|

시장보고서

상품코드

1808080

원예용 플라스틱 시장 : 플라스틱 유형별, 조성별, 용도별, 지역별 예측(-2030년)Garden Plastics Market by Plastic Type (Commodity Plastics, Engineering Plastics, Performance Plastics ), Application, Composition, and Region - Global Forecast to 2030 |

||||||

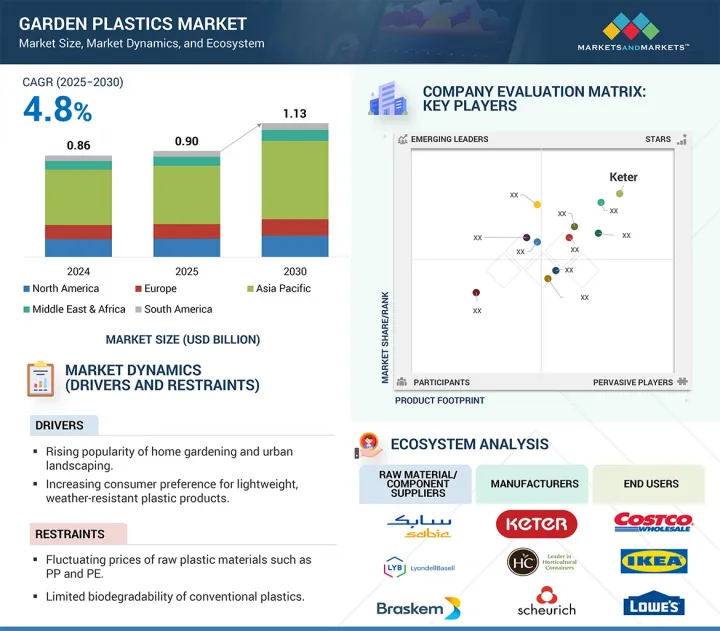

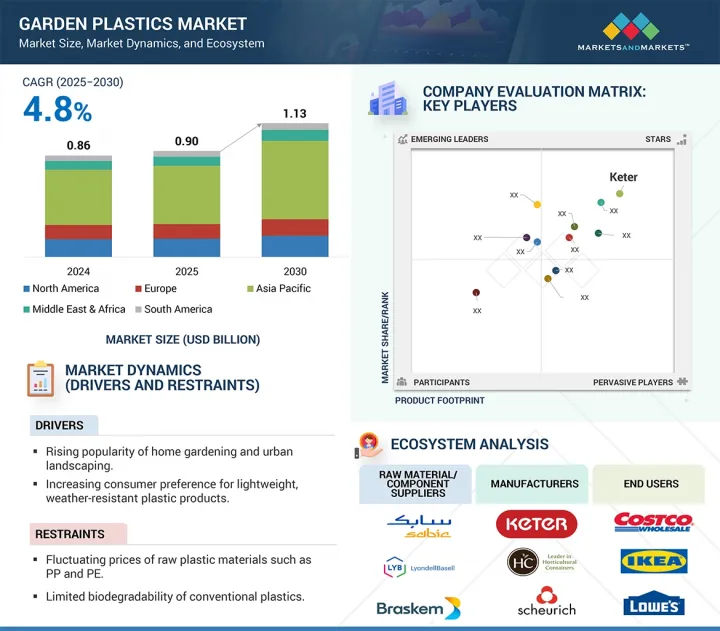

세계의 원예용 플라스틱 시장 규모는 2025년 9억 달러에서 2030년까지 11억 3,000만 달러로 증가해, 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 4.8%를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2023-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러, KT) |

| 부문 | 플라스틱 유형별, 조성별, 용도별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동, 아프리카, 남미 |

이 성장의 대부분은 도시 지역의 고객과 이동 수단 및 공간이 제한된 고객을 위해 DIY에 의한 정세 정비 및 컨테이너 원예가 전체적으로 증가하고 있기 때문입니다. 게다가, 주로 폴리에틸렌, 폴리프로필렌, 재활용 플라스틱으로 만들어진 플라스틱 기반 재배자, 울타리, 수납함, 정원 액세서리의 가용성 증가는 유지 보수 노력이 적고 내구성있는 제품을 요구하는 소비자의 관심에 부응하고 있습니다. 내자외선성, 색유지성, 환경적합성을 향상시키는 플라스틱 배합의 혁신이 시장의 가능성을 넓히고 있습니다.

시장의 지속적인 전망은 재활용 플라스틱 및 사후 소비자, 플라스틱, 정원 제품의 가용성 확대, 지속 가능한 설계에 대한 규제 당국의 압력, 순환 경제 설계를 채택하려는 제조업체의 노력도 뒷받침하고 있습니다. 모듈식 가든 시스템, 스마트 관개용 플라스틱, 고급 장식용기 등 수요도 특히 노후화가 진행되어 원예용 플라스틱에 대한 지출이 많은 신흥국 시장에서 확대될 것으로 보입니다.

유리 섬유 강화 플라스틱(GFRP)은 견고한 기계적 특성과 지속적인 내후성으로 인해 원예용 플라스틱 시장에서 두 번째로 빠르게 성장하는 구성 부문입니다. 이러한 강화 소재는 내하중성이나 내충격성의 강화가 요구되는 고급 가든 가구, 구조용 플랜터, 울타리 패널, 툴 핸들 등에 점점 사용되고 있습니다. GFRP는 구조적 강도와 디자인 적응성의 균형을 맞추는 이상적인 솔루션으로 미적 가치가 있는 지속적인 정원 솔루션에 대한 소비자의 관심이 커지고 있습니다. GFRP는 목재나 금속과 같은 외관을 가지면서 경량화를 실현해, 뛰어난 내식성도 갖추고 있기 때문에 옥외에서의 고급 용도에 적합합니다. 디자인 중심의 조경 추세는 기능적 복잡성과 함께 고급 제품 카테고리에서 GFRP의 사용 증가를 이끌고 있습니다.

비충전 플라스틱 산업은 원예용 플라스틱 분야 전체에서 큰 성장을 이루고 있으며, 예측 기간 동안 추가적인 혜택을 누릴 것으로 예측됩니다. 비충전 플라스틱은 보강되지 않고 충전재도 첨가되지 않았기 때문에 원예용 플라스틱 포장 공급망의 중심 역할을 담당하고 있습니다. 비충전 플라스틱은 화분, 정원 테두리, 옥외 쓰레기통, 경량 컨테이너 등 특히 구조적 무결성이 낮다는 문제가 없는 제품의 생산에 계속 사용되고 있습니다. 성형 공정을 다양화할 수 있어 복합재료의 배합을 고려할 필요가 없기 때문에 비충전 플라스틱은 가공의 다양성과 복합재료의 투입량을 절약할 수 있습니다. 저비용 대체품인 비충전 플라스틱은 DIY 원예와 작은 정원에서 원예의 큰 격차를 메우기 때문에 지속가능성은 앞으로도 제조업체와 소비자들에게 큰 도전입니다. 사용하기 쉽고, 소비자가 환경 친화적 인 원예의 일환으로 비 강화 플라스틱을 채택하는 경향이 강해지고 있다는 것도 비 강화 플라스틱 시장의 성장을 가속화할 것입니다.

2024년 식목에서 고밀도 폴리에틸렌(HDPE)은 원예용 플라스틱 분야에서 사용 가능한 제품을 생산하는 두 번째로 큰 플라스틱 유형을 대표합니다. HDPE의 가장 중요한 장점은 널리 사용 가능하고, 일부는 상품 유형의 플라스틱으로 간주되며, 가장 광범위한 성능 특성을 가지고 있다는 것입니다. HDPE는 정원 가구, 화분, 플랜터, 물뿌리개 등 다양한 유형의 정원 제품에 사용됩니다. HDPE는 유연성, 내구성, 내후성을 겸비한 독특한 소재입니다. HDPE는 내구 수명이 긴 정원 제품에 매우 적합합니다. HDPE는 버진 원료의 과립에 비해 저렴하고 가공하기 쉽고 재활용이 가능합니다. HDPE는 원예용 플라스틱 제조업체에게 저렴하고 환경적으로 지속 가능한 옵션입니다.

2024년 북미는 세계 원예용 플라스틱 시장에서 두 번째로 큰 지역 시장이 되었습니다. 특히 미국과 캐나다에서는 주택 및 상업용 조경 시장에서 조경용 플라스틱 제품에 대한 일관되고 강한 수요가 있습니다. 유행 후, 주택 리노베이션 프로젝트와 DIY(Du-it-Yourself) 원예가 증가하고 지속 가능한 조경 방법에 대한 관심이 높아지고 있습니다. 그 결과 컴포스터, 레이즈드 가든 베드, 갑판 상자, 야외 가구 등의 플라스틱 원예 제품도 증가했습니다. 게다가 북미 소비자들의 환경 의식이 높아짐에 따라 지역 플라스틱 제품 제조업체들에게 플라스틱 제품을 생산하기 위한 기술 혁신을 추진하는 높은 동기를 창출하고 있습니다. 따라서 UV 안정화 플라스틱과 재활용 가능한 플라스틱 제품을 사용하게 되며, 이러한 제품은 환경 친화적인 원예에 대한 소비자의 요구를 충족시킬 수 있기 때문입니다. 또한 국가 및 지역 유통업체와 제휴하는 대규모 소매 브랜드는 광범위한 제품 유통망을 제공하며 이 지역에 광범위한 제품을 공급할 수 있습니다.

대상 기업: Keter(이스라엘), THE HC COMPANIES, INC.(미국), Schurich GmbH &Co.KG(독일), Elho BV(네덜란드), Horst Brandstatter Group(독일), The AMES Companies(미국), Berry Global Inc.(미국), RKW Group(독일), BASF Group(스팬)을 대상으로 합니다. 본 연구에는 원예용 플라스틱 시장에서 이러한 주요 기업의 기업 프로파일, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석이 포함되어 있습니다.

조사 대상

이 조사 보고서는 원예용 플라스틱 시장을 플라스틱 유형별, 용도별, 조성별, 지역별로 분류하고 있습니다. 본 보고서의 조사 범위에서는 원예용 플라스틱 시장의 성장에 영향을 미치는 촉진요인 및 시장 억제요인과 과제 및 기회에 관한 상세정보를 망라하고 있습니다. 주요 업계 진출기업의 상세한 분석을 통해 사업 개요, 제공 제품, 원예용 플라스틱 시장과 관련된 제휴, 계약, 제품 발매, 인수 등 주요 전략에 대한 통찰력을 제공합니다. 이 보고서는 원예 플라스틱 시장 생태계에서 향후 신흥 기업의 경쟁 분석을 다룹니다.

이 보고서는 시장의 리더/신규 참가자에게 원예 플라스틱 시장 전체와 하위 부문 수익의 가장 가까운 근사치에 대한 정보를 제공합니다. 이 보고서는 이해 관계자가 경쟁 구도를 이해하고 비즈니스를 더 잘 파악할 수 있도록 고찰을 심화하고 적절한 시장 진출 전략을 계획하는 데 도움이 됩니다. 이 보고서는 이해관계자가 시장의 박동을 이해하고 주요 시장 성장 촉진요인 및 억제요인과 과제 및 기회에 관한 정보를 제공하는 데 도움이 됩니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- Porter's Five Forces 분석

- 고객사업에 영향을 주는 동향/혼란

- 생태계 분석

- 밸류체인 분석

- 규제 상황

- 무역 분석

- 가격 분석

- 기술 분석

- 특허 분석

- 사례 연구 분석

- 2025-2026년의 주된 회의와 이벤트

- 투자 및 자금조달 시나리오

- 생성형 AI/AI가 원예용 플라스틱 시장에 미치는 영향

- 주요 이해관계자와 구매 기준

- 거시경제 분석

- 2025년 미국 관세가 원예용 플라스틱 시장에 미치는 영향

제6장 원예용 플라스틱 시장(플라스틱 유형별)

- 소개

- 범용 플라스틱

- 엔지니어링 및 성능 플라스틱

제7장 원예용 플라스틱 시장(조성별)

- 소개

- 비충전

- 미네랄 충전

- 유리 섬유 강화

- 기타

제8장 원예용 플라스틱 시장(용도별)

- 소개

- 멀티 필름

- 관개 시스템

- 온실 및 터널 덮개

- 레이즈드 베드 및 가든 라이너

- 화분 및 용기

- 기타

제9장 원예용 플라스틱 시장(지역별)

- 소개

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제10장 경쟁 구도

- 개요

- 주요 참가 기업의 전략, 2022-2025년

- 시장 점유율 분석, 2024년

- 수익 분석, 2020-2024년

- 기업 평가와 재무지표, 2024년

- 제품/브랜드 비교

- 기업 평가 매트릭스: 주요 진입기업, 2024년

- 기업 평가 매트릭스: 스타트업/중소기업, 2024년

- 경쟁 시나리오

제11장 기업 프로파일

- 주요 진출기업

- KETER

- THE HC COMPANIES, INC.

- SCHEURICH GMBH & CO. KG

- ELHO BV

- HORST BRANDSTATTER GROUP

- GRIFFON CORPORATION INC.

- BERRY GLOBAL INC.

- RKW GROUP

- BASF

- ARMANDO ALVAREZ GROUP

- 기타 기업

- LANDMARK PLASTIC INC.

- EAST JORDAN PLASTICS, INC.

- CREO GROUP

- TO PLASTICS, INC.

- CAPI EUROPE

- HARSHDEEP INDIA

- EURO3PLAST SPA

- SA PLASTIKOR(PTY) LTD.

- COSMOPLAST UAE

- FINOLEX PLASSON

- KISAN

- TAIZHOU SHENGERDA PLASTIC CO., LTD.

- HOSCO INDIA

- TAIZHOU KEDI PLASTIC CO., LTD.

- VIP PLASTICS

제12장 부록

JHS 25.09.16The global garden plastics market is expected to increase from USD 0.90 billion in 2025 to USD 1.13 billion by 2030, exhibiting a compound annual growth rate (CAGR) of 4.8% between 2025 and 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) Volume (KT) |

| Segments | Plastic Type, Application, Composition, and Region |

| Regions covered | Asia Pacific, North America, Europe, the Middle East & Africa, and South America |

Most of this growth is attributed to the overall increase of DIY landscaping and container gardening for urban customers and limited mobility or space. In addition, the increased availability of plastic-based planters, fencing, storage bins, and garden accessories, made mostly from polyethylene, polypropylene, and recycled plastics, are addressing consumer interests for low-maintenance and durable products. Innovations in plastic formulations that offer improved UV resistance, color retention, and eco-friendliness are widening the market potential.

The continued outlook for the market is also aided by the growing availability of recycled and post-consumer plastic garden products, regulatory pressure for sustainable design, and manufacturer's efforts to embrace circular economy design. Demand should also grow in modular garden systems, smart irrigation plastics, and premium decorative containers, especially in developed markets with aging populations that spend on high levels on garden plastics.

"Glass-fiber-reinforced plastics to be second-fastest-growing composition segment"

Glass-fiber-reinforced plastics (GFRPs) is the second-highest expanding composition segment of the garden plastics market because of their robust mechanical properties, together with their enduring resistance to weathering. These reinforced materials are increasingly used for premium garden furniture, structural planters, fencing panels, and tool handles that require enhanced load-bearing and impact resistance capabilities. The growing interest among consumers for enduring garden solutions with esthetic value positions GFRP as an ideal solution that balances structural strength and design adaptability. These materials duplicate the appearance of wood and metal yet deliver reduced weight, together with superior corrosion protection which makes them desirable for upscale outdoor applications. The design-focused landscaping trend, combined with functional complexity drives the rising use of GFRP across premium product categories.

"Unfilled plastics segment to be fastest-growing in the garden plastics market"

The unfilled plastics industry has experienced significant growth throughout the garden plastics sector and is expected to benefit further during the forecast period. Because they are not reinforced and have no added fillers, unfilled plastics are a central part of the garden plastic packaging supply chain, because unfilled plastics are cheaper, easy to process, and recyclable. Usage of unfilled plastics continues to grow in the production of plant pots, garden borders, outdoor bins, and lightweight containers, especially where low structural integrity is not an issue. Because the molding processes can be varied and there are no composite formulations to consider, unfilled plastics provide fabrication versatility and composite input savings. Sustainability will remain a major issue for manufacturers and consumers as low-cost alternatives and unfilled plastics are filling a major gap in DIY gardening and small garden horticulture. Their comparative ease of use along with the growing acceptance of consumers to consider unfilled plastics as part of their eco-friendly gardening solution will continue to expedite the market growth of unfilled plastics..

"HDPE to be second-largest plastic type in the garden plastics market"

In tree planting in 2024, high-density polyethylene (HDPE) represented the second-largest plastic type to create products available in the garden plastics sector. The most relevant benefits of HDPE are that it is extensively available, regarded by some as a commodity-type plastic, and has the widest range of performance characteristics. HDPE is used in a wider variety of garden products such as garden furniture, pots, planters, and watering cans. HDPE has a unique combination of flexibility, durability, and weathering. HDPE is very suited for garden products intended for durable lifespans. HDPE is inexpensive compared to virgin raw granules, cheap to process, easy to process, and can be recycled. HDPE is a cheap, and environmentally sustainable option for manufacturers in garden plastics.

"North America to be second-largest regional market in 2024"

In 2024, North America was the second-largest regional market in the world garden plastics market. There is a consistent, strong demand for landscaping plastic products in the residential and commercial landscaping markets, particularly in the US and Canada. After the pandemic, there was an increase in home improvement projects, Do-It-Yourself (DIY) gardening, and a growing interest in sustainable landscaping practices. As a consequence, there has also been a rise in plastic gardening products, such as composters, raised garden beds, deck boxes, and outdoor furniture. Additionally, the growing environmental awareness of North American consumers has created higher motivation for regional producers of plastic products to promote innovation to produce plastic products. Due this, they are now using UV stabilized plastic and recyclable plastic products as these products can satisfy consumer needs for eco-conscious gardening. Furthermore, the larger retail brands that align with national and regional distributors, provide an extensive product distribution network that allows extensive product reach into the region.

By Company Type: Tier 1: 22%, Tier 2: 45%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Note: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Keter (Israel), THE HC COMPANIES, INC. (US), Scheurich GmbH & Co. KG (Germany), Elho B.V. (Netherlands), Horst Brandstatter Group (Germany), The AMES Companies (US), Berry Global Inc. (US), RKW Group (Germany), BASF (Germany), and Armando Alvarez Group (Span) are covered in the report. The study includes an in-depth competitive analysis of these key players in the garden plastics market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the garden plastics market, based on plastic type (commodity plastics and engineering plastics and performance plastics ), application (pots & containers, irrigation systems, greenhouse & tunnel coverings, raised beds & garden liners, and mulch films), composition (unfilled, mineral filled, and glass fiber-reinforced) and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the garden plastics market. A detailed analysis of the key industry players has been done to provide insights into their business overviews, products offered, and key strategies, such as partnerships, agreements, product launches, and acquisitions associated with the garden plastics market. This report covers a competitive analysis of the upcoming startups in the garden plastics market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall garden plastics market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Assessment of primary drivers (Rising popularity of home gardening and urban landscaping, Increasing consumer preference for lightweight, weather-resistant plastic products, Growth in residential construction and outdoor living spaces, Cost-effectiveness and ease of manufacturing of plastic garden products.) restraints (Fluctuating prices of raw plastic materials such as PP and PE, and Limited biodegradability of conventional plastics), opportunities (Rising demand for recycled and bio-based plastics in garden products, Growth in smart gardening tools and modular plastic planters, Innovation in UV-resistant and esthetic-enhanced garden plastics and Expansion into emerging markets with rising urban green space initiatives), and challenges (Increasing competition from biodegradable and natural alternatives, such as clay, metal, and wood, Balancing cost vs. sustainability in material selection , and Managing product durability against prolonged sun and moisture exposure).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the garden plastics market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the garden plastics market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the garden plastics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Keter (Israel), THE HC COMPANIES, INC. (US), Scheurich GmbH & Co. KG (Germany), Elho B.V. (Netherlands), Horst Brandstatter Group (Germany), The AMES Companies (US), Berry Global Inc. (US), RKW Group (Germany), BASF (Germany), and Armando Alvarez Group (Spain).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 GROWTH RATE ASSUMPTIONS/FORECAST

- 2.5.1 SUPPLY SIDE

- 2.5.2 DEMAND SIDE

- 2.6 RISK ASSESSMENT

- 2.7 LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GARDEN PLASTICS MARKET

- 4.2 GARDEN PLASTICS MARKET, BY PLASTIC TYPE

- 4.3 GARDEN PLASTICS MARKET, BY COMPOSITION

- 4.4 GARDEN PLASTICS MARKET, BY APPLICATION

- 4.5 GARDEN PLASTICS MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising popularity of home gardening and urban landscaping

- 5.2.1.2 Increasing preference for lightweight, weather-resistant plastic products

- 5.2.1.3 Growth in residential construction and outdoor living spaces

- 5.2.1.4 Cost-effectiveness and ease of manufacturing plastic garden products

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fluctuating prices of raw plastic materials such as PP and PE

- 5.2.2.2 Limited biodegradability of conventional plastics

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising demand for recycled and bio-based plastics in garden products

- 5.2.3.2 Growth in demand for smart gardening tools and modular plastic planters

- 5.2.3.3 Innovation in UV-resistant and esthetically enhanced garden plastics

- 5.2.3.4 Expansion into emerging markets with rising urban green space initiatives

- 5.2.4 CHALLENGES

- 5.2.4.1 Increasing competition from biodegradable and natural alternatives such as clay, metal, and wood

- 5.2.4.2 Balancing cost vs. sustainability in material selection

- 5.2.4.3 Managing product durability against prolonged sun and moisture exposure

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 BARGAINING POWER OF SUPPLIERS

- 5.3.2 BARGAINING POWER OF BUYERS

- 5.3.3 INTENSITY OF COMPETITIVE RIVALRY

- 5.3.4 THREAT OF NEW ENTRANTS

- 5.3.5 THREAT OF SUBSTITUTES

- 5.4 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 REGULATORY LANDSCAPE

- 5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7.2 REGULATIONS

- 5.7.2.1 California Proposition 65 - Safe Drinking Water and Toxic Enforcement Act of 1986

- 5.7.2.2 TSCA (Toxic Substances Control Act) - 15 U.S.C. 2601 et seq.

- 5.7.2.3 Canada's Single-Use Plastics Prohibition Regulations (SOR/2022-138)

- 5.7.2.4 REACH Regulation (EC) No 1907/2006 - Registration, Evaluation, Authorisation and Restriction of Chemicals

- 5.7.2.5 Packaging and Packaging Waste Directive (94/62/EC)

- 5.7.2.6 Circular Economy Action Plan (2020)

- 5.7.2.7 Brazil's National Solid Waste Policy (Law No. 12.305/2010)

- 5.7.2.8 Chile's EPR Law (Law No. 20.920)

- 5.7.2.9 India - Plastic Waste Management Rules, 2016 (Amended 2022)

- 5.7.2.10 China - Plastic Pollution Control Measures (2020-2025)

- 5.7.2.11 Japan - Containers and Packaging Recycling Law (Act No. 112 of 1995)

- 5.7.2.12 South Africa - Extended Producer Responsibility Regulations (2021)

- 5.7.2.13 UAE - Integrated Waste Management Strategy (2021-2040)

- 5.7.2.14 Saudi Arabia - SASO Technical Regulation for Biodegradable Plastics (M.A-156-16-03-01)

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 391733)

- 5.8.2 EXPORT SCENARIO (HS CODE 391733)

- 5.8.3 EXPORT SCENARIO (HS CODE 392690)

- 5.8.4 IMPORT SCENARIO (HS CODE 392690)

- 5.9 PRICING ANALYSIS

- 5.9.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION, 2024

- 5.9.2 AVERAGE SELLING PRICE TREND, BY REGION, 2024-2030

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Bio-Based Plastic Formulation

- 5.10.1.2 Recycled Polymer Integration (PCR & PIR)

- 5.10.2 COMPLEMENTARY TECHNOLOGIES

- 5.10.2.1 Smart Self-watering Systems

- 5.10.2.2 UV Stabilization and Weather-resistant Additives

- 5.10.3 ADJACENT TECHNOLOGIES

- 5.10.3.1 Smart Gardening & IoT Integration

- 5.10.3.2 Vertical Farming & Modular Urban Planters

- 5.10.1 KEY TECHNOLOGIES

- 5.11 PATENT ANALYSIS

- 5.11.1 METHODOLOGY

- 5.11.2 DOCUMENT TYPES

- 5.11.3 PUBLICATION TRENDS IN LAST 10 YEARS

- 5.11.4 INSIGHTS

- 5.11.5 LEGAL STATUS OF PATENTS

- 5.11.6 JURISDICTION ANALYSIS

- 5.11.7 TOP APPLICANTS

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 TRANSITIONING TO RECYCLED PLASTIC IN GARDEN STORAGE PRODUCTS BY KETER

- 5.12.2 IMPLEMENTING CLOSED-LOOP RECYCLING FOR PLASTIC PLANTERS BY THE HC COMPANIES

- 5.12.3 SHIFTING TO BIO-BASED COMPOSITE MATERIALS FOR GARDEN FURNITURE BY NARDI (ITALY)

- 5.13 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.14 INVESTMENT AND FUNDING SCENARIO

- 5.15 IMPACT OF GEN AI/AI ON GARDEN PLASTICS MARKET

- 5.15.1 INTRODUCTION

- 5.15.2 AI IN PRODUCT DESIGN AND CONSUMER INSIGHTS

- 5.15.3 AI-ENABLED MANUFACTURING AND SUPPLY CHAIN OPTIMIZATION

- 5.15.4 GENAI FOR SUSTAINABILITY AND CIRCULARITY

- 5.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.16.2 BUYING CRITERIA

- 5.17 MACROECONOMIC ANALYSIS

- 5.17.1 INTRODUCTION

- 5.17.2 GDP TRENDS AND FORECASTS

- 5.18 IMPACT OF 2025 US TARIFF ON GARDEN PLASTICS MARKET

- 5.18.1 INTRODUCTION

- 5.18.2 KEY TARIFF RATES

- 5.18.3 PRICE IMPACT ANALYSIS

- 5.18.4 IMPACT ON COUNTRY/REGION

- 5.18.4.1 US

- 5.18.4.2 China

- 5.18.4.3 Europe

- 5.18.5 IMPACT ON APPLICATIONS

- 5.18.5.1 Residential landscaping & gardening

- 5.18.5.2 Municipal landscaping

- 5.18.5.3 E-Commerce & Direct-to-Consumer (DTC) channels

6 GARDEN PLASTICS MARKET, BY PLASTIC TYPE

- 6.1 INTRODUCTION

- 6.2 COMMODITY PLASTICS

- 6.2.1 ABUNDANCE, COST-EFFICIENCY, AND DURABILITY TO DRIVE DEMAND

- 6.2.2 HDPE (HIGH-DENSITY POLYETHYLENE)

- 6.2.3 LDPE (LOW-DENSITY POLYETHYLENE)

- 6.2.4 PP (POLYPROPYLENE)

- 6.2.5 PVC (POLYVINYL CHLORIDE)

- 6.2.6 OTHER COMMODITY PLASTICS

- 6.3 ENGINEERING & PERFORMANCE PLASTICS

- 6.3.1 SUPERIOR MECHANICAL PROPERTIES, WEATHER RESISTANCE, AND LONGEVITY TO FUEL MARKET

- 6.3.2 ABS (ACRYLONITRILE BUTADIENE STYRENE)

- 6.3.3 PA (POLYAMIDE)

- 6.3.4 PVDF (POLYVINYLIDENE FLUORIDE)

- 6.3.5 POM (POLYOXYMETHYLENE)

- 6.3.6 OTHER ENGINEERING & PERFORMANCE PLASTICS

7 GARDEN PLASTICS MARKET, BY COMPOSITION

- 7.1 INTRODUCTION

- 7.2 UNFILLED

- 7.2.1 COST-EFFICIENT AND VERSATILE SOLUTION FOR MASS MARKET GARDEN PRODUCTS

- 7.3 MINERAL-FILLED

- 7.3.1 ENHANCED RIGIDITY, DIMENSIONAL STABILITY, AND UV RESISTANCE TO DRIVE ADOPTION

- 7.4 GLASS FIBER REINFORCED

- 7.4.1 HIGH TENSILE STRENGTH, DIMENSIONAL STABILITY, AND LONG-TERM DURABILITY TO BOOST ADOPTION

- 7.5 OTHER COMPOSITIONS

8 GARDEN PLASTICS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 MULCH FILMS

- 8.2.1 SUSTAINABLE AGRICULTURAL PRACTICES TO DRIVE ADOPTION

- 8.3 IRRIGATION SYSTEMS

- 8.3.1 EXPANDING WATER CONSERVATION PRACTICES TO BOOST MARKET

- 8.4 GREENHOUSE & TUNNEL COVERINGS

- 8.4.1 INCREASING CONTROLLED-ENVIRONMENT FARMING TO FUEL DEMAND

- 8.5 RAISED BEDS & GARDEN LINERS

- 8.5.1 RISING URBAN FARMING AND DIY LANDSCAPING TO PROPEL MARKET

- 8.6 POTS & CONTAINERS

- 8.6.1 GROWING URBAN GARDENING AND LANDSCAPING TO BOOST DEMAND

- 8.7 OTHER APPLICATIONS

9 GARDEN PLASTICS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 US

- 9.2.1.1 Demand for durable, weather-resistant, and sustainable plastic products to drive market

- 9.2.2 CANADA

- 9.2.2.1 Strong demand across residential landscaping, commercial horticulture, and urban infrastructure projects to drive growth

- 9.2.3 MEXICO

- 9.2.3.1 Rising demand for urban green infrastructure to boost growth

- 9.2.1 US

- 9.3 EUROPE

- 9.3.1 GERMANY

- 9.3.1.1 Strong domestic consumption, sustainability mandates, and rising demand across garden and outdoor living segments to propel market

- 9.3.2 FRANCE

- 9.3.2.1 Shift toward sustainable lifestyles, esthetic functionality, and urban gardening to fuel market

- 9.3.3 UK

- 9.3.3.1 Consumer shift toward sustainability, DIY culture, and durable outdoor living solutions to drive market

- 9.3.4 ITALY

- 9.3.4.1 Major line expansions and rising demand from home, garden, and construction segments to drive market growth

- 9.3.5 SPAIN

- 9.3.5.1 Multi-sectoral expansion and sustainability push to support growth

- 9.3.6 REST OF EUROPE

- 9.3.1 GERMANY

- 9.4 ASIA PACIFIC

- 9.4.1 CHINA

- 9.4.1.1 large-scale manufacturing capacity, growing domestic landscaping trends, and expanding global exports to boost market

- 9.4.2 JAPAN

- 9.4.2.1 Advanced innovation, demographic-driven product development, and strong shift toward environmental responsibility to fuel demand

- 9.4.3 INDIA

- 9.4.3.1 Rapid urbanization, government push for sustainability, and domestic innovation to drive growth

- 9.4.4 SOUTH KOREA

- 9.4.4.1 Demographic trends, rise of home-based lifestyle, and growing environmental consciousness to support market growth

- 9.4.5 REST OF ASIA PACIFIC

- 9.4.1 CHINA

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.5.1.1 Saudi Arabia

- 9.5.1.1.1 Reshaping urban spaces, boosting green infrastructure, and use of durable, eco-friendly plastic products to propel demand

- 9.5.1.2 UAE

- 9.5.1.2.1 Rising per capita income, expanding residential infrastructure, and thriving landscaping industry to fuel market growth

- 9.5.1.3 Rest of GCC countries

- 9.5.1.1 Saudi Arabia

- 9.5.2 SOUTH AFRICA

- 9.5.2.1 Renewed focus on sustainable urban living, water conservation, and public space development to drive demand

- 9.5.3 REST OF MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.6 SOUTH AMERICA

- 9.6.1 BRAZIL

- 9.6.1.1 Transition toward recyclable and durable outdoor goods to propel market

- 9.6.2 ARGENTINA

- 9.6.2.1 Growing demand for durable, UV-resistant, and weather-tolerant plastic products to boost market

- 9.6.3 REST OF SOUTH AMERICA

- 9.6.1 BRAZIL

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES, 2022-2025

- 10.3 MARKET SHARE ANALYSIS, 2024

- 10.4 REVENUE ANALYSIS, 2020-2024

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS, 2024

- 10.6 PRODUCT/BRAND COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 Type footprint

- 10.7.5.4 Application footprint

- 10.7.5.5 Composition footprint

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 KETER

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Solutions/Services offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 THE HC COMPANIES, INC.

- 11.1.2.1 Business overview

- 11.1.2.1.1 Products/Solutions/Services offered

- 11.1.2.2 Recent developments

- 11.1.2.2.1 Product launches

- 11.1.2.2.2 Deals

- 11.1.2.3 MnM view

- 11.1.2.3.1 Right to win

- 11.1.2.3.2 Strategic choices

- 11.1.2.3.3 Weaknesses and competitive threats

- 11.1.2.1 Business overview

- 11.1.3 SCHEURICH GMBH & CO. KG

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Solutions/Services offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Deals

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 ELHO B.V.

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Solutions/Services offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches

- 11.1.4.4 MnM view

- 11.1.4.4.1 Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 HORST BRANDSTATTER GROUP

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Solutions/Services offered

- 11.1.5.3 MnM view

- 11.1.5.3.1 Right to win

- 11.1.5.3.2 Strategic choices

- 11.1.5.3.3 Weaknesses and competitive threats

- 11.1.6 GRIFFON CORPORATION INC.

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Solutions/Services offered

- 11.1.6.3 MnM view

- 11.1.7 BERRY GLOBAL INC.

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Solutions/Services offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Deals

- 11.1.7.4 MnM view

- 11.1.8 RKW GROUP

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Solutions/Services offered

- 11.1.8.3 MnM view

- 11.1.9 BASF

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Solutions/Services offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches

- 11.1.9.4 MnM view

- 11.1.10 ARMANDO ALVAREZ GROUP

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Solutions/Services offered

- 11.1.10.3 MnM view

- 11.1.1 KETER

- 11.2 OTHER PLAYERS

- 11.2.1 LANDMARK PLASTIC INC.

- 11.2.2 EAST JORDAN PLASTICS, INC.

- 11.2.3 CREO GROUP

- 11.2.4 T.O. PLASTICS, INC.

- 11.2.5 CAPI EUROPE

- 11.2.6 HARSHDEEP INDIA

- 11.2.7 EURO3PLAST SPA

- 11.2.8 SA PLASTIKOR (PTY) LTD.

- 11.2.9 COSMOPLAST UAE

- 11.2.10 FINOLEX PLASSON

- 11.2.11 KISAN

- 11.2.12 TAIZHOU SHENGERDA PLASTIC CO., LTD.

- 11.2.13 HOSCO INDIA

- 11.2.14 TAIZHOU KEDI PLASTIC CO., LTD.

- 11.2.15 VIP PLASTICS

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS