|

시장보고서

상품코드

1856925

폴리에틸렌 퓨라노에이트(PEF) 시장 : 유래별, 등급별, 용도별, 최종 이용 산업별, 지역별 - 예측(-2030년)Polyethylene Furanoate (PEF) Market by Source (Plant Based, Bio Based), Grade, Application (Bottles, Films, Fibers), End-Use Industry (Packaging, Fiber & Textiles, Electronics & Electrical, Pharmaceuticals), And Region - Global Forecast to 2030 |

||||||

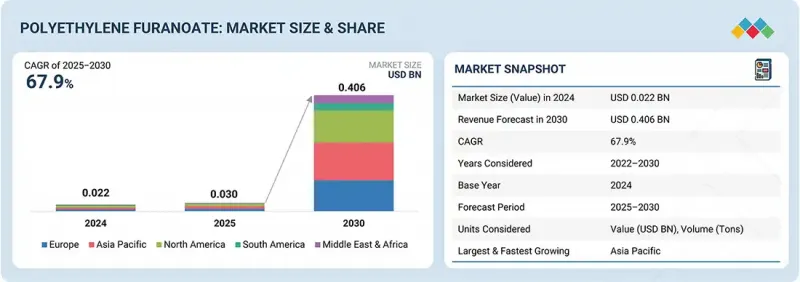

폴리에틸렌 퓨라노에이트(PEF) 시장 규모는 2025년 3,050만 달러에서 2030년에는 4억 660만 달러에 이르고, CAGR은 67.9%를 보일 것으로 예측됩니다.

PEF는 재생 가능한 식물 유래 원료로 생산되기 때문에 PET와 같은 기존 석유계 플라스틱보다 우수한 차단 특성과 재활용성을 가지고 있습니다. 환경에 미치는 악영향을 최소화하면서 유통기한을 연장할 수 있는 PEF의 능력은 소비자의 높아진 환경 인식과 전 세계적인 규제 강화 정책에 부합합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2022-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 검토 단위 | 수량(톤), 금액(100만 달러) |

| 부문 | 유래별, 등급별, 용도별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미 |

기업들이 생분해성 및 저탄소 발자국을 남기지 않는 대안을 도입하기 시작하면서 식음료, 화장품, 의약품 등의 포장재 분야에서 PEF의 급격한 성장세를 뒷받침하고 있습니다. PEF 생산에 대한 투자와 기술 혁신 증가는 소비자와 기업 모두 환경 친화적인 포장 대체품에 대한 요구가 증가하고 있음을 반영합니다.

지속 가능하고 친환경적인 포장 솔루션에 대한 수요가 증가함에 따라 폴리에틸렌 푸라노에이트 시장의 성장이 촉진되고 있습니다. 최종 용도별로는 예측 기간 동안 포장 부문이 금액 기준으로 PEF 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. PEF는 매우 우수한 배리어 소재이며, 재활용이 가능하고 바이오이며, 식음료를 포함한 포장 용도에 적합합니다. 또한, 플라스틱 폐기물과 이산화탄소 배출량을 줄이기 위한 전 세계적인 변화도 이를 촉진하고 있습니다.

섬유 분야는 예측 기간 동안 폴리에틸렌 푸라노에이트 시장에서 금액 기준으로 두 번째로 큰 점유율을 차지할 것으로 예측됩니다. PEF 섬유는 폴리에스테르 섬유에 비해 강도, 열 안정성, 재활용성이 우수합니다. 의류, 산업용 섬유, 포장용 필름에 PEF 섬유를 사용하면 시장 수요가 증가하고 있습니다. 지속 가능한 바이오 소재를 추구하는 섬유 산업의 추세는 PEF 섬유 세계 시장을 확대하고 있습니다.

유럽이 폴리에틸렌 푸라노에이트 시장에서 가장 높은 점유율을 차지하고 있는 것은 EU 그린딜, 포장 및 포장 폐기물 규제 등 지속 가능한 바이오 소재를 장려하는 엄격한 환경 정책의 배경에 기인합니다. 친환경 포장에 대한 소비자 수요 증가와 순환 경제 발전에 대한 기업의 노력도 지속 가능한 바이오 소재의 사용을 촉진하고 있습니다. 독일, 프랑스, 영국을 포함한 이 지역의 주요 시장은 잘 정비된 산업 인프라와 연구개발(R&D)에 대한 막대한 투자의 혜택을 누리고 있습니다. 또한, 민관 파트너십과 자금 지원의 존재는 식품, 음료 및 특수 포장의 새로운 혁신과 새로운 시장 창출을 촉진하는 데 도움이 되고 있습니다.

세계의 폴리에틸렌 푸라노에이트(PEF) 시장에 대해 조사했으며, 유래별, 등급별, 용도별, 최종 이용 산업별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요

- 서론

- 시장 역학

제6장 업계 동향

- 밸류체인 분석

- 생태계 분석

- Porter의 Five Forces 분석

- 주요 이해관계자와 구입 기준

- 무역 분석

- 고객의 비즈니스에 영향을 미치는 동향/혼란

- 기술 분석

- 거시경제 지표

- 가격 분석

- 규제 상황

- AI/생성형 AI의 영향

- 주요 컨퍼런스 및 이벤트

- 사례 연구 분석

- 투자 및 자금조달 시나리오

- 특허 분석

- 2025년 미국 관세의 영향 - 개요

제7장 폴리에틸렌 퓨라노에이트(PEF) 시장(유래별)

- 서론

- 식물 유래

- 바이오

제8장 폴리에틸렌 퓨라노에이트(PEF) 시장(등급별)

- 서론

- 표준 등급

- 고성능 등급

- 블렌드/커스터마이즈 등급

- 기타

제9장 폴리에틸렌 퓨라노에이트(PEF) 시장(용도별)

- 서론

- 보틀

- 섬유

- 필름

- 성형 부품

- 압출 부품

- 기타

제10장 폴리에틸렌 퓨라노에이트(PEF) 시장(최종 이용 산업별)

- 서론

- 포장

- 섬유 및 직물

- 전자 및 전기 부품

- 자동차 부품

- 의약품

- 기타

제11장 폴리에틸렌 퓨라노에이트(PEF) 시장(지역별)

- 서론

- 북미

- 미국

- 캐나다

- 멕시코

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제12장 경쟁 구도

- 개요

- 주요 시장 진출기업의 전략/강점

- 매출 분석

- 시장 점유율 분석

- 기업 평가와 재무 지표

- 브랜드/제품 비교 분석

- 기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제13장 기업 개요

- 주요 시장 진출기업

- AVANTIUM

- SULZER LTD

- AVA BIOCHEM AG

- ORIGIN MATERIALS

- TOYOBO CO., LTD

- ZHEJIANG SUGAR ENERGY TECHNOLOGY CO., LTD

- SWICOFIL AG(DISTRIBUTOR)

- ALPLA

- DANONE

- EASTMAN CHEMICAL COMPANY

- 기타 기업

- THE COCA-COLA COMPANY

- TERPHANE

- LVMH

- KVADRAT

- CARLSBERG GROUP

제14장 부록

LSH 25.11.10The polyethylene furanoate market is projected to reach USD 406.6 million by 2030 from USD 30.5 million in 2025, at a CAGR of 67.9%. PEF is produced from renewable plant-based feedstocks and therefore has better barrier properties and recyclability than traditional petroleum-based plastics like PET. PEF's ability to prolong shelf life while minimizing adverse environmental impacts fits into consumers' increased environmental awareness as well as the stricter regulatory policies worldwide.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Volume (Tons); Value (USD Million) |

| Segments | Source, Grade, Application, and End-use Industry |

| Regions covered | Asia Pacific, North America, Europe, the Middle East & Africa, and South America |

The transition by companies to incorporate biodegradable, low-carbon-footprint alternatives helps sustain the rapid growth of PEF in packaging applications such as food and beverage, cosmetics, and pharmaceuticals. The increase in investment and innovation in PEF production reflects the growing desire for greener packaging alternatives for both consumers and companies.

"Based on end-use industry, packaging accounts for the largest share in the polyethylene furanoate market, in terms of value, during the forecast period."

The rising demand for sustainable and eco-friendly packaging solutions is driving the growth of the polyethylene furanoate market. By end-use segment, packaging is estimated to account for the largest share in the PEF market, in terms of value, during the forecast period. PEF is a very good barrier material, recyclable and bio-based, and is perfect for packaging applications, including food and beverages. This is also driven by the global shift to reduce plastic waste and carbon emissions.

"Based on application, fibers is the second-largest segment in the polyethylene furanoate market, in terms of value, during the forecast period."

The fibers segment is projected to account for the second-largest share in the polyethylene furanoate market, in terms of value, during the forecast period. PEF fibers offer impressive strength, thermal stability, and recyclability compared to polyester fibers. The use of PEF fibers in apparel, industrial textiles, and packaging films is increasing their demand within the market. The trend within the textile industry towards sustainable and bio-based materials increases the global market for PEF fibers.

"Based on region, Europe accounted for the largest share of the polyethylene furanoate market, in terms of value, in 2024."

Europe has the highest market share in the polyethylene furanoate market because of stringent environmental policies such as the EU Green Deal and the Packaging and Packaging Waste Regulation that promote sustainable, bio-based materials. The rise of consumer demand for eco-friendly packaging and corporate commitments to developing a circular economy have also boosted the use of sustainable, bio-based materials. Key markets in the region, including Germany, France, and the UK, benefit from a well-developed industrial infrastructure and substantial investments in research and development (R&D). Additionally, the presence of public-private partnerships and funding helps to stimulate new innovations and the creation of new markets for food, beverages, and specialty packaging.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: Directors- 35%, Managers - 25%, and Others - 40%

- By Region: North America - 22%, Europe - 22%, Asia Pacific - 45%, RoW - 11%

The key players in this market are Avantium (Netherlands), Sulzer Ltd (Switzerland), AVA Biochem AG (Switzerland), Origin Materials (US), Toyobo Co., Ltd (Japan), Zhejiang Sugar Energy Technology Co., Ltd (China), Swicofil AG (Switzerland), ALPLA (Austria), Danone (France), and Eastman Chemical Company (US).

Research Coverage

This report segments the polyethylene furanoate market based on source, grade, application, end-use industry, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products and services, key strategies, product launches, expansions, and mergers & acquisitions associated with the polyethylene furanoate market.

Key benefits of buying this report

This research report focuses on various levels of analysis, including industry analysis (industry trends), market ranking analysis of top players, and company profiles. Together, these provide an overall view of the competitive landscape; emerging and high-growth segments; high-growth regions; and market drivers, restraints, opportunities, and challenges in the polyethylene furanoate market.

The report provides insights into the following pointers:

- Analysis of key drivers (Rising demand for sustainable and eco-friendly packaging solutions, government policies and incentives promoting renewable materials, technological advancements lowering production costs and improving commercial scalability), restraints (Dominance of conventional plastics, immature production infrastructure for PEF), opportunities (Diverse application potential, growth of bio-based plastics), and challenges (High production costs)

- Market Penetration: Comprehensive information on the polyethylene furanoate market offered by top players in the global polyethylene furanoate market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the polyethylene furanoate market

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for polyethylene furanoate across regions

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global polyethylene furanoate market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the polyethylene furanoate market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 List of primary interview participants - demand and supply sides

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.4 DATA TRIANGULATION

- 2.5 FACTOR ANALYSIS

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS & RISKS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN POLYETHYLENE FURANOATE MARKET

- 4.2 POLYETHYLENE FURANOATE MARKET, BY GRADE

- 4.3 POLYETHYLENE FURANOATE MARKET, BY END-USE INDUSTRY

- 4.4 POLYETHYLENE FURANOATE MARKET, BY APPLICATION

- 4.5 POLYETHYLENE FURANOATE MARKET, BY KEY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising demand for sustainable and eco-friendly packaging solutions

- 5.2.1.2 Government policies and incentives promoting renewable materials

- 5.2.1.3 Technological advancements lowering production costs and improving commercial scalability

- 5.2.2 RESTRAINTS

- 5.2.2.1 Dominance of conventional plastics

- 5.2.2.2 Immature production infrastructure for PEF

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Diverse application potential

- 5.2.3.2 Growth of bio-based plastics

- 5.2.4 CHALLENGES

- 5.2.4.1 High production costs

- 5.2.1 DRIVERS

6 INDUSTRY TRENDS

- 6.1 VALUE CHAIN ANALYSIS

- 6.1.1 RAW MATERIAL SUPPLIERS

- 6.1.2 MANUFACTURERS

- 6.1.3 DISTRIBUTORS

- 6.1.4 END USERS

- 6.2 ECOSYSTEM ANALYSIS

- 6.3 PORTER'S FIVE FORCES ANALYSIS

- 6.3.1 THREAT OF NEW ENTRANTS

- 6.3.2 THREAT OF SUBSTITUTES

- 6.3.3 BARGAINING POWER OF SUPPLIERS

- 6.3.4 BARGAINING POWER OF BUYERS

- 6.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.4.2 QUALITY

- 6.4.3 SERVICE

- 6.4.4 BUYING CRITERIA

- 6.5 TRADE ANALYSIS

- 6.5.1 EXPORT SCENARIO (HS CODE 170250)

- 6.5.2 IMPORT SCENARIO (HS CODE 170250)

- 6.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 KEY TECHNOLOGIES

- 6.7.1.1 YXY technology

- 6.7.1.2 Improved polymerization

- 6.7.2 COMPLEMENTARY TECHNOLOGIES

- 6.7.2.1 Robot-assisted film handling

- 6.7.1 KEY TECHNOLOGIES

- 6.8 MACROECONOMIC INDICATORS

- 6.8.1 GDP TRENDS AND FORECASTS

- 6.9 PRICING ANALYSIS

- 6.9.1 AVERAGE SELLING PRICE TREND, BY REGION

- 6.9.2 AVERAGE SELLING PRICE TREND OF PEF AMONG KEY PLAYERS, BY END USER

- 6.10 REGULATORY LANDSCAPE

- 6.10.1 NORTH AMERICA

- 6.10.2 ASIA PACIFIC

- 6.10.3 EUROPE

- 6.10.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11 IMPACT OF AI/GEN AI

- 6.12 KEY CONFERENCES AND EVENTS

- 6.13 CASE STUDY ANALYSIS

- 6.13.1 FOOD & BEVERAGE PACKAGING TRANSFORMATION

- 6.13.2 SUSTAINABLE TEXTILES USING PEF FIBERS

- 6.13.3 REGULATORY-DRIVEN INNOVATION IN EUROPE

- 6.14 INVESTMENT AND FUNDING SCENARIO

- 6.15 PATENT ANALYSIS

- 6.15.1 INTRODUCTION

- 6.15.2 LEGAL STATUS OF PATENTS

- 6.15.3 JURISDICTION ANALYSIS

- 6.16 IMPACT OF 2025 US TARIFF - OVERVIEW

- 6.16.1 INTRODUCTION

- 6.16.2 KEY TARIFF RATES

- 6.16.3 PRICE IMPACT ANALYSIS

- 6.16.4 IMPACT ON COUNTRY/REGION

- 6.16.4.1 US

- 6.16.4.2 Europe

- 6.16.4.3 Asia Pacific

- 6.16.5 IMPACT ON END-USE INDUSTRIES

7 POLYETHYLENE FURANOATE MARKET, BY SOURCE

- 7.1 INTRODUCTION

- 7.2 PLANT-BASED

- 7.2.1 REDUCE RELIANCE ON FOSSIL FUELS AND ENABLE SUSTAINABLE PRODUCTION OF PEF

- 7.3 BIO-BASED

- 7.3.1 LOWER GREENHOUSE GAS EMISSIONS WHILE DELIVERING HIGH-PERFORMANCE PROPERTIES IN PEF

8 POLYETHYLENE FURANOATE MARKET, BY GRADE

- 8.1 INTRODUCTION

- 8.2 STANDARD GRADE

- 8.2.1 SUPERIOR BARRIER PERFORMANCE AND RENEWABLE SOURCING TO DRIVE DEMAND

- 8.3 HIGH PERFORMANCE GRADE

- 8.3.1 EXCEPTIONAL STRENGTH AND DURABILITY TO DRIVE GROWTH IN DEMANDING PACKAGING AND INDUSTRIAL APPLICATIONS

- 8.4 BLENDED/CUSTOMIZED GRADE

- 8.4.1 ENHANCES MATERIAL VERSATILITY BY COMBINING WITH OTHER POLYMERS TO ACHIEVE TAILORED PERFORMANCE PROPERTIES

- 8.5 OTHER GRADES

9 POLYETHYLENE FURANOATE MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 BOTTLES

- 9.2.1 PEF BOTTLES MAINTAIN BEVERAGE FRESHNESS THROUGH SUPERIOR GAS BARRIER PROPERTIES

- 9.3 FIBERS

- 9.3.1 PEF FIBERS ENHANCE TEXTILE SUSTAINABILITY BY REDUCING RELIANCE ON FOSSIL FUELS

- 9.4 FILMS

- 9.4.1 PEF FILMS IMPROVE PACKAGING APPEAL WITH HIGH CLARITY AND PRINTABILITY

- 9.5 MOLDED COMPONENTS

- 9.5.1 PEF MOLDED PRODUCTS PROVIDE DURABILITY AND STRENGTH FOR CONSUMER AND INDUSTRIAL USE

- 9.6 EXTRUDED COMPONENTS

- 9.6.1 SUPERIOR MECHANICAL STRENGTH AND HEAT RESISTANCE TO DRIVE DEMAND

- 9.7 OTHER APPLICATIONS

10 POLYETHYLENE FURANOATE MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 PACKAGING

- 10.2.1 PEF STRENGTHENS PACKAGING WITH SUPERIOR BARRIER PROPERTIES AND SUSTAINABLE ALTERNATIVES TO PET

- 10.3 FIBER & TEXTILE

- 10.3.1 PEF FIBERS DRIVE SUSTAINABILITY IN TEXTILES WHILE DELIVERING STRENGTH, DURABILITY, AND BREATHABILITY

- 10.4 ELECTRONIC & ELECTRICAL COMPONENTS

- 10.4.1 PEF COMBINES MECHANICAL STRENGTH WITH INSULATING PROPERTIES FOR NEXT-GENERATION ELECTRONIC COMPONENTS

- 10.5 AUTOMOTIVE COMPONENTS

- 10.5.1 PEF ENABLES LIGHTWEIGHT, FUEL-EFFICIENT AUTOMOTIVE SOLUTIONS THROUGH MOLDABILITY AND GAS BARRIER STRENGTH

- 10.6 PHARMACEUTICALS

- 10.6.1 PEF ENHANCES PHARMACEUTICAL PACKAGING BY PROLONGING SHELF LIFE AND ENSURING PRODUCT INTEGRITY

- 10.7 OTHER END-USE INDUSTRIES

11 POLYETHYLENE FURANOATE MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Strategic advantage of abundant corn stover feedstock to drive market

- 11.2.2 CANADA

- 11.2.2.1 Strong government commitment to circular economy accelerates polyethylene furanoate adoption

- 11.2.3 MEXICO

- 11.2.3.1 Strategic geographic location boosts polyethylene furanoate market expansion

- 11.2.1 US

- 11.3 ASIA PACIFIC

- 11.3.1 CHINA

- 11.3.1.1 Robust agricultural waste utilization boosts polyethylene furanoate market growth

- 11.3.2 JAPAN

- 11.3.2.1 Advanced regulatory framework accelerates polyethylene furanoate market growth

- 11.3.3 INDIA

- 11.3.3.1 Rapid urbanization and government policies propel polyethylene furanoate market

- 11.3.4 SOUTH KOREA

- 11.3.4.1 Rapid E-commerce expansion drives demand for sustainable polyethylene furanoate packaging

- 11.3.5 REST OF ASIA PACIFIC

- 11.3.1 CHINA

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Rigorous environmental policies and circular economy drive polyethylene furanoate market growth

- 11.4.2 UK

- 11.4.2.1 Strategic push on sustainable beverage packaging accelerates polyethylene furanoate market growth

- 11.4.3 FRANCE

- 11.4.3.1 Strong government support and eco-conscious consumer base propel polyethylene furanoate market

- 11.4.4 ITALY

- 11.4.4.1 Commitment to sustainable fashion and packaging drives polyethylene furanoate market growth

- 11.4.5 SPAIN

- 11.4.5.1 Growing eco-conscious consumer base and regulatory support fuel polyethylene furanoate market

- 11.4.6 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Vision 2030 and industrial growth drive polyethylene furanoate market expansion

- 11.5.1.2 Rest of GCC countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Growing environmental awareness and agricultural resources drive polyethylene furanoate market growth

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Vast agricultural resources and growing eco-conscious market propel polyethylene furanoate demand

- 11.6.2 ARGENTINA

- 11.6.2.1 Agricultural wealth and growing sustainable packaging demand fuel polyethylene furanoate market

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.4.1 AVANTIUM

- 12.4.2 SULZER LTD

- 12.4.3 AVA BIOCEHM AG

- 12.4.4 ORIGIN MATERIALS

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.6.1 AVANTIUM

- 12.6.2 SULZER LTD

- 12.6.3 AVA BIOCHEM AG

- 12.6.4 ORIGIN MATERIALS

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Source footprint

- 12.7.5.4 Grade footprint

- 12.7.5.5 Application footprint

- 12.7.5.6 End-use industry footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 DEALS

- 12.9.2 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 AVANTIUM

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.3.2 Other developments

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 SULZER LTD

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Deals

- 13.1.2.3.2 Other developments

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 AVA BIOCHEM AG

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 ORIGIN MATERIALS

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 TOYOBO CO., LTD

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 MnM view

- 13.1.5.3.1 Key strengths

- 13.1.5.3.2 Strategic choices

- 13.1.5.3.3 Weaknesses and competitive threats

- 13.1.6 ZHEJIANG SUGAR ENERGY TECHNOLOGY CO., LTD

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 MnM view

- 13.1.6.3.1 Key strengths

- 13.1.6.3.2 Strategic choices

- 13.1.6.3.3 Weaknesses and competitive threats

- 13.1.7 SWICOFIL AG (DISTRIBUTOR)

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 MnM view

- 13.1.7.3.1 Key strengths

- 13.1.7.3.2 Strategic choices

- 13.1.7.3.3 Weaknesses and competitive threats

- 13.1.8 ALPLA

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 MnM view

- 13.1.9 DANONE

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 MnM view

- 13.1.10 EASTMAN CHEMICAL COMPANY

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Deals

- 13.1.10.4 MnM view

- 13.1.1 AVANTIUM

- 13.2 OTHER PLAYERS

- 13.2.1 THE COCA-COLA COMPANY

- 13.2.2 TERPHANE

- 13.2.3 LVMH

- 13.2.4 KVADRAT

- 13.2.5 CARLSBERG GROUP

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS