으로 인해 여전히 널리 선호되고 있습니다. 이들은 중요하고 고성능의 구조적 응용 분야에서 필수적인 요소입니다. 재활용 탄소섬유가 비용 효율적이고 지속가능한 대안으로 떠오르고 있지만, 버진 탄소섬유는 우수한 구조적 무결성, 강화된 내구성, 첨단 복합재 응용 분야에서의 폭넓은 적용 가능성으로 인해 여전히 시장을 지배하고 있습니다.

"금액 기준으로 볼 때, 고탄성 탄소섬유는 전체 탄소섬유 시장에서 3번째로 높은 점유율을 차지했습니다."

고탄성 탄소섬유 부문은 고성능 응용 분야에서 우수한 강성과 치수 안정성으로 인해 세계 탄소섬유 시장에서 3번째로 높은 점유율을 차지했습니다. 고탄성 탄소섬유는 인장강도보다 강성과 변형 저항성이 더 중요한 용도에 맞게 특별히 설계되었습니다. 이 섬유는 일반적으로 탄소 함량이 98% 이상이며, 이는 뛰어난 강성, 열 안정성 및 구조적 성능에 기여합니다. 고탄성 탄소섬유의 주요 특징 중 하나는 일반적으로 370GPa 이상의 높은 탄성률로 표준 탄성률 탄소섬유보다 훨씬 더 높은 강성을 발휘합니다. 이러한 특성으로 인해 고탄성 탄소섬유는 경량 구조가 요구되는 항공우주 부품, 위성, 국방 시스템, 스포츠 용품 및 정밀 산업 장비에 널리 사용되고 있습니다.

"금액 기준으로 볼 때, 장섬유는 전체 탄소섬유 시장에서 3번째로 높은 점유율을 차지했습니다."

장섬유 탄소섬유 부문은 우수한 기계적 성능과 고성능 복합재료 응용 분야에서의 활용 확대에 힘입어 세계 탄소섬유 시장 점유율 3위를 차지했습니다. 일반적으로 길이가 1mm를 초과하는 장섬유 탄소섬유는 우수한 강도와 내구성이 요구되는 첨단 복합재료 구조의 보강재로 널리 사용되고 있습니다. 단섬유 탄소섬유에 비해 장섬유 탄소섬유는 높은 인장 강도, 우수한 강성, 우수한 내충격성 및 향상된 피로 성능을 제공하므로 지속적인 기계적 응력 및 가혹한 작동 조건에 노출되는 응용 분야에 적합합니다. 이러한 특성으로 인해 풍력발전, 항공우주 및 방위, 자동차, 모터스포츠 등의 산업에서 채택이 증가하고 있습니다. 장섬유 탄소 복합재료는 풍력 터빈 블레이드, 항공기 구조 부품, 고성능 자동차 부품, F1 머신 등 구조적 무결성과 장기적인 신뢰성을 갖춘 경량 소재가 필수적인 분야에서 널리 사용되고 있습니다.

"금액 기준으로 보면, 비복합재 부문이 탄소섬유 시장에서 두 번째 점유율을 차지했습니다."

비복합재 부문은 기존 복합재 구조를 넘어 단독 용도 및 특수 용도에서의 탄소섬유 활용 확대에 힘입어 세계 탄소섬유 시장 점유율 2위를 차지했습니다. 탄소섬유는 뛰어난 강도 대 중량비, 강성, 내식성 및 내피로성으로 널리 인정받고 있으며, 이러한 특성으로 인해 다양한 비복합재료 응용 분야에서 점점 더 많이 채택되고 있습니다. 탄소섬유는 구조적 용도 외에도 열전도율과 전기전도율이 우수하여 방열판, 전자기 간섭(EMI) 차폐, 반도체, 첨단 배터리, 연료전지 부품 등 전자 및 전기 응용 분야에 매우 적합합니다. 또한, 이 소재는 생체적합성, 경량성 및 방사선 투과성을 갖추고 있어 의료 및 헬스케어 분야에서도 큰 주목을 받고 있으며, 수술기구, 의족, 정형외과용 기기, 의료용 영상 진단 장치 등에 이상적입니다. 기술 발전과 전자, 의료, 산업 분야에서 고성능 소재에 대한 수요 증가로 비복합재용 탄소섬유 부문의 성장이 지속되고 있습니다.

"예측 기간 동안 압력 용기 산업은 가장 빠르게 성장하는 최종 이용 산업이 될 것으로 예상됩니다."

압력 용기 산업은 수소, 압축천연가스(CNG), 항공우주 및 산업용 경량 및 고압 저장 솔루션에 대한 수요 증가에 힘입어 예측 기간 동안 세계 탄소섬유 시장에서 가장 빠른 성장을 기록할 것으로 예상됩니다. 탄소섬유는 필라멘트 와인딩에 의한 압력 용기 제조에 널리 사용되며, 이 방법은 고강도 토우를 라이너와 맨드릴에 감아 내구성과 기밀성이 높은 구조물을 형성합니다. 탄소섬유 강화 압력 용기는 우수한 강도, 내식성, 내압 성능을 유지하면서 대폭적인 경량화를 실현합니다. 일반적으로 기존 강철이나 알루미늄 용기에 비해 최대 75%까지 가볍습니다. 이러한 장점으로 인해 경량화와 운영 효율성이 매우 중요한 수소 저장 탱크, CNG 실린더, 항공우주 시스템 및 운송 응용 분야에 매우 적합합니다. 또한, 탄소섬유 압력 용기는 우수한 피로 저항성, 내구성 및 긴 수명을 가지고 있어 차세대 청정에너지 및 모빌리티 솔루션에 대한 채택이 확대되고 있습니다. 수소 인프라, 연료전지차, 대체 연료 저장 기술에 대한 투자 확대로 인해 전 세계적으로 탄소섬유 압력 용기에 대한 수요가 더욱 가속화될 것으로 예상됩니다.

"예측 기간 동안 아시아태평양은 탄소섬유 시장에서 가장 높은 성장률을 기록할 것으로 예상됩니다."

아시아태평양은 급속한 산업화, 자동차, 항공우주, 제조 산업에서 경량 소재에 대한 수요 증가, 기술 혁신에 대한 강한 집중에 힘입어 예측 기간 동안 탄소섬유 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다. 특히 일본, 중국, 한국 등의 국가들은 첨단 제조기술과 항공우주, 자동차, 인프라 용도의 탄소섬유 복합재 개발 등 탄소섬유 시장에 많은 투자를 하고 있습니다. 이들 국가는 최첨단 기술과 혁신으로 유명하며, 도레이와 미쓰비시 화학 그룹과 같은 주요 기업들이 고성능 용도의 탄소섬유 생산 발전을 주도하고 있습니다.

본 보고서에서는 다음과 같은 기업에 대한 종합적인 분석을 제공합니다:

이 시장의 주요 기업으로는 Toray Industries, Inc.(일본), DowAksa(터키), Mitsubishi Chemical Group Corporation(일본), Syensqo(벨기에), Teijin Limited(일본), SGL Carbon(독일), Hexcel Corporation(미국), HS Hyosung Advanced Materials(한국), Zhongfu Shenying Carbon Fiber(중국), Kureha Corporation(일본), Osaka Gas Chemicals(일본), UMATEX(러시아), Jilin Chemical Fiber Group(중국), Jiangsu Hengshen(중국), China National Bluestar (Group) Co., Ltd.(중국) 등이 있습니다.

조사 범위

본 보고서는 탄소섬유 시장을 원료 유형(팬 및 피치), 섬유 유형(버진 및 재활용), 탄성률(표준, 중간, 고탄성), 제품 유형(연속, 장섬유, 단섬유), 용도(복합재 및 비복합재), 최종 이용 산업(항공우주 및 방위, 자동차, 풍력에너지, 파이프, 압력 용기, 스포츠용품, 건설, 인프라, 의료, 헬스케어, 선박), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)으로 분류하고 있습니다. 이 보고서의 연구 범위에는 촉진요인, 제약요인, 과제 및 기회와 같은 탄소섬유 시장의 성장에 영향을 미치는 주요 요인에 대한 자세한 정보가 포함되어 있습니다. 이 보고서는 주요 산업 플레이어에 대한 철저한 조사를 통해 사업 개요, 솔루션 및 서비스, 주요 전략, 탄소섬유 시장의 최근 동향에 대한 인사이트를 제공합니다. 이 보고서에는 탄소섬유 시장 생태계의 신흥 스타트업 기업들에 대한 경쟁 분석도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 전체 탄소섬유 시장과 그 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한, 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 도전 과제 및 기회에 대한 정보를 제공하는 데 도움이 될 것입니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(위성 부품 제조 확대, 항공우주 및 방위 산업 수요 증가, 엄격한 환경 규제에 따른 자동차 응용 분야에서의 채택 확대, 풍력발전 산업에서의 사용 증가, 압력 용기용 일반 탄소 수요 증가), 제약요인(높은 생산 비용, 제조 기술 표준화 부족, 손상 복구 및 호환성 문제), 기회(저비용 석탄계 탄소섬유 개발에 대한 투자 확대, 신규 용도의 잠재적 기회, 연료전지 전기자동차(FCEV) 수요 증가, 3D 프린팅 활용 확대, 탄소섬유 재활용 기술 발전), 도전과제(저비용 탄소섬유 생산, 자본 집약적인 생산 및 복잡한 제조 공정, 재활용성 문제)에 대해 탄소섬유 시장 성장에 영향을 미치는 요인을 분석하고 있습니다.

- 제품 개발 및 혁신 : 탄소섬유 시장의 미래 기술, R&D 활동 및 서비스 출시에 대한 심층적인 인사이트.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보. 본 보고서에서는 다양한 지역의 탄소섬유 시장을 분석합니다.

- 시장 다각화 : 탄소섬유 시장의 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보.

- 경쟁사 평가 : Toray Industries, Inc.(일본), DowAksa(튀르키예), Mitsubishi Chemical Group Corporation(일본), Syensqo(벨기에), Teijin Limited(일본), SGL Carbon(독일), Hexcel Corporation(미국), HS Hyosung Advanced Materials(한국), Zhongfu Shenying Carbon Fiber(중국), Kureha Corporation(일본), Osaka Gas Chemicals(일본), UMATEX(러시아), Jilin Chemical Fiber Group(중국), Jiangsu Hengshen(중국), China National Bluestar (Group) Co., Ltd.(중국) 등 주요 기업들의 시장 점유율, 성장전략, 서비스 제공내용에 대한 상세한 평가가 이루어집니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 탄소섬유 시장(원료별)

제10장 탄소섬유 시장(계수별)

제11장 탄소섬유 시장(제품 유형별)

제12장 탄소섬유 시장(섬유 유형별)

제13장 탄소섬유 시장(용도별)

제14장 탄소섬유 시장(최종 이용 산업별)

제15장 탄소섬유 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.06.08The carbon fiber market is estimated at USD 6.41 billion in 2026 and is projected to reach USD 9.07 billion by 2031, at a CAGR of 7.2% from 2026 to 2031. Pitch-based carbon fibers, derived from petroleum-based pitch, offer superior mechanical properties and high thermal stability. They possess excellent tensile strength, exceeding 5 GPa, which is comparable to steel.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD million) and volume (kiloton) |

| Segments | Raw material type, fiber type, modulus, product type, application, end-use industry, and region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and Latin America |

Moreover, their specific stiffness is twice that of aluminum, making them ideal for lightweight applications. Pitch carbon fibers exhibit exceptional resistance to corrosion, chemicals, and extreme temperatures, enabling their utilization in demanding environments. Their high thermal conductivity ensures efficient heat dissipation, making them suitable for heat-sensitive applications. Pitch-based carbon fiber offers enhanced fatigue resistance and can be manufactured with greater precision in certain applications compared to PAN-based fibers.

''In terms of value, virgin carbon fiber accounted for the largest share of the overall carbon fiber market.''

The virgin carbon fiber segment accounted for the largest share of the global carbon fiber market owing to its superior mechanical properties, including high strength, lightweight characteristics, stiffness, and excellent chemical resistance. These properties make virgin carbon fiber highly suitable for demanding applications across industries such as aerospace & defense, automotive, wind energy, sporting goods, and pressure vessels. End-use industries increasingly rely on lightweight materials to improve fuel efficiency, enhance structural performance, and reduce overall emissions in aircraft, vehicles, and renewable energy systems. Virgin carbon fiber remains widely preferred for its consistent quality, reliable performance, and well-established manufacturing processes, which are essential for critical and high-performance structural applications. Although recycled carbon fiber is gaining momentum as a cost-effective and sustainable alternative, virgin carbon fiber continues to dominate the market because of its superior structural integrity, enhanced durability, and broader applicability across advanced composite applications.

''In terms of value, high modulus accounted for the third-largest share of the overall carbon fiber market.''

The high-modulus carbon fiber segment accounted for the third-largest share of the global carbon fiber market, owing to its superior stiffness and dimensional stability in high-performance applications. High modulus carbon fiber is specifically engineered for applications where rigidity and resistance to deformation are more critical than tensile strength. These fibers typically possess a carbon content exceeding 98%, which contributes to their exceptional stiffness, thermal stability, and structural performance. One of the key characteristics of high-modulus carbon fiber is its high modulus of elasticity, generally above 370 GPa, making it considerably stiffer than standard-modulus carbon fiber. Owing to these properties, high-modulus carbon fibers are extensively used in aerospace components, satellites, defense systems, sporting goods, and precision industrial equipment, where lightweight structures with minimal flex and high accuracy are required.

''In terms of value, long fiber accounted for the third-largest share of the overall carbon fiber market.''

The long carbon fiber segment held the third-largest share of the global carbon fiber market, driven by its enhanced mechanical performance and growing use in high-performance composite applications. Long carbon fibers, typically measuring more than 1 mm in length, are widely used as reinforcement in advanced composite structures that require superior strength and durability. Compared to short carbon fibers, long carbon fibers provide higher tensile strength, improved stiffness, better impact resistance, and enhanced fatigue performance, making them suitable for applications exposed to continuous mechanical stress and demanding operating conditions. These characteristics have increased their adoption across industries such as wind energy, aerospace & defense, automotive, and motorsports. Long carbon fiber composites are extensively utilized in wind turbine blades, aircraft structural components, high-performance automotive parts, and Formula 1 vehicles, where lightweight materials with superior structural integrity and long-term reliability are critical.

''In terms of value, the non-composites segment accounted for the second-largest share of the carbon fiber market.''

The non-composites segment accounted for the second-largest share of the global carbon fiber market, driven by the expanding use of carbon fiber in standalone and specialty applications beyond traditional composite structures. Carbon fiber is widely recognized for its exceptional strength-to-weight ratio, stiffness, corrosion resistance, and fatigue resistance, and these properties are increasingly driving its adoption in various non-composite applications. In addition to structural uses, carbon fiber demonstrates excellent thermal and electrical conductivity, making it highly suitable for electronic and electrical applications such as heat sinks, electromagnetic interference (EMI) shielding, semiconductors, advanced batteries, and fuel cell components. The material is also gaining significant traction in the medical and healthcare sectors owing to its biocompatibility, lightweight nature, and radiolucency, which make it ideal for surgical instruments, prosthetics, orthopedic devices, and medical imaging equipment. Growing technological advancements and the increasing need for high-performance materials across electronics, healthcare, and industrial applications continue to support the growth of the non-composites carbon fiber segment.

"The pressure vessels industry is projected to be the fastest-growing end-use industry during the forecast period."

The pressure vessels industry is projected to register the fastest growth in the global carbon fiber market during the forecast period, driven by rising demand for lightweight, high-pressure storage solutions across hydrogen, compressed natural gas (CNG), aerospace, and industrial applications. Carbon fiber is widely used in pressure vessel manufacturing via filament winding, where high-strength tows are wound over a liner or mandrel to create durable, gas-tight structures. Carbon fiber-reinforced pressure vessels offer significant weight reduction, typically being up to 75% lighter than conventional steel or aluminum vessels, while maintaining superior strength, corrosion resistance, and pressure-handling capability. These advantages make them highly suitable for hydrogen storage tanks, CNG cylinders, aerospace systems, and transportation applications where weight reduction and operational efficiency are critical. In addition, carbon fiber pressure vessels provide excellent fatigue resistance, durability, and long service life, supporting their increasing adoption in next-generation clean energy and mobility solutions. Growing investments in hydrogen infrastructure, fuel cell vehicles, and alternative fuel storage technologies are expected to further accelerate demand for carbon fiber-based pressure vessels globally.

"The Asia Pacific region is projected to register the highest growth rate in the carbon fiber market during the forecast period."

The Asia Pacific is projected to be the fastest-growing region in the carbon fiber market during the forecast period, driven by rapid industrialization, rising demand for lightweight materials across the automotive, aerospace, and manufacturing industries, and a strong focus on technological advancements. In particular, countries like Japan, China, and South Korea are investing substantially in the carbon fiber market, including advanced manufacturing technologies and the development of carbon fiber composites for aerospace, automotive, and infrastructure applications. These countries are known for their cutting-edge technology and innovation, with major companies such as Toray Industries, Inc. and Mitsubishi Chemical Group Corporation driving advancements in carbon fiber production for high-performance applications.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 40%, Tier 2 - 33%, and Tier 3 - 27%

- By Designation: C-level - 50%, Director-level - 30%, and Managers - 20%

- By Region: North America - 15%, Europe - 50%, Asia Pacific - 20%, the Middle East & Africa - 10%, and Latin America - 5%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market include Toray Industries, Inc. (Japan), DowAksa (Turkey), Mitsubishi Chemical Group Corporation (Japan), Syensqo (Belgium), Teijin Limited (Japan), SGL Carbon (Germany), Hexcel Corporation (US), HS Hyosung Advanced Materials (South Korea), Zhongfu Shenying Carbon Fiber Co., Ltd. (China), Kureha Corporation (Japan), Osaka Gas Chemicals Co., Ltd., (Japan), UMATEX (Russia), Jilin Chemical Fiber Group Co., Ltd. (China), Jiangsu Hengshen Co., Ltd. (China), and China National Bluestar (Group) Co., Ltd. (China).

Research coverage

This research report categorizes the carbon fiber market by raw material type (pan and pitch), fiber type (virgin and recycled), modulus (standard, intermediate, and high), product type (continuous, long, and short), application (composites and non-composites), end-use industry (aerospace & defense, automotive, wind energy, pipe, pressure vessels, sporting goods, construction & infrastructure, medical & healthcare, and marine), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America). The scope of the report includes detailed information on the major factors influencing the growth of the carbon fiber market, including drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted in order to provide insights into their business overview, solutions and services, key strategies, and recent developments in the carbon fiber market. This report includes a competitive analysis of upcoming startups in the carbon fiber market ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market with information on the closest approximations of revenue for the overall carbon fiber market and its subsegments. This report will help stakeholders understand the competitive landscape and gain insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (growth in manufacturing of satellite parts, high demand from aerospace & defense industry, rising adoption in automobile applications due to stringent eco-friendly regulations, increased use in wind energy industry, and rising demand for regular tow carbon in pressure vessels), restraints (high production cost, lack of standardization in manufacturing technologies, and damage repair and compatibility issues), opportunities (increased investments in the development of low-cost coal-based carbon fibers, potential opportunities in new applications, increasing demand for fuel cell electric vehicles (FCEVs), increasing use in 3D printing, advancements in carbon fiber recycling technologies), and challenges (production of low-cost carbon fiber, capital-intensive production and complex manufacturing processes, and recyclability issues) influencing the growth of the carbon fiber market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the carbon fiber market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the carbon fiber market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the carbon fiber market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Toray Industries, Inc. (Japan), DowAksa (Turkey), Mitsubishi Chemical Group Corporation (Japan), Syensqo (Belgium), Teijin Limited (Japan), SGL Carbon (Germany), Hexcel Corporation (US), HS Hyosung Advanced Materials (South Korea), Zhongfu Shenying Carbon Fiber Co., Ltd. (China), Kureha Corporation (Japan), Osaka Gas Chemicals Co., Ltd., (Japan), UMATEX (Russia), Jilin Chemical Fiber Group Co., Ltd. (China), Jiangsu Hengshen Co., Ltd. (China), and China National Bluestar (Group) Co., Ltd. (China) in the carbon fiber market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CARBON FIBER MARKET

- 3.2 CARBON FIBER MARKET, BY END-USE INDUSTRY AND REGION

- 3.3 CARBON FIBER MARKET, BY RAW MATERIAL

- 3.4 CARBON FIBER MARKET, BY APPLICATION

- 3.5 CARBON FIBER MARKET, BY MODULUS

- 3.6 CARBON FIBER MARKET, BY FIBER TYPE

- 3.7 CARBON FIBER MARKET, BY PRODUCT TYPE

- 3.8 CARBON FIBER MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing demand for lightweight and fuel-efficient vehicles

- 4.2.1.2 Growth in manufacturing of satellite parts

- 4.2.1.3 High usage in aerospace & defense industry

- 4.2.1.4 Increased use in wind energy industry

- 4.2.2 RESTRAINTS

- 4.2.2.1 High material and production cost

- 4.2.2.2 Lack of standardization in manufacturing technologies

- 4.2.2.3 Damage repair and compatibility issues

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increased investments in development of low-cost coal-based carbon fibers

- 4.2.3.2 Increasing use in 3D printing

- 4.2.3.3 Growing demand for recyclable and sustainable composite materials

- 4.2.3.4 Increasing demand for fuel-cell electric vehicles (FCEVs)

- 4.2.4 CHALLENGES

- 4.2.4.1 Supply chain concentration and precursor dependency

- 4.2.4.2 Certification and qualification barriers in high-performance applications

- 4.2.4.3 Demand volatility driven by policy-dependent end-use industries

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CARBON FIBER MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN AUTOMOTIVE INDUSTRY

- 5.2.4 TRENDS IN AEROSPACE & DEFENSE

- 5.2.5 TRENDS IN WIND ENERGY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY

- 5.5.2 AVERAGE SELLING PRICE TREND OF CARBON FIBER, BY REGION

- 5.6 TRADE ANALYSIS, 2021-2025

- 5.6.1 IMPORT SCENARIO (HS CODE 681511)

- 5.6.2 EXPORT SCENARIO (HS CODE 681511)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2028

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 MITSUBISHI'S DEVELOPMENT OF CARBON FIBER-REINFORCED PLASTICS FOR STRUCTURAL AIRCRAFT PARTS

- 5.10.2 SGL CARBON'S CLIMATE-FRIENDLY CARBON FIBER TO REVOLUTIONIZE SUSTAINABLE MANUFACTURING

- 5.10.3 TRUE TEMPER SPORTS PARTNERS WITH HEXCEL CORPORATION FOR ITS FIRST GOLF SHAFT LINE

- 5.11 IMPACT OF 2025 US TARIFF ON CARBON FIBER MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.4.4 Middle East & Africa

- 5.11.5 IMPACT ON TOP END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 LOW-COST CARBON FIBER (LCCF) VIA ALTERNATIVE PRECURSORS (LIGNIN/BIO-BASED/PAN-BLENDS)

- 6.1.2 PLASMA OXIDATION & MICROWAVE-ASSISTED CARBONIZATION (RAPID PROCESSING CF TECHNOLOGY)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CARBON FIBER RECYCLING (RCF) & CLOSED-LOOP MANUFACTURING

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2028) | FOUNDATION & INCREMENTAL COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2031) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2032-2036+) | DISRUPTION & MASS ADOPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPES

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 TOP 10 PATENT OWNERS (US) IN LAST 5 YEARS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 STRUCTURAL EV BATTERY INTEGRATION (CELL-TO-PACK/ STRUCTURAL COMPOSITES)

- 6.5.2 HYBRID MULTI-MATERIAL VEHICLE ARCHITECTURES

- 6.5.3 ADVANCED STRUCTURAL & INFRASTRUCTURE SYSTEMS

- 6.5.4 HIGH-PERFORMANCE DATA CENTERS & ELECTRONICS

- 6.5.5 NEXT-GENERATION MOBILITY (UAVS, EVTOLS, SPACE SYSTEMS)

- 6.6 IMPACT OF AI/GEN AI ON CARBON FIBER MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN CARBON FIBER MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN CARBON FIBER MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN CARBON FIBER MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 TORAY INDUSTRIES: HIGH-PERFORMANCE AEROSPACE AND SPORTS APPLICATIONS

- 6.7.2 HEXCEL CORPORATION: ADVANCED COMPOSITE STRUCTURES FOR AEROSPACE

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF CARBON FIBER

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF CARBON FIBER

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY APPLICATION

9 CARBON FIBER MARKET, BY RAW MATERIAL

- 9.1 INTRODUCTION

- 9.2 PAN-BASED CARBON FIBER

- 9.2.1 EXTENSIVE DEMAND FOR LIGHTWEIGHT STRUCTURAL COMPOSITES TO DRIVE MARKET

- 9.3 PITCH-BASED CARBON FIBER

- 9.3.1 WIDE USAGE IN SATELLITES, INDUSTRIAL, CONSTRUCTION, AND SPORTING GOODS SEGMENTS TO DRIVE MARKET

- 9.3.2 PETROLEUM-BASED PITCH CARBON FIBER

- 9.3.3 COAL-BASED PITCH CARBON FIBER

10 CARBON FIBER MARKET, BY MODULUS

- 10.1 INTRODUCTION

- 10.2 STANDARD MODULUS

- 10.2.1 USAGE ACROSS INDUSTRIES TO DRIVE MARKET

- 10.3 INTERMEDIATE MODULUS

- 10.3.1 DEMAND IN PRESSURE VESSELS, WIND TURBINE BLADES, AND AEROSPACE TO DRIVE MARKET

- 10.4 HIGH MODULUS

- 10.4.1 DEMAND FOR AEROSPACE APPLICATIONS TO DRIVE MARKET

11 CARBON FIBER MARKET, BY PRODUCT TYPE

- 11.1 INTRODUCTION

- 11.2 CONTINUOUS CARBON FIBER

- 11.2.1 RISING DEMAND FOR LIGHTWEIGHT HIGH-STRENGTH COMPOSITES TO DRIVE MARKET

- 11.3 LONG CARBON FIBER

- 11.3.1 INCREASING DEMAND FOR DURABLE LIGHTWEIGHT COMPOSITES TO DRIVE MARKET

- 11.4 SHORT CARBON FIBER

- 11.4.1 COST-EFFECTIVE LIGHTWEIGHT MATERIALS TO DRIVE MARKET

12 CARBON FIBER MARKET, BY FIBER TYPE

- 12.1 INTRODUCTION

- 12.2 VIRGIN CARBON FIBER

- 12.2.1 LONG-TERM HIGH PERFORMANCE IN TERMS OF FATIGUE AND ENVIRONMENTAL EFFECTS TO DRIVE MARKET

- 12.3 RECYCLED CARBON FIBER

- 12.3.1 GROWING ENVIRONMENTAL CONCERNS TO DRIVE MARKET

13 CARBON FIBER MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 COMPOSITES

- 13.2.1 RIGIDITY AND HIGH TENSILE STRENGTH TO FUEL DEMAND

- 13.2.2 PREPREGS

- 13.2.3 MOLDING COMPOUNDS

- 13.2.4 WOVEN FABRICS

- 13.3 NON-COMPOSITES

- 13.3.1 RISING DEMAND FOR EVS AND 3D PRINTING TO DRIVE MARKET

14 CARBON FIBER MARKET, BY END-USE INDUSTRY

- 14.1 INTRODUCTION

- 14.2 AEROSPACE & DEFENSE

- 14.2.1 MAJOR CONSUMER OF CARBON FIBER COMPOSITE MATERIALS

- 14.2.2 ROCKETS, SPACE VEHICLES, HABITATION EQUIPMENT

- 14.2.3 UMA (URBAN AIR MOBILITY) AND SMALL AIRCRAFT EQUIPMENT

- 14.3 WIND ENERGY

- 14.3.1 STEADY INCREASE IN GLOBAL WIND ENERGY INSTALLATION

- 14.4 AUTOMOTIVE

- 14.4.1 INCREASING ADOPTION OF CARBON FIBERS BY AUTOMOTIVE GIANTS TO DRIVE MARKET

- 14.4.2 INTERIOR COMPONENTS

- 14.4.3 EXTERIOR COMPONENTS

- 14.4.4 SMALL MOBILITY APPLICATION

- 14.5 PIPES

- 14.5.1 UNIQUE BLEND OF PROPERTIES TO DRIVE MARKET

- 14.6 SPORTING GOODS

- 14.6.1 INTEREST IN HIGHER PERFORMANCE AND SUSTAINABILITY TO DRIVE NEW CFRP MATERIALS IN SPORTING GOODS

- 14.7 MEDICAL & HEALTHCARE

- 14.7.1 SUSTENANCE UNDER EXTREME ENVIRONMENTAL CONDITIONS TO DRIVE MARKET

- 14.7.2 DIAGNOSTICS IMAGING

- 14.7.3 BODY IMPLANT, SURGICAL INSTRUMENTS, AND OTHERS

- 14.8 CONSTRUCTION & INFRASTRUCTURE

- 14.8.1 GROWTH IN CONSTRUCTION & INFRASTRUCTURE SEGMENT TO BOOST DEMAND

- 14.8.2 BUILDING INFRASTRUCTURE

- 14.8.3 CIVIL INFRASTRUCTURE

- 14.9 PRESSURE VESSELS

- 14.9.1 INCREASE IN DEMAND FOR TYPE IV CYLINDERS TO DRIVE MARKET

- 14.10 MARINE

- 14.10.1 GROWING MARINE APPLICATIONS TO DRIVE MARKET

- 14.11 OTHER END-USE INDUSTRIES

- 14.11.1 ELECTRICAL & ELECTRONICS

- 14.11.2 CABLES

- 14.11.3 MOLDING COMPOUNDS

15 CARBON FIBER MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 EUROPE

- 15.2.1 EUROPE: CARBON FIBER MARKET, BY END-USE INDUSTRY

- 15.2.2 EUROPE: CARBON FIBER MARKET, BY COUNTRY

- 15.2.2.1 Germany

- 15.2.2.1.1 Strong automotive, aerospace, and renewable energy demand to drive market

- 15.2.2.2 France

- 15.2.2.2.1 Strong aerospace, EV, and renewable energy industries to drive market

- 15.2.2.3 UK

- 15.2.2.3.1 Growing demand for lightweight materials and offshore wind energy to drive market

- 15.2.2.4 Italy

- 15.2.2.4.1 Growing demand from automotive, wind energy, and advanced composites to drive market

- 15.2.2.5 Spain

- 15.2.2.5.1 Strong wind energy and aerospace demand to drive market

- 15.2.2.6 Rest of Europe

- 15.2.2.1 Germany

- 15.3 NORTH AMERICA

- 15.3.1 NORTH AMERICA: CARBON FIBER MARKET, BY END-USE INDUSTRY

- 15.3.2 NORTH AMERICA: CARBON FIBER MARKET, BY COUNTRY

- 15.3.2.1 US

- 15.3.2.1.1 Presence of well-established industries to drive market

- 15.3.2.2 Canada

- 15.3.2.2.1 Presence of well-established aerospace industry to fuel demand

- 15.3.2.1 US

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: CARBON FIBER MARKET, BY END-USE INDUSTRY

- 15.4.2 ASIA PACIFIC: CARBON FIBER MARKET, BY COUNTRY

- 15.4.2.1 Japan

- 15.4.2.1.1 Strong carbon fiber exports and advanced manufacturing to drive market

- 15.4.2.2 China

- 15.4.2.2.1 Strong EV, wind energy, and aerospace demand to drive market

- 15.4.2.3 Taiwan

- 15.4.2.3.1 Strong bicycle and advanced composites industries to drive market

- 15.4.2.4 South Korea

- 15.4.2.4.1 Strong automotive, hydrogen, and shipbuilding industries to drive market

- 15.4.2.5 Rest of Asia Pacific

- 15.4.2.1 Japan

- 15.5 MIDDLE EAST & AFRICA

- 15.5.1 MIDDLE EAST & AFRICA: CARBON FIBER MARKET, BY END-USE INDUSTRY

- 15.5.2 MIDDLE EAST & AFRICA: CARBON FIBER MARKET, BY COUNTRY

- 15.5.2.1 GCC Countries

- 15.5.2.1.1 UAE

- 15.5.2.1.1.1 Regional hub for advanced composites and lightweight mobility

- 15.5.2.1.2 Saudi Arabia

- 15.5.2.1.2.1 High demand in pipes & pressure vessels industry

- 15.5.2.1.3 Rest of GCC Countries

- 15.5.2.1.1 UAE

- 15.5.2.2 South Africa

- 15.5.2.2.1 Strengthens position in wind energy and advanced composites

- 15.5.2.3 Rest of Middle East & Africa

- 15.5.2.1 GCC Countries

- 15.6 LATIN AMERICA

- 15.6.1 LATIN AMERICA: CARBON FIBER MARKET, BY END-USE INDUSTRY

- 15.6.2 LATIN AMERICA: CARBON FIBER MARKET, BY COUNTRY

- 15.6.2.1 Brazil

- 15.6.2.1.1 Key hub for aerospace, wind energy, and automotive composites

- 15.6.2.2 Mexico

- 15.6.2.2.1 Automotive and wind energy industries to be prominent consumers of carbon fiber

- 15.6.2.3 Rest of Latin America

- 15.6.2.1 Brazil

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.3 REVENUE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS

- 16.5 BRAND COMPARISON

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.6.5.1 Company footprint

- 16.6.5.2 Region footprint

- 16.6.5.3 Raw material type footprint

- 16.6.5.4 Fiber type footprint

- 16.6.5.5 Modulus type footprint

- 16.6.5.6 Product type footprint

- 16.6.5.7 Application footprint

- 16.6.5.8 End-use industry footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.8 COMPANY VALUATION AND FINANCIAL METRICS

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY COMPANIES

- 17.1.1 TORAY INDUSTRIES, INC.

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Expansions

- 17.1.1.3.4 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 DOWAKSA

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Deals

- 17.1.2.3.2 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 MITSUBISHI CHEMICAL GROUP CORPORATION

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Deals

- 17.1.3.3.2 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 SYENSQO

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 TEIJIN LIMITED

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Expansions

- 17.1.5.3.4 Other developments

- 17.1.5.4 MnM view

- 17.1.5.4.1 Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 SGL CARBON

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.6.3.2 Expansions

- 17.1.6.4 MnM view

- 17.1.6.4.1 Right to win

- 17.1.6.4.2 Strategic choices

- 17.1.6.4.3 Weaknesses and competitive threats

- 17.1.7 HEXCEL CORPORATION

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Expansions

- 17.1.7.4 MnM view

- 17.1.7.4.1 Right to win

- 17.1.7.4.2 Strategic choices

- 17.1.7.4.3 Weaknesses and competitive threats

- 17.1.8 HS HYOSUNG ADVANCED MATERIALS

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.8.3.2 Deals

- 17.1.8.3.3 Expansions

- 17.1.8.4 MnM view

- 17.1.8.4.1 Right to win

- 17.1.8.4.2 Strategic choices

- 17.1.8.4.3 Weaknesses and competitive threats

- 17.1.9 ZHONGFU SHENYING CARBON FIBER CO., LTD.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Expansions

- 17.1.9.4 MnM view

- 17.1.9.4.1 Right to win

- 17.1.9.4.2 Strategic choices

- 17.1.9.4.3 Weaknesses and competitive threats

- 17.1.10 UMATEX

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 MnM view

- 17.1.10.3.1 Right to win

- 17.1.10.3.2 Strategic choices

- 17.1.10.3.3 Weaknesses and competitive threats

- 17.1.11 KUREHA CORPORATION

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 MnM view

- 17.1.11.3.1 Key strengths

- 17.1.11.3.2 Strategic choices

- 17.1.11.3.3 Weaknesses and competitive threats

- 17.1.12 OSAKA GAS CHEMICALS CO., LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 MnM view

- 17.1.12.3.1 Key strengths

- 17.1.12.3.2 Strategic choices

- 17.1.12.3.3 Weaknesses & competitive threats

- 17.1.13 JILIN CHEMICAL FIBER GROUP CO., LTD.

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.13.3.2 Expansions

- 17.1.13.4 MnM view

- 17.1.13.4.1 Key strengths

- 17.1.13.4.2 Strategic choices

- 17.1.13.4.3 Weaknesses & competitive threats

- 17.1.14 JIANGSU HENGSHEN CO., LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Expansions

- 17.1.14.4 MnM view

- 17.1.14.4.1 Key strengths

- 17.1.14.4.2 Strategic choices

- 17.1.14.4.3 Weaknesses & competitive threats

- 17.1.15 CHINA NATIONAL BLUESTAR (GROUP) CO., LTD.

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 MnM view

- 17.1.15.3.1 Key strengths

- 17.1.15.3.2 Strategic choices

- 17.1.15.3.3 Weaknesses & competitive threats

- 17.1.1 TORAY INDUSTRIES, INC.

- 17.2 OTHER PLAYERS

- 17.2.1 CHINA WEIHAI GUANGWEI COMPOSITES CO., LTD.

- 17.2.2 CHANGSHENG (LANGFANG) TECHNOLOGY CO., LTD.

- 17.2.3 JILIN JIYAN HIGH-TECH FIBER CO., LTD.

- 17.2.4 JILIN SHENZHOU CARBON FIBER CO., LTD.

- 17.2.5 ALFA CHEMISTRY

- 17.2.6 BCIRCULAR

- 17.2.7 VARTEGA INC.

- 17.2.8 FLINK INTERNATIONAL CO., LTD.

- 17.2.9 CHINA COMPOSITES GROUP CORPORATION LTD.

- 17.2.10 FORMOSA PLASTICS CORPORATION

- 17.2.11 NIPPON GRAPHITE FIBER CO., LTD.

- 17.2.12 NEWTECH GROUP CO., LTD.

- 17.2.13 ACE C&TECH CO., LTD.

- 17.2.14 PROCOTEX

- 17.2.15 CARBON CONVERSIONS

- 17.2.16 OAK RIDGE NATIONAL LABORATORY

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Key primary interview participants

- 18.1.2.3 Breakdown of interviews with experts

- 18.1.2.4 Key industry insights

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 BASE NUMBER CALCULATION

- 18.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 18.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 18.4 FORECAST NUMBER CALCULATION

- 18.5 DATA TRIANGULATION

- 18.6 FACTOR ANALYSIS

- 18.7 RESEARCH ASSUMPTIONS

- 18.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS