|

시장보고서

상품코드

1822298

살선충제 시장 : 유형별, 선충 유형별, 시용 방식별, 제형별, 작물 유형별, 지역별 - 예측(-2030년)Nematicide Market by Type (Chemical, Biological), Nematode Type (Root-knot, Cyst, Lesion), Mode of Application (Drenching, Soil Dressing, Seed Treatment, Fumigation), Formulation, Crop Type and Region - Global Forecast to 2030 |

||||||

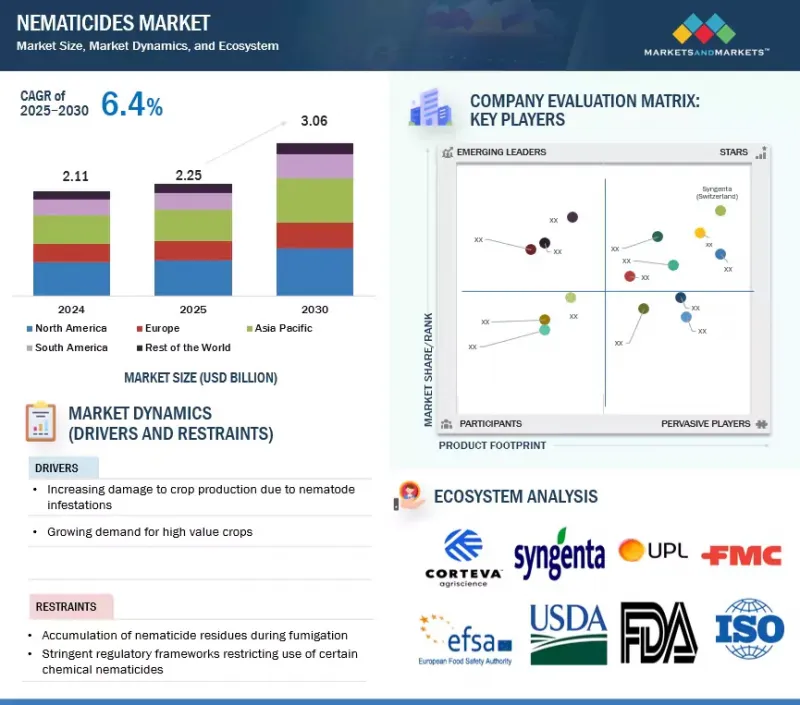

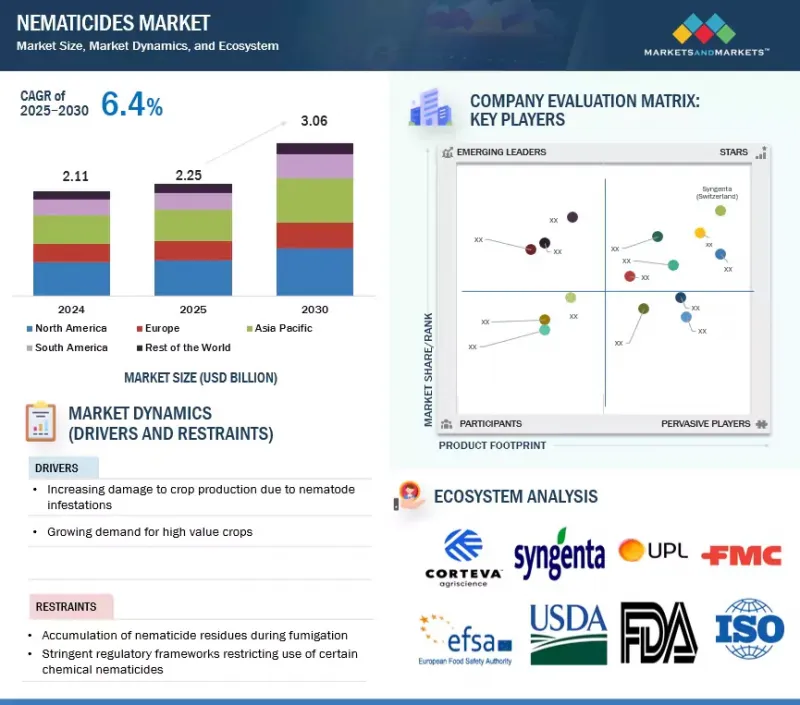

세계의 살선충제 시장 규모는 2025년에 약 22억 5,000만 달러로 평가되었고, 2030년까지 30억 6,000만 달러에 이를 것으로 예측되며, 예측 기간에 CAGR 6.4%의 성장이 전망됩니다. 시장 성장 촉진요인은 식물 기생성 선충에 의한 작물 손실 증가이며, 대두, 옥수수, 면화, 채소 등의 주요 작물 수량을 대폭 감소시키고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2025-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 달러, 킬로톤 |

| 부문 | 유형, 제제, 선충 유형, 시용 방식, 작물 유형, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 아시아태평양 |

세계 식량 수요 증가와 경작지 면적 감소로 인해 농부들은 헥타르당 생산성을 극대화해야 하는 상황에 처해 있으며, 효과적인 선충 관리가 필수적입니다. 과일, 채소, 플랜테이션 작물 등 고부가가치 작물은 특히 피해를 입기 쉬워 살선충제에 대한 수요가 더욱 증가하고 있습니다. 또한, 대규모 상업적 농업과 보호 재배 시스템의 확대로 인해 신뢰할 수 있는 선충 방제 솔루션에 대한 요구가 증가하고 있습니다.

또한, 종자 살선충제, 정밀농업, 종합적 해충관리(IPM)와 같은 첨단 기술의 급속한 채택도 중요한 촉진요인으로 작용하고 있으며, 이러한 기술은 적용 효율을 향상시키고 투입 비용을 절감합니다. 기존 훈증제에 대한 규제 제한도 정부의 이니셔티브와 지속가능성 목표에 힘입어 보다 안전한 바이오 살선충제로의 전환을 가속화하고 있습니다. 또한, 세계 농약 기업들의 지속적인 제품 혁신, 전략적 파트너십, 투자로 인해 화학적/생물학적 살선충제 솔루션의 가용성이 확대되고 시장 성장이 강화되고 있습니다.

"적용 방식별로는 종자 처리 부문이 예측 기간 동안 빠르게 성장할 것으로 예측됩니다. "

종자 처리 방식은 효율성, 비용 효율성, 작물에 초기 단계 보호 기능을 제공하는 능력으로 인해 살선충제 시장에서 빠르게 성장하고 있습니다. 종자처리에서는 기존의 토양살포나 엽면살포와 달리 살선충제를 종자에 직접 정확하게 살포할 수 있기 때문에 균일한 살포가 가능하여 필요한 약제의 총량을 줄일 수 있습니다. 이 표적화된 접근 방식은 환경에 미치는 영향을 최소화하고 발아율을 높이며 식물의 정착을 강화하여 작물 수확량을 향상시킬 수 있습니다. 지속 가능한 농법에 대한 수요 증가와 과도한 화학물질 사용을 줄여야 한다는 규제 압력으로 인해 종자 적용 기술 채택이 더욱 가속화되고 있습니다. 또한, 제형 기술의 발전과 생물학적 살선충제의 종자 처리에의 통합으로 인해, 특히 종합적인 해충 관리 솔루션을 원하는 농부들 사이에서 그 호소력이 커지고 있습니다. 세계 기업들이 혁신적인 종자 처리 솔루션에 투자하고 있는 만큼, 이 적용 방식은 선충제 시장에서 강력한 성장세를 이어갈 것으로 예측됩니다.

"선충 유형별로 보면, 고양이 부센츄리 부문이 예측 기간 동안 시장을 주도할 것으로 추정됩니다. "

선충 유형별로 보면, 고양이 부세균의 광범위한 분포와 농업 생산성에 미치는 심각한 영향으로 인해 고양이 부세균 부문이 선충 시장에서 가장 큰 점유율을 차지할 것으로 추정됩니다. 이 선충은 과일, 채소, 곡물, 콩류 등 다양한 작물을 감염시켜 뿌리에 혹을 형성하고 성장을 억제하여 수확량을 크게 감소시킵니다. 다양한 농업 기후 조건에서 증식할 수 있는 능력으로 인해 세계에서 가장 파괴적인 식물 기생 선충 그룹 중 하나가 되었습니다. 고양이벼룩의 침입에 매우 취약한 고부가가치 작물 재배가 증가함에 따라 효과적인 방제 솔루션에 대한 수요가 더욱 가속화되고 있습니다. 농부들은 이러한 해충을 관리하기 위해 화학적/생물학적 살선충제에 대한 의존도를 높이고 있으며, 종자 처리와 종합적인 해충 관리 기법의 발전에 힘입어 이러한 해충을 관리할 수 있게 되었습니다. 지속적인 제품 혁신과 바이오 대체품의 도입으로 내성 및 환경 안전에 대한 우려도 해소되고 있으며, 선충 유형 부문에서 네코부센츄의 우위는 더욱 강화되고 있습니다.

"북미가 가장 큰 시장 점유율을 차지할 것으로 추정되며, 유럽은 예측 기간 동안 가장 빠르게 성장하는 시장이 될 것으로 예측됩니다. "

북미는 농업 부문이 고도로 상업화되어 있고, 채소, 과일, 옥수수, 콩 등 고부가가치 작물 재배가 활발하여 세계 선충제 시장을 선도할 것으로 추정됩니다. 이 지역의 농부들은 식물 기생 선충, 특히 고양이 선충과 시스트 선충으로 인한 수확량 감소에 직면하고 있으며, 이로 인해 효과적인 방제 솔루션에 대한 강력한 수요가 증가하고 있습니다. 종자 살선충제, 종합 해충 관리 시스템 등 첨단 농업 기술의 채택이 시장 성장을 더욱 촉진하고 있습니다.

세계의 살선충제 시장에 대해 조사 분석했으며, 주요 촉진요인과 억제요인, 경쟁 구도, 향후 동향 등의 정보를 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 지견

- 살선충제 시장의 매력적인 기회

- 북미의 살선충제 시장 : 유형별, 국가별

- 살선충제 시장 : 주요 국가별

- 살선충제 시장 : 유형별, 지역별

- 살선충제 시장 : 선충 유형별, 지역별

- 살선충제 시장 : 제형별, 지역별

- 살선충제 시장 : 시용 방식별, 지역별

- 살선충제 시장 : 작물별, 지역별

제5장 시장 개요

- 서론

- 거시경제 지표

- 해충 공격에 대한 방어를 목적으로 한 살충제 채택

- 외국 간접투자

- 선충에 기인한 세계의 작물 손실

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 살선충제 시장에 대한 AI/생성형 AI의 영향

- 서론

- 살선충제 시장에서의 생성형 AI 사용

- 사례 연구 분석

제6장 산업 동향

- 서론

- 2025년 미국 관세의 영향 - 살선충제 시장

- 서론

- 주요 관세율

- 가격 영향 분석

- 국가/지역에 대한 영향

- 최종 이용 산업에 대한 영향

- 밸류체인 분석

- 연구개발

- 제조

- 유통

- 마케팅 세일즈

- 애프터 서비스

- 무역 분석

- HS코드 3808 수출 시나리오

- HS코드 3808 수입 시나리오

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 가격 결정 분석

- 살선충제 가격대 : 주요 기업별(2024년)

- 가격 동향 : 살선충제 유형별(2020년-2024년)

- 살선충제 가격 동향 : 지역별(2020년-2024년)

- 생태계 분석

- 수요측

- 공급측

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 특허 분석

- 주요 컨퍼런스 및 이벤트(2025년-2026년)

- 규제 상황

- 규제기관, 정부기관, 기타 조직

- 북미

- 유럽

- 아시아태평양

- 남미

- 기타 지역

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 투자 및 자금조달 시나리오

- 사례 연구 분석

제7장 살선충제 시장 : 유형별

- 서론

- 화학적

- 생물학적

제8장 살선충제 시장 : 선충 유형별

- 서론

- ROOT-KNOT NEMATODES

- CYST NEMATODES

- LESION NEMATODES

- 기타 선충 유형

제9장 살선충제 시장 : 제형별

- 서론

- 입상

- 액체

제10장 살선충제 시장 : 시용 방식별

- 서론

- 훈증

- 관주

- 객지

- 종자 처리

- 기타 시용 방식

제11장 살선충제 시장 : 작물별

- 서론

- 곡류

- 지방종자 및 콩류

- 과일 및 채소

- 기타 작물

제12장 살선충제 시장 : 지역별

- 서론

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 아르헨티나

- 브라질

- 기타 남미

- 기타 지역

- 중동

- 아프리카

제13장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석(2020년-2024년)

- 시장 점유율 분석(2024년)

- 기업 평가 매트릭스 : 주요 기업(2024년)

- 기업 평가 매트릭스 : 스타트업/중소기업(2024년)

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 경쟁 시나리오와 동향

제14장 기업 개요

- 주요 기업

- BASF SE

- SYNGENTA

- CORTEVA

- UPL

- BAYER AG

- FMC CORPORATION

- SUMITOMO CHEMICAL CO., LTD.

- NUFARM

- AMERICAN VANGUARD CORPORATION

- NOVONESIS GROUP

- BIOCERES CROP SOLUTIONS

- GOWAN COMPANY

- CERTIS USA L.L.C.

- LALLEMAND INC

- AECI PLANT HEALTH

- 기타 기업

- ANDERMATT GROUP AG

- IPL BIOLOGICALS

- PHERONYM, INC.

- AGRILIFE

- CROP IQ TECHNOLOGY

- ROVENSA NEXT

- BIONEMA

- BIOCONSORTIA

- VIVE CROP PROTECTION INC.

- VEGALAB SA

제15장 인접 시장과 관련 시장

- 서론

- 제한 사항

- 작물 보호 화학제품 시장

- 시장의 정의

- 시장 개요

- 생물학적 살충제 시장

- 시장의 정의

- 시장 개요

제16장 부록

LSH 25.09.30The market for nematicides is estimated to be USD 2.25 billion in 2025 and is projected to reach USD 3.06 billion by 2030, at a CAGR of 6.4% during the forecast period. The market is driven by rising crop losses caused by plant-parasitic nematodes, significantly reducing yields in major crops such as soybeans, corn, cotton, and vegetables.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD) and Volume (KT) |

| Segments | By Type, Formulation, Nematode Type, Mode of Application, Crop Type, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Rest of the World |

With growing global food demand and shrinking arable land, farmers are under increasing pressure to maximize productivity per hectare, making effective nematode management essential. High-value crops like fruits, vegetables, and plantation crops are particularly vulnerable, further boosting the demand for nematicides. In addition, the expansion of large-scale commercial farming and protected cultivation systems has heightened the need for reliable nematode control solutions.

Another key driver is the rapid adoption of advanced technologies such as seed-applied nematicides, precision agriculture, and integrated pest management (IPM), which improve application efficiency and reduce input costs. Regulatory restrictions on traditional fumigants have also accelerated the shift toward safer, bio-based nematicides, supported by government initiatives and sustainability goals. Furthermore, continuous product innovations, strategic partnerships, and investments by global agrochemical companies are expanding the availability of both chemical and biological nematicide solutions, thereby reinforcing market growth.

"By mode of application, the seed treatment segment is projected to grow at a significant rate during the forecast period"

Seed treatment as a mode of application is growing at a significant rate in the nematicides market, driven by its efficiency, cost-effectiveness, and ability to provide early-stage protection to crops. Unlike traditional soil or foliar applications, seed treatment enables precise application of nematicides directly onto seeds, ensuring uniform coverage and reducing the overall quantity of chemicals required. This targeted approach minimizes environmental impact, enhances germination rates, and strengthens plant establishment, thereby improving crop yield potential. Rising demand for sustainable agricultural practices and regulatory pressures to reduce excessive chemical usage have further accelerated the adoption of seed-applied technologies. Additionally, advancements in formulation technology and the integration of biological nematicides into seed treatments have broadened their appeal, particularly among farmers seeking integrated pest management solutions. With global players investing in innovative seed treatment solutions, this mode of application is expected to continue its strong growth trajectory in the nematicides market.

"By nematode type, the root-knot nematodes segment is estimated to lead the market during the forecast period"

By nematode type, the root-knot nematodes segment is estimated to account for the largest share of the nematicides market due to the wide distribution and severe impact of root-knot nematodes on agricultural productivity. These nematodes infect a broad range of crops, including fruits, vegetables, cereals, and pulses, causing gall formation on roots, stunted growth, and significant yield losses. Their ability to thrive in diverse agro-climatic conditions makes them one of the most destructive groups of plant-parasitic nematodes globally. The rising cultivation of high-value crops that are highly susceptible to root-knot nematode infestations has further accelerated the demand for effective control solutions. Farmers are increasingly relying on both chemical and biological nematicides to manage these pests, supported by advancements in seed treatments and integrated pest management practices. Continuous product innovations and the introduction of bio-based alternatives are also addressing concerns over resistance and environmental safety, reinforcing root-knot nematodes' dominance in the nematode type segment.

"North America is estimated to hold the largest market share, while Europe is expected to be the fastest-growing market during the forecast period"

North America is estimated to lead the global nematicides market, driven by its highly commercialized agriculture sector and extensive cultivation of high-value crops such as vegetables, fruits, corn, and soybeans. Farmers in the region face significant yield losses from plant-parasitic nematodes, particularly root-knot and cyst nematodes, which have fueled strong demand for effective control solutions. The adoption of advanced farming technologies, including seed-applied nematicides and integrated pest management systems, has further strengthened the market's growth. Additionally, the presence of leading agrochemical companies with strong product portfolios and continuous innovations supports regional dominance. Stringent regulations on chemical pesticide use have also accelerated the shift toward biological nematicides, aligning with consumer demand for residue-free produce. These factors position North America as the leading market for nematicides, reflecting both the scale of production and advanced crop protection practices.

The European market is projected to grow at the highest rate, supported by strong regulatory backing for sustainable agriculture and rising adoption of biological crop protection solutions. The European Union's strict restrictions on conventional chemical pesticides have increased reliance on bio-based and environmentally friendly nematicides, driving innovation and market expansion. Countries such as Spain, Italy, and France, with large-scale fruit and vegetable cultivation, face significant nematode infestations, creating high demand for effective and safer alternatives. The region is also witnessing rapid integration of precision agriculture practices, enabling targeted nematicide application and minimizing environmental impact. Furthermore, increasing consumer preference for organic and residue-free food products is encouraging growers to invest in biological nematicide solutions. With active support from government policies and continuous R&D investments, Europe is positioned to emerge as the fastest-growing region in the global nematicides market.

Break-up of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the nematicides market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors- 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World - 10%

Prominent companies in the market include BASF SE (Germany), Bayer AG (Germany), UPL (India), T. STANES AND COMPANY LIMITED (India), Corteva (US), Koppert (Netherlands), FMC Corporation (US), Nufarm (Australia), Syngenta (Switzerland), American Vanguard Corporation (US), Sumitomo Chemicals (Japan), Lallemand Inc. (Canada), Novonesis Group (Denmark), Biobest Group NV (Belgium), and PI Industries (India).

Other players include IPL Biologicals (India), Bioceres Crop Solutions (Argentina), Rovensa Next (Spain), Bionema (UK), BioConsortia (US), Certis USA L.L.C. (US), Futureco Bioscience (Spain), Gowan Company (US), AgriLife (India), and Andermatt Group AG (Switzerland).

Research Coverage

This research report categorizes the nematicides market by type (chemical and biological), nematode type (root-knot nematodes, cyst nematodes, lesion nematodes, and other nematodes), formulation (granular and liquid), mode of application (fumigation, soil dressing, drenching, seed treatment, and other modes of application), crop type (cereals & grains, oilseeds, fruits & vegetables, and other crop types), and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding drivers, restraints, challenges, and opportunities influencing the growth of the nematicides market.

A detailed analysis of the key industry players was done to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments associated with the nematicides market. This report covers competitive analysis of upcoming startups in the nematicides market ecosystem. Furthermore, the study also covers industry-specific trends such as technology analysis, ecosystem and market mapping, and patent and regulatory landscape, among others.

Reasons to buy this report

The report will help market leaders/new entrants in this market by providing information on the closest approximations of the revenue numbers for the overall nematicides and the subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

It provides insights into the following pointers:

- Analysis of key drivers (high demand for high-value crops), restraints (varying government regulations), opportunities (use of plant-based nematicides in organic agriculture), and challenges (resistance development) influencing the growth of the nematicides market

- New Product Launch/Innovation: Detailed insights on research & development activities and new product launches in the nematicides market

- Market Development: Comprehensive information about lucrative markets - analysis of the nematicides market across varied regions

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the nematicides market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparisons, and product footprints of leading players such as BASF (Germany), Syngenta (Switzerland), Bayer AG (Germany), UPL (India), Corteva (US), FMC Corporation (US), and others in the nematicides market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.5.1 CURRENCY/VALUE UNIT

- 1.5.2 VOLUME CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of primaries

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN NEMATICIDES MARKET

- 4.2 NORTH AMERICA: NEMATICIDES MARKET, BY TYPE & COUNTRY

- 4.3 NEMATICIDE MARKETS, BY KEY COUNTRY

- 4.4 NEMATICIDES MARKET, BY TYPE AND REGION

- 4.5 NEMATICIDES MARKET, BY NEMATODE TYPE AND REGION

- 4.6 NEMATICIDES MARKET, BY FORMULATION AND REGION

- 4.7 NEMATICIDES MARKET, BY MODE OF APPLICATION AND REGION

- 4.8 NEMATICIDES MARKET, BY CROP TYPE AND REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 ADOPTION OF PESTICIDES FOR DEFENSE AGAINST PEST ATTACKS

- 5.2.2 FOREIGN DIRECT INVESTMENTS

- 5.3 GLOBAL CROP LOSSES DUE TO NEMATODES

- 5.4 MARKET DYNAMICS

- 5.4.1 DRIVERS

- 5.4.1.1 Strong demand for high-value crops

- 5.4.1.2 Rising demand for low-cost crop protection solutions

- 5.4.1.3 Increasing damage to crop production due to nematode infestations

- 5.4.1.4 Integration of nematicides with modern farming practices

- 5.4.1.5 Advancements in biological nematicides

- 5.4.2 RESTRAINTS

- 5.4.2.1 Technological limitations in using biological products

- 5.4.2.2 Stringent government regulations

- 5.4.3 OPPORTUNITIES

- 5.4.3.1 Use of plant-based nematicides in organic agriculture and horticulture

- 5.4.3.2 Resistance to crop protection chemicals

- 5.4.3.3 Rising demand for biological solutions

- 5.4.4 CHALLENGES

- 5.4.4.1 Expanding adoption of GM crops to reduce dependence on conventional crop protection chemicals

- 5.4.4.2 Lack of awareness and low utilization of biologicals

- 5.4.4.3 Inconsistent field performance

- 5.4.1 DRIVERS

- 5.5 IMPACT OF AI/GEN AI ON NEMATICIDES MARKET

- 5.5.1 INTRODUCTION

- 5.5.2 USE OF GEN AI IN NEMATICIDES MARKET

- 5.5.3 CASE STUDY ANALYSIS

- 5.5.3.1 Revolutionizing nematode management: Syngenta's satellite-powered precision tool

- 5.5.3.2 Agmatix and BASF partnered to develop AI-powered detection of soybean cyst nematode

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 IMPACT OF 2025 US TARIFF - NEMATICIDES MARKET

- 6.2.1 INTRODUCTION

- 6.2.2 KEY TARIFF RATES

- 6.2.3 PRICE IMPACT ANALYSIS

- 6.2.4 IMPACT ON COUNTRY/REGION

- 6.2.4.1 US

- 6.2.4.2 Europe

- 6.2.4.3 Asia Pacific

- 6.2.5 IMPACT ON END-USE INDUSTRIES

- 6.3 VALUE CHAIN ANALYSIS

- 6.3.1 RESEARCH & DEVELOPMENT

- 6.3.2 MANUFACTURING

- 6.3.3 DISTRIBUTION

- 6.3.4 MARKETING & SALES

- 6.3.5 POST-SALE SERVICES

- 6.4 TRADE ANALYSIS

- 6.4.1 EXPORT SCENARIO OF HS CODE 3808

- 6.4.2 IMPORT SCENARIO OF HS CODE 3808

- 6.5 TECHNOLOGY ANALYSIS

- 6.5.1 KEY TECHNOLOGIES

- 6.5.1.1 RNAi-based nematicides

- 6.5.2 COMPLEMENTARY TECHNOLOGIES

- 6.5.2.1 Precision agriculture tools

- 6.5.3 ADJACENT TECHNOLOGIES

- 6.5.3.1 Seed treatment technologies

- 6.5.1 KEY TECHNOLOGIES

- 6.6 PRICING ANALYSIS

- 6.6.1 PRICING RANGE OF NEMATICIDE TYPES, BY KEY PLAYER, 2024

- 6.6.2 PRICING TREND, BY NEMATICIDE TYPE, 2020-2024

- 6.6.3 PRICING TREND OF NEMATICIDE PRODUCTS, BY REGION, 2020-2024

- 6.7 ECOSYSTEM ANALYSIS

- 6.7.1 DEMAND SIDE

- 6.7.2 SUPPLY SIDE

- 6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.9 PATENT ANALYSIS

- 6.10 KEY CONFERENCES & EVENTS, 2025-2026

- 6.11 REGULATORY LANDSCAPE

- 6.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11.2 NORTH AMERICA

- 6.11.2.1 US

- 6.11.2.2 Canada

- 6.11.3 EUROPE

- 6.11.3.1 UK

- 6.11.3.2 France

- 6.11.3.3 Russia

- 6.11.4 ASIA PACIFIC

- 6.11.4.1 India

- 6.11.4.2 China

- 6.11.4.3 Australia

- 6.11.5 SOUTH AMERICA

- 6.11.5.1 Brazil

- 6.11.6 REST OF WORLD

- 6.11.6.1 South Africa

- 6.11.6.2 UAE

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREAT OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF BUYERS

- 6.12.4 BARGAINING POWER OF SUPPLIERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.13.2 BUYING CRITERIA

- 6.14 INVESTMENT AND FUNDING SCENARIO

- 6.15 CASE STUDY ANALYSIS

- 6.15.1 NUFARM LAUNCHED EVOLVANCE BIOLOGICAL BIONEMATICIDE TO ENHANCE CROP RESILIENCE

- 6.15.2 SYNGENTA LAUNCHED TYMIRIUM TECHNOLOGY FOR SUSTAINABLE NEMATODE AND FUNGAL DISEASE CONTROL

7 NEMATICIDES MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 CHEMICAL

- 7.2.1 LONGER RESIDUAL ACTIVITY AND QUICK MODE OF ACTION AGAINST NEMATODES TO DRIVE SEGMENT

- 7.2.2 FUMIGANTS

- 7.2.2.1 Broad-spectrum functionality of fumigants against nematodes to drive market

- 7.2.2.2 Methyl bromide

- 7.2.2.2.1 Ability to penetrate quickly into sorptive materials at normal atmospheric pressure to drive segment

- 7.2.2.3 Metam sodium

- 7.2.2.3.1 Increasing adoption in agriculture sector to boost market

- 7.2.2.4 1-3-Dichloropropene

- 7.2.2.4.1 Minimum soil contamination and air dispersion to drive segment

- 7.2.2.5 Other fumigant types

- 7.2.3 NON-FUMIGANTS

- 7.2.3.1 Carbamates

- 7.2.3.1.1 Low toxicity to non-target organisms and selective action against nematodes

- 7.2.3.2 Organophosphates

- 7.2.3.2.1 Fast absorption rate and immediate protection against nematode feeding damage

- 7.2.3.3 Abamectin (Next-gen)

- 7.2.3.3.1 Targeted activity against nematodes, disrupting their nerve and muscle functions

- 7.2.3.4 SDHI (Next-gen)

- 7.2.3.4.1 Disrupting energy production in nematodes, leading to their effective control

- 7.2.3.4.2 Fluopyram

- 7.2.3.4.3 Cyclobutrifluram

- 7.2.3.1 Carbamates

- 7.2.4 OTHER CHEMICALS

- 7.2.4.1 Fluoroalkenyl compounds

- 7.2.4.2 Fluensulfone

- 7.2.4.3 Tioxazafen

- 7.2.4.4 Fluazaindolizine

- 7.3 BIOLOGICAL

- 7.3.1 STRINGENT REGULATORY POLICIES ON CONVENTIONAL AGROCHEMICALS TO DRIVE MARKET

- 7.3.2 MICROBIALS

- 7.3.2.1 High adoption of sustainable agricultural techniques to fuel growth

- 7.3.3 BIOCHEMICALS

- 7.3.3.1 Residue-free nematode management by biochemicals to propel growth

8 NEMATICIDES MARKET, BY NEMATODE TYPE

- 8.1 INTRODUCTION

- 8.2 ROOT-KNOT NEMATODES

- 8.2.1 RISING NEED TO REDUCE ECONOMIC LOSSES AND ENHANCE CROP QUALITY TO DRIVE DEMAND FOR NEMATICIDES

- 8.3 CYST NEMATODES

- 8.3.1 LARGE-SCALE ECONOMIC LOSSES AND LOWER YIELD QUALITY DUE TO CYST NEMATODE INFESTATION TO INCREASE DEMAND

- 8.4 LESION NEMATODES

- 8.4.1 WIDE HOST RANGE AND PRESENCE IN TEMPERATE AND TROPICAL ENVIRONMENTS TO DRIVE MARKET

- 8.5 OTHER NEMATODE TYPES

9 NEMATICIDES MARKET, BY FORMULATION

- 9.1 INTRODUCTION

- 9.2 GRANULAR

- 9.2.1 GOOD STORAGE VIABILITY TO DRIVE SEGMENT GROWTH

- 9.3 LIQUID

- 9.3.1 GREATER DEGREE OF DISPERSION PROPERTY OFFERED BY LIQUID NEMATICIDES TO DRIVE DEMAND

10 NEMATICIDES MARKET, BY MODE OF APPLICATION

- 10.1 INTRODUCTION

- 10.2 FUMIGATION

- 10.2.1 LOWER COSTS INVOLVED IN FUMIGATION FOR NEMATODE CONTROL TO PROPEL GROWTH

- 10.3 DRENCHING

- 10.3.1 PRECISE APPLICATION AND DEEP PENETRATION OF NEMATICIDES ON TARGET NEMATODES TO DRIVE DEMAND

- 10.4 SOIL DRESSING

- 10.4.1 EFFECTIVE MANAGEMENT OF EARLY SEASON NEMATODE TO DRIVE DEMAND

- 10.5 SEED TREATMENT

- 10.5.1 SAFER APPLICATION AND EARLY SEASON PROTECTION AGAINST NEMATODE TO AUGMENT DEMAND

- 10.6 OTHER MODES OF APPLICATION

11 NEMATICIDES MARKET, BY CROP TYPE

- 11.1 INTRODUCTION

- 11.2 CEREALS & GRAINS

- 11.2.1 RISE IN CONSUMPTION AND EXTENSIVE CULTIVATION AREA TO DRIVE MARKET

- 11.2.2 CORN

- 11.2.3 WHEAT

- 11.2.4 RICE

- 11.2.5 OTHER CEREALS & GRAINS

- 11.3 OILSEEDS & PULSES

- 11.3.1 INCREASE IN CONSUMPTION OF PROTEIN- AND HEALTHY FAT-RICH MEALS TO DRIVE SEGMENTAL GROWTH

- 11.3.2 SOYBEAN

- 11.3.3 SUNFLOWER

- 11.3.4 OTHER OILSEEDS & PULSES

- 11.4 FRUITS & VEGETABLES

- 11.4.1 RISE IN EXPORTS OF FRESH, FROZEN, AND PROCESSED FRUITS & VEGETABLES FROM SOUTH ASIA TO DRIVE DEMAND

- 11.4.2 POME FRUITS

- 11.4.3 CITRUS FRUITS

- 11.4.4 LEAFY VEGETABLES

- 11.4.5 BERRIES

- 11.4.6 ROOTS & TUBERS VEGETABLES

- 11.4.7 OTHER FRUITS & VEGETABLES

- 11.5 OTHER CROP TYPES

12 NEMATICIDES MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Research undertaken to introduce nematode-resistant vegetables and field crops to drive market

- 12.2.2 CANADA

- 12.2.2.1 Losses in high-value cash crops to drive adoption of nematicides

- 12.2.3 MEXICO

- 12.2.3.1 Increase in root-knot and root-lesion nematode infestation in wheat to fuel market

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Environment-friendly and organic farming practices to cater to nematode attacks in field crops

- 12.3.2 UK

- 12.3.2.1 High demand for nematicides since farmers still use traditional farming methods

- 12.3.3 FRANCE

- 12.3.3.1 Extensive government funds in R&D to devise sustainable methods for nematode control

- 12.3.4 SPAIN

- 12.3.4.1 Surge in government initiatives to encourage use of biological nematicides

- 12.3.5 ITALY

- 12.3.5.1 Adoption of sustainable farming procedures to drive market

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Rise in infestation by root-knot nematodes in crops to propel market

- 12.4.2 JAPAN

- 12.4.2.1 Rising demand for novel nematicides catering to long-term viability of crops to drive growth

- 12.4.3 INDIA

- 12.4.3.1 Protected environment in polyhouses to create favorable environment for root-knot nematodes

- 12.4.4 AUSTRALIA & NEW ZEALAND

- 12.4.4.1 Increase in canola losses due to nematode attacks to support adoption of nematicides

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 SOUTH AMERICA

- 12.5.1 ARGENTINA

- 12.5.1.1 Increasing focus on soybean and corn cultivation to boost demand for nematicides

- 12.5.2 BRAZIL

- 12.5.2.1 High adoption of genetically modified crops to increase usage of nematicides

- 12.5.3 REST OF SOUTH AMERICA

- 12.5.1 ARGENTINA

- 12.6 REST OF THE WORLD (ROW)

- 12.6.1 MIDDLE EAST

- 12.6.1.1 Rise in population, high dependency on imports, and yield loss due to nematodes to boost market

- 12.6.2 AFRICA

- 12.6.2.1 Growth in demand for vegetable crops to drive growth

- 12.6.1 MIDDLE EAST

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Type footprint

- 13.5.5.4 Formulation footprint

- 13.5.5.5 Crop type footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPANY VALUATION AND FINANCIAL METRICS

- 13.8 BRAND/PRODUCT COMPARISON

- 13.9 COMPETITIVE SCENARIO AND TRENDS

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BASF SE

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 SYNGENTA

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 CORTEVA

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 UPL

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 BAYER AG

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 FMC CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.3.2 Expansions

- 14.1.7 SUMITOMO CHEMICAL CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.7.3.2 Expansions

- 14.1.8 NUFARM

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Other developments

- 14.1.9 AMERICAN VANGUARD CORPORATION

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.10 NOVONESIS GROUP

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.11 BIOCERES CROP SOLUTIONS

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches

- 14.1.11.3.2 Deals

- 14.1.12 GOWAN COMPANY

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.13 CERTIS USA L.L.C.

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Deals

- 14.1.13.3.2 Other developments

- 14.1.14 LALLEMAND INC

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches

- 14.1.15 AECI PLANT HEALTH

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.1 BASF SE

- 14.2 OTHER PLAYERS

- 14.2.1 ANDERMATT GROUP AG

- 14.2.1.1 Business overview

- 14.2.1.2 Products offered

- 14.2.2 IPL BIOLOGICALS

- 14.2.2.1 Business overview

- 14.2.2.2 Products offered

- 14.2.2.3 Recent developments

- 14.2.2.3.1 Expansions

- 14.2.3 PHERONYM, INC.

- 14.2.3.1 Business overview

- 14.2.3.2 Products offered

- 14.2.4 AGRILIFE

- 14.2.4.1 Business overview

- 14.2.4.2 Products offered

- 14.2.5 CROP IQ TECHNOLOGY

- 14.2.5.1 Business overview

- 14.2.5.2 Products offered

- 14.2.5.3 Recent developments

- 14.2.5.3.1 Expansions

- 14.2.6 ROVENSA NEXT

- 14.2.7 BIONEMA

- 14.2.8 BIOCONSORTIA

- 14.2.9 VIVE CROP PROTECTION INC.

- 14.2.10 VEGALAB SA

- 14.2.1 ANDERMATT GROUP AG

15 ADJACENT AND RELATED MARKETS

- 15.1 INTRODUCTION

- 15.2 LIMITATIONS

- 15.3 CROP PROTECTION CHEMICALS MARKET

- 15.3.1 MARKET DEFINITION

- 15.3.2 MARKET OVERVIEW

- 15.4 BIORATIONAL PESTICIDES MARKET

- 15.4.1 MARKET DEFINITION

- 15.4.2 MARKET OVERVIEW

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 AVAILABLE CUSTOMIZATION

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS