|

시장보고서

상품코드

1802926

3D 프린팅 세라믹 시장 예측(-2030년) : 세라믹 유형별, 형태별, 최종 용도 산업별, 지역별3D Printing Ceramics Market by Type (Oxides, Non-oxides), Form (Filament, Powder, Liquid), End-use Industry (Aerospace & Defense, Healthcare, Automotive, Consumer Goods & Electronics, Other End-use Industry), and Region - Global Forecast to 2030 |

||||||

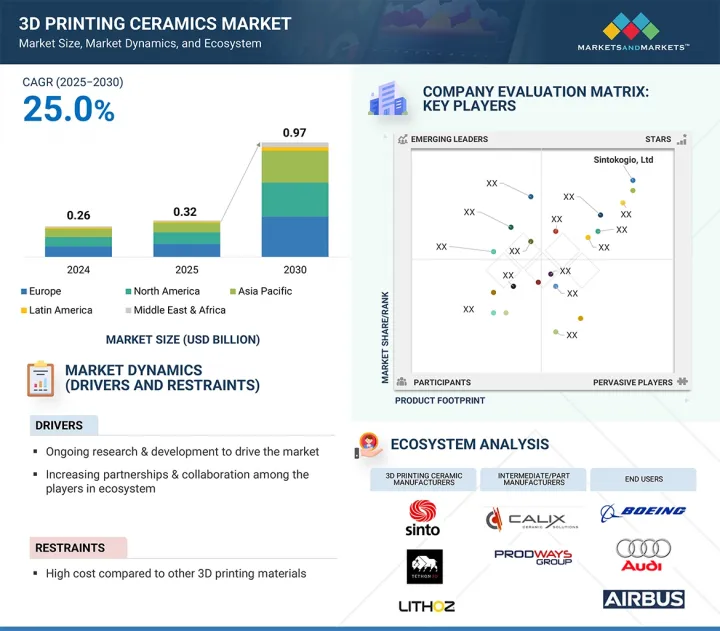

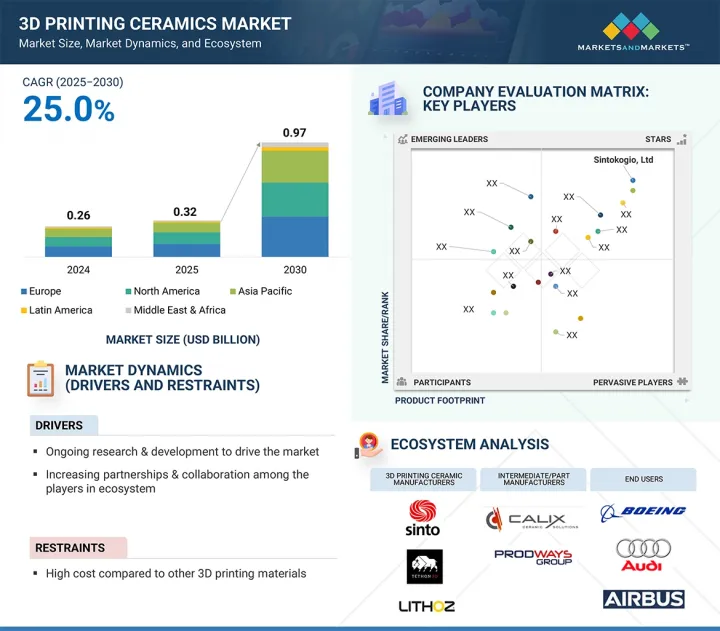

3D 프린팅 세라믹 시장 규모는 2025년에 3억 2,000만 달러로 추정되어 25.0%의 CAGR로 확대하며, 2030년에는 9억 7,000만 달러에 달할 것으로 예측됩니다.

3D 프린팅 세라믹 시장 확대의 주요 원동력은 경량, 내열성, 기계적 강도가 높은 부품을 필요로 하는 항공우주, 헬스케어, 전자 산업 등 산업 전반에 걸쳐 고성능 맞춤형 세라믹 부품에 대한 수요가 증가하고 있다는 점입니다.

| 조사 범위 | |

|---|---|

| 조사 대상연도 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러) 및 톤 |

| 부문 | 세라믹 유형별, 형태별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

적층제조은 기존 세라믹 제조에서 어렵거나 불가능했던 독보적인 설계 자유도와 지오메트리를 제공합니다. 이와 함께 세라믹 재료의 배합, 인쇄 장비(바인더 제트, 스테레오리소그래피, 압출), 디지털 공정 제어의 발전으로 효율, 정확도, 재료 성능이 크게 향상되었습니다. 이러한 측면은 재료 폐기물 감소 및 에너지 사용량 감소로 인한 지속가능성 이점과 함께 산업 및 상업 공정에 광범위하게 적용되고 있습니다.

3D 프린팅 세라믹 산업의 필라멘트 부문은 주로 취급 용이성, 일반적으로 사용되는 FDM/FFF 프린터와의 호환성, 데스크톱 수준의 저비용 세라믹 프린팅 솔루션에 대한 관심 증가에 따라 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 가장 높은 CAGR을 보이고 있습니다. 필라멘트 기반 세라믹 프린팅은 제조 공정을 간소화하여 치과, 전자, 연구 등 다양한 산업에서 시제품 제작 및 소규모 생산 목적으로 사용할 수 있습니다. 하지만 전 세계에서 고품질 세라믹 필라멘트를 제조하는 제조업체가 거의 없기 때문에 공급 격차가 존재하고, 신규 진입과 기술 혁신을 위한 높은 시장 잠재력이 남아있어 미충족 수요도 성장을 가속하고 있습니다.

헬스케어 분야는 치과 수복물, 뼈 임플란트, 수술기구에 생체적합성 세라믹 재료의 사용이 증가함에 따라 3D 프린팅 세라믹 시장에서 두 번째로 높은 CAGR을 보일 것으로 추정됩니다. 지르코니아, 알루미나 등의 세라믹 소재는 생체적합성, 내마모성, 강도가 우수하여 맞춤형 치관 및 정형외과용 임플란트에 적합합니다. 3D 프린팅은 정확하고 환자 맞춤형 설계를 가능하게 하고, 수술 시간을 단축하며, 치료 결과를 향상시킬 수 있습니다. 또한 의료가 개인맞춤형 치료와 최소침습 치료로 진화함에 따라 맞춤형 고성능 세라믹 부품의 필요성이 증가하고 있습니다. 세라믹 인쇄 기술에 사용되는 공정과 재료의 발전으로 인해 치과 및 정형외과 용도에서의 채택이 가속화되고 있습니다.

유럽은 적층제조에 대한 정부의 강력한 지원, 탄탄한 산업 기반, 첨단 소재에 대한 R&D 비용 증가로 인해 3D 프린팅 세라믹 시장에서 두 번째로 높은 CAGR을 보일 것으로 예측됩니다. 독일, 프랑스, 러시아는 세라믹 3D 프린팅의 기술 혁신을 주도하고 있으며, 특히 항공우주, 헬스케어, 자동차 산업에 중점을 두고 있습니다. 또한 이 지역은 미래의 세라믹 프린팅 기술을 창출하기 위해 업계 리더들과 협력하는 대학 및 연구 기관의 강력한 기반이 지원되고 있습니다. 또한 디지털 제조와 지속가능성에 중점을 두고 있는 EU는 저폐기물, 효율적, 경량 생산을 위한 3D 프린팅 세라믹의 적용을 추진하고 있습니다.

세계의 3D 프린팅세라믹슨 시장에 대해 조사했으며, 세라믹 유형별, 형태별, 최종 용도 산업별, 지역별 동향 및 시장에 참여하는 기업의 개요 등을 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 주요 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 에코시스템 분석

- 가격 분석

- 밸류체인 분석

- 무역 분석

- 기술 분석

- AI/생성형 AI가 3D 프린트 세라믹 시장에 미치는 영향

- 거시경제 전망

- 특허 분석

- 규제 상황

- 2025-2026년의 주요 컨퍼런스와 이벤트

- 사례 연구 분석

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 투자와 자금조달 시나리오

- 2025년 미국 관세가 3D 프린트 세라믹 시장에 미치는 영향

제6장 3D 프린트 세라믹 시장(세라믹 유형별)

- 서론

- 산화물

- 비산화물

제7장 3D 프린트 세라믹 시장(형태별)

- 서론

- 필라멘트

- 액체

- 분말

제8장 3D 프린트 세라믹 시장(최종 용도 산업별)

- 서론

- 항공우주 및 방위

- 헬스케어

- 자동차

- 소비재·전자기기

- 기타

제9장 3D 프린트 세라믹 시장(지역별)

- 서론

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

제10장 경쟁 구도

- 개요

- 주요 참여 기업의 전략/강점

- 매출 분석, 2020-2024년

- 시장 점유율 분석, 2024년

- 브랜드/제품 비교 분석

- 기업 평가 매트릭스 : 주요 참여 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 3D 프린트 세라믹 벤더의 기업 평가와 재무 지표

- 경쟁 시나리오

제11장 기업 개요

- 주요 참여 기업

- SINTOKOGIO, LTD.

- SGL CARBON

- CERAMTEC GMBH

- NANOE

- SAINT-GOBAIN

- CONCR3DE

- JIANGSU SANZER NEW MATERIALS TECHNOLOGY CO., LTD.

- LITHOZ GMBH

- TETHON 3D

- KYOCERA CORPORATION

- 기타 기업

- STEINBACH AG

- XJET

- ZRAPID TECH

- TRUNNANO

- INTERNATIONAL SYALONS

- FORMLABS

- SCHUNK TECHNICAL CERAMICS

- STANDARD NUCLEAR

- SHENZHEN ADVENTURE TECHNOLOGY CO., LTD

- SINTX TECHNOLOGIES, INC.

- SPECTRUM FILAMENTS

- CERAMARET

- ZHENGZHOU HAIXU ABRASIVES CO., LTD

- NISHIMURA ADVANCED CERAMICS

- WUNDER-MOLD, INC.

제12장 부록

KSA 25.09.08The 3D printing ceramics market is estimated at USD 0.32 billion in 2025 and is projected to reach USD 0.97 billion by 2030, at a CAGR of 25.0%. The main impetus for the expansion of the 3D-printing ceramics market is the increasing need for high-performance, tailor-made ceramic parts across industries like aerospace, health-care, and electronics industries that necessitate light, heat-resistant, and mechanically strong components.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Ton) |

| Segments | Ceramic Type, Form, End-use Industry, and Region |

| Regions covered | Europe, North America, Asia Pacific, the Middle East & Africa, and South America |

Additive manufacturing provides unparalleled design freedom and geome-tries that are hard or impossible to achieve with conventional ceramic manufacture. Parallel to this, advances in ceramic materials formulation, printing equipment (binder jetting, stereolithography, and extrusion), and digital process control have greatly enhanced efficiency, precision, and material performance. These aspects, combined with sustainability advantages resulting from decreased material waste and lower energy usage, are driving widespread application in industrial and commercial processes.

"Filament is projected to be the fastest-growing form during the forecast period."

The filament segment of the 3D printing ceramics industry is exhibiting the highest CAGR, based mainly on its handling ease, compatibility with commonly utilized FDM/FFF printers, and growing interest in low-cost ceramic printing solutions at the desktop level. Filament-based ceramic printing streamlines the manufacturing process, allowing it to be made accessible for prototyping and small-scale production purposes in various industries such as dental, electronics, and research. Nonetheless, the unmet demand also fuels growth since there are virtually no manufacturers of high-quality ceramic filaments worldwide, leaving a supply gap and high market potential for new entrants and innovations.

"The healthcare segment is projected to register the second-highest growth rate during the forecast period."

The healthcare sector is estimated to exhibit the second-best CAGR in the 3D printing ceramics market because of the increasing use of biocompatible ceramic material for dental restorations, bone implants, and surgical instruments. Ceramic materials such as zirconia and alumina are highly biocompatible, resistant to wear, and strong, and hence can be well-suited for tailor-made dental crowns and orthopedic implants. 3D printing allows accurate, patient-specific designs that save surgery time and enhance outcomes. Further, as medicine evolves toward personalized care and minimally invasive treatments, the need for tailored, high-performance ceramic parts is growing. Advances in the processes and materials used in ceramic printing technologies are accelerating adoption in dental and orthopedic applications.

"Europe is projected to register the second-highest growth rate in the 3D printing ceramics market during the forecast period."

Europe is pegged to witness the second-highest CAGR in the 3D printing ceramics market because of robust government backing of additive manufacturing, an established industrial foundation, and rising R&D spending in advanced materials. Germany, France, and Russia are leading the charge in ceramic 3D printing innovation, with specific emphasis in the aerospace, healthcare, and automotive industries, with high demand for precision and material performance. The area is also underpinned by a strong base of universities and research institutes cooperating with industry leaders to create tomorrow's ceramic printing technologies. In addition, the EU's focus on digital manufacturing and sustainability drives the application of 3D printed ceramics for low-waste, efficient, and lightweight production.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 40%; Tier 2 - 33%; and Tier 3 - 27%

- By Designation: C-level - 50%; Director-level - 30%; and Managers - 20%

- By Region: North America - 15%; Europe - 50%; Asia Pacific - 20%; the Middle East & Africa - 10%; and Latin America - 5%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market include Sintokogio, Ltd. (Japan), Lithoz GmbH (Austria), SGL Carbon (France), CeramTec GmbH (Germany), Tethon 3D (US), Saint-Gobain (France), Nanoe (France), Jiangsu Sanzer New Materials Technology Co., Ltd. (China), and KYOCERA Corporation (Japan).

Research Coverage

This research report categorizes the 3D printing ceramics market by ceramic type (oxides, non-oxides), form (liquid, filament, powder), end-use industry (aerospace & defense, healthcare, automotive, consumer goods & electronics, other end-use industries), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America). The scope of the report includes detailed information about the major factors influencing the growth of the 3D printing ceramics market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions and services, key strategies, and recent developments in the 3D printing ceramics market. This report includes a competitive analysis of upcoming startups in the 3D printing ceramics market ecosystem.

Reasons to buy this report

The report will help market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall 3D printing ceramics market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increasing research & development activities in 3D printing ceramics), restraints (availability of substitutes and high cost of 3D printing ceramics), opportunities (growing investments and fundings in the market), and challenges (low adoption and acceptance of 3D printing ceramics and high cost compared to substitute materials) are influencing the growth of the 3D printing ceramics market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the 3D printing ceramics market.

- Market Development: Comprehensive information about lucrative markets-the report analyses the 3D printing ceramics market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the 3D printing ceramics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like Sintokogio, Ltd. (Japan), Lithoz GmbH (Austria), SGL Carbon (France), CeramTec GmbH (Germany), Tethon 3D (US), Saint-Gobain (France), Nanoe (France), Jiangsu Sanzer New Materials Technology Co., Ltd. (China), and KYOCERA Corporation (Japan).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET S COVERED AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Interviews with top 3D printing ceramics manufacturers

- 2.1.2.3 Breakdown of primary interviews with experts

- 2.1.2.4 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 BASE NUMBER CALCULATION

- 2.3 GROWTH FORECAST

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN 3D PRINTING CERAMICS MARKET

- 4.2 3D PRINTING CERAMICS MARKET BY END-USE INDUSTRY AND REGION

- 4.3 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 4.4 3D PRINTING CERAMICS MARKET, BY FORM

- 4.5 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 4.6 3D PRINTING CERAMICS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Ongoing research & development

- 5.2.1.2 Increase in partnerships & collaboration among players in ecosystem

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost compared to other 3D printing materials

- 5.2.2.2 Economy of scale not achieved

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increase in investments in 3D printing ceramics manufacturing

- 5.2.3.2 Development of advanced printers compatible with ceramics

- 5.2.4 CHALLENGES

- 5.2.4.1 Availability of substitutes

- 5.2.4.2 Capital-intensive production and complex manufacturing process

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

- 5.6.2 AVERAGE SELLING PRICE TREND, BY CERAMIC TYPE

- 5.6.3 AVERAGE SELLING PRICE TREND, BY FORM

- 5.6.4 AVERAGE SELLING PRICE TREND, BY REGION

- 5.7 VALUE CHAIN ANALYSIS

- 5.8 TRADE ANALYSIS

- 5.8.1 EXPORT SCENARIO (HS CODE 69)

- 5.8.2 IMPORT SCENARIO (HS CODE 69)

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Stereolithography

- 5.9.1.2 Binder jetting

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Fused filament fabrication (FFF)

- 5.9.1 KEY TECHNOLOGIES

- 5.10 IMPACT OF AI/GEN AI ON 3D PRINTING CERAMICS MARKET

- 5.10.1 TOP USE CASES AND MARKET POTENTIAL

- 5.10.2 CASE STUDIES OF AI IMPLEMENTATION IN 3D PRINTING CERAMICS MARKET

- 5.11 MACROECONOMIC OUTLOOK

- 5.11.1 INTRODUCTION

- 5.11.2 GDP TRENDS AND FORECAST

- 5.11.3 TRENDS IN GLOBAL AEROSPACE & DEFENSE INDUSTRY

- 5.11.4 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.12 PATENT ANALYSIS

- 5.12.1 INTRODUCTION

- 5.12.2 METHODOLOGY

- 5.12.3 PATENT TYPES

- 5.12.4 INSIGHTS

- 5.12.5 LEGAL STATUS

- 5.12.6 JURISDICTION ANALYSIS

- 5.12.7 TOP APPLICANTS

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 DENBY POTTERY AND UWE BRISTOL: TRANSFORMING TABLEWARE PROTOTYPING WITH 3D PRINTED CERAMICS

- 5.15.2 LITHOZ LITHABONE TCP 300 FOR PATIENT-SPECIFIC BONE IMPLANTS IN HEALTHCARE

- 5.15.3 3DCERAM'S CERIA AI-TRANSFORMING MEDICAL 3D PRINTED CERAMICS

- 5.16 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.17 INVESTMENT AND FUNDING SCENARIO

- 5.18 IMPACT OF 2025 US TARIFF ON 3D PRINTING CERAMICS MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACTS ON COUNTRY/REGION

- 5.18.4.1 US

- 5.18.4.2 Europe

- 5.18.4.3 Asia Pacific

- 5.18.5 IMPACT ON END-USE INDUSTRIES

6 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 6.1 INTRODUCTION

- 6.1.1 OXIDES

- 6.1.1.1 Growing demand from various end-use industries to drive market

- 6.1.1.2 Alumina

- 6.1.1.3 Zirconia

- 6.1.1.4 Other oxide types

- 6.1.2 NON-OXIDES

- 6.1.2.1 Advanced performance requirements to drive non-oxide ceramic demand in 3D printing

- 6.1.2.2 Silicon carbide

- 6.1.2.3 Silicon nitride

- 6.1.2.4 Other non-oxide types

- 6.1.1 OXIDES

7 3D PRINTING CERAMICS MARKET, BY FORM

- 7.1 INTRODUCTION

- 7.1.1 FILAMENT

- 7.1.1.1 Technological development in manufacturing of ceramic filament to drive market

- 7.1.2 LIQUID

- 7.1.2.1 Increased adoption of liquid-based ceramics for high-resolution applications

- 7.1.3 POWDER

- 7.1.3.1 Extensive industry backing and process simplicity to propel powder-based ceramic printing

- 7.1.1 FILAMENT

8 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- 8.2 AEROSPACE & DEFENSE

- 8.2.1 INCREASE IN USE IN MANUFACTURING COMPLEX COMPONENTS AND EQUIPMENT TO DRIVE MARKET

- 8.3 HEALTHCARE

- 8.3.1 ADVANCEMENTS IN BIOCOMPATIBLE CERAMICS TO FUEL GROWTH IN HEALTHCARE 3D PRINTING

- 8.4 AUTOMOTIVE

- 8.4.1 DEMAND FOR HIGH-PERFORMANCE COMPONENTS TO FUEL ADOPTION OF 3D PRINTING CERAMICS

- 8.5 CONSUMER GOODS & ELECTRONICS

- 8.5.1 HIGH DEMAND FOR MANUFACTURING COMPLEX DESIGNS IN CONSUMER GOODS & ELECTRONICS TO DRIVE MARKET

- 8.6 OTHER END-USE INDUSTRIES

9 3D PRINTING CERAMICS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 9.2.2 NORTH AMERICA: 3D PRINTING CERAMICS MARKET, BY FORM

- 9.2.3 NORTH AMERICA: 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 9.2.4 NORTH AMERICA: 3D PRINTING CERAMICS MARKET, BY COUNTRY

- 9.2.4.1 US

- 9.2.4.1.1 Growing strategic partnerships to drive market

- 9.2.4.2 Canada

- 9.2.4.2.1 Adoption of 3D printing technology for consumer goods to support market growth

- 9.2.4.1 US

- 9.3 EUROPE

- 9.3.1 EUROPE: 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 9.3.2 EUROPE: 3D PRINTING CERAMICS MARKET, BY FORM

- 9.3.3 EUROPE: 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 9.3.4 EUROPE: 3D PRINTING CERAMICS MARKET, BY COUNTRY

- 9.3.4.1 Germany

- 9.3.4.1.1 Presence of 3D-printed ceramic manufacturers to drive market

- 9.3.4.2 France

- 9.3.4.2.1 Increase in demand from aerospace & defense industries to fuel market

- 9.3.4.3 UK

- 9.3.4.3.1 Growth in research & development centers to propel market

- 9.3.4.4 Italy

- 9.3.4.4.1 Adoption of 3D printing ceramics in various sectors to drive market

- 9.3.4.5 Rest of Europe

- 9.3.4.1 Germany

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 9.4.2 ASIA PACIFIC: 3D PRINTING CERAMICS MARKET, BY FORM

- 9.4.3 ASIA PACIFIC: 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 9.4.4 ASIA PACIFIC: 3D PRINTING CERAMICS MARKET, BY COUNTRY

- 9.4.4.1 China

- 9.4.4.1.1 Rapid industrialization and investments to propel market

- 9.4.4.2 Japan

- 9.4.4.2.1 Ongoing research collaborations to result in surge in demand

- 9.4.4.3 South Korea

- 9.4.4.3.1 Strategic collaborations among universities & manufacturers to drive market

- 9.4.4.4 India

- 9.4.4.4.1 Growing government initiatives and partnerships to support market growth

- 9.4.4.5 Rest of Asia Pacific

- 9.4.4.1 China

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST & AFRICA: 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 9.5.2 MIDDLE EAST & AFRICA: 3D PRINTING CERAMICS MARKET, BY FORM

- 9.5.3 MIDDLE EAST & AFRICA: 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 9.5.4 MIDDLE EAST & AFRICA: 3D PRINTING CERAMICS MARKET, BY COUNTRY

- 9.5.4.1 GCC Countries

- 9.5.4.1.1 UAE

- 9.5.4.1.1.1 High demand from end-use industries to propel growth

- 9.5.4.1.2 Saudi Arabia

- 9.5.4.1.2.1 Growing government initiatives toward technological innovation and industrial diversification to drive market

- 9.5.4.1.3 Rest of GCC

- 9.5.4.1.1 UAE

- 9.5.4.2 South Africa

- 9.5.4.2.1 Growing adoption of 3D printing ceramics across various sectors to fuel market

- 9.5.4.3 Rest of Middle East & Africa

- 9.5.4.1 GCC Countries

- 9.6 LATIN AMERICA

- 9.6.1 LATIN AMERICA: 3D PRINTING CERAMICS MARKET, BY CERAMIC TYPE

- 9.6.2 LATIN AMERICA: 3D PRINTING CERAMICS MARKET, BY FORM

- 9.6.3 LATIN AMERICA: 3D PRINTING CERAMICS MARKET, BY END-USE INDUSTRY

- 9.6.4 LATIN AMERICA: 3D PRINTING CERAMICS MARKET, BY COUNTRY

- 9.6.4.1 Brazil

- 9.6.4.1.1 Economic improvements to propel market for 3D printing ceramics

- 9.6.4.2 Mexico

- 9.6.4.2.1 Increase in innovations to augment market growth

- 9.6.4.3 Rest of Latin America

- 9.6.4.1 Brazil

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 10.3 REVENUE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 10.5.1 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 10.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.6.1 STARS

- 10.6.2 EMERGING LEADERS

- 10.6.3 PERVASIVE PLAYERS

- 10.6.4 PARTICIPANTS

- 10.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.7.1 PROGRESSIVE COMPANIES

- 10.7.2 RESPONSIVE COMPANIES

- 10.7.3 DYNAMIC COMPANIES

- 10.7.4 STARTING BLOCKS

- 10.7.5 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

- 10.7.5.1 Detailed list of key startups/SMEs

- 10.7.5.2 Competitive benchmarking of key startups/SMEs

- 10.8 COMPANY VALUATION AND FINANCIAL METRICS OF 3D PRINTING CERAMICS VENDORS

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 SINTOKOGIO, LTD.

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Deals

- 11.1.1.3.2 Expansions

- 11.1.1.3.3 Other developments

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 SGL CARBON

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Deals

- 11.1.2.4 MnM view

- 11.1.2.4.1 Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 CERAMTEC GMBH

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Deals

- 11.1.3.3.2 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 NANOE

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches

- 11.1.4.3.2 Deals

- 11.1.4.3.3 Expansions

- 11.1.4.4 MnM view

- 11.1.4.4.1 Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 SAINT-GOBAIN

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Deals

- 11.1.5.4 MnM view

- 11.1.5.4.1 Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 CONCR3DE

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 MnM view

- 11.1.6.3.1 Right to win

- 11.1.6.3.2 Strategic choices

- 11.1.6.3.3 Weaknesses and competitive threats

- 11.1.7 JIANGSU SANZER NEW MATERIALS TECHNOLOGY CO., LTD.

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Expansions

- 11.1.7.4 MnM view

- 11.1.7.4.1 Right to win

- 11.1.7.4.2 Strategic choices

- 11.1.7.4.3 Weaknesses and competitive threats

- 11.1.8 LITHOZ GMBH

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Product launches

- 11.1.8.3.2 Other developments

- 11.1.8.4 MnM view

- 11.1.8.4.1 Right to win

- 11.1.8.4.2 Strategic choices

- 11.1.8.4.3 Weaknesses and competitive threats

- 11.1.9 TETHON 3D

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches

- 11.1.9.3.2 Deals

- 11.1.9.3.3 Other developments

- 11.1.9.4 MnM view

- 11.1.9.4.1 Right to win

- 11.1.9.4.2 Strategic choices

- 11.1.9.4.3 Weaknesses and competitive threats

- 11.1.10 KYOCERA CORPORATION

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Expansions

- 11.1.10.4 MnM view

- 11.1.10.4.1 Right to win

- 11.1.10.4.2 Strategic choices

- 11.1.10.4.3 Weaknesses and competitive threats

- 11.1.1 SINTOKOGIO, LTD.

- 11.2 OTHER PLAYERS

- 11.2.1 STEINBACH AG

- 11.2.2 XJET

- 11.2.3 ZRAPID TECH

- 11.2.4 TRUNNANO

- 11.2.5 INTERNATIONAL SYALONS

- 11.2.6 FORMLABS

- 11.2.7 SCHUNK TECHNICAL CERAMICS

- 11.2.8 STANDARD NUCLEAR

- 11.2.9 SHENZHEN ADVENTURE TECHNOLOGY CO., LTD

- 11.2.10 SINTX TECHNOLOGIES, INC.

- 11.2.11 SPECTRUM FILAMENTS

- 11.2.12 CERAMARET

- 11.2.13 ZHENGZHOU HAIXU ABRASIVES CO., LTD

- 11.2.14 NISHIMURA ADVANCED CERAMICS

- 11.2.15 WUNDER-MOLD, INC.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS