|

시장보고서

상품코드

1830045

탄소 포집 재료 시장 : 프로세스별, 재료별, 기술별, 최종사용자별, 지역별 - 예측(-2030년)Carbon Capture Materials Market by Material, Process, Technique, End-Use Industry & Region - Forecast to 2030 |

||||||

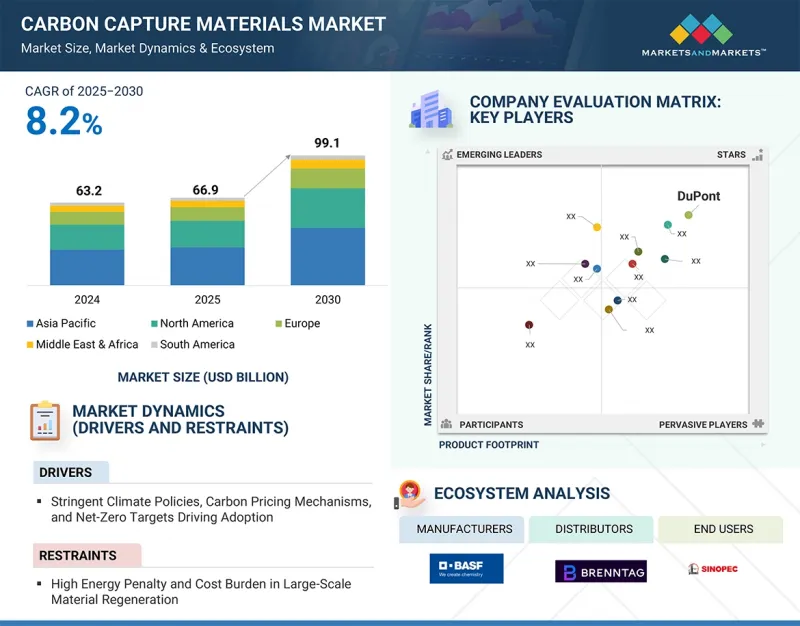

탄소 포집 재료 시장 규모는 2025년 669억 470만 달러에서 2030년에는 990억 9,850만 달러로 성장하고, 예측 기간 중 연평균 복합 성장률(CAGR)은 8.2%를 보일 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 금액(100만 달러/10억 달러), 킬로톤 |

| 부문 | 프로세스별, 재료별, 기술별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미 |

탄소 포집 재료 시장을 가속화하는 주요 요인으로는 엄격한 기후 정책, 기업의 지속가능성에 대한 약속 증가, 기술 발전 등이 있습니다. 엄격한 정부 규제로 인해 산업계는 온실가스 배출을 줄여야 하고, 효율적인 탄소 포집 재료에 대한 수요가 증가하고 있습니다. 넷제로 목표를 달성하고자 하는 기업들은 지속 가능한 재료와 탄소 감축을 점점 더 우선순위로 삼고 있으며, 이는 시장 도입을 촉진하고 있습니다.

또한, 바이오 유래 순환형 탄소 포집 소재 원료의 기술 혁신이 진행됨에 따라 효율성이 향상되고, 비용이 절감되며, 환경적 이점이 강화되고, 이용 사례가 확대되고 있습니다. 이러한 요인들은 기후 변화에 대한 영향을 완화하고 환경 규제를 준수하려는 업계 전반의 투자를 불러일으키며 급격한 성장을 뒷받침하고 있습니다.

아민 및 알칼리성 용액을 포함한 액체 용매는 산업 배출물에서 CO2를 회수하는 데 있어 입증된 효율성과 범용성으로 인해 탄소 포집 시장에서 가장 빠르게 성장하는 재료입니다. 아민계 용매는 CO2 분자와의 친화력이 높고 효과적인 CO2 포집가 가능하기 때문에 수십년동안 널리 사용되어 왔습니다. 비록 저농도일지라도 일반적으로 배기가스에 포함된 CO2를 흡수할 수 있습니다. 이러한 실적이 있기 때문에 특히 탄소 배출이 큰 관심사인 발전 및 산업 부문에서 연소 후 탄소 포집 프로세스에 대한 신뢰도가 높습니다.

용매 배합의 발전으로 재생 에너지 요구 사항이 크게 개선되고 운영 비용이 절감되어 이러한 솔루션이 경제적으로 실행 가능한 솔루션이 되었습니다. 또한, 용매의 열화, 부식 등의 단점을 해결하고, 이들 소재의 내구성과 수명주기를 향상시키는 기술 혁신이 진행되고 있습니다. 한편, 알칼리성 용매는 CO2와의 반응 속도가 빠르고, 다양한 공정 조건에서 사용하기에 적합하다는 등의 장점을 제공하여 산업적 응용 범위를 넓히고 있습니다. 액체 용매 시스템은 대규모 변경 없이 기존 산업 설비에 통합할 수 있는 유연성을 가지고 있어 큰 성장 동력이 되고 있습니다. 이러한 용매는 배기 가스 조성 및 온도 변화에 대응하고 특정 공정의 요구에 맞게 조정할 수 있습니다. 탄소 배출량 감축을 위한 전 세계적인 강력한 규제 강화도 산업계가 이러한 성숙한 용매 기술을 채택하도록 동기를 부여하고 있습니다.

흡착은 에너지 효율성, 다용도성, 확장 가능한 탈탄소 솔루션과의 일관성 등으로 인해 탄소 포집 시장에서 가장 빠르게 성장하는 공정 분야입니다. 제올라이트나 유기 금속 골격과 같은 고체 물질을 이용하는 흡착은 가스 흐름에서 CO2를 최대 90%의 회수 효율로 회수하며, 필요한 에너지는 흡수 공정보다 30% 정도 적은 경우가 많습니다. 급속한 성장의 원동력은 발전소부터 주변 공기까지 다양한 배출원에 대응할 수 있는 후연소 및 직접 공기 회수 모두에 적용할 수 있다는 점입니다. 애드솔루션의 모듈식 소형 시스템은 시멘트 및 철강 설비와 같은 기존 산업 설비에 쉽게 통합할 수 있어 개조 비용을 절감할 수 있습니다. 고용량, 고선택성 흡착제의 기술 혁신으로 성능이 향상되어 소규모에서 대규모 응용까지 비용 효율적인 공정을 실현할 수 있습니다. 탄소 가격제와 같은 지원 정책과 함께 마이너스 배출 기술에 대한 수요가 증가함에 따라, 특히 넷제로 목표가 엄격한 지역에서 채택이 가속화되고 있습니다. 액체 용매에 비해 화학 폐기물을 줄일 수 있는 등 흡착제의 환경적 장점은 흡착제의 매력을 더욱 높여주고 있습니다. 저농도 CO2를 처리할 수 있는 능력과 자재관리의 지속적인 개선으로 흡착은 가장 빠르게 성장하는 공정으로, 효율적이고 확장 가능한 탄소 포집 솔루션에 대한 긴급한 수요에 대응하고 있습니다.

연소 전 탄소 포집는 탄소 포집 시장에서 가장 빠르게 성장하는 기술이며, 그 이유는 매우 효율적이고 대규모 탈탄소화에 유망한 몇 가지 중요한 이점이 있기 때문입니다. 연소 후 회수와는 달리, 연소 전 기술은 가스화 또는 개질 공정을 통해 화석연료를 수소와 이산화탄소의 혼합가스(합성가스로 알려져 있음)로 변환하여 연소 전에 이산화탄소를 제거합니다. 그 결과, CO2의 농도와 압력이 높은 가스 흐름을 얻을 수 있으며, 물리적 또는 화학적 흡수법에 의한 회수의 용이성과 효율성이 크게 향상됩니다. 이처럼 CO2 농도가 높기 때문에 연소 전 회수 시 필요한 장비가 더 작고, 분리를 위한 에너지가 적어 다른 방식에 비해 자본비용과 운영비용을 모두 절감할 수 있습니다. 이 공정은 청정 연소 연료인 수소를 귀중한 제품별로 생산하여 저탄소 수소 경제로의 광범위한 에너지 전환을 지원합니다. 또한, 연소 전 수익은 청정 에너지 생산을 위해 설계된 새로운 플랜트 및 산업 시설에 통합될 수 있어 전 세계 탈탄소화 추세에 부합하는 미래지향적인 접근 방식입니다. 가스화 공정의 초기 투자비용은 기존 시스템보다 높지만, 회수 효율 향상, 에너지 비용 절감, 연료 품질 향상 등 장기적인 이점이 가스화 공정의 성장을 견인하고 있습니다. 또한, 산업계가 발전 및 중공업과 같이 배출량 감축이 어려운 부문에서 배출량 감축을 요구하고 있는 가운데, 예비 연소 기술은 상대적으로 저렴한 비용으로 대량의 CO2를 회수할 수 있는 효과적인 솔루션을 제공합니다.

석유 및 가스 산업은 전 세계 CO2 배출에 크게 기여하고 있으며, 이산화탄소 배출량 감축에 대한 압력이 증가함에 따라 탄소 포집 시장에서 가장 빠르게 성장하고 있는 최종 이용 산업 분야입니다. 이 산업은 업스트림, 중류, 하류 부문에서 탄소 집약적인 공정을 많이 운영하고 있으며, 탄소 포집 및 저장(CCS)은 배출량을 효과적으로 줄이기 위해 필수적인 기술입니다. 성장의 주요 원동력 중 하나는 CCS가 환경 문제를 해결하면서 화석연료 사용을 지속할 수 있는 능력으로, 생산 중단 없이 산업계가 저탄소 운영으로 전환할 수 있도록 지원하는 것입니다. CCS와 석유증진회수(EOR) 기술의 통합이 시장을 견인하는 주요 요인으로 꼽힙니다. 회수한 CO2를 성숙한 유전에 주입하여 석유 추출을 촉진함으로써 배출량 감소와 자원 회수량 증가라는 두 가지 이점을 얻을 수 있습니다. 이러한 시너지 효과로 인해 CCS를 채택할 수 있는 경제적 인센티브가 생겨나며, 다른 분야보다 경제적으로 더 현실적인 대안이 될 수 있습니다. 또한, 규제 요건과 세계 순배출량 제로에 대한 약속으로 인해 석유 및 가스 회사들은 기후 변화 목표와 이해관계자들의 지속가능성에 대한 기대에 부응하기 위해 탄소 포집 기술에 많은 투자를 해야 합니다. 회수 효율을 높이고 비용을 절감하며 안전한 CO2 저장을 보장하는 기술의 발전은 이 분야에서의 채택을 더욱 가속화하고 있습니다. CO2 수송 및 저장 네트워크를 포함한 대규모 인프라 프로젝트는 석유 및 가스 분야의 CCS 이니셔티브 확대를 뒷받침하고 있습니다. 업계는 지속가능성에 초점을 맞추고 있으며, 정부의 인센티브와 탄소 시장의 변화와 함께 석유 및 가스는 탄소 포집 전망에서 고성장 분야로 자리매김하고 있습니다.

세계의 탄소 포집 재료 시장에 대해 조사했으며, 공정별, 재료별, 기술별, 최종사용자별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

- 생성형 AI/AI가 탄소 포집 재료 시장에 미치는 영향

제6장 업계 동향

- 서론

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 공급망 분석

- 2025년 미국 관세가 탄소 포집 재료 시장에 미치는 영향

- 가격 분석

- 투자 및 자금조달 시나리오

- 생태계 분석

- 기술 분석

- 특허 분석

- 무역 분석

- 2025-2027년 주요 컨퍼런스 및 이벤트

- 관세 및 규제 상황

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 전망

- 사례 연구 분석

제7장 탄소 포집 재료 시장(프로세스별)

- 서론

- 흡착

- 흡수

제8장 탄소 포집 재료 시장(재료별)

- 서론

- 액체 용제

- 강력 용제

- 멤브레인

제9장 탄소 포집 재료 시장(기술별)

- 서론

- 연소 전 회수

- 연소 후 회수

- 산소 연소 회수

- 직접 공기 회수

제10장 탄소 포집 재료 시장(최종사용자별)

- 서론

- 발전

- 석유 및 가스

- 화학제품 및 석유화학제품

- 금속 및 광업

- 산업

- 기타

제11장 탄소 포집 재료 시장(지역별)

- 서론

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 이탈리아

- 프랑스

- 영국

- 스페인

- 러시아

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제12장 경쟁 구도

- 서론

- 주요 시장 진출기업의 전략/강점

- 시장 점유율 분석

- 매출 분석

- 브랜드/제품 비교

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표

- 경쟁 시나리오

제13장 기업 개요

- 주요 시장 진출기업

- BASF

- DOW

- HONEYWELL INTERNATIONAL INC.

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- TOSOH CORPORATION

- AIR PRODUCTS AND CHEMICALS, INC.

- ZEOCHEM AG

- ECOLAB

- SVANTE TECHNOLOGIES INC.

- CALGON CARBON CORPORATION

- 기타 기업

- BOYCE CARBON

- JALON

- SPIRITUS

- CARBON ACTIVATED CORPORATION

- WARTSILA

- CLARIANT AG

제14장 부록

LSH 25.10.16The carbon capture materials market is projected to grow from USD 66,904.7 million in 2025 to USD 99,098.5 million by 2030, registering a CAGR of 8.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Kiloton) |

| Segments | Process, Material, End-Use Industries, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, South America |

key factors accelerating the carbon capture materials market include stringent climate policies, rising corporate sustainability commitments, and technological advancements. Stringent government regulations compel industries to reduce greenhouse gas emissions, driving demand for efficient carbon capture materials. Corporations aiming to meet net-zero targets increasingly prioritize sustainable materials and carbon reduction, boosting market adoption.

Additionally, ongoing innovation in bio-derived and circular carbon capture materials improves efficiency, reduces costs, and enhances environmental benefits, expanding use cases. These factors create favorable market conditions, attracting investments and supporting rapid growth across industries seeking to mitigate climate impact and comply with environmental mandates.

"Liquid solvents are the fastest-growing material segment of the carbon capture materials market in terms of value."

Liquid solvents, including amine-based and alkaline-based solutions, are the fastest-growing materials in the carbon capture market due to their proven efficiency and versatility in capturing CO2 from industrial emissions. Amine-based solvents have been widely used for decades because of their high affinity for CO2 molecules, enabling effective. Absorptions, even at low concentrations, are typically found in flue gases. This established track record makes them highly reliable for post-combustion carbon capture processes, particularly in power generation and industrial sectors where carbon emissions are a major concern.

Advancements in solvent formulations have significantly improved their regeneration energy requirements, reducing operational costs and making these solutions more economically viable. Innovations are addressing drawbacks such as solvent degradation and corrosion, enhancing the durability and lifecycle of these materials. Alkaline-based solvents, on the other hand, offer benefits including faster reaction rates with CO2 and suitability for use in different process conditions, which broadens their industrial applicability. The flexibility of liquid solvent systems to be integrated into existing industrial setups without extensive modifications is a major growth driver. These solvents can be tailored for specific process needs, adapting to varying flue gas compositions and temperatures. The strong regulatory push for carbon emission reductions globally also incentivizes industries to adopt these mature solvent technologies.

"Absorptions are the fastest-growing process segment of the carbon capture materials market in terms of value."

Adsorptions are the fastest-growing process segment in the carbon capture market due to their energy efficiency, versatility, and alignment with scalable decarbonization solutions. Utilizing solid materials like zeolites or metal-organic frameworks, adsorptions capture CO2 from gas streams with capture efficiencies up to 90%, requiring significantly less energy, often 30% lower than absorption processes. Its rapid growth is driven by its applicability in both post-combustion and direct air capture, addressing diverse emission sources from power plants to ambient air. Adsorptions' modular and compact systems enable easy integration into existing industrial setups, such as cement or steel facilities, reducing retrofitting costs. Innovations in high-capacity, selective sorbents enhance performance, making the process cost-effective for small- and large-scale applications. The growing demand for negative emissions technologies, coupled with supportive policies like carbon pricing, accelerates adoption, particularly in regions with stringent net-zero goals. Adsorptions' environmental benefits, including reduced chemical waste compared to liquid solvents, further boost their appeal. Its ability to handle low CO2 concentrations and continuous improvements in material durability make Adsorptions the fastest-growing process, addressing the urgent need for efficient, scalable carbon capture solutions.

"Pre-combustion is the fastest-growing technique segment of the carbon capture materials market in terms of value."

Pre-combustion carbon capture is the fastest-growing technique in the carbon capture market due to several key advantages that make it highly efficient and promising for large-scale decarbonization. Unlike post-combustion capture, pre-combustion technology removes CO2 before combustion by converting fossil fuels into a mixture of hydrogen and carbon dioxide (known as syngas) through a gasification or reforming process. This results in a gas stream with a higher concentration and pressure of CO2, which significantly enhances the ease and efficiency of capture using physical or chemical absorption methods. This higher concentration of CO2 means pre-combustion capture requires smaller equipment and less energy for separation, reducing both the capital and operational costs compared to other techniques. The process produces hydrogen, a clean-burning fuel, as a valuable byproduct, supporting the broader energy transition toward low-carbon hydrogen economies. Furthermore, pre-combustion capture can be integrated into new plants and industrial facilities designed for clean energy production, making it a forward-looking approach aligned with global decarbonization trends. Though the initial investment for the gasification process is higher than that of conventional systems, the long-term benefits of greater capture efficiency, lower energy penalties, and enhanced fuel quality are driving its growth. Additionally, as industries seek to reduce emissions from hard-to-abate sectors like power generation and heavy industry, pre-combustion technology offers an effective solution capable of capturing large volumes of CO2 at relatively lower cost.

"Oil & gas is the fastest-growing end-use industry segment of the carbon capture materials market in terms of value."

The oil & gas industry is the fastest-growing end-use sector in the carbon capture market because of its significant contribution to global CO2 emissions and the increasing pressure to lower its carbon footprint. This industry operates many carbon-intensive processes across upstream, midstream, and downstream segments, making carbon capture and storage (CCS) an essential technology for effectively reducing emissions. One of the main drivers of growth is CCS's ability to allow continued fossil fuel use while addressing environmental concerns, supporting the industry's transition to lower-carbon operations without stopping production. A major factor boosting the market is the integration of CCS with enhanced oil recovery (EOR) techniques. Captured CO2 is injected into mature oil fields to boost oil extraction, providing the dual benefit of reducing emissions and increasing resource recovery. This synergy creates economic incentives for adopting CCS, making it more financially practical than in other sectors. Additionally, regulatory requirements and global net-zero commitments compel oil and gas companies to heavily invest in carbon capture technologies to meet climate goals and stakeholder sustainability expectations. Technological advances that improve capture efficiency, cut costs, and ensure safe CO2 storage are further speeding up adoption in this sector. Large-scale infrastructure projects, including CO2 transportation and storage networks, support the expansion of CCS initiatives in oil and gas. The industry's focus on sustainability, along with government incentives and changing carbon markets, places oil and gas as a high-growth area within the carbon capture landscape.

In-depth interviews were conducted with Chief Executive Officers (CEOs), marketing directors, other innovation and technology directors, and executives from various key organizations operating in the carbon capture materials market, and information was gathered from secondary research to determine and verify the market size of several segments.

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: Managers- 15%, Directors - 20%, and Others - 65%

- By Region: North America - 15%, Europe - 10%, Asia Pacific - 65%, Middle East & Africa - 7%, South America - 3%.

The key players in the carbon capture materials market include Ecolab (US), BASF (Germany), DOW (US), MITSUBISHI HEAVY INDUSTRIES, LTD (Japan), Solvay (Belgium), Air Products and Chemicals, Inc. (US), Tosoh Corporation (Japan), Honeywell International Inc. (US), and Zeochem (Switzerland). The study includes an in-depth competitive analysis of these key players in the carbon capture materials market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This report segments the market for carbon capture materials by process, technique, material, end-use industry, and region, and estimates the overall market value across various regions. It also provides a detailed analysis of key industry players to provide insights into their business overviews, products and services, key strategies, and expansions associated with the carbon capture materials market.

Key Benefits of Buying This Report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the carbon capture materials market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of drivers (Stringent Climate Policies, Carbon Pricing Mechanisms, and Net-Zero Targets Driving Adoption), restraints (High Energy Penalty and Cost Burden in Large-Scale Material Regeneration), opportunities (Innovation of Bio-Derived and Circular Carbon Capture Materials), and challenges (Supply-Chain Reliability & Plant-Retrofit Compatibility Constraints).

- Market Penetration: Comprehensive information on the carbon capture materials market offered by top players in the carbon capture materials market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, partnerships, agreements, and collaborations in the market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the carbon capture materials market across regions.

- Market Capacity: Production capacities of companies producing carbon capture materials market are provided wherever available, with upcoming capacities for the carbon capture materials market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the carbon capture materials market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary sources

- 2.1.2.3 Key participants for primary interviews

- 2.1.2.4 Breakdown of primary interviews

- 2.1.2.5 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 SUPPLY-SIDE ANALYSIS

- 2.2.2 DEMAND-SIDE ANALYSIS

- 2.3 MARKET FORECAST

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 GROWTH FORECAST

- 2.8 RISK ASSESSMENT

- 2.9 FACTOR ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CARBON CAPTURE MATERIALS MARKET

- 4.2 CARBON CAPTURE MATERIALS MARKET, BY MATERIAL

- 4.3 CARBON CAPTURE MATERIALS MARKET, BY PROCESS

- 4.4 CARBON CAPTURE MATERIALS MARKET, BY TECHNIQUE

- 4.5 CARBON CAPTURE MATERIALS MARKET, BY END USER

- 4.6 CARBON CAPTURE MATERIALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising decarbonization pressure in energy-intensive industries

- 5.2.1.2 Stringent climate policies, carbon pricing mechanisms, and net-zero targets

- 5.2.2 RESTRAINTS

- 5.2.2.1 High energy requirement and cost burden in large-scale material regeneration

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of bio-derived and circular carbon capture materials

- 5.2.3.2 Integration of capture systems with utilization and mineralization technologies

- 5.2.4 CHALLENGES

- 5.2.4.1 Supply chain reliability and plant-retrofit compatibility constraints

- 5.2.1 DRIVERS

- 5.3 IMPACT OF GENERATIVE AI/AI ON CARBON CAPTURE MATERIALS MARKET

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.3 SUPPLY CHAIN ANALYSIS

- 6.4 IMPACT OF 2025 US TARIFFS ON CARBON CAPTURE MATERIALS MARKET

- 6.4.1 INTRODUCTION

- 6.4.2 KEY TARIFF RATES

- 6.4.3 PRICE IMPACT ANALYSIS

- 6.4.4 IMPACT ON COUNTRY/REGION

- 6.4.4.1 US

- 6.4.4.2 Europe

- 6.4.4.3 Asia Pacific

- 6.4.5 IMPACT ON END-USE INDUSTRIES

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE TREND, BY REGION, 2021-2024

- 6.5.2 AVERAGE SELLING PRICE TREND, BY MATERIAL, 2021-2024

- 6.5.3 AVERAGE SELLING PRICE TREND OF KEY PLAYER, BY MATERIAL, 2024

- 6.6 INVESTMENT AND FUNDING SCENARIO

- 6.7 ECOSYSTEM ANALYSIS

- 6.8 TECHNOLOGY ANALYSIS

- 6.8.1 KEY TECHNOLOGIES

- 6.8.2 COMPLEMENTARY TECHNOLOGIES

- 6.9 PATENT ANALYSIS

- 6.9.1 METHODOLOGY

- 6.9.2 PATENTS GRANTED

- 6.9.3 PATENT PUBLICATION TRENDS

- 6.9.4 INSIGHTS

- 6.9.5 LEGAL STATUS OF PATENTS

- 6.9.6 JURISDICTION ANALYSIS

- 6.9.7 TOP APPLICANTS

- 6.9.8 LIST OF MAJOR PATENTS

- 6.10 TRADE ANALYSIS

- 6.10.1 EXPORT SCENARIO (HS CODE 380210)

- 6.10.2 IMPORT SCENARIO (HS CODE 380210)

- 6.11 KEY CONFERENCES AND EVENTS, 2025-2027

- 6.12 TARIFF AND REGULATORY LANDSCAPE

- 6.12.1 TARIFF ANALYSIS

- 6.12.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12.3 REGULATIONS AND STANDARDS RELATED TO CARBON CAPTURE MATERIALS

- 6.13 PORTER'S FIVE FORCES ANALYSIS

- 6.13.1 THREAT OF NEW ENTRANTS

- 6.13.2 THREAT OF SUBSTITUTES

- 6.13.3 BARGAINING POWER OF SUPPLIERS

- 6.13.4 BARGAINING POWER OF BUYERS

- 6.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.14.2 BUYING CRITERIA

- 6.15 MACROECONOMIC OUTLOOK

- 6.15.1 GDP TRENDS AND FORECASTS, BY COUNTRY

- 6.16 CASE STUDY ANALYSIS

- 6.16.1 TECHNOLOGY ANALYSIS OF CARBON CAPTURE MATERIALS: KEY AND COMPLEMENTARY TECHNOLOGIES SHAPING MARKET EVOLUTION

- 6.16.2 ADVANCED NANOSTRUCTURED MATERIALS FOR INDUSTRIAL CARBON CAPTURE

7 CARBON CAPTURE MATERIALS MARKET, BY PROCESS

- 7.1 INTRODUCTION

- 7.2 ADSORPTION

- 7.2.1 INCREASING DEMAND FOR ENERGY-EFFICIENT AND REGENERABLE MATERIALS IN INDUSTRIAL CARBON CAPTURE SYSTEMS TO DRIVE DEMAND

- 7.3 ABSORPTION

- 7.3.1 GROWING DEPLOYMENT OF SOLVENT-BASED CO2 CAPTURE SYSTEMS IN LARGE-SCALE POWER PLANTS AND INDUSTRIAL FACILITIES TO FUEL DEMAND

8 CARBON CAPTURE MATERIALS MARKET, BY MATERIAL

- 8.1 INTRODUCTION

- 8.2 LIQUID SOLVENTS

- 8.2.1 ADVANCEMENTS IN SOLVENT FORMULATIONS TO DRIVE DEMAND

- 8.2.2 AMINE-BASED SOLUTIONS

- 8.2.3 ALKALINE SOLUTIONS

- 8.3 STRONG SOLVENTS

- 8.3.1 GROWING EMPHASIS ON ENVIRONMENTALLY SUSTAINABLE AND REUSABLE MATERIALS TO FUEL DEMAND

- 8.3.2 ZEOLITES

- 8.3.3 ACTIVATED CARBON

- 8.3.4 CALCIUM-BASED SORBENTS

- 8.3.5 METAL-ORGANIC FRAMEWORKS

- 8.4 MEMBRANES

- 8.4.1 ABILITY TO SELECTIVELY SEPARATE CO2 FROM FLUE GASES OR INDUSTRIAL STREAMS TO PROPEL DEMAND

- 8.4.2 POLYMERIC MEMBRANES

9 CARBON CAPTURE MATERIALS MARKET, BY TECHNIQUE

- 9.1 INTRODUCTION

- 9.2 PRE-COMBUSTION CAPTURE

- 9.2.1 RISING DEMAND FOR HYDROGEN AS CLEAN FUEL TO DRIVE MARKET

- 9.3 POST-COMBUSTION CAPTURE

- 9.3.1 RETROFITTING POTENTIAL IN EXISTING POWER PLANTS AND INDUSTRIES TO DRIVE DEMAND

- 9.4 OXYFUEL COMBUSTION CAPTURE

- 9.4.1 HIGHER CO2 PURITY AND SIMPLIFIED CAPTURE PROCESSES TO PROPEL MARKET

- 9.5 DIRECT AIR CAPTURE

- 9.5.1 INCREASING GLOBAL EMPHASIS ON ACHIEVING NET-ZERO CARBON TARGETS TO DRIVE DEMAND

10 CARBON CAPTURE MATERIALS MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 POWER

- 10.2.1 RISING EMISSION REDUCTION MANDATES AND CARBON-NEUTRALITY TARGETS TO ACCELERATE DEMAND

- 10.3 OIL & GAS

- 10.3.1 COMPLIANCE WITH EMISSION REDUCTION MANDATES TO DRIVE DEMAND

- 10.4 CHEMICAL & PETROCHEMICAL

- 10.4.1 RISING NEED TO DECARBONIZE ENERGY-INTENSIVE CHEMICAL PRODUCTION TO PROPEL DEMAND

- 10.5 METALS & MINING

- 10.5.1 INCREASING PRESSURE TO DECARBONIZE ENERGY-INTENSIVE SMELTING, REFINING, AND MINERAL PROCESSING OPERATIONS TO FUEL DEMAND

- 10.6 INDUSTRIAL

- 10.6.1 DECARBONIZATION REQUIREMENTS ACROSS DIVERSE INDUSTRIAL OPERATIONS TO BOOST DEMAND

- 10.7 OTHER END USERS

- 10.7.1 WASTE WATER TREATMENT

- 10.7.2 AGRICULTURE

11 CARBON CAPTURE MATERIALS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Extensive industrial activity and government-backed decarbonization goals to drive market

- 11.2.2 JAPAN

- 11.2.2.1 Focus on development of hydrogen economy to drive market

- 11.2.3 INDIA

- 11.2.3.1 High coal dependency and industrial emissions to fuel demand

- 11.2.4 SOUTH KOREA

- 11.2.4.1 Government-backed CCUS pilot projects in heavy industries to propel demand

- 11.2.5 REST OF ASIA PACIFIC

- 11.2.1 CHINA

- 11.3 NORTH AMERICA

- 11.3.1 US

- 11.3.1.1 Federal incentives under Inflation Reduction Act (IRA) and 45Q tax credits to drive adoption

- 11.3.2 CANADA

- 11.3.2.1 Stringent carbon pricing policies and large-scale CCUS infrastructure to fuel demand

- 11.3.3 MEXICO

- 11.3.3.1 Alignment with North American CCUS strategies and potential for industrial decarbonization to accelerate demand

- 11.3.1 US

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Ambitious climate neutrality targets and industrial decarbonization mandates to drive demand

- 11.4.2 ITALY

- 11.4.2.1 National decarbonization strategies and EU-funded CCS pilot projects to fuel demand

- 11.4.3 FRANCE

- 11.4.3.1 Expansion of industrial CCS initiatives and regulatory frameworks to drive demand

- 11.4.4 UK

- 11.4.4.1 High emphasis on negative emissions technologies and direct air capture pilot programs to fuel demand

- 11.4.5 SPAIN

- 11.4.5.1 High R&D support and innovation-driven policies to drive market

- 11.4.6 RUSSIA

- 11.4.6.1 Emerging CCU economic viability and CO2-EOR opportunities to drive demand

- 11.4.7 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Strategic focus on large-scale CCUS infrastructure to drive demand

- 11.5.1.2 UAE

- 11.5.1.2.1 Strategic focus on blue hydrogen production and large-scale industrial CCUS projects to fuel demand

- 11.5.1.3 Rest of GCC Countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Government incentives to reduce coal-related emissions to drive adoption

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Robust legislative framework and abundant geological storage resources to fuel market growth

- 11.6.2 ARGENTINA

- 11.6.2.1 Growing industrial initiatives and supportive regulatory measures to propel market

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 MARKET SHARE ANALYSIS

- 12.4 REVENUE ANALYSIS

- 12.5 BRAND/PRODUCT COMPARISON

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.6.5.1 Company footprint

- 12.6.5.2 Material footprint

- 12.6.5.3 Process footprint

- 12.6.5.4 End-user footprint

- 12.6.5.5 Region footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.7.5.1 Detailed list of key startups/SMEs

- 12.7.5.2 Competitive benchmarking of key startups/SMEs

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 DEALS

- 12.9.2 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 BASF

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths/Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses/Competitive threats

- 13.1.2 DOW

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths/Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses/Competitive threats

- 13.1.3 HONEYWELL INTERNATIONAL INC.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths/Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses/Competitive threats

- 13.1.4 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths/Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses/Competitive threats

- 13.1.5 TOSOH CORPORATION

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Key strengths/Right to win

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses/Competitive threats

- 13.1.6 AIR PRODUCTS AND CHEMICALS, INC.

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Expansions

- 13.1.7 ZEOCHEM AG

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.8 ECOLAB

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.9 SVANTE TECHNOLOGIES INC.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.10 CALGON CARBON CORPORATION

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.1 BASF

- 13.2 OTHER PLAYERS

- 13.2.1 BOYCE CARBON

- 13.2.2 JALON

- 13.2.3 SPIRITUS

- 13.2.4 CARBON ACTIVATED CORPORATION

- 13.2.5 WARTSILA

- 13.2.6 CLARIANT AG

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS