|

시장보고서

상품코드

1793321

특수 사료 첨가물 시장 : 유형별, 가축별, 유래별, 형상별, 기능별, 제조 기술별, 지역별 예측(-2030년)Specialty Feed Additives Market by Livestock, Type, Form, Source, Function, Manufacturing Technology, and Region - Global Forecast to 2030 |

||||||

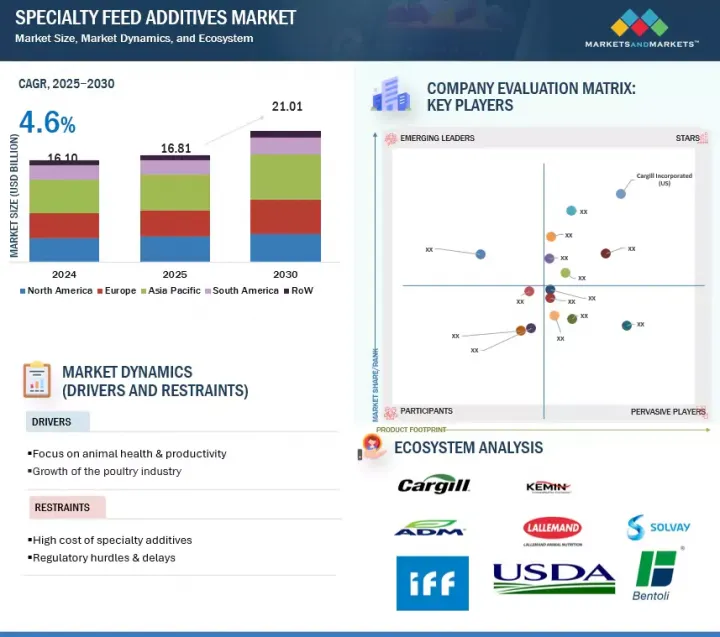

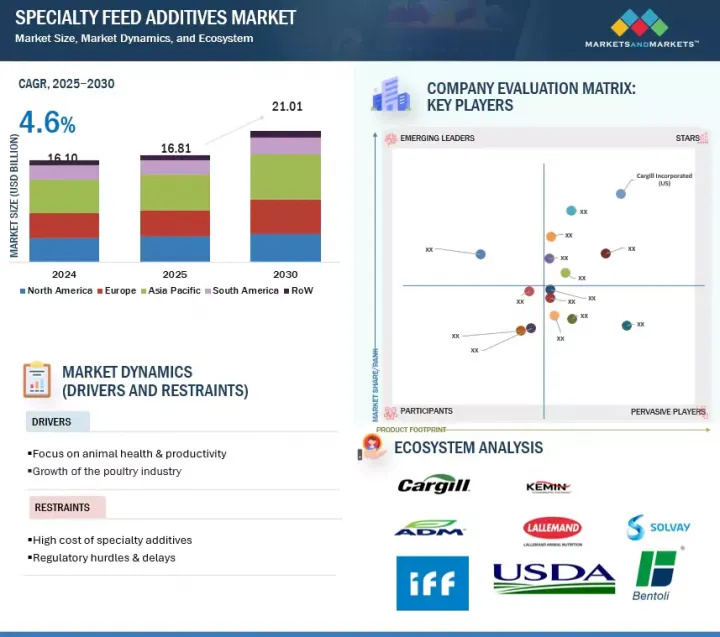

특수 사료 첨가물 시장 규모는 2025년에 168억 1,000만 달러로 추정되며, 4.6%의 연평균 성장률(CAGR)로 성장할 것으로 예측되며, 2030년에는 210억 1,000만 달러에 이를 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2025-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(달러) 및 킬로톤(KT) |

| 부문별 | 유형별, 가축별, 유래별, 형상별, 기능별, 제조 기술별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미 및 기타 지역 |

특수 사료 첨가제 시장은 고품질 동물 단백질에 대한 전 세계 수요 증가와 동물 건강 및 성능에 대한 강조가 강화되면서 안정적인 성장을 보이고 있습니다. 아미노산, 효소, 유기산, 식물성 성분, 곰팡이 독소 결합제 등 이러한 첨가제는 사료 효율성 향상, 장 건강 개선, 가축 면역력 강화에 중요한 역할을 합니다. 이 시장은 항생제 무첨가 생산으로의 전환, 동물 복지 인식 향상, 엄격한 사료 안전 규제로 인해 촉진되고 있습니다. 아시아태평양과 라틴 아메리카와 같은 지역에서는 동물 사육의 산업화와 급속한 도시화가 성능 향상 첨가제의 채택을 촉진하고 있습니다. 그러나 원재료 가격 변동, 공급망 차질, 규제 복잡성 등 산업은 다양한 도전 과제에 직면해 있습니다.

특수 사료 첨가제 미래는 전 세계 문제로 인해 어려운 상황을 겪고 있습니다. 2023년 전체 사료 생산량은 0.2% 감소했으며, 이는 생산 비용 증가, 지정학적 긴장, 동물 사료 공급에 대한 고려 증가로 인해 촉진되었습니다. 주요 이슈로는 생산 비용 증가, 지역적 긴장, 기후 변화가 있으며, 이는 유럽의 공급 복잡성과 미국의 소 사육 주기 변화와 관련된 변동성을 초래하고 있습니다. 사료 효율성은 아메리카 지역을 포함한 세계 일부 지역에서 개선되고 있습니다. 이는 원재료 공급의 불확실성으로 인한 일부 문제를 완화했지만, 비용과 공급 안정성은 생산과 가격에 미치는 영향으로 인해 여전히 전 세계 우려 사항입니다.

시장은 네 가지 주요 요인에 의해 영향을 받고 있습니다: 동물 영양 기술의 발전, 지정학적 긴장, 식량 안보, 에너지 문제. 국가 간 지정학적 긴장은 시장에 영향을 미치고 있습니다. 예시로는 미국과 중국의 갈등, 우크라이나-러시아 갈등이 있습니다. 이 갈등은 전 세계 공급망을 재편하고 생산 비용 및 운송 비용을 증가시켰으며, 소비자의 선호도를 동물 단백질에서 다른 방향으로 전환시켰습니다. 두 번째로, 식물 기반 천연 사료와 지속 가능성 동향은 혁신과 사료 첨가제 개발을 통해 시장을 영향을 미치고 있습니다. 이러한 동향은 운영 비용과 건강 문제에도 크게 영향을 미치고 있습니다.

건조 특수 사료 첨가제 시장은 분쇄 사료가 펠릿 사료보다 비용이 저렴하기 때문에 지배적일 것으로 예상됩니다. 펠릿 사료는 기계적 펠릿화 과정에서 10% 더 많은 비용을 소비합니다. 이 과정은 사료 손실을 최소화하고 신체 영양소 흡수 능력을 향상시킵니다. 가금류 산업은 분쇄된 펠릿으로 구성된 분쇄 사료를 선호하며, 이는 육계 닭에게 간단한 사료 공급 솔루션을 제공합니다. 건조 형태는 액체 형태에 비해 우수한 보관 능력과 분해 저항성을 제공하기 때문에 가축 사육자에게 매력적입니다. 이 제품의 안정성은 폐기물과 비용을 최소화하며, 건조 구성은 운송 비용 감소와 포장 요구사항 감소로 이어집니다. 제조사와 사용자의 편의성은 온도 변동에 강하고 제품의 유통기한을 연장하는 건조 첨가물에서 비롯됩니다. 시장 참여자들은 주로 향료, 감미료, 프로바이오틱스, 산화방지제, 항산화제, 사료 전환율 개선제 등 가축 사료에 사용되는 건조 제품을 주로 공급합니다.

프로바이오틱스 부문은 특수 사료 첨가제 시장 내 유형 부문에서 상당한 점유율을 차지합니다. 유럽 등 지역에서 사료 첨가제 내 항생제 사용 제한, 항생제 무첨가 제품에 대한 소비자 선호도, 환경 지속 가능성 등으로 인해 프로바이오틱스 채택이 증가하고 있습니다. 2024년 펜실베이니아 주립대 연구에 따르면 Bacillus subtilis와 Bacillus amyloliquefaciens와 같은 프로바이오틱스는 320마리의 육계 병아리에서 장 건강, 영양소 흡수, 성장 성능을 개선했습니다. 열대 지역 가금류 건강을 타겟으로 한 에보닉은 최근 인도에서 Poultry India 2024에서 공개된 Ecobiol Soluble Plus를 출시했으며, 이는 시장 확대를 지원할 것으로 예상됩니다. 프로바이오틱스는 전략적 산업 협력, 지속적인 혁신, 전 세계 육류 소비 증가, 지속 가능한 동물 영양 솔루션에 대한 연구 확대에 촉진되어 특수 사료 첨가제 시장에서 큰 성장을 보일 것으로 예상됩니다.

2024년, 미국 육류 산업은 전 세계 단백질 공급망의 리더십, 혁신, 경쟁 우위를 입증하며 우수한 수출 성과를 기록했습니다. 미국산 돼지고기의 수출량은 과거 최고치인 303만 톤(334만 톤), 수출액은 86억 3,000만 달러에 이르고, 업계는 살두수 1마리당 66.53 달러의 피크 수출액을 기록해, 왕성한 국제 수요와 미국산 돼지고기의 안정된 품질을 뒷받침했습니다. 마찬가지로 미국산 쇠고기 수출액은 104억 5,000만 달러로 과거 최고를 기록했고, 1마리당 수출액은 415.08 달러로 상승했습니다.

이 강력한 수출 성과와 함께 미국은 혁신 주도형 고급 기술 발전을 바탕으로 북미 특수 사료 첨가제 시장에서 지배적인 점유율을 유지하고 있습니다. 2024년의 주목할 만한 발전으로는 Kemin Industries Inc. (미국)의 Animal Nutrition and Health - North America 부문에서 개발한 향후 돼지 사료 산화제 FORMYL의 출시입니다. 이 제품은 칼슘 포르메이트와 시트르산의 독점적 캡슐화 블렌드를 활용해 항생제 비사용 메커니즘을 통해 장 건강을 촉진하고 돼지 생산성을 향상시킵니다. 위장관 내의 표적 작용은 pH 감소와 병원체 통제를 지원하며, 이는 미국 산업의 사료 기술적 발전과 특수 첨가제 분야 리더십 유지에 대한 의지를 반영합니다.

본 보고서에서는 세계의 특수 사료 첨가물 시장에 대해 조사했으며, 유형별, 가축별, 유래별, 형상별, 기능별, 제조 기술별, 지역별 동향, 시장 진출기업프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 거시경제지표

- 시장 역학

- 생성형 AI가 동물 영양/특수 사료 첨가물에 미치는 영향

제6장 업계 동향

- 소개

- 미국 관세의 영향(2025년) - 특수 사료 첨가물 시장

- 공급망 분석

- 밸류체인 분석

- 무역 분석

- 기술 분석

- 가격 분석

- 생태계 분석

- 구매자에게 영향을 미치는 동향 및 혼란

- 특허 분석

- 주요 회의 및 이벤트

- 관세 및 규제 상황

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 사례 연구

- 투자 및 자금조달 시나리오

제7장 특수 사료 첨가물 시장(유형별)

- 소개

- 식물성 첨가제

- 유기산

- 마이코톡신 결합제 및 조절제

- 해조류 오메가-3

- 펠렛 결합제

- 프로바이오틱스

- 항산화제

- 물 살균제

- 향료 및 감미료

제8장 특수 사료 첨가물 시장(가축별)

- 소개

- 가금

- 반추동물

- 돼지

- 수생동물

- 반려동물

제9장 특수 사료 첨가물 시장(유래별)

- 소개

- 합성

- 천연

제10장 특수 사료 첨가물 시장(형상별)

- 소개

- 건조

- 액체

제11장 특수 사료 첨가물 시장(기능별)

- 소개

- 장 건강과 소화 기능

- 마이코톡신 관리

- 기호성 향상제

- 기능성 성분의 보존

- 기타

제12장 특수 사료 첨가물 시장(제조 기술별)

- 소개

- 발효

- 추출 및 정제

- 마이크로캡슐화/코팅

- 입자화 및 건조

- 기타 제조 기술

제13장 특수 사료 첨가물 시장(지역별)

- 소개

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 중국

- 인도

- 일본

- 호주 및 뉴질랜드

- 한국

- 인도네시아

- 태국

- 베트남

- 말레이시아

- 필리핀

- 기타

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 콜롬비아

- 베네수엘라

- 기타

- 기타 지역

- 아프리카

- 기타

- 중동

제14장 경쟁 구도

- 개요

- 주요 진입기업의 전략 및 강점

- 수익 분석

- 시장 점유율 분석

- 기업평가와 재무지표

- 브랜드 비교 분석

- 기업평가 매트릭스 : 주요 진출기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오와 동향

제15장 기업 프로파일

- 주요 진출기업

- CARGILL, INCORPORATED

- ARCHER DANIELS MIDLAND(ADM) COMPANY

- INTERNATIONAL FLAVORS & FRAGRANCES INC.

- EVONIK INDUSTRIES AG

- BASF SE

- NOVONESIS GROUP

- NUTRECO

- LALLEMAND INC.

- BENTOLI

- ALLTECH

- PETROLIAM NASIONAL BERHAD(PETRONAS)

- ADISSEO

- KEMIN INDUSTRIES, INC.

- LAND O'LAKES, INC.

- NOVUS INTERNATIONAL, INC.

- 기타 기업

- NEOSPARK DRUGS AND CHEMICALS PRIVATE LIMITED

- GLOBAL NUTRITION INTERNATIONAL

- VOLAC INTERNATIONAL LTD.

- NUTREX

- IMPEXTRACO NV

- INNOVAD

- TEX BIOSCIENCES(P) LTD.

- CENTAFARM SRL

- NUQO FEED ADDITIVES

- PALITAL FEED ADDITIVES BV

제16장 인접 시장과 관련 시장

제17장 부록

HBR 25.08.22The specialty feed additives market is estimated at USD 16.81 billion in 2025 and is projected to reach USD 21.01 billion by 2030, at a CAGR of 4.6%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD) and Volume (KT) |

| Segments | By Livestock, Type, Form, Source, Function, Manufacturing Technology, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and RoW |

The specialty feed additives market is experiencing steady growth due to rising global demand for high-quality animal protein and increasing emphasis on animal health and performance. These additives, including amino acids, enzymes, organic acids, phytogenics, and mycotoxin binders, play a vital role in enhancing feed efficiency, improving gut health, and boosting immunity in livestock. The market is driven by the shift toward antibiotic-free production, growing awareness about animal welfare, and stringent feed safety regulations. In regions such as Asia-Pacific and Latin America, industrialization of animal farming and rapid urbanization are accelerating the adoption of performance-enhancing additives. However, the industry faces challenges such as fluctuating raw material prices, supply chain disruptions, and regulatory complexities.

"Disruptions in the specialty feed additives market"

The landscape for specialty feed additives is difficult due to broad-based global issues, as overall feed production fell by 0.2% in 2023. The decreased production is driven by the increasing costs of production, geopolitical tensions, and increased considerations of supply for animal feed, which have created pressures on the sector. Key issues include increased costs of production, geographic tensions, and climate change, which contribute to the complications of supply in Europe and the shifts associated with the cattle cycle in the United States. Feed efficiency is improving in parts of the world, including the Americas. It has alleviated some issues caused by unpredictability in the supply of raw materials, although cost and availability are still global issues of concern for their implications on production and price.

The market is influenced by four key factors: advances in animal nutrition, geopolitical tensions, food security, and energy issues. Geopolitical tensions between nations are influencing the market. Examples include the conflict between the US and China as well as the Ukraine-Russia conflict, which has re-positioned global supply chains, increased production costs and shipping costs, and redirected consumer preferences away from animal protein. Second, plant-based natural feeds and sustainability trends are impacting the market by developing innovations and feed additives, as these trends also prominently impact operational costs and health concerns.

"The dry form is projected to be dominant in the market."

The dry specialty feed additive market is projected to be dominant because mash feed costs less than pellet feed, which consumes 10% more expenses during the mechanical pelletization process. The process minimizes feed loss and increases the body's ability to digest nutrients. The poultry industry prefers crumbling because it consists of broken pellets, which provide simple feeding solutions for broiler birds. Dry forms attract livestock producers because they offer superior storage capabilities and better resistance to degradation compared to liquid forms. The stable nature of this product minimizes waste and expenses while its dry composition results in lower transportation costs and reduced packaging requirements. The ease of use for manufacturers and users comes from dry additives that resist temperature variations and help products last longer on store shelves. Market participants predominantly distribute dry products, including flavors, sweeteners, probiotics, acidifiers, mycotoxin binders, antioxidants that enhance digestibility and palatability, and feed conversion ratios in livestock.

"The probiotics segment will hold a significant market share among the types in the specialty feed additives market."

The probiotic segment holds a significant share within the type segment of the specialty feed additives market. Probiotic adoption has increased in regions such as Europe due to restrictions on antibiotics in feed additives, consumer preferences for antibiotic-free products, and environmental sustainability. A 2024 Penn State study found that probiotics, like Bacillus subtilis and Bacillus amyloliquefaciens, improve gut health, nutrient absorption, and growth performance in 320 broiler chicks. Targeting poultry health in tropical regions, Evonik recently introduced Ecobiol Soluble Plus in India, which was unveiled at Poultry India 2024 and is expected to support market expansion. Probiotics are expected to witness significant growth in the specialty feed additives market, driven by strategic industry collaborations, continuous innovation, rising global meat consumption, and increasing research focused on sustainable animal nutrition solutions.

"The US is projected to dominate the North American specialty feed additives market during the forecast period."

In 2024, the US meat industry demonstrated exceptional export performance, affirming its leadership, innovation, and competitive advantage in the global protein supply chain. US pork exports reached a historic high of 3.03 million tonnes (3.34 million tons), valued at USD 8.63 billion, while the industry recorded a peak export value of USD 66.53 per head slaughtered, underscoring robust international demand and the consistent quality of US pork. Similarly, US beef exports delivered a record value of USD 10.45 billion, with per-head export value rising to USD 415.08, reflecting the premium positioning of US beef in overseas markets despite supply-side constraints.

Complementing this strong export performance, the US continues to hold a dominant share in the North American specialty feed additives market, supported by innovation-led advancements. A notable development in 2024 was Kemin Industries Inc.'s (US) launch of FORMYL, a next-generation swine feed acidifier developed by its Animal Nutrition and Health - North America division. The product utilizes a proprietary encapsulated blend of calcium formate and citric acid to promote gut health and enhance pig productivity via a non-antibiotic mechanism. Its targeted action in the gastrointestinal tract aids in pH reduction and supports pathogen control, reflecting the US industry's commitment to advancing feed technologies and maintaining its leadership in specialty additives.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the specialty feed additives market.

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: CXOs - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 20%, Asia Pacific - 30%, South America - 15%, and Rest of the World - 10%

Prominent companies in the market include Cargill, Incorporated (US), ADM (US), International Flavors & Fragrances Inc. (US), Evonik Industries AG (Germany), BASF SE (Germany), Novonesis Group (Denmark), Adisseo (France), Solvay (Belgium), Nutreco (Netherlands), Kemin Industries, Inc. (US), and Lallemand Inc. (Canada).

Research Coverage

This research report categorizes the specialty feed additives market by type (phytogenics, organic acids, probiotics, mycotoxin binders & modifiers, algae omega 3, pellet binders, probiotics, antioxidants, water disinfectants, flavors & sweeteners), livestock (poultry, swine, ruminants, aquatic animals & companion animals), form (dry, liquid), source (natural, synthetic), functions, and manufacturing technology (qualitative), and region (North America, Europe, Asia Pacific, South America, and Rest of the World).

The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of specialty feed additives. A thorough analysis of the key industry players has provided insights into their business, services, key strategies, contracts, partnerships, agreements, product launches, mergers & acquisitions, and recent developments associated with the specialty feed additives market. This report covers the competitive analysis of upcoming startups in the specialty feed additives market ecosystem. Furthermore, industry-specific trends such as technology analysis, ecosystem & market mapping, and patent & regulatory landscape, among others, are also covered in the study.

Reasons to Buy This Report

The report will offer market leaders/new entrants' information on the closest approximate revenue numbers for the overall specialty feed additives and subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (Increased demand for meat-based products drives the demand), restraints (reliance on antibiotics for growth promotion in livestock production), opportunities (evolution of precision livestock farming), and challenges (fluctuating raw material costs) influencing the growth of the specialty feed additives market

- Product Development/Innovation: Detailed insights into research & development activities and new product launches in the specialty feed additives market

- Market Development: Comprehensive information about lucrative market analysis of specialty feed additives across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the specialty feed additives market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as Cargill, Incorporated (US), ADM (US), International Flavors & Fragrances Inc. (US), and other players in the specialty feed additives market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary profiles

- 2.1.2.3 Key insights from industry experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 TOP-DOWN APPROACH

- 2.2.2 SUPPLY-SIDE ANALYSIS

- 2.2.3 BOTTOM-UP APPROACH (DEMAND SIDE)

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 LIMITATIONS & RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 SPECIALTY FEED ADDITIVES MARKET OVERVIEW

- 4.2 SPECIALTY FEED ADDITIVES MARKET: SHARE OF MAJOR REGIONAL SUBMARKETS

- 4.3 ASIA PACIFIC: SPECIALTY FEED ADDITIVES MARKET, BY SOURCE & COUNTRY

- 4.4 SPECIALTY FEED ADDITIVES MARKET, BY FORM FOR REGION

- 4.5 SPECIALTY FEED ADDITIVES MARKET, BY TYPE

- 4.6 SPECIALTY FEED ADDITIVES MARKET, BY LIVESTOCK

- 4.7 SPECIALTY FEED ADDITIVES MARKET, BY FUNCTION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 RISE IN DEMAND FOR COMPOUND FEED

- 5.2.2 GROWTH OPPORTUNITIES IN DEVELOPING REGIONS

- 5.3 MARKET DYNAMICS

- 5.3.1 DRIVERS

- 5.3.1.1 Increase in demand for meat-based products

- 5.3.1.2 Growth in feed production

- 5.3.1.3 Rise in awareness about feed quality

- 5.3.1.4 Increase in number of feed mills across regions

- 5.3.2 RESTRAINTS

- 5.3.2.1 Reliance on antibiotics for growth promotion in livestock production

- 5.3.2.2 Inconsistency in regulatory structure

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Evolution of precision livestock farming

- 5.3.3.2 Increase in demand for nutritional supplements for monogastric animals

- 5.3.4 CHALLENGES

- 5.3.4.1 Rising operational and raw material costs

- 5.3.4.2 Sustainability of feed and livestock chain

- 5.3.1 DRIVERS

- 5.4 IMPACT OF GEN AI ON ANIMAL NUTRITION/SPECIALTY FEED ADDITIVES

- 5.4.1 INTRODUCTION

- 5.4.2 USE OF GEN AI IN ANIMAL NUTRITION/SPECIALTY FEED ADDITIVES

- 5.4.3 CASE STUDY ANALYSIS

- 5.4.3.1 Revolutionizing dairy nutrition through AI innovations

- 5.4.3.2 Enhancing livestock feed formulation through decision support tools

- 5.4.4 IMPACT ON SPECIALTY FEED ADDITIVES MARKET

- 5.4.5 ADJACENT ECOSYSTEM WORKING ON GEN AI

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 IMPACT OF 2025 US TARIFF - SPECIALTY FEED ADDITIVES MARKET

- 6.2.1 INTRODUCTION

- 6.2.2 KEY TARIFF RATES

- 6.2.3 DISRUPTION IN SPECIALTY FEED ADDITIVE PRODUCTS

- 6.2.4 PRICE IMPACT ANALYSIS

- 6.2.5 IMPACT ON COUNTRY/REGION

- 6.2.5.1 US

- 6.2.5.2 Europe

- 6.2.5.3 Asia Pacific

- 6.2.6 IMPACT ON END-USE INDUSTRIES

- 6.3 SUPPLY CHAIN ANALYSIS

- 6.4 VALUE CHAIN ANALYSIS

- 6.4.1 RESEARCH AND PRODUCT DEVELOPMENT

- 6.4.2 RAW MATERIAL SOURCING

- 6.4.3 PRODUCTION

- 6.4.4 QUALITY CONTROL & SAFETY

- 6.4.5 DISTRIBUTION & LOGISTICS

- 6.4.6 MARKETING & SALES

- 6.4.7 END USERS

- 6.5 TRADE ANALYSIS

- 6.5.1 EXPORT SCENARIO

- 6.5.2 IMPORT SCENARIO

- 6.6 TECHNOLOGY ANALYSIS

- 6.6.1 KEY TECHNOLOGIES

- 6.6.1.1 Pelletizing and extrusion

- 6.6.1.2 Coating technologies

- 6.6.2 COMPLEMENTARY TECHNOLOGY

- 6.6.2.1 Omics technologies

- 6.6.3 ADJACENT TECHNOLOGY

- 6.6.3.1 Precision livestock farming

- 6.6.1 KEY TECHNOLOGIES

- 6.7 PRICING ANALYSIS

- 6.7.1 INTRODUCTION

- 6.7.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS

- 6.7.3 AVERAGE SELLING PRICE TREND, BY TYPE

- 6.7.4 AVERAGE SELLING PRICE TREND, BY REGION

- 6.8 ECOSYSTEM ANALYSIS

- 6.8.1 DEMAND SIDE

- 6.8.2 SUPPLY SIDE

- 6.9 TRENDS/DISRUPTIONS IMPACTING BUYERS

- 6.10 PATENT ANALYSIS

- 6.10.1 LIST OF MAJOR PATENTS

- 6.11 KEY CONFERENCES AND EVENTS

- 6.12 TARIFF AND REGULATORY LANDSCAPE

- 6.12.1 TARIFF RELATED TO FEED ADDITIVES

- 6.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12.3 REGULATIONS

- 6.12.3.1 Feed additives regulatory approval from European Union

- 6.12.3.2 Time duration for specialty feed additives in register

- 6.12.3.3 Registration of specialty feed additives

- 6.12.3.4 Packaging of specialty feed additives

- 6.12.3.5 Labeling of specialty feed additives

- 6.12.3.6 Manufacture and sale of specialty feed additives

- 6.12.3.7 Import of specialty feed additives

- 6.12.3.8 Revaluation of feed additives

- 6.12.4 REGULATORY FRAMEWORK, BY COUNTRY

- 6.12.4.1 US

- 6.12.4.1.1 Labeling

- 6.12.4.1.2 Association of American Feed Control Officials (AAFCO)

- 6.12.4.2 Canada

- 6.12.4.2.1 Legal authorities

- 6.12.4.3 China

- 6.12.4.4 European Union

- 6.12.4.5 Japan

- 6.12.4.6 South Africa

- 6.12.4.1 US

- 6.13 PORTER'S FIVE FORCES ANALYSIS

- 6.13.1 INTENSITY OF COMPETITIVE RIVALRY

- 6.13.2 BARGAINING POWER OF SUPPLIERS

- 6.13.3 BARGAINING POWER OF BUYERS

- 6.13.4 THREAT OF SUBSTITUTES

- 6.13.5 THREAT OF NEW ENTRANTS

- 6.14 KEY STAKEHOLDERS & BUYING CRITERIA

- 6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.14.2 BUYING CRITERIA

- 6.15 CASE STUDIES

- 6.15.1 ENHANCING POULTRY HEALTH WITH PHYTOGENIC FEED ADDITIVES BY KEMIN INDUSTRIES

- 6.15.2 PICHIA GUILLIERMONDII IN AQUAFEED BY ADM FOR BETTER IMMUNE SUPPORT IN SHRIMP

- 6.16 INVESTMENT & FUNDING SCENARIO

7 SPECIALTY FEED ADDITIVES MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 PHYTOGENICS

- 7.2.1 ROLE IN IMPROVEMENT OF GUT HEALTH AND HEALTHY DIGESTION IN ANIMAL FEED TO BOOST MARKET

- 7.2.2 ESSENTIAL OILS

- 7.2.3 FLAVONOIDS

- 7.2.4 SAPONINS

- 7.2.5 OLEORESINS

- 7.2.6 OTHER PHYTOGENICS

- 7.3 ORGANIC ACIDS

- 7.3.1 ROLE IN CONSISTENT FEED FORMULATIONS AND FEED PRESERVATION TO DRIVE MARKET

- 7.3.2 PROPIONIC ACID

- 7.3.3 FORMIC ACID

- 7.3.4 CITRIC ACID

- 7.3.5 LACTIC ACID

- 7.3.6 SORBIC ACID

- 7.3.7 MALIC ACID

- 7.3.8 BENZOIC ACID

- 7.3.9 OTHER ORGANIC ACIDS

- 7.4 MYCOTOXIN BINDERS & MODIFIERS

- 7.4.1 INCREASE IN AWARENESS REGARDING BENEFITS OF BINDERS TO DRIVE MARKET

- 7.4.2 BINDERS

- 7.4.3 MODIFIERS

- 7.5 ALGAE OMEGA-3

- 7.5.1 ALGAE OMEGA-3 TO GAIN TRACTION AS SUSTAINABLE FEED ADDITIVE ACROSS ANIMAL NUTRITION SECTORS

- 7.6 PELLET BINDERS

- 7.6.1 PELLET BINDERS SUPPORT NUTRITIONAL STABILITY WHILE MEETING DURABILITY DEMANDS

- 7.7 PROBIOTICS

- 7.7.1 POTENTIAL TO REPLACE ANTIBIOTIC GROWTH PROMOTERS TO DRIVE MARKET

- 7.7.2 BACTERIA

- 7.7.3 YEAST & FUNGI

- 7.8 ANTIOXIDANTS

- 7.8.1 ROLE IN PROTECTION OF FAT-SOLUBLE VITAMINS AGAINST OXIDATIVE DEGRADATION TO DRIVE MARKET

- 7.8.2 SYNTHETIC ANTIOXIDANTS

- 7.8.3 NATURAL ANTIOXIDANTS

- 7.9 WATER DISINFECTANTS

- 7.9.1 RISING THREATS FROM CONTAMINATED WATER TO BOOST DEMAND FOR EFFECTIVE DISINFECTANTS

- 7.10 FLAVORS & SWEETENERS

- 7.10.1 ROLE OF SWEETENERS TO MASK UNDESIRED TASTE OF FEED TO DRIVE MARKET

- 7.10.2 FEED FLAVORS

- 7.10.3 FEED SWEETENERS

8 SPECIALTY FEED ADDITIVES MARKET, BY LIVESTOCK

- 8.1 INTRODUCTION

- 8.2 POULTRY

- 8.2.1 RISE IN DEMAND FOR HIGH-QUALITY CHICKEN AND EGGS TO DRIVE MARKET

- 8.2.2 BROILERS

- 8.2.3 LAYERS

- 8.2.4 BREEDERS

- 8.3 RUMINANTS

- 8.3.1 INCREASE IN CONSUMPTION OF DAIRY PRODUCTS AND BEEF TO DRIVE DEMAND

- 8.3.2 DAIRY CATTLE

- 8.3.3 BEEF CATTLE

- 8.3.4 SHEEP & GOATS

- 8.4 SWINE

- 8.4.1 RISE IN PORK TRADE AND CONCERNS OVER MEAT SAFETY TO BOOST MARKET

- 8.4.2 STARTERS

- 8.4.3 GROWERS

- 8.4.4 SOWS

- 8.5 AQUATIC ANIMALS

- 8.5.1 INCREASE IN HIGH-QUALITY AQUAFEED PRODUCTION TO DRIVE MARKET

- 8.5.2 FISH

- 8.5.3 CRUSTACEANS

- 8.5.4 MOLLUSKS

- 8.5.5 OTHER AQUATIC ANIMALS

- 8.6 COMPANION ANIMALS

9 SPECIALTY FEED ADDITIVES MARKET, BY SOURCE

- 9.1 INTRODUCTION

- 9.2 SYNTHETIC

- 9.2.1 COST-EFFECTIVENESS AND HIGH STABILITY PROPERTIES TO PROPEL GROWTH

- 9.3 NATURAL

- 9.3.1 NEED FOR ALTERNATIVES TO ANTIBIOTICS AND CHEMICAL BINDERS TO DRIVE MARKET

10 SPECIALTY FEED ADDITIVES MARKET, BY FORM

- 10.1 INTRODUCTION

- 10.2 DRY

- 10.2.1 CONVENIENCE IN STORAGE, HANDLING, AND TRANSPORTATION TO DRIVE MARKET

- 10.3 LIQUID

- 10.3.1 UNIFORM MIXING AND PRECISE DOSING OF LIQUID FEED ADDITIVES TO PROPEL MARKET

11 SPECIALTY FEED ADDITIVES MARKET, BY FUNCTION

- 11.1 INTRODUCTION

- 11.2 GUT HEALTH & DIGESTIVE PERFORMANCE

- 11.2.1 INCREASED DEMAND FOR HEALTHY GUT MICROBIOTA TO IMPROVE DIGESTION AND PREVENT GASTROINTESTINAL DISEASES

- 11.3 MYCOTOXIN MANAGEMENT

- 11.3.1 INCREASE IN CONCERNS OVER FEED SAFETY, ANIMAL HEALTH, AND PRODUCTIVITY LOSSES TO DRIVE DEMAND FOR MYCOTOXIN MANAGEMENT FUNCTIONS

- 11.4 PALATABILITY ENHANCERS

- 11.4.1 IMPROVED TASTE, SMELL, AND OVERALL APPEAL OF ANIMAL FEED TO DRIVE DEMAND

- 11.5 PRESERVATION OF FUNCTIONAL INGREDIENTS

- 11.5.1 EFFECTIVE PRESERVATION ENHANCES OVERALL FEED QUALITY, SUPPORTING BETTER ANIMAL HEALTH AND PRODUCTIVITY

- 11.6 OTHER FUNCTIONS

12 SPECIALTY FEED ADDITIVES, BY MANUFACTURING TECHNOLOGY

- 12.1 INTRODUCTION

- 12.2 FERMENTATION

- 12.3 EXTRACTION & PURIFICATION

- 12.4 MICROENCAPSULATION/COATING

- 12.5 GRANULATION & DRYING

- 12.6 OTHER MANUFACTURING TECHNOLOGIES

13 SPECIALTY FEED ADDITIVES MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Investments by companies like Kemin and IFF in innovative feed solutions reflect growing demand for specialty feed additives

- 13.2.2 CANADA

- 13.2.2.1 Increased production of poultry products to boost market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Increased production of animal-based food while strengthening biosecurity to fuel demand

- 13.3.2 UK

- 13.3.2.1 Rise in horse-riding to require targeted nutritional additives for efficiency

- 13.3.3 FRANCE

- 13.3.3.1 Increase in investments in livestock sector to fuel market growth

- 13.3.4 ITALY

- 13.3.4.1 Focus on improving animal health and nutrition to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Growth in caged poultry sector to boost demand for nutritious feed additives

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Strategic partnerships between key players in market to show rising demand

- 13.4.2 INDIA

- 13.4.2.1 Rising dairy & poultry supported by key players' initiatives to support market growth

- 13.4.3 JAPAN

- 13.4.3.1 Increasing consumer demand for premium animal-based products to drive market

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Rise in demand for poultry meat to drive market

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Growing pet culture in country to augment demand

- 13.4.6 INDONESIA

- 13.4.6.1 High demand for feed due to growing poultry sector to drive market

- 13.4.7 THAILAND

- 13.4.7.1 Expansion of poultry meat export sector to drive market

- 13.4.8 VIETNAM

- 13.4.8.1 Goal to meet domestic feed demand by 2030 to support use of natural and functional additives

- 13.4.9 MALAYSIA

- 13.4.9.1 Rise in demand for animal meat to fuel market growth

- 13.4.10 PHILIPPINES

- 13.4.10.1 Key players launching new products to showcase market demand

- 13.4.11 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Increase in livestock population and export opportunities to fuel market growth

- 13.5.2 ARGENTINA

- 13.5.2.1 Export pork opportunity to drive market

- 13.5.3 MEXICO

- 13.5.3.1 Expansions by key players in country to exhibit market demand

- 13.5.4 COLOMBIA

- 13.5.4.1 Rise in per capita pork consumption to emphasize need for quality feed to support higher production levels

- 13.5.5 VENEZUELA

- 13.5.5.1 Poultry production's more than doubling since 2018 to signal rise in demand for advanced feed additives

- 13.5.6 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD (ROW)

- 13.6.1 AFRICA

- 13.6.1.1 Rise in disease incidences and growth of poultry sector to drive demand

- 13.6.1.2 South Africa

- 13.6.1.2.1 Preventive animal health strategies to increase reliance on functional feed additives

- 13.6.1.3 Egypt

- 13.6.1.3.1 Shift toward sustainable production to accelerate adoption of innovative feed solutions

- 13.6.2 REST OF AFRICA

- 13.6.3 MIDDLE EAST

- 13.6.3.1 Growth in livestock population and demand for dairy products to drive market

- 13.6.3.2 Turkiye

- 13.6.3.2.1 Disease threats like avian influenza to push producers toward immunity-boosting nutritional strategies

- 13.6.3.3 Israel

- 13.6.3.3.1 Advanced dairy genetics and intensive herd management to increase reliance on nutritional optimization tools

- 13.6.3.4 Iraq

- 13.6.3.4.1 Government support for domestic livestock producers to drive market demand

- 13.6.3.5 Rest of Middle East

- 13.6.1 AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.4.1 MARKET RANKING ANALYSIS

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 EV/EBITDA

- 14.6 BRAND COMPARISON ANALYSIS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Regional footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Livestock footprint

- 14.7.5.5 Form footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO AND TRENDS

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 CARGILL, INCORPORATED

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Services/Solutions offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 ARCHER DANIELS MIDLAND (ADM) COMPANY

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Services/Solutions offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 INTERNATIONAL FLAVORS & FRAGRANCES INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Services/Solutions offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 EVONIK INDUSTRIES AG

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Services/Solutions offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 BASF SE

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent development

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 NOVONESIS GROUP

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.4 MnM view

- 15.1.7 NUTRECO

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.7.3.2 Expansions

- 15.1.7.4 MnM view

- 15.1.8 LALLEMAND INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.4 MnM view

- 15.1.9 BENTOLI

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.4 MnM view

- 15.1.10 ALLTECH

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.4 MnM view

- 15.1.11 PETROLIAM NASIONAL BERHAD (PETRONAS)

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches

- 15.1.11.4 MnM view

- 15.1.12 ADISSEO

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Expansions

- 15.1.12.4 MnM view

- 15.1.13 KEMIN INDUSTRIES, INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Deals

- 15.1.13.3.3 Expansions

- 15.1.13.4 MnM view

- 15.1.14 LAND O'LAKES, INC.

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 MnM view

- 15.1.15 NOVUS INTERNATIONAL, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches

- 15.1.15.3.2 Deals

- 15.1.15.3.3 Other developments

- 15.1.15.4 MnM view

- 15.1.1 CARGILL, INCORPORATED

- 15.2 OTHER PLAYERS

- 15.2.1 NEOSPARK DRUGS AND CHEMICALS PRIVATE LIMITED

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.4 MnM view

- 15.2.2 GLOBAL NUTRITION INTERNATIONAL

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.4 MnM view

- 15.2.3 VOLAC INTERNATIONAL LTD.

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Expansions

- 15.2.3.3.2 Other developments

- 15.2.3.4 MnM view

- 15.2.4 NUTREX

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.4 MnM view

- 15.2.5 IMPEXTRACO NV

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.4 MnM view

- 15.2.6 INNOVAD

- 15.2.7 TEX BIOSCIENCES (P) LTD.

- 15.2.8 CENTAFARM SRL

- 15.2.9 NUQO FEED ADDITIVES

- 15.2.10 PALITAL FEED ADDITIVES B.V.

- 15.2.1 NEOSPARK DRUGS AND CHEMICALS PRIVATE LIMITED

16 ADJACENT AND RELATED MARKETS

- 16.1 INTRODUCTION

- 16.2 LIMITATIONS

- 16.3 FEED ADDITIVES MARKET

- 16.3.1 MARKET DEFINITION

- 16.3.2 MARKET OVERVIEW

- 16.4 COMPOUND FEED MARKET

- 16.4.1 MARKET DEFINITION

- 16.4.2 MARKET OVERVIEW

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS