|

시장보고서

상품코드

1972230

사료 첨가제 시장 : 유형별, 기능별, 최종사용자별, 축종별, 유래별, 형태별, 지역별 - 세계 예측(-2031년)Feed Additives Market by Type (Amino Acids, Phosphates, Vitamins, Acidifiers, Carotenoids, Enzymes, Antioxidants, Antibiotics, Phytogenics, Probiotics, and Others), Source, Form, Livestock, End Users, Function, and Region - Global Forecast to 2031 |

||||||

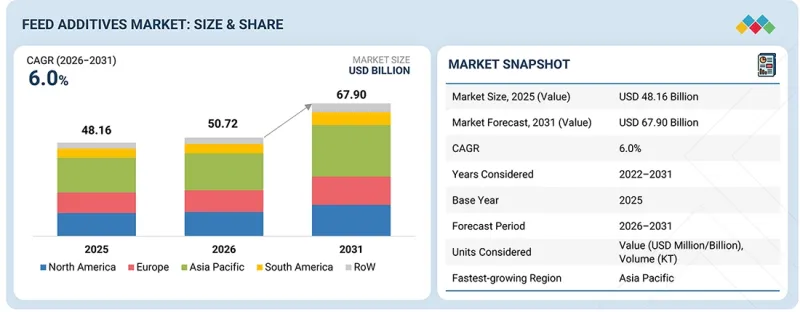

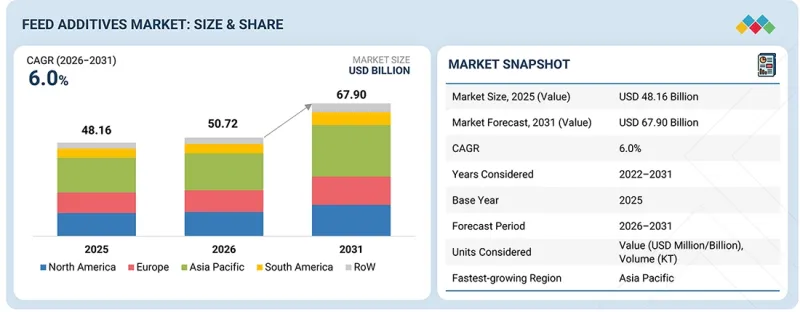

세계의 사료 첨가제 시장 규모는 2026년에 507억 2,000만 달러로 추정되며, 2026년부터 2031년까지 CAGR 6.0%를 기록하며 2031년까지 679억 달러에 달할 것으로 예측됩니다.

이 시장은 고품질 동물성 단백질에 대한 수요 증가, 동물 영양 최적화에 대한 인식 증가, 축산 항생제 사용 규제 강화 등을 배경으로 꾸준히 성장하고 있습니다. 아미노산, 효소, 프로바이오틱스, 비타민, 미네랄, 항산화제, 마이코톡신 흡착제 등의 사료 첨가제는 사료요구율 향상, 장내 환경 개선, 면역력 강화 및 동물의 종합적인 생산성 극대화에 중요한 역할을 하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 가치(100만/10억 달러) 및 수량(천 톤) |

| 부문 | 유형별, 기능별, 최종사용자별, 축종별, 유래별, 형태별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

또한, 특히 신흥 경제국에서 축산 및 양식 부문의 급속한 산업화로 인해 과학적으로 배합된 사료 솔루션의 채택이 가속화되고 있습니다. 정밀 영양학의 발전, 맞춤형 프리믹스 배합, 메탄 배출량 감소 및 지속가능성 향상을 위한 기능성 첨가제 개발은 시장 성장 전망을 더욱 강화시키고 있습니다.

그러나 원재료 가격의 변동성, 지역별 규제의 복잡성, 첨가제의 안전성 및 환경 영향에 대한 감시 강화는 시장 확대에 있어 두드러진 도전과제로 작용하고 있습니다. 신규 첨가제 개발에 따른 높은 연구개발 비용과 천연 및 비GMO 원료로의 전환도 제조업체의 부담으로 작용하고 있습니다. 이러한 제약에도 불구하고, 통합 축산 사업에 대한 투자 증가, 수산 사료 및 반려동물 사료 산업의 확대, 무항생제 및 기능성 사료 솔루션의 증가 추세는 큰 성장 기회를 창출할 것으로 예상됩니다. 또한, 마이크로캡슐화 기술, 식물성 첨가제, 정밀 사료 공급 시스템의 혁신은 제품 효과를 높일 가능성이 높으며, 이를 통해 사료 첨가제 제조업체는 진화하는 세계 시장에서 더욱 견고한 기반을 구축할 수 있습니다.

Kemin Industries, Inc.(미국)의 연구 결과에 따르면, 아미노산은 동물의 성장, 건강, 성능에 필수적입니다. 이들은 단백질의 구성 성분으로 주요 신체 기능을 지탱하는 역할을 합니다. 동물이 건강하게 성장하고 건강을 유지하기 위해서는 사료에 필수 아미노산이 적절한 수준과 균형으로 포함되어야 합니다. 동물의 단백질 생산은 체내에서 특정 아미노산의 이용 가능 여부에 따라 달라집니다. 사료에 필수 아미노산이 하나라도 부족하면 동물은 성장, 회복, 정상 기능에 필요한 특정 단백질을 생산할 수 없습니다. 필수 아미노산은 체내에서 충분한 양을 생산할 수 없기 때문에 사료를 통해 공급받아야 합니다. 여기에는 페닐알라닌, 발린, 트레오닌, 트립토판, 이소류신, 메티오닌, 히스티딘, 아르기닌(경우에 따라), 류신, 라이신 등이 포함됩니다.

현대의 축산 시스템에서는 사료 비용이 높고 생산 목표도 엄격합니다. 리신, 메티오닌, 트레오닌, 트립토판 등의 아미노산을 첨가하여 조단백질 수준을 낮추어도 생산 성과에 영향을 미치지 않습니다. 이는 사료요구율을 개선하고, 성장을 촉진하며, 질소 폐기물을 감소시킵니다. 이러한 뚜렷한 생산성 및 비용 이점이 세계 사료 첨가제 시장에서 아미노산 유형의 성장을 강력하게 견인하고 있습니다.

Alltech의 '농식품 전망 2025'에 따르면 육계용 사료 생산량은 3억 8,540만 톤(4억 2,480만 톤), 산란계용은 1억 7,300만 톤(1억 9,070만 톤)으로 증가하였습니다. 육계 사료는 가장 큰 부문이며, 전 세계 사료 총량의 27.6%를 차지합니다. 육계 고기는 여전히 저렴한 단백질 공급원으로서 아시아태평양 및 라틴아메리카의 수요를 뒷받침하고 있습니다. 고병원성 조류인플루엔자(HPAI) 문제에도 불구하고 저렴한 가격과 수출 수요로 육계 생산량은 꾸준히 증가할 것으로 예상됩니다. 산란계 생산량은 1.4%로 성장률은 둔화되었으나, 아시아태평양, 라틴아메리카, 아프리카의 수요에 힘입어 플러스 성장을 유지했습니다. 이러한 가금류 사료의 꾸준한 증가는 사료 첨가제 시장을 직접적으로 뒷받침하고 있습니다. 가금류 양식은 높은 생산성 향상이 요구됩니다. 생산자들은 양떼를 보호하고 사료 효율을 유지하기 위해 아미노산, 효소, 비타민, 장 건강 제품에 의존하고 있습니다. 가금류 사료량이 증가함에 따라 사료 첨가제에 대한 수요도 크게 확대되고 있습니다. 이것이 가금류 부문이 사료 첨가제 시장에서 가장 큰 점유율을 차지하는 주요 이유입니다.

아시아태평양은 축산 및 양식업 규모가 크고, 동물성 단백질에 대한 수요가 빠르게 증가하고 있습니다. Alltech Agri Food Outlook 2025에 따르면, 아시아태평양은 세계 최대의 사료 생산지입니다. 이 지역이 선도적인 위치에 있는 배경에는 탄탄한 가금류, 양돈, 양식업 부문이 있습니다. 많은 인구와 소득 증가로 인해 저렴한 가격의 육류와 생선에 대한 수요가 증가하고 있습니다. 중국, 인도, 베트남, 인도네시아, 태국 등의 국가들은 이러한 수요를 충족시키기 위해 사료 생산을 지속적으로 확대하고 있습니다. 이들 시장의 대부분의 농장은 상업적이고 집약적인 시스템으로 운영되고 있습니다. 사료 생산량의 증가는 사료 첨가제의 사용량 증가를 의미합니다. 생산자들은 사료 이용 효율을 높이고 동물의 건강을 보호하기 위해 아미노산, 효소, 비타민, 미네랄, 장 건강 제품 등을 첨가하고 있습니다. 그들은 성장 촉진과 안정적인 생산량에 중점을 두고 있습니다. 아시아태평양의 축산 및 양식업이 지속적으로 성장함에 따라 아시아태평양은 예측 기간 동안 세계 사료 첨가제 시장에서 확고한 위치를 유지할 것으로 예상됩니다.

주요 기업으로는 Cargill, Incorporated(미국), ADM(미국), International Flavors & Fragrances Inc. Firmenich(스위스), Alltech(미국), Ajinomoto Co., Inc.(일본), Novonesis Group(덴마크), Adisseo(프랑스), Jubilant Ingrevia Ltd(인도), Nutreco(네덜란드), BRF Global(브라질), Volac International Ltd.(영국), Kemin Industries, Inc.(미국), Lallemand Inc.(캐나다), Bentoli(미국), Neospark Drugs and Chemicals Pvt.(인도), Novus International, Inc.(미국), Global Nutrition International(프랑스) 등이 있습니다.

조사 범위

본 조사 보고서는 사료 첨가제 시장을 유형별, 기능별, 최종사용자별, 축종별, 유래별, 형태별, 지역별로 분류하고 있습니다.

이 보고서의 조사 범위에는 사료 첨가제 산업의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 사료 첨가제 시장과 관련된 주요 업계 참가업체를 심층 분석하여 사업 내용, 서비스, 주요 전략, 계약, 제휴, 합의, 제품 출시, 인수합병, 최근 동향에 대한 인사이트를 제공합니다. 본 보고서는 사료첨가제 시장 생태계에서 신생 스타트업 기업의 경쟁적 인사이트도 제공합니다. 또한, 기술 분석, 생태계 및 시장 매핑, 특허 및 규제 현황 등 산업별 트렌드도 조사 대상입니다.

본 보고서 구매 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 사료 첨가제 시장과 그 하위 부문의 수익 수치에 대한 가장 근접한 추정치에 대한 정보를 제공합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 비즈니스를 더 잘 포지셔닝하고, 적절한 시장 진입 전략을 수립할 수 있는 추가 인사이트를 얻을 수 있습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 사료 첨가제 시장 성장에 영향을 미치는 주요 촉진요인(축산물 기반 제품에 대한 수요 및 소비 증가), 억제요인(각국의 항생제 금지), 기회(천연 성장 촉진제로의 전환), 과제(아시아 기업이 제조하는 유전자 변형 사료 첨가제 제품의 품질 관리) 분석

- 제품 개발/혁신 : 사료 첨가제 시장의 R&D 활동 및 신제품 출시에 대한 심층 분석

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보, 지역별 사료 첨가제 분석

- 시장 다각화 : 사료 첨가제 시장의 신제품 소스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보

- 경쟁력 평가 - Cargill, Incorporated(미국), ADM(미국), International Flavors & Fragrances Inc.(미국), Evonik Industries AG(독일), BASF SE(독일), DSM-Firmenich(스위스), Alltech(미국), Ajinomoto Co., Inc.(일본), Novonesis Group(덴마크), Adisseo(프랑스), Jubilant Ingrevia Ltd(인도), Nutreco(네덜란드), BRF Global(브라질), Volac International Ltd.(영국), Volac International Ltd.(영국), Kemin Industries, Inc.(미국), Lallemand Inc.(캐나다), Bentoli(미국), Neospark Drugs and Chemicals Pvt. International, Inc.(미국), Global Nutrition International(프랑스) 및 기타 사료 첨가제 시장의 주요 기업들

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 사료 첨가제 시장(유형별)

제10장 사료 첨가제 시장(기능별)

제11장 사료 첨가제 시장(최종사용자별)

제12장 사료 첨가제 시장(축종별)

제13장 사료 첨가제 시장(유래별)

제14장 사료 첨가제 시장(형태별)

제15장 사료 첨가제 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 인접 시장과 관련 시장

제20장 부록

KSM 26.03.30The global feed additives market is estimated at USD 50.72 billion in 2026 and is projected to reach USD 67.90 billion by 2031, at a CAGR of 6.0% between 2026 and 2031. The market is witnessing steady expansion, driven by increasing demand for high-quality animal protein, growing awareness regarding animal nutrition optimization, and stricter regulations on antibiotic usage in livestock production. Feed additives, including amino acids, enzymes, probiotics, vitamins, minerals, antioxidants, and mycotoxin binders, play a critical role in enhancing feed conversion ratios, improving gut health, boosting immunity, and maximizing overall animal performance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) and Volume (KT) |

| Segments | By Type, livestock, source, form, function, end user, and region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Rest of the World (RoW) |

Additionally, rapid industrialization of livestock and aquaculture sectors, particularly in emerging economies, is accelerating the adoption of scientifically formulated feed solutions. Advancements in precision nutrition, customized premix formulations, and functional additives aimed at reducing methane emissions and improving sustainability are further strengthening market growth prospects.

However, vVolatility in raw material prices, regulatory complexities across regions, and increasing scrutiny over additive safety and environmental impact pose notable challenges to market expansion. High R&D costs associated with novel additive development and the shift toward natural and non-GMO ingredients also add pressure on manufacturers. Despite these constraints, rising investments in integrated livestock operations, expansion of aquafeed and pet food industries, and the growing trend toward antibiotic-free and performance-enhancing feed solutions are expected to create substantial growth opportunities. Furthermore, innovations in microencapsulation technologies, phytogenic additives, and precision feeding systems are likely to enhance product efficacy, thereby enabling feed additive manufacturers to secure a stronger foothold in the evolving global market.

"Amino Aacids type of feed additives isare expected projected to hold account for a dominant market share during the forecast period."

According to insights by Kemin Industries, Inc. (US), amino acids are essential for animal growth, health, and performance. They are the building blocks of protein and support key body functions. Animals need the right proper levels and balance of essential amino acids in their feed to grow well and stay healthy. An animal's protein production depends on the availability of specific amino acids in the body. If even one essential amino acid is lacking in the diet, the animal cannot produce certain specific proteins needed for growth, repair, and normal functions. Essential amino acids must be supplied through feed because the body cannot produce them in adequate amounts. These include phenylalanine, valine, threonine, tryptophan, isoleucine, methionine, histidine, arginine (in some cases), leucine, and lysine..

In modern livestock systems, feed cost is high, and performance targets are strict. Adding amino acids like lysine, methionine, threonine, and tryptophan helps produce lower crude protein levels without affecting results. This improves feed conversion, supports better growth, and reduces nitrogen waste. These clear performance and cost benefits are strongly driving the growth of the amino acids type within the global feed additives market.

"Among livestock, poultry is estimated to hold a strong market share in the feed additives market."

As per the Alltech Agri Food Outlook 2025, poultry feed output increased for broilers to 385.4 million metric tons (424.8 million tons) and for layers to 173.0 million metric tons (190.7 million tons). Broiler feed is the largest segment and holds 27.6% of total global feed volume. Broiler meat remains a low-cost protein option, which supports demand in Asia Pacific and Latin America. Even with highly pathogenic avian influenza (HPAI) issues, broiler volumes are expected to see steady growth due to affordability and export demand. Layer growth stayed positive despite a slower 1.4% rise, supported by demand in Asia Pacific, Latin America, and Africa. This steady rise in poultry feed directly supports the feed additives market. Poultry farming is highly performance-driven. Producers depend on amino acids, enzymes, vitamins, and gut health products to protect flocks and maintain feed efficiency. As poultry feed volumes grow, there is a significant growth in demand for feed additives. This is a key reason the poultry segment holds the highest share in the feed additives market.

"Asia Pacific is set to lead the global feed additives market during the forecast period."

Asia Pacific has a large livestock and aquaculture sector with fast-growing demand for animal protein. According to the Alltech Agri Food Outlook 2025, Asia Pacific remained the largest feed producer in the world. The region leads because it has strong poultry, swine, and aquaculture sectors. Large populations and rising incomes increase demand for affordable meat and fish. Countries such as China, India, Vietnam, Indonesia, and Thailand continue to expand feed production to meet this demand. Most farms in these markets run on commercial and intensive systems. Higher feed production means higher use of feed additives. Producers add amino acids, enzymes, vitamins, minerals, and gut health products to improve feed use and protect animal health. They focus on better growth and steady output. As livestock and aquaculture continue to grow in the Asia Pacific, the region keeps its strong position in the global feed additives market during the forecast period.

- By Company Type: Tier 1 - 30%, Tier 2 - 25%, and Tier 3 - 45%

- By Designation: CXOs - 25%, Managers - 35%, Others - 40%

- By Region: North America - 20%, Europe - 30%, Asia Pacific - 35%, South America - 10%, and Rest of the World - 5%

Prominent companies in the market include Cargill, Incorporated (US), ADM (US), International Flavors & Fragrances Inc. (US), Evonik Industries AG (Germany), BASF SE (Germany), DSM-Firmenich (Switzerland), Alltech (US), Ajinomoto Co., Inc. (Japan), Novonesis Group (Denmark), Adisseo (France), Jubilant Ingrevia Ltd (India), Nutreco (Netherlands), BRF Global (Brazil), Volac International Ltd. (England), Kemin Industries, Inc. (US), Lallemand Inc. (Canada), Bentoli (US), Neospark Drugs and Chemicals Pvt. Ltd. (India), Novus International, Inc. (US), and Global Nutrition International (France).

Research Coverage

This research report categorizes the feed additives market by type (amino acids, phosphates, vitamins, acidifiers, carotenoids, enzymes, mycotoxin detoxifiers, flavors and sweeteners, antibiotics, minerals, antioxidants, nonprotein nitrogen, phytogenic, preservatives, and probiotics), by livestock (poultry, ruminants, swine, aquatic animals, and other livestock), by form (dry and liquid), by source (natural and synthetic), by function (qualitative) (gut health, palatability enhancers, growth boosters, immune system support, feed efficiency improvement, other functions), by end user (commercial feed manufacturers, integrated livestock and poultry production companies, aquafeed manufacturing industry, pet food manufacturing industry, feed premix manufacturing facility, large commercial farms [on farm feed mixing]) and region (North America, Europe, Asia Pacific, South America, and Rest of the World).

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the Feed Additives industry. A thorough analysis of the key industry players has been done to provide insights into their business, services, key strategies, contracts, partnerships, agreements, product launches, mergers & acquisitions, and recent developments associated with the Feed Additives market. This report provides a competitive analysis of emerging startups in the Feed Additives market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem & market mapping, and patent & regulatory landscape, among others.

Reasons to Buy This Report

The report provides market leaders/new entrants with information on the closest approximations of revenue numbers for the overall feed additives and their subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (increase in demand and consumption of livestock-based products), restraints (ban on antibiotics in different nations), opportunities (shift toward natural growth promoters), and challenges (quality control of genetic feed additive products manufactured by Asian companies) influencing the growth of the feed additives market

- Product Development/Innovation: Detailed insights into research & development activities and new product launches in the feed additives market

- Market Development: Comprehensive information about lucrative markets, analysis of feed additives across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the feed additives market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as Cargill, Incorporated (US), ADM (US), International Flavors & Fragrances Inc. (US), Evonik Industries AG (Germany), BASF SE (Germany), DSM-Firmenich (Switzerland), Alltech (US), Ajinomoto Co., Inc. (Japan), Novonesis Group (Denmark), Adisseo (France), Jubilant Ingrevia Ltd (India), Nutreco (Netherlands), BRF Global (Brazil), Volac International Ltd. (UK), Kemin Industries, Inc. (US), Lallemand Inc. (Canada), Bentoli (US), Neospark Drugs and Chemicals Pvt. Ltd. (India), Novus International, Inc. (US), Global Nutrition International (France) and other players in the feed additive market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED

- 1.3.2 REGIONAL SCOPE

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.3.4 YEARS CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.3.5.1 Currency/value unit

- 1.3.5.2 Volume unit

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN FEED ADDITIVES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FEED ADDITIVES MARKET

- 3.2 FEED ADDITIVES MARKET, BY TYPE AND REGION

- 3.3 FEED ADDITIVES MARKET: TOP THREE TYPES

- 3.4 FEED ADDITIVES MARKET, BY LIVESTOCK

- 3.5 FEED ADDITIVES MARKET, BY FORM

- 3.6 FEED ADDITIVES MARKET, BY SOURCE

- 3.7 FEED ADDITIVES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increase in demand and consumption of livestock-based products

- 4.2.1.2 Growth in feed production

- 4.2.1.3 Rise in awareness about feed quality

- 4.2.1.4 Standardization of meat products owing to disease outbreaks

- 4.2.1.5 Implementation of innovative animal husbandry practices to improve meat quality

- 4.2.2 RESTRAINTS

- 4.2.2.1 Ban on antibiotics in different nations

- 4.2.2.2 Volatile raw material prices

- 4.2.2.3 Stringent regulatory framework

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Shift toward natural growth promoters

- 4.2.3.2 Increase in demand for nutritional supplements for monogastric animals

- 4.2.3.3 Growth of precision livestock farming driving demand for advanced feed additives

- 4.2.3.4 Growing demand for natural and clean-label feed additives

- 4.2.4 CHALLENGES

- 4.2.4.1 Quality control of genetic feed additive products manufactured by Asian companies

- 4.2.4.2 Sustainability of feed and livestock chain

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN FEED ADDITIVES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GROWTH OPPORTUNITIES IN DEVELOPING REGIONS

- 5.2.3 KEY ECONOMIC AND SECTORAL FORCES INFLUENCING GLOBAL FEED ADDITIVES MARKET IN 2025

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH AND PRODUCT DEVELOPMENT

- 5.3.2 RAW MATERIAL SOURCING

- 5.3.3 PRODUCTION

- 5.3.4 QUALITY CONTROL & SAFETY

- 5.3.5 DISTRIBUTION & LOGISTICS

- 5.3.6 MARKETING & SALES

- 5.3.7 END USERS

- 5.4 ECOSYSTEM ANALYSIS/MARKET MAP

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 INTRODUCTION

- 5.5.2 INDICATIVE PRICE TREND AMONG MARKET PLAYERS

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO OF HS CODE 230990

- 5.6.2 EXPORT SCENARIO OF HS CODE 230990

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING BUYERS

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 EVONIK VLAND BIOTECH JOINT VENTURE STRENGTHENS GUT HEALTH SOLUTIONS IN CHINA

- 5.10.2 DSM-FIRMENICH STRENGTHENS MYCOTOXIN RISK MANAGEMENT WITH NEW FEED ADDITIVE PLANT IN INDIA

- 5.10.3 ADM AQUATRAX (PICHIA GUILLIERMONDII) ENHANCES IMMUNE RESPONSE AND GROWTH PERFORMANCE IN SHRIMP

- 5.10.4 CARGILL ACQUIRES DELACON TO LEAD GLOBAL PHYTOGENIC FEED ADDITIVES MARKET

- 5.11 IMPACT OF 2025 US TARIFF - FEED ADDITIVES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END USE INDUSTRIES

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Fermentation & bioprocessing

- 6.1.1.2 Chemical synthesis

- 6.1.1.3 Premix blending technology

- 6.1.1.4 Microencapsulation technology for feed

- 6.1.2 COMPLEMENTARY TECHNOLOGY

- 6.1.2.1 Feed pelleting technology

- 6.1.2.2 Precision & micro-dosing systems

- 6.1.2.3 Animal health monitoring systems

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Precision nutrition

- 6.1.3.2 Extrusion processing technology

- 6.1.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.1.4.1 Short-term | Foundation & early commercialization

- 6.1.4.2 Mid-term | Expansion & standardization

- 6.1.4.3 Long-term | Precision nutrition

- 6.1.1 KEY TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.3 FUTURE APPLICATIONS

- 6.3.1 ASPARAGOPSIS SEAWEED-BASED METHANE REDUCTION ADDITIVE BY FUTUREFEED (CSIRO)

- 6.3.2 NANO-MINERALS AS NEXT-GENERATION SOLUTION FOR SUSTAINABLE POULTRY NUTRITION

- 6.3.3 HIGH-DOSE (SUPER-DOSING) PHYTASE FOR ENHANCED NUTRIENT UTILIZATION IN POULTRY

- 6.3.4 OPTIMIZING NITROGEN EFFICIENCY IN DAIRY COWS THROUGH RUMEN-PROTECTED ESSENTIAL AMINO ACID SUPPLEMENTATION

- 6.3.5 PHYTOGENIC ADDITIVES AND ORGANIC ACIDS AS ANTIBIOTIC ALTERNATIVES IN BROILER PRODUCTION

- 6.4 IMPACT OF GENERATIVE AI ON FEED ADDITIVES MARKET

- 6.4.1 INTRODUCTION

- 6.4.2 TOP USE CASES AND MARKET POTENTIAL

- 6.4.3 BEST PRACTICES IN FEED ADDITIVES

- 6.4.4 CASE STUDIES OF AI IMPLEMENTATION IN FEED ADDITIVES MARKET

- 6.4.5 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.6 CLIENTS' READINESS TO ADOPT GENERATIVE AI FEED ADDITIVES

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 LABELING REQUIREMENTS AND CLAIMS

- 7.1.4 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.4.1 Mandatory validation of efficacy, safety & environmental impact

- 7.1.4.2 Global harmonization of feed additive classifications & approval pathways

- 7.1.4.3 Strengthened contaminant, residue & antimicrobial control regulations

- 7.1.4.4 Digital labeling, traceability & supply chain transparency

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABLE SOURCING

- 7.2.2 CARBON FOOTPRINT REDUCTION INITIATIVES

- 7.2.3 CIRCULAR ECONOMY APPROACHES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS APPLICATION INDUSTRIES ACROSS SUPPLY CHAIN

- 8.5 MARKET PROFITABILITY

- 8.6 REVENUE POTENTIAL

- 8.6.1 COST DYNAMICS

- 8.6.2 MARGIN OPPORTUNITIES, BY TYPE

9 FEED ADDITIVES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 AMINO ACIDS

- 9.2.1 METHIONINE

- 9.2.1.1 Ability to tailor amino acid supplements for livestock to drive market

- 9.2.2 LYSINE

- 9.2.2.1 Relatively high value and digestibility of lysine to boost market

- 9.2.3 THREONINE

- 9.2.3.1 Role in providing optimal protein synthesis to boost market

- 9.2.4 TRYPTOPHAN

- 9.2.4.1 Ability to improve protein utilization and stress reduction in livestock to drive market

- 9.2.5 OTHER AMINO ACIDS

- 9.2.1 METHIONINE

- 9.3 PHOSPHATES

- 9.3.1 DICALCIUM PHOSPHATE

- 9.3.1.1 Role in regulating energy metabolism and maintaining adequate dietary levels for livestock to drive market

- 9.3.2 MONOCALCIUM PHOSPHATE

- 9.3.2.1 Ability to prevent abnormal development of bones in livestock to propel market

- 9.3.3 MON0-DICALCIUM PHOSPHATE

- 9.3.3.1 Enhancement of functioning of immune system to drive market

- 9.3.4 DEFLUORINATED PHOSPHATE

- 9.3.4.1 Role in reducing fluorine content in animal feed to boost market

- 9.3.5 TRICALCIUM PHOSPHATE

- 9.3.5.1 Role in enhancement of immune system and energy regulation of livestock to drive market

- 9.3.6 OTHER PHOSPHATES

- 9.3.1 DICALCIUM PHOSPHATE

- 9.4 VITAMINS

- 9.4.1 FAT-SOLUBLE VITAMINS

- 9.4.1.1 Role of vitamins as key constituent of metabolic functions to drive market

- 9.4.2 WATER-SOLUBLE VITAMINS

- 9.4.2.1 Significance of water-soluble vitamins for optimum growth and development of livestock to drive market

- 9.4.1 FAT-SOLUBLE VITAMINS

- 9.5 ACIDIFIERS

- 9.5.1 PROPIONIC ACID

- 9.5.1.1 Role in silage production and prevention of fertility disorders in livestock to drive market

- 9.5.2 FORMIC ACID

- 9.5.2.1 Role in consistent feed formulations and feed preservation to drive market

- 9.5.3 CITRIC ACID

- 9.5.3.1 Importance of citric acid in enhancing immunity of vaccinated broilers to boost market

- 9.5.4 LACTIC ACID

- 9.5.4.1 Significance of lactic acid in improving animal health and productivity to drive market

- 9.5.5 SORBIC ACID

- 9.5.5.1 Importance of sorbic acid in feed preservation to drive market

- 9.5.6 MALIC ACID

- 9.5.6.1 Role as cost-efficient preservative and acidity regulator to drive market

- 9.5.7 BENZOIC ACID

- 9.5.7.1 Strong antimicrobial properties and low pungency to drive market

- 9.5.8 OTHER ACIDIFIERS

- 9.5.1 PROPIONIC ACID

- 9.6 CAROTENOIDS

- 9.6.1 ASTAXANTHIN

- 9.6.1.1 Health benefits of astaxanthin to fuel market growth

- 9.6.2 CANTHAXANTHIN

- 9.6.2.1 Role of canthaxanthin in providing consistent egg color to boost market

- 9.6.3 LUTEIN

- 9.6.3.1 Health benefits of lutein and improvement of feed palatability to drive market

- 9.6.4 BETA CAROTENE

- 9.6.4.1 Improvement of reproductive performance of ruminants and protection against oxidative stress to accelerate market growth

- 9.6.5 OTHER CAROTENOIDS

- 9.6.1 ASTAXANTHIN

- 9.7 ENZYMES

- 9.7.1 PHYTASE

- 9.7.1.1 Low cost and nutritional benefits to boost growth

- 9.7.2 CARBOHYDRASE

- 9.7.2.1 Significance in improvement of digestibility of carbohydrates in feed ingredients to drive market

- 9.7.3 PROTEASE

- 9.7.3.1 Role in reduction of dietary protein levels of livestock to drive market

- 9.7.4 OTHER ENZYMES

- 9.7.1 PHYTASE

- 9.8 MYCOTOXIN DETOXIFIERS

- 9.8.1 BINDERS

- 9.8.1.1 Increase in awareness regarding benefits of binders to drive market

- 9.8.2 MODIFIERS

- 9.8.2.1 Enhancement of feed by conversion of mycotoxin into less toxic compounds to drive market

- 9.8.1 BINDERS

- 9.9 FLAVORS & SWEETENERS

- 9.9.1 FEED FLAVORS

- 9.9.1.1 Rise in focus on improving livestock performance to drive market

- 9.9.2 FEED SWEETENERS

- 9.9.2.1 Role of sweeteners to mask undesired taste of feed to drive market

- 9.9.1 FEED FLAVORS

- 9.10 ANTIBIOTICS

- 9.10.1 TETRACYCLINE

- 9.10.1.1 Role in improvement of egg production and feed efficiency to drive market

- 9.10.2 PENICILLIN

- 9.10.2.1 Significance of penicillin as antibiotic to drive market

- 9.10.3 OTHER ANTIBIOTICS

- 9.10.1 TETRACYCLINE

- 9.11 MINERALS

- 9.11.1 POTASSIUM

- 9.11.1.1 Regulation of metabolism of proteins and carbohydrates to boost market

- 9.11.2 CALCIUM

- 9.11.2.1 Role of calcium in strengthening bones and improving eggshell quality to drive market

- 9.11.3 PHOSPHORUS

- 9.11.3.1 Vital role of phosphorus in egg production and prevention of skeletal deformities to drive market

- 9.11.4 MAGNESIUM

- 9.11.4.1 Necessity of magnesium for bone growth and stability to drive market

- 9.11.5 SODIUM

- 9.11.5.1 Role of sodium in regulation of acid-base equilibrium and maintenance of osmotic pressure to drive market

- 9.11.6 IRON

- 9.11.6.1 Significance of iron in formation of hemoglobin and myoglobin to drive market

- 9.11.7 ZINC

- 9.11.7.1 Role of zinc in development of immune system and reproductive capacity to drive market

- 9.11.8 COPPER

- 9.11.8.1 Health benefits of copper and vital role in cellular respiration to boost market

- 9.11.9 MANGANESE

- 9.11.9.1 Role in efficient functioning of mitochondria in cells and prevention of oxidative stress to drive market

- 9.11.10 OTHER MINERALS

- 9.11.1 POTASSIUM

- 9.12 ANTIOXIDANTS

- 9.12.1 SYNTHETIC ANTIOXIDANTS

- 9.12.1.1 Role in protection of fat-soluble vitamins against oxidative degradation to drive market

- 9.12.2 NATURAL ANTIOXIDANTS

- 9.12.2.1 Fewer side effects than synthetic antioxidants to drive market

- 9.12.1 SYNTHETIC ANTIOXIDANTS

- 9.13 NON-PROTEIN NITROGEN

- 9.13.1 UREA

- 9.13.1.1 Low cost and easy availability to drive market

- 9.13.2 AMMONIA

- 9.13.2.1 Role of ammonia in improving digestibility and increasing feed intake to drive market

- 9.13.3 OTHER NON-PROTEIN NITROGEN ADDITIVES

- 9.13.1 UREA

- 9.14 PHYTOGENICS

- 9.14.1 ESSENTIAL OILS

- 9.14.1.1 Role in improvement of gut health and healthy digestion in poultry to boost market

- 9.14.2 FLAVONOIDS

- 9.14.2.1 Improvement of gut health and heart stress control in livestock to boost market

- 9.14.3 SAPONINS

- 9.14.3.1 Role of saponins in suppressing intestinal and ruminal ammonia production to drive market

- 9.14.4 OLEORESINS

- 9.14.4.1 Role of oleoresins in imparting color, flavor, and aroma to livestock feed to drive market

- 9.14.5 OTHER PHYTOGENICS

- 9.14.1 ESSENTIAL OILS

- 9.15 PRESERVATIVES

- 9.15.1 MOLD INHIBITORS

- 9.15.1.1 Role of mold inhibitors in preventing mold growth and contamination to drive market

- 9.15.2 ANTICAKING AGENTS

- 9.15.2.1 Significance of anticaking agents in preventing accumulation of feed nutrients to drive market

- 9.15.1 MOLD INHIBITORS

- 9.16 PROBIOTICS

- 9.16.1 BACTERIA

- 9.16.1.1 Bacterial Probiotics Enhancing animal yield through gut health optimization

- 9.16.1.2 Lactobacillus

- 9.16.1.2.1 Potential to replace antibiotic growth promoters to drive market

- 9.16.1.3 Bifidobacteria

- 9.16.1.3.1 Benefits to adult livestock, such as controlling pH level of large intestine to accelerate market growth

- 9.16.1.4 Streptococcus

- 9.16.1.4.1 Usage in manufacture of various feed probiotic products to drive market

- 9.16.1.5 Bacillus

- 9.16.1.5.1 Bacillus probiotics: Stable, spore-powered solutions for superior animal performance

- 9.16.2 YEAST & FUNGI

- 9.16.2.1 Role in increased production of milk in dairy cattle to drive market

- 9.16.1 BACTERIA

10 FEED ADDITIVES MARKET, BY FUNCTION

- 10.1 INTRODUCTION

- 10.2 GUT HEALTH

- 10.2.1 INCREASED DEMAND FOR HEALTHY GUT MICROBIOTA TO IMPROVE DIGESTION AND PREVENT GASTROINTESTINAL DISEASES

- 10.3 PALATABILITY ENHANCERS

- 10.3.1 IMPROVED TASTE, SMELL, AND OVERALL APPEAL OF ANIMAL FEED TO DRIVE DEMAND

- 10.4 GROWTH BOOSTERS

- 10.4.1 RISING DEMAND FOR MEAT TO DRIVE DEMAND FOR GROWTH BOOSTERS

- 10.5 IMMUNE SYSTEM SUPPORT

- 10.5.1 INCREASED DISEASE INCIDENCES TO DRIVE DEMAND

- 10.6 FEED EFFICIENCY IMPROVEMENT

- 10.6.1 OPTIMIZING ANIMAL PERFORMANCE THROUGH SMARTER FEED UTILIZATION

- 10.7 OTHER FUNCTIONS

11 FEED ADDITIVES MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 COMMERCIAL FEED MANUFACTURERS

- 11.3 INTEGRATED LIVESTOCK AND POULTRY PRODUCTION COMPANIES

- 11.4 AQUAFEED MANUFACTURING INDUSTRY

- 11.5 PET FOOD MANUFACTURING INDUSTRY

- 11.6 FEED PREMIX MANUFACTURING INDUSTRY

- 11.7 COMMERCIAL FARMS (ON FARM FEED MIXING)

12 FEED ADDITIVES MARKET, BY LIVESTOCK

- 12.1 INTRODUCTION

- 12.2 POULTRY

- 12.2.1 RISE IN DEMAND FOR HIGH-QUALITY CHICKEN AND EGGS TO DRIVE MARKET

- 12.2.2 BROILERS

- 12.2.3 LAYERS

- 12.2.4 BREEDERS

- 12.3 RUMINANTS

- 12.3.1 INCREASE IN CONSUMPTION OF DAIRY PRODUCTS AND BEEF TO DRIVE DEMAND

- 12.3.2 CALF

- 12.3.3 DAIRY

- 12.3.4 BEEF

- 12.3.5 OTHER RUMINANTS

- 12.4 SWINE

- 12.4.1 RISE IN PORK TRADE AND CONCERNS OVER MEAT SAFETY TO BOOST MARKET

- 12.4.2 STARTERS

- 12.4.3 GROWERS

- 12.4.4 SOWS

- 12.5 AQUATIC ANIMALS

- 12.5.1 INCREASE IN AQUAFEED PRODUCTION TO DRIVE MARKET

- 12.5.2 FISH

- 12.5.3 CRUSTACEANS

- 12.5.4 MOLLUSKS

- 12.5.5 OTHER AQUATIC ANIMALS

- 12.6 OTHER LIVESTOCK

13 FEED ADDITIVES MARKET, BY SOURCE

- 13.1 INTRODUCTION

- 13.2 SYNTHETIC

- 13.2.1 COST-EFFECTIVENESS AND HIGH STABILITY PROPERTIES TO PROPEL GROWTH

- 13.3 NATURAL

- 13.3.1 CONCERNS REGARDING ANTIBIOTIC RESISTANCE TO DRIVE MARKET FOR NATURAL ADDITIVES

14 FEED ADDITIVES MARKET, BY FORM

- 14.1 INTRODUCTION

- 14.2 DRY

- 14.2.1 CONVENIENCE IN STORAGE, HANDLING, AND TRANSPORTATION TO DRIVE MARKET

- 14.3 LIQUID

- 14.3.1 UNIFORM MIXING AND PRECISE DOSING OF LIQUID FEED ADDITIVES TO PROPEL MARKET

15 FEED ADDITIVES MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Increasing trend of precision feeding techniques to boost demand for effective feed additives

- 15.2.2 CANADA

- 15.2.2.1 Rise in demand for meat and lenient regulations pertaining to use of growth promoters to boost market

- 15.2.3 MEXICO

- 15.2.3.1 Significant rise in livestock production to drive feed additive consumption in Mexico

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 SPAIN

- 15.3.1.1 Higher preference for meat and dairy products to boost market

- 15.3.2 RUSSIA

- 15.3.2.1 Increasing feed production rate to drive market

- 15.3.3 GERMANY

- 15.3.3.1 Technological advancements in livestock management to drive market

- 15.3.4 FRANCE

- 15.3.4.1 High domestic demand for meat products to drive market

- 15.3.5 ITALY

- 15.3.5.1 Focus on improving animal health and nutrition to drive market

- 15.3.6 UK

- 15.3.6.1 Rising demand for high-quality meat and dairy products to boost market

- 15.3.7 REST OF EUROPE

- 15.3.1 SPAIN

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Large feed production to drive market

- 15.4.2 INDIA

- 15.4.2.1 Increased consumption of meat and dairy products to drive market

- 15.4.3 JAPAN

- 15.4.3.1 Increasing consumer demand for premium animal-based products to drive market

- 15.4.4 THAILAND

- 15.4.4.1 Export opportunities in poultry and aquaculture industry to drive market

- 15.4.5 INDONESIA

- 15.4.5.1 High demand for feed due to growing poultry sector to drive market

- 15.4.6 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.5.1.1 Brazil's thriving meat export industry to drive market

- 15.5.2 ARGENTINA

- 15.5.2.1 High consumption of meat and thriving livestock industry to drive market

- 15.5.3 REST OF SOUTH AMERICA

- 15.5.1 BRAZIL

- 15.6 REST OF THE WORLD (ROW)

- 15.6.1 MIDDLE EAST

- 15.6.1.1 Rising demand for animal-based products to drive market

- 15.6.2 AFRICA

- 15.6.2.1 Increase in disease outbreaks to drive market

- 15.6.1 MIDDLE EAST

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN

- 16.3 REVENUE ANALYSIS, 2022-2024

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 BRAND/PRODUCT COMPARISON

- 16.5.1 CARGILL, INCORPORATED (DELACON)

- 16.5.2 ADM (PANCOSMA)

- 16.5.3 NUTRECO (SELKO)

- 16.5.4 ADISSEO (RHODIMET)

- 16.5.5 DSM-FIRMENICH (MYCOFIX)

- 16.6 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6.1 COMPANY VALUATION

- 16.6.2 EV/EBITDA

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Regional footprint

- 16.7.5.3 Type footprint

- 16.7.5.4 Livestock footprint

- 16.7.5.5 Form footprint

- 16.7.5.6 Source footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO AND TRENDS

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 CARGILL, INCORPORATED

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.3.2 Expansions

- 17.1.1.3.3 Product launches

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses & competitive threats

- 17.1.2 ADM

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 INTERNATIONAL FLAVORS & FRAGRANCES INC.

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 EVONIK INDUSTRIES AG

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Expansions

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses & competitive threats

- 17.1.5 BASF SE

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses & competitive threats

- 17.1.6 DSM-FIRMENICH

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.6.3.3 Expansions

- 17.1.6.4 MnM view

- 17.1.6.4.1 Key strengths

- 17.1.6.4.2 Strategic choices

- 17.1.6.4.3 Weaknesses & competitive threats

- 17.1.7 ALLTECH

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.7.4 MnM view

- 17.1.7.4.1 Key strengths

- 17.1.7.4.2 Strategic choices

- 17.1.7.4.3 Weaknesses & competitive threats

- 17.1.8 AJINOMOTO CO., INC.

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Deals

- 17.1.8.4 MnM view

- 17.1.9 NOVONESIS GROUP

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Deals

- 17.1.9.4 MnM view

- 17.1.10 ADISSEO

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deals

- 17.1.10.4 MnM view

- 17.1.11 JUBILANT INGREVIA LIMITED

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Expansions

- 17.1.11.4 MnM view

- 17.1.12 NUTRECO

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Deals

- 17.1.12.3.2 Expansions

- 17.1.12.4 MnM view

- 17.1.13 BRF GLOBAL

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.13.4 MnM view

- 17.1.14 VOLAC INTERNATIONAL LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Solutions/Services offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Expansions

- 17.1.14.3.2 Other developments

- 17.1.14.4 MnM view

- 17.1.15 KEMIN INDUSTRIES, INC.

- 17.1.15.1 Business overview

- 17.1.15.2 Products/Solutions/Services offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product launches

- 17.1.15.3.2 Deals

- 17.1.15.3.3 Expansions

- 17.1.15.4 MnM view

- 17.1.16 LALLEMAND INC.

- 17.1.16.1 Business overview

- 17.1.16.2 Products/Solutions/Services offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Product launches

- 17.1.16.3.2 Deals

- 17.1.16.4 MnM view

- 17.1.17 BENTOLI

- 17.1.17.1 Business overview

- 17.1.17.2 Products/Solutions/Services offered

- 17.1.17.3 Recent developments

- 17.1.17.3.1 Deals

- 17.1.17.4 MnM view

- 17.1.18 NEOSPARK DRUGS AND CHEMICALS PRIVATE LIMITED

- 17.1.18.1 Business overview

- 17.1.18.2 Products/Solutions/Services offered

- 17.1.18.3 MnM view

- 17.1.19 NOVUS INTERNATIONAL, INC.

- 17.1.19.1 Business overview

- 17.1.19.2 Products/Solutions/Services offered

- 17.1.19.3 Recent developments

- 17.1.19.3.1 Deals

- 17.1.19.3.2 Other developments

- 17.1.19.4 MnM view

- 17.1.20 GLOBAL NUTRITION INTERNATIONAL

- 17.1.20.1 Business overview

- 17.1.20.2 Products/Solutions/Services offered

- 17.1.20.3 MnM view

- 17.1.1 CARGILL, INCORPORATED

- 17.2 OTHER PLAYERS

- 17.2.1 VITALAC

- 17.2.2 TEX BIOSCIENCES (P) LTD.

- 17.2.3 CENTAFARM SRL

- 17.2.4 NUQO FEED ADDITIVES

- 17.2.5 PHYTOBIOTICS FUTTERZUSATZSTOFFE GMBH

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Breakdown of primary profiles

- 18.1.2.2 Key insights from industry experts

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 TOP-DOWN APPROACH

- 18.2.2 SUPPLY-SIDE ANALYSIS

- 18.2.3 BOTTOM-UP APPROACH (DEMAND SIDE)

- 18.3 DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

19 ADJACENT & RELATED MARKETS

- 19.1 INTRODUCTION

- 19.2 STUDY LIMITATIONS

- 19.3 AQUAFEED MARKET

- 19.3.1 MARKET DEFINITION

- 19.3.2 MARKET OVERVIEW

- 19.4 COMPOUND FEED MARKET

- 19.4.1 MARKET DEFINITION

- 19.4.2 MARKET OVERVIEW

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS