|

시장보고서

상품코드

1856926

철도 차량 시장 예측(-2032년) : 컴포넌트, 제품 유형(기관차, 고속 철도, 객차), 기관차 기술(기존형, 터보차저, 자기 부상식), 용도(여객 운송, 화물 운송), 지역별Rolling Stock Market by Component, Product Type (Locomotive, Rapid Transit, Coach), Locomotive Technology (Conventional, Turbocharged, Maglev), Application (Passenger Transportation, Freight Transportation) and Region - Global Forecast to 2032 |

||||||

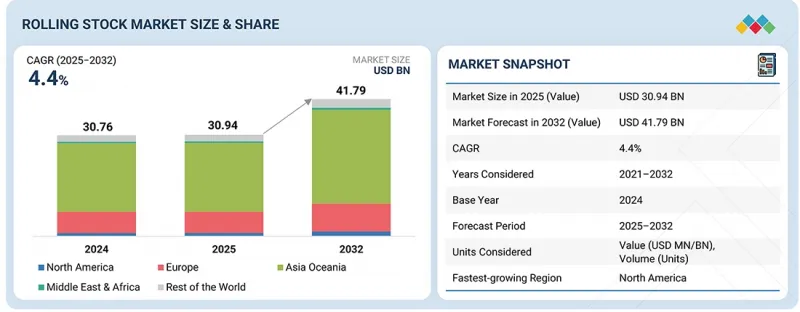

철도 차량 시장 규모는 CAGR 4.4%로 추이하며, 2025년 309억 4,000만 달러에서 2032년에는 417억 9,000만 달러로 성장할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2032년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 금액(달러)·수량(유닛) |

| 부문 | 제품 유형, 기관차 기술, 컴포넌트, 용도, 지역별 |

| 대상 지역 | 아시아·오세아니아, 유럽, 북미, 기타 중동 및 아프리카, 기타 지역 |

철도 차량 수요는 주로 신규 철도 프로젝트, 철도 노선 확장, 노후 열차 교체 수요에 의해 주도되고 있습니다. 각국 정부와 기업은 기차를 더욱 자동화하고 사람의 개입을 줄이면서 이동 시간을 단축하는 것을 목표로 하고 있습니다. 철도망의 전기화, 확장 및 현대화에 대한 투자가 증가하고 있으며, 이는 새로운 철도 차량에 대한 수요를 증가시키고 있습니다. 또한 자율주행형, 배터리 구동형, 수소연료전지형 기관차 개발이 진행됨에 따라 업계 관계자들에게 새로운 비즈니스 기회가 창출되고 있습니다.

"지하철 부문이 예측 기간 중 도시 고속철도 시장에서 큰 점유율을 차지할 것으로 예측됩니다."

세계 최대 지하철망을 보유한 중국은 궤도 연장 측면에서 가장 큰 지하철 시장이며, 광활한 철도망에 수많은 열차가 운행되고 있습니다. 급속한 도시화와 교통 혼잡이 심화되면서 지하철과 같은 효율적이고 대용량의 교통수단에 대한 수요가 증가하고 있습니다. 정부 및 민간 이해관계자들은 기존 네트워크 확장, 신규 노선 개발, 인프라 고도화에 투자하여 여객 운송 능력과 운행 신뢰성을 향상시키기 위해 노력하고 있습니다. 이러한 시스템은 도시 교통 혼잡 완화, 이산화탄소 배출 감소, 경제 성장 지원 등의 역할을 하는 것으로 널리 인식되고 있으며, 이는 지하철 부문에 대한 지속적인 자금 투입과 개발을 지원하고 있습니다. 마찬가지로 인도에서도 도시 교통망의 확장은 지하철 시장의 성장을 가속하고 있습니다.

여객 운송용 철도차량 시장에서는 객차 부문이 예측 기간 중 선두를 차지할 것으로 예측됩니다."

객차는 단거리 출퇴근부터 장거리 이동까지 다양한 여행 수요에 대응할 수 있는 범용성으로 여객 운송용 철도차량 시장을 촉진할 것으로 예측됩니다. 또한 전 세계에서 지속가능하고 비용 효율적인 교통수단에 대한 관심이 높아지는 가운데, 객차는 많은 대체 교통수단보다 에너지 효율이 높기 때문에 수요가 증가하고 있습니다. 예를 들어 인도 철도(Indian Railways)는 2024-2025년도에 4,601대의 객차를 제작했습니다. 최근 객차 설계는 안전성을 높이기 위해 충돌 방지 기술, 강화 구조, 화재 감지 및 억제 시스템, 개선된 비상구 등을 갖추는 한편, 인체공학적 좌석 설계, 공조 제어, 방음 설계, Wi-Fi 연결, 최신 인포테인먼트 시스템 등으로 승객의 편안함도 크게 향상시켰습니다. 안전하고 편안한 이동을 실현하고 있습니다. 또한 객차 운영은 수요에 따라 유연하게 운송력을 조정할 수 있으며, 운행 효율을 최적화할 수 있습니다. 전 세계에서 진행되고 있는 철도 네트워크의 현대화도 객차의 확장 및 업그레이드를 촉진하여 현대적 기준과 승객의 기대에 부응하는 형태로 시장 확대를 지원하고 있습니다.

"예측 기간 중 유럽이 철도 차량 시장에서 큰 점유율을 차지할 것으로 예측됩니다."

유럽은 광범위하고 고도로 현대화 및 전기화된 철도 인프라를 보유하고 있으며, 철도차량 시장에서 큰 비중을 차지할 것으로 예측됩니다. 유럽연합(EU)은 지속가능성과 탈탄소화를 중시하고 있으며, 배터리 열차, 수소열차 등 친환경 철도 기술에 많은 투자를 하고 있으며, 탄소배출을 줄이고 청정 운송을 촉진하는 EU의 목표에 힘을 실어주고 있습니다. 독일, 프랑스, 영국 등의 국가에서는 고속철도와 지역 열차 도입이 진행되고 있으며, 승객 수요와 환경 정책의 양 측면이 이러한 움직임을 지원하고 있습니다. 유럽 그린딜(European Green Deal), 디지털 철도 아젠다(Digital Rail Agenda)와 같은 구상도 철도 차량의 자동화, 디지털화, 국경 간 상호운용성 추진을 가속화하고 있습니다. 또한 Siemens Mobility, Alstom, Stadler Rail과 같은 주요 제조업체를 보유한 강력한 제조거점도 국내외 시장 공급을 지원하며 유럽 철도차량 생산의 리더십을 강화하고 있습니다. 도시화와 지속가능한 모빌리티의 발전에 따라 효율적이고 친환경적인 철도 운송에 대한 수요도 더욱 증가하고 있습니다.

세계의 철도 차량 시장을 조사했으며, 시장 개요, 시장 성장에 대한 각종 영향요인의 분석, 기술·특허의 동향, 법규제 환경, 사례 연구, 시장 규모 추이·예측, 각종 구분·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업의 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 시장 역학

- 촉진요인

- 억제요인

- 기회

- 과제

제6장 업계 동향

- 고객 사업에 영향을 미치는 동향과 혼란

- 가격 분석

- 에코시스템 분석

- 공급망 분석

- 사례 연구 분석

- 특허 분석

- 기술 분석

- 투자와 자금조달 시나리오

- 자금 제공

- AI/생성형 AI의 영향

- 무역 분석

- 관세와 규제 상황

- 주요 컨퍼런스와 이벤트

- 주요 이해관계자와 구입 기준

- 대체 추진 시스템을 위한 전략적 경로

- 철도 인프라 현대화 전략

- 자율주행 열차 기술의 실장 프레임워크

제7장 철도 차량 시장 : 제품 유형별

- 기관차

- 디젤 기관차

- 전기 기관차

- 전기 디젤 기관차

- 도시 고속 철도

- 디젤식 동력 분산차

- 열차(전동 동력 분산차)

- 라이트 레일/트램

- 지하철

- 모노레일

- 객차

- 화차

- 기타

- 주요 인사이트

제8장 철도 차량 시장 : 기관차 기술별

- 기존형 기관차

- 터보차저 부착 기관차

- 초전도 자기 부상식 철도(MAGLEV)

- 전자 서스펜션 방식

- 전동 서스펜션 방식

- 인덕트랙 방식

- 주요 인사이트

제9장 철도 차량 시장 : 용도별

- 여객 운송

- 기관차

- 객차

- 화물 운송

- 기관차

- 화차

- 주요 인사이트

제10장 철도 차량 시장 : 컴포넌트별

- 열차 제어 시스템

- 팬터그래프

- 차축

- 윤축

- 트랙션 모터

- 승객 정보 시스템

- 브레이크

- 공조 시스템

- 보조 전원 시스템

- 기어박스

- 배플 기어

- 커플러

제11장 철도 차량 시장 : 지역별

- 아시아·오세아니아

- 거시경제 전망

- 도시 고속 철도 프로젝트

- 라이트 레일(트램) 프로젝트

- 고속 철도/고속 열차 프로젝트

- 중국

- 인도

- 일본

- 한국

- 호주

- 말레이시아

- 유럽

- 거시경제 전망

- 지하철/고속 철도 프로젝트

- 도시 고속 철도 프로젝트

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 스위스

- 오스트리아

- 스웨덴

- 북미

- 거시경제 전망

- 고속 철도/고속 열차 프로젝트

- 도시 고속 철도 프로젝트

- 미국

- 멕시코

- 캐나다

- 중동 및 아프리카

- 거시경제 전망

- 지하철/모노레일 프로젝트

- 도시 고속 철도 프로젝트

- 남아프리카공화국

- 아랍에미리트

- 이집트

- 이란

- 세계의 기타 지역

- 거시경제 전망

- 지하철/모노레일 프로젝트

- 브라질

- 러시아

- 아르헨티나

제12장 경쟁 구도

- 주요 참여 기업의 전략/강점

- 시장 점유율 분석

- 매출 분석

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 신규 기업/중소기업

- 경쟁 시나리오

제13장 기업 개요

- 주요 기업

- CRRC CORPORATION LIMITED

- SIEMENS AG

- ALSTOM SA

- STADLER RAIL AG

- WABTEC CORPORATION

- KAWASAKI HEAVY INDUSTRIES, LTD.

- CAF GROUP

- HYUNDAI ROTEM COMPANY

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- TALGO

- TRANSMASHHOLDING

- TITAGARH RAIL SYSTEMS LIMITED

- 기타 기업

- TOSHIBA CORPORATION

- HITACHI RAIL LIMITED

- STRUKTON

- DEUTSCHE BAHN AG

- BEML LIMITED

- RAIL VIKAS NIGAM LIMITED

- BRAITHWAITE & CO.(INDIA) LTD.

- CHITTARANJAN LOCOMOTIVE WORKS

- WJIS

- RHOMBERG SERSA RAIL HOLDING GMBH

- SINARA TRANSPORT MACHINES

- TRINITY INDUSTRIES, INC.

- THE GREENBRIER COMPANIES

- DAWONSYS CO., LTD.

제14장 MARKETSANDMARKETS에 의한 제안

- 아시아·오세아니아 지역이 철도 차량 시장을 촉진

- 화물 운송의 증가에 수반하는 화차 수요 증가

- 도시 고속 교통에 대한 수요 증가가 지하철·메트로 시장을 확대

- 결론

제15장 부록

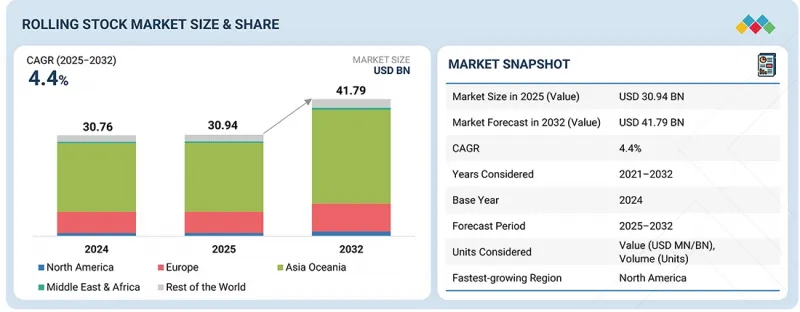

KSA 25.11.14The rolling stock market is projected to grow from USD 30.94 billion in 2025 to USD 41.79 billion by 2032, at a CAGR of 4.4%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion), and Volume (Units) |

| Segments | By product type, locomotive technology, component, application, and region |

| Regions covered | Asia Oceania, Europe, North America, the Middle East & Africa, and the Rest of the World |

The demand for rolling stock is largely driven by new railway projects, rail line expansions, and the need to replace aging trains. Governments and companies aim to make trains more autonomous while reducing human involvement and travel time. Increased investment in electrifying, expanding, and modernizing rail networks is boosting the need for new rolling stock. Additionally, the development of autonomous, battery-powered, and hydrogen fuel cell locomotives is creating new opportunities for industry players.

Metro/Subways are expected to hold a significant market share of the rapid transit rolling stock market during the forecast period.

China, with the largest metro network in the world, is the biggest market for metro systems in terms of track length, supported by a substantial number of trains operating across its extensive rail network. Rapid urbanization and rising traffic congestion are driving the demand for efficient, high-capacity transit solutions such as metros and subways. Governments and private stakeholders are investing in expanding existing networks, developing new lines, and upgrading infrastructure to enhance passenger capacity and service reliability. These systems are increasingly recognized for their role in reducing urban traffic, lowering carbon emissions, and supporting economic growth, which sustains ongoing funding and development in the metro sector. Similarly, in India, expanding urban transit networks are driving metro growth. For instance, in June 2025, Alstom was awarded a USD 158 million (EUR 135 million) contract by Chennai Metro Rail Limited (CMRL) to design, manufacture, supply, test, and commission 96 Metropolis metro cars for Chennai Metro Phase II.

Coaches are expected to lead the passenger transportation rolling stock market during the forecast period.

Coaches are expected to lead the passenger transportation rolling stock market due to their versatility in meeting diverse travel needs, from short-distance commutes to long-distance journeys. The global focus on sustainable and cost-effective transportation further drives coach demand, as they are more energy-efficient than many alternative modes of travel. For instance, Indian Railways produced 4,601 coaches in 2024-2025. Advances in coach design now include enhanced safety features such as anti-collision technology, reinforced structures, fire detection and suppression systems, and improved emergency exits, while passenger comfort is elevated with ergonomically designed seating, climate control, noise reduction, Wi-Fi connectivity, and modern infotainment systems, ensuring a safer and more pleasant travel experience. The scalability of coach operations allows rail operators to adjust capacity according to demand, optimizing efficiency. Furthermore, the ongoing modernization of rail networks worldwide supports the expansion and upgrading of coach fleets to meet contemporary standards and passenger expectations. Aligned with this growth, in August 2024, the Massachusetts Bay Transportation Authority (MBTA) signed an option with Hyundai Rotem for an additional 41 double-deck commuter rail coaches.

"Europe is expected to hold a significant share of the rolling stock market during the forecast period."

Europe is expected to hold a significant share of the rolling stock market due to its extensive, modernized, and highly electrified rail infrastructure. The European Union's focus on sustainability and decarbonization has driven substantial investments in green rail technologies, including battery-electric and hydrogen-powered trains, supporting the EU's goals to reduce carbon emissions and promote clean transportation. Countries such as Germany, France, and the UK are leading in the adoption of high-speed and regional trains, driven by passenger demand and environmental policies. Initiatives such as the European Green Deal and the Digital Rail Agenda have accelerated the modernization of rolling stock, emphasizing automation, digitalization, and cross-border interoperability. Europe's strong manufacturing base, with key players such as Siemens Mobility, Alstom, and Stadler Rail, supports both domestic and export markets, reinforcing the region's leadership in rolling stock production. The ongoing trends of urbanization and sustainable mobility further boost demand for efficient, eco-friendly rail transport. Reflecting this momentum, in June 2024, Alstom signed a USD 377.5 million (€323 million) contract with Polo Logistica FS to supply 70 Traxx Universal locomotives with maintenance services. The locomotives will be manufactured in Italy at Alstom's Vado Ligure site, and maintenance services will be provided across the country. Similarly, in June 2025, Siemens Mobility received a major order from France's Akiem for 50 Vectron Dual Mode locomotives, with the first units scheduled for delivery in the fourth quarter of 2026.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 40%, Tier I - 41%, and Tier II - 19%

- By Designation: CXOs - 23%, Directors - 42%, and Others - 35%

- By Region: North America - 20%, Europe - 24%, Asia Oceania - 36%, MEA - 15%, and RoW - 5%

The rolling stock market is dominated by major players, including CRRC Corporation Limited (China), Siemens AG (Germany), Alstom SA (France), Stadler Rail AG (Switzerland), and Wabtec Corporation (US). These companies offer a wide range of products, including locomotives, passenger coaches, metro and light rail vehicles, freight wagons, and high-speed trains. They also provide comprehensive services such as maintenance, signaling and control systems, digital solutions, spare parts supply, and long-term service contracts, enabling operators to optimize fleet performance and operational efficiency.

Research Coverage:

The report covers the rolling stock market in terms of components, product type (locomotive, rapid transit, coach), locomotive technology (conventional, turbocharged, maglev), application (passenger transportation, freight transportation), and region. It also covers the competitive landscape and company profiles of the major players in the rolling stock market ecosystem.

The study also includes an in-depth competitive analysis of the key market players, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall rolling stock market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights, enabling them to better position their businesses and plan suitable go-to-market strategies.

- The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (energy-efficient and sustainable transportation shift, traffic decongestion and network optimization, expansion of freight transport capacity, and expansion of railroad network and freight corridors) restraints (optimization of the existing fleet through refurbishment, and high capital intensity and investment barriers), opportunities (adoption of hydrogen fuel cell locomotives, rising rail demand from industrial and mining expansion, growing market for battery-operated trains, and leveraging big data and smart analytics in rail infrastructure), and challenges (rising overhaul and maintenance cost burden, and intensive R&D investment requirements).

- Product Development/Innovation: Detailed insights on upcoming technologies and research & development activities in the rolling stock market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the rolling stock market across varied regions.

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the rolling stock market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players, such as CRRC Corporation Limited (China), Siemens AG (Germany), Alstom SA (France), Stadler Rail AG (Switzerland), and Wabtec Corporation (US), in the rolling stock market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews: demand and supply sides

- 2.1.2.2 Primary participants

- 2.1.2.3 Breakdown of primary interviews

- 2.1.2.4 Insights from industry experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ROLLING STOCK MARKET

- 4.2 ROLLING STOCK MARKET, BY PRODUCT TYPE

- 4.3 ROLLING STOCK MARKET, BY APPLICATION

- 4.4 ROLLING STOCK MARKET, BY LOCOMOTIVE TECHNOLOGY

- 4.5 ROLLING STOCK MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Traffic decongestion and network optimization

- 5.2.1.2 Shift toward energy-efficient and sustainable transportation

- 5.2.1.3 Development of advanced rolling stock technologies to enhance passenger comfort

- 5.2.1.4 Advancements in rail network electrification

- 5.2.1.5 Expansion of freight transport capacity

- 5.2.2 RESTRAINTS

- 5.2.2.1 Optimization of existing fleet through refurbishment

- 5.2.2.2 High capital intensity and investment barriers

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Leveraging big data and smart analytics in rail infrastructure

- 5.2.3.2 Rising rail demand from industrial and mining sectors

- 5.2.3.3 Adoption of hydrogen fuel cell locomotives

- 5.2.3.4 Growing market for battery-operated trains

- 5.2.4 CHALLENGES

- 5.2.4.1 Rising overhaul and maintenance cost burden

- 5.2.4.2 Intensive R&D investment requirements

- 5.2.1 DRIVERS

6 INDUSTRY TRENDS

- 6.1 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.2 PRICING ANALYSIS

- 6.2.1 INDICATIVE PRICING OF ROLLING STOCK OFFERED BY KEY PLAYERS

- 6.2.2 AVERAGE SELLING PRICE TREND, BY PRODUCT TYPE

- 6.2.3 AVERAGE SELLING PRICE TREND, BY REGION

- 6.3 ECOSYSTEM ANALYSIS

- 6.4 SUPPLY CHAIN ANALYSIS

- 6.4.1 RAW MATERIAL PROVIDERS AND COMPONENT SUPPLIERS

- 6.4.2 OEMS

- 6.4.3 OPERATORS AND END USERS

- 6.5 CASE STUDY ANALYSIS

- 6.5.1 MODERNIZATION OF ROLLING STOCK WITH STADLER RAIL'S FLIRT EMUS

- 6.5.2 CRRC SETS BENCHMARK FOR EXCAVATION OF BIG ANALOG DATA VALUE

- 6.5.3 GOLINC-M MODULES ENABLE RETROFITTING OF REMOTE CONDITION MONITORING

- 6.5.4 MONORAIL SYSTEMS REDUCE TRAFFIC CONGESTION IN KOREAN METROPOLIS

- 6.5.5 HYDROGEN TRAIN PROJECT HELPS SCOTTISH GOVERNMENT ACHIEVE NET ZERO TARGETS

- 6.5.6 FREIGHTLINER SHIFTS TOWARD NET ZERO WITH LOW-CARBON FUEL

- 6.6 PATENT ANALYSIS

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 KEY TECHNOLOGIES

- 6.7.1.1 Regenerative braking

- 6.7.1.2 Autonomous trains

- 6.7.1.3 Tri-mode trains

- 6.7.1.4 Tilting trains

- 6.7.1.5 Digitalization

- 6.7.1.6 Internet of Trains

- 6.7.2 COMPLEMENTARY TECHNOLOGIES

- 6.7.2.1 Train control and management systems

- 6.7.2.2 Collision avoidance systems

- 6.7.2.3 Intelligent rail transit

- 6.7.3 ADJACENT TECHNOLOGIES

- 6.7.3.1 Big data analytics

- 6.7.3.2 Rail traffic management systems

- 6.7.3.3 Renewable energy systems

- 6.7.1 KEY TECHNOLOGIES

- 6.8 INVESTMENT AND FUNDING SCENARIO

- 6.9 FUNDING, BY APPLICATION

- 6.10 IMPACT OF AI/GEN AI

- 6.11 TRADE ANALYSIS

- 6.12 TARIFF AND REGULATORY LANDSCAPE

- 6.12.1 TARIFF ANALYSIS

- 6.12.1.1 US

- 6.12.1.2 Europe

- 6.12.1.3 India

- 6.12.1.4 South Korea

- 6.12.1.5 China

- 6.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12.1 TARIFF ANALYSIS

- 6.13 KEY CONFERENCES AND EVENTS

- 6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.14.2 BUYING CRITERIA

- 6.15 STRATEGIC PATHWAYS FOR ALTERNATIVE PROPULSION SYSTEMS

- 6.15.1 TECHNOLOGY READINESS

- 6.15.1.1 Hydrogen fuel cells

- 6.15.1.2 Battery-electric

- 6.15.1.3 Hybrid/Alternative engines

- 6.15.1.4 Emerging options

- 6.15.2 POLICY AND INCENTIVE ALIGNMENT

- 6.15.2.1 Government strategies and targets

- 6.15.2.2 Funding and grants

- 6.15.2.3 Regulations and mandates

- 6.15.2.4 Regional Initiatives

- 6.15.3 SUPPLY CHAIN AND INFRASTRUCTURE

- 6.15.3.1 Manufacturing ecosystems

- 6.15.3.2 Fueling and charging infrastructure

- 6.15.3.3 Supplier networks

- 6.15.1 TECHNOLOGY READINESS

- 6.16 RAILWAY INFRASTRUCTURE MODERNIZATION STRATEGY

- 6.16.1 DIGITALIZATION AND IOT INTEGRATION

- 6.16.1.1 DB/Digital train control

- 6.16.1.2 Onboard diagnostics and telematics

- 6.16.2 ENERGY EFFICIENCY UPGRADES

- 6.16.3 CYBERSECURITY AND DATA STRATEGIES

- 6.16.4 EU CYBERSECURITY REGULATIONS

- 6.16.5 US CYBERSECURITY DIRECTIVES

- 6.16.6 DATA-CENTRIC INITIATIVES

- 6.16.1 DIGITALIZATION AND IOT INTEGRATION

- 6.17 IMPLEMENTATION FRAMEWORK FOR AUTONOMOUS TRAIN TECHNOLOGY

- 6.17.1 SAFETY AND REGULATORY COMPLIANCE

- 6.17.2 OPERATIONAL TRANSFORMATION STRATEGY

7 ROLLING STOCK MARKET, BY PRODUCT TYPE

- 7.1 INTRODUCTION

- 7.2 LOCOMOTIVES

- 7.2.1 DIESEL LOCOMOTIVES

- 7.2.1.1 Electrification of railway networks in Europe and Asia to impede market

- 7.2.2 ELECTRIC LOCOMOTIVES

- 7.2.2.1 Rapid electrification of rail networks to drive market

- 7.2.3 ELECTRO-DIESEL LOCOMOTIVES

- 7.2.3.1 Public and private sectors' emphasis on sustainable practices to drive market

- 7.2.1 DIESEL LOCOMOTIVES

- 7.3 RAPID TRANSIT

- 7.3.1 DIESEL MULTIPLE UNITS

- 7.3.1.1 Electrification constraints in select regions to drive market

- 7.3.2 ELECTRIC MULTIPLE UNITS

- 7.3.2.1 Performance and efficiency advantages over diesel fueling to drive market

- 7.3.3 LIGHT RAILS/TRAMS

- 7.3.3.1 Push for alternatives to traditional buses and cars to drive market

- 7.3.4 SUBWAYS/METROS

- 7.3.4.1 Investments in urban transportation networks to drive market

- 7.3.5 MONORAILS

- 7.3.1 DIESEL MULTIPLE UNITS

- 7.4 COACHES

- 7.4.1 DEMAND FOR ENHANCED RAIL TRAVEL EXPERIENCES TO DRIVE MARKET

- 7.5 WAGONS

- 7.5.1 NEED FOR HIGH-CAPACITY FREIGHT IN LOGISTICS AND MANUFACTURING TO DRIVE MARKET

- 7.6 OTHER PRODUCT TYPES

- 7.7 PRIMARY INSIGHTS

8 ROLLING STOCK MARKET, BY LOCOMOTIVE TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 CONVENTIONAL LOCOMOTIVES

- 8.2.1 IMPROVED PERFORMANCE WITH TECHNOLOGICAL INNOVATIONS TO DRIVE MARKET

- 8.3 TURBOCHARGED LOCOMOTIVES

- 8.3.1 COMPLIANCE WITH STRICT EMISSION REGULATIONS TO DRIVE MARKET

- 8.4 MAGLEV

- 8.4.1 ELECTROMAGNETIC SUSPENSION

- 8.4.2 ELECTRODYNAMIC SUSPENSION

- 8.4.3 INDUCTRACK

- 8.5 PRIMARY INSIGHTS

9 ROLLING STOCK MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 PASSENGER TRANSPORTATION

- 9.2.1 LOCOMOTIVES

- 9.2.1.1 Rising adoption of electric rail systems to drive market

- 9.2.2 COACHES

- 9.2.2.1 Integration of enhanced safety systems to drive market

- 9.2.1 LOCOMOTIVES

- 9.3 FREIGHT TRANSPORTATION

- 9.3.1 LOCOMOTIVES

- 9.3.1.1 Efforts to lower operational expenses to drive market

- 9.3.2 WAGONS

- 9.3.2.1 Growing application in freight and logistics to drive market

- 9.3.1 LOCOMOTIVES

- 9.4 PRIMARY INSIGHTS

10 ROLLING STOCK MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 TRAIN CONTROL SYSTEMS

- 10.3 PANTOGRAPHS

- 10.4 AXLES

- 10.5 WHEELSETS

- 10.6 TRACTION MOTORS

- 10.7 PASSENGER INFORMATION SYSTEMS

- 10.8 BRAKES

- 10.9 AIR CONDITIONING SYSTEMS

- 10.10 AUXILIARY POWER SYSTEMS

- 10.11 GEARBOXES

- 10.12 BAFFLE GEARS

- 10.13 COUPLERS

11 ROLLING STOCK MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA OCEANIA

- 11.2.1 MACROECONOMIC OUTLOOK

- 11.2.2 RAPID TRANSIT PROJECTS

- 11.2.3 LIGHT RAIL PROJECTS

- 11.2.4 HIGH-SPEED RAIL/BULLET TRAIN PROJECTS

- 11.2.5 CHINA

- 11.2.5.1 Expansion of high-speed rail infrastructure to drive market

- 11.2.6 INDIA

- 11.2.6.1 Growth of electrified rail infrastructure to drive market

- 11.2.7 JAPAN

- 11.2.7.1 Strong presence of rail service providers to drive market

- 11.2.8 SOUTH KOREA

- 11.2.8.1 Government initiatives supporting public transportation to drive market

- 11.2.9 AUSTRALIA

- 11.2.10 MALAYSIA

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK

- 11.3.2 METRO/HIGH-SPEED RAILWAY PROJECTS

- 11.3.3 RAPID TRANSIT PROJECTS

- 11.3.4 GERMANY

- 11.3.4.1 Rising investments in railway infrastructure modernization to drive market

- 11.3.5 FRANCE

- 11.3.5.1 Government subsidies and incentives for sustainable transportation to drive market

- 11.3.6 UK

- 11.3.6.1 Ongoing upgrades of domestic rail networks to drive market

- 11.3.7 ITALY

- 11.3.7.1 Expanding railway networks to drive market

- 11.3.8 SPAIN

- 11.3.8.1 Modernization of mass rapid transit to drive market

- 11.3.9 SWITZERLAND

- 11.3.10 AUSTRIA

- 11.3.11 SWEDEN

- 11.4 NORTH AMERICA

- 11.4.1 MACROECONOMIC OUTLOOK

- 11.4.2 HIGH-SPEED RAIL/BULLET TRAIN PROJECTS

- 11.4.3 RAPID TRANSIT PROJECTS

- 11.4.4 US

- 11.4.4.1 Modernization of existing transportation modalities to drive market

- 11.4.5 MEXICO

- 11.4.5.1 Rail network expansion and modernization to drive market

- 11.4.6 CANADA

- 11.4.6.1 Elevated demand for passenger and freight transportation to drive market

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MACROECONOMIC OUTLOOK

- 11.5.2 METRO/MONORAIL PROJECTS

- 11.5.3 RAPID TRANSIT PROJECTS

- 11.5.4 SOUTH AFRICA

- 11.5.4.1 Government investments in railway sector to drive market

- 11.5.5 UAE

- 11.5.5.1 Advances in rail infrastructure to drive market

- 11.5.6 EGYPT

- 11.5.6.1 Booming tourism industry to drive market

- 11.5.7 IRAN

- 11.6 REST OF THE WORLD

- 11.6.1 MACROECONOMIC OUTLOOK

- 11.6.2 METRO/MONORAIL PROJECTS

- 11.6.3 BRAZIL

- 11.6.3.1 Growing rail investments and modernization to drive market

- 11.6.4 RUSSIA

- 11.6.4.1 Expansion of metro and subway networks to drive market

- 11.6.5 ARGENTINA

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 REVENUE ANALYSIS, 2020-2024

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Application footprint

- 12.7.5.4 Product type footprint

- 12.7.5.5 Locomotive technology footprint

- 12.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING

- 12.8.5.1 List of start-ups/SMEs

- 12.8.5.2 Competitive benchmarking of start-ups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 CONTRACTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 CRRC CORPORATION LIMITED

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches/developments

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Contracts

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 SIEMENS AG

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches/developments

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.3.4 Contracts

- 13.1.2.3.5 Other developments

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 ALSTOM SA

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches/developments

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.3.4 Contracts

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 STADLER RAIL AG

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches/developments

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.3.4 Contracts

- 13.1.4.3.5 Other developments

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 WABTEC CORPORATION

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches/developments

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.3.4 Contracts

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 KAWASAKI HEAVY INDUSTRIES, LTD.

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches/developments

- 13.1.6.3.2 Contracts

- 13.1.7 CAF GROUP

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.3.2 Expansions

- 13.1.7.3.3 Contracts

- 13.1.8 HYUNDAI ROTEM COMPANY

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches/developments

- 13.1.8.3.2 Deals

- 13.1.8.3.3 Contracts

- 13.1.8.3.4 Other developments

- 13.1.9 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.9.3.2 Expansions

- 13.1.9.3.3 Contracts

- 13.1.10 TALGO

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches/developments

- 13.1.10.3.2 Deals

- 13.1.10.3.3 Contracts

- 13.1.11 TRANSMASHHOLDING

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches/developments

- 13.1.11.3.2 Deals

- 13.1.11.3.3 Expansions

- 13.1.11.3.4 Contracts

- 13.1.12 TITAGARH RAIL SYSTEMS LIMITED

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches/developments

- 13.1.12.3.2 Deals

- 13.1.12.3.3 Contracts

- 13.1.1 CRRC CORPORATION LIMITED

- 13.2 OTHER PLAYERS

- 13.2.1 TOSHIBA CORPORATION

- 13.2.2 HITACHI RAIL LIMITED

- 13.2.3 STRUKTON

- 13.2.4 DEUTSCHE BAHN AG

- 13.2.5 BEML LIMITED

- 13.2.6 RAIL VIKAS NIGAM LIMITED

- 13.2.7 BRAITHWAITE & CO. (INDIA) LTD.

- 13.2.8 CHITTARANJAN LOCOMOTIVE WORKS

- 13.2.9 WJIS

- 13.2.10 RHOMBERG SERSA RAIL HOLDING GMBH

- 13.2.11 SINARA TRANSPORT MACHINES

- 13.2.12 TRINITY INDUSTRIES, INC.

- 13.2.13 THE GREENBRIER COMPANIES

- 13.2.14 DAWONSYS CO., LTD.

14 RECOMMENDATIONS BY MARKETSANDMARKETS

- 14.1 ASIA OCEANIA TO BE LEADING MARKET FOR ROLLING STOCK

- 14.2 ELEVATED DEMAND FOR WAGONS DUE TO RISE IN FREIGHT TRANSPORTATION

- 14.3 NEED FOR FAST URBAN TRANSPORTATION TO BOOST MARKET FOR SUBWAYS/METROS

- 14.4 CONCLUSION

15 APPENDIX

- 15.1 KEY INDUSTRY INSIGHTS

- 15.2 DISCUSSION GUIDE

- 15.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.4 CUSTOMIZATION OPTIONS

- 15.4.1 ADDITIONAL COMPANY PROFILES (UP TO FIVE)

- 15.4.2 ROLLING STOCK MARKET, BY TECHNOLOGY, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 15.4.3 ROLLING STOCK MARKET, BY PRODUCT TYPE, AT COUNTRY LEVEL (FOR COUNTRIES COVERED IN REPORT)

- 15.5 RELATED REPORTS

- 15.6 AUTHOR DETAILS