|

시장보고서

상품코드

1859655

엔지니어링 수지용 난연제 시장 : 유형별, 용도별, 최종 이용 산업별, 지역별 - 예측(-2030년)Flame Retardants for Engineering Resins Market by Type (Brominated, Phosphorous), Application (Polyamide, ABS, PET & PBT, PC/ABS Blends), End-use Industries (Electrical & Electronics, Automotive & Transportation), and Region - Global Forecast to 2030 |

||||||

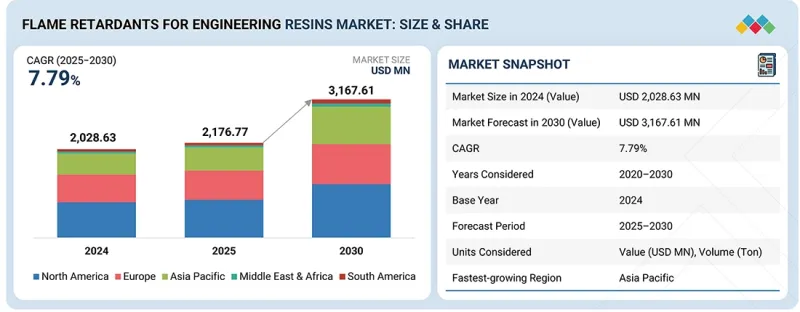

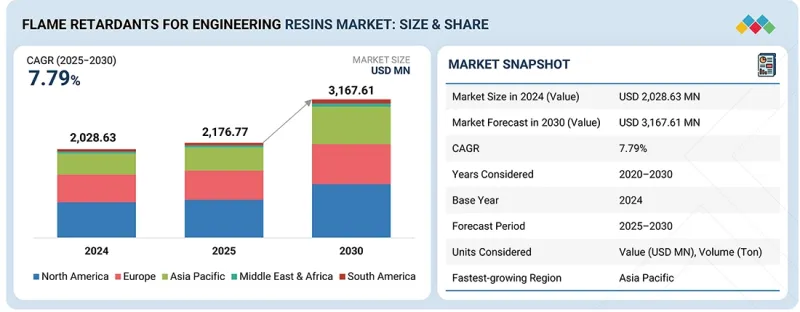

엔지니어링 수지용 난연제 시장 규모는 2025년 추정 22억 달러에서 2030년에는 32억 달러로 성장할 것으로 예상되며, 연평균 복합 성장률(CAGR)은 7.79%로 견조한 증가세를 보이며 큰 성장이 기대됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 연도 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 유닛 | 금액(100만 달러) 및 킬로톤 |

| 부문 | 유형별, 용도별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 아시아태평양, 북미, 유럽, 중동 및 아프리카, 남미 |

엔지니어링 수지용 난연제는 열 안정성, 내화성 향상, 연소성을 효과적으로 낮추고 화염 확산을 지연시키는 능력 등 우수한 특성을 가지고 있어 엔지니어링 수지용 난연제 채택에 박차를 가하고 있습니다. 전기 기기, 도포 방법, 재료의 혁신으로 엔지니어링 수지용 난연제의 성능, 기능성, 유연성이 크게 향상되었습니다. 이러한 요인들은 다양한 최종 이용 산업에서 엔지니어링 수지용 난연제에 대한 수요를 촉진하고 있습니다.

브롬계 난연제 부문은 그 효과와 광범위한 가용성으로 인해 전체 엔지니어링 수지용 난연제 시장에서 가장 큰 점유율을 차지하고 있습니다. 환경에 대한 관심이 높아지고 있음에도 불구하고, 효과적으로 가연성을 낮추는 능력이 입증되었고, 대체품에 비해 상대적으로 저렴하기 때문에 그 우위를 유지하고 있습니다. 또한, 다양한 엔지니어링 수지 배합에 대한 적합성과 엄격한 업계 표준으로 인해 시장 세분화에서 선도적 인 위치를 더욱 확고히하고 있습니다.

폴리아미드 부문은 엔지니어링 수지용 난연제의 가장 큰 용도이며, 그 주요 이유는 광범위한 난연 첨가제와의 호환성입니다. 폴리아미드 수지는 배합이 유연하기 때문에 제조업체는 원하는 기계적 및 열적 특성을 유지하면서 다양한 난연제를 배합할 수 있습니다. 이러한 다용도성으로 인해 폴리아미드계 엔지니어링 수지는 난연성과 재료 성능이 모두 중요한 용도에 적합합니다.

전기 및 전자 분야는 엔지니어링 수지용 난연제의 주요 최종사용자로서 우위를 점하고 있습니다. 다양한 분야에서 전자부품이 곳곳에 내장되어 있어 안전성을 높이고 규제를 준수하기 위해 난연성 소재가 요구되고 있습니다. 또한, 전 세계 전자기기 수요의 급증과 기술 발전이 맞물리면서 난연성이 우수한 엔지니어링 수지에 대한 요구가 높아지고 있습니다. 엄격한 산업 기준과 규제에 따라 엔지니어링 수지의 배합에 난연 첨가제를 포함하도록 의무화하여 가장 큰 최종 이용 산업으로 자리 매김하고 있습니다.

아시아태평양은 엔지니어링 수지용 난연제 시장에서 가장 빠르게 성장할 것으로 예상됩니다. 이 지역에서는 자동차, 전자, 건설 부문이 확대되고 있어 엔지니어링 수지에 사용되는 난연성 소재에 대한 수요가 증가하고 있습니다. 아시아태평양은 산업화와 도시화가 급속히 진행되고 인프라 구축이 진행됨에 따라 건축용 엔지니어링 수지용 난연제에 대한 수요가 증가하고 있습니다.

세계의 엔지니어링 수지용 난연제 시장에 대해 조사했으며, 유형별, 용도별, 최종 이용 산업별, 지역별 동향, 시장 진입 기업 프로파일 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

- 소개

- 시장 역학

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 지표

제6장 업계 동향

- 공급망 분석

- 가격 분석

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 생태계 분석

- 사례 연구 분석

- 기술 분석

- 무역 분석

- 규제 상황

- 주요 회의와 이벤트

- 투자와 자금 조달 시나리오

- 특허 분석

- 2025년 미국 관세의 영향 - 개요

- AI/생성형 AI가 엔지니어링 수지용 난연제 시장에 미치는 영향

제7장 엔지니어링 수지용 난연제 시장(유형별)

- 소개

- 브롬계 난연제

- 인계 난연제

- 기타 난연제

제8장 엔지니어링 수지용 난연제 시장(용도별)

- 소개

- 폴리아미드

- ABS

- PET와 PBT

- 폴리카보네이트

- PC/ABS 블렌드

- 기타

제9장 엔지니어링 수지용 난연제 시장(최종 이용 산업별)

- 소개

- 전기·전자공학

- 자동차·운송

- 기타

제10장 엔지니어링 수지용 난연제 시장(지역별)

- 소개

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 러시아

- 중동 및 아프리카

- GCC

- 남미

- 브라질

제11장 경쟁 구도

- 소개

- 주요 진출 기업의 전략

- 시장 점유율 분석

- 매출 분석

- 기업 평가 매트릭스 : 주요 진출 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 기업 평가와 재무 지표

- 브랜드/제품 비교

- 경쟁 시나리오

제12장 기업 개요

- 주요 진출 기업

- ALBEMARLE CORPORATION

- CLARIANT AG

- LANXESS AG

- BASF SE

- ISRAEL CHEMICALS LTD.

- NABALTEC AG

- HUBER ENGINEERED MATERIALS

- ITALMATCH CHEMICALS S.P.A.

- RTP COMPANY

- CHEMISCHE FABRIK BUDENHEIM KG

- ARKEMA S.A.

- 기타 기업

- GREENCHEMICALS SRL

- STAHL HOLDINGS B.V.

- GULEC CHEMICALS GMBH

- FRX POLYMERS, INC.

- CELANESE CORPORATION

- AMFINE CHEMICAL CORPORATION

- THOR GROUP LTD.

- AXIPOLYMER INC.

- DONGYING JINGDONG CHEMICAL CO., LTD.

- OTSUKA CHEMICAL CO., LTD.

- POLYPLASTICS CO., LTD.

- CENTURY MULTECH, INC.

- PRESAFER(QINGYUAN) PHOSPHOR CHEMICAL CO., LTD.

- QINGDAO FUNDCHEM CO., LTD.

제13장 인접 시장과 관련 시장

제14장 부록

KSM 25.11.17The flame retardants for engineering resins market is poised for significant growth, with a projected value of USD 3.2 billion by 2030 from the estimated USD 2.2 billion in 2025, exhibiting a robust CAGR of 7.79%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Type, Application, End-use Industry, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

The superior properties of flame retardants for engineering resins, such as thermal stability, enhanced fire resistance, and the ability to effectively reduce flammability and slow the spread of flames, are fueling the adoption of flame retardants for engineering resins. Innovations in electrical devices, application methods, and materials have significantly enhanced the performance, functionality, and flexibility of flame retardants for engineering resins. These factors are propelling the demand for flame retardants for engineering resins in various end-use industries.

"Brominated flame retardant segment to account for largest market share in 2025"

The brominated flame retardants segment accounts for the largest share of the overall flame retardants for engineering resins market due to their established efficacy and wide availability. Despite growing environmental concerns, their proven ability to effectively reduce flammability and their relatively lower cost compared to alternatives sustained their dominance. Additionally, their compatibility with various engineering resin formulations and stringent industry standards further solidified their leading position in the market segment.

"Polyamide to be largest application of flame retardants for engineering resins in 2025"

The polyamide segment is the largest application of flame retardants for engineering resins market, primarily due to its compatibility with a broad range of flame retardant additives. Polyamide resins offer flexibility in formulation, allowing manufacturers to incorporate various flame retardant agents while maintaining desirable mechanical and thermal properties. This versatility makes polyamide-based engineering resins a preferred choice for applications where both flame resistance and material performance are critical.

"Electrical & electronics to be largest end-use industry of flame retardants for engineering resins market in 2025"

The electrical & electronics sector asserts its dominance as the leading end user of flame retardants for engineering resins. The ubiquitous integration of electronic components across various sectors necessitated flame-retardant materials for enhanced safety and regulatory compliance. Moreover, the global surge in demand for electronic devices, coupled with technological advancements, fueled the requirement for engineering resins with superior fire resistance properties. Stringent industry standards and regulations mandated the incorporation of flame-retardant additives in engineering resin formulations, solidifying its position as the largest end-use industry.

"Asia Pacific to be fastest-growing flame retardants for engineering resins market during forecast period"

Asia Pacific is projected to be the fastest-growing market for flame retardants for engineering resins. The region's expanding automotive, electronics, and construction sectors are driving escalated demand for flame-retardant materials integrated into engineering resins. Robust industrialization and urbanization across Asia Pacific are fostering infrastructure development, thereby intensifying the requirement for flame retardants for engineering resins in construction applications.

In the process of determining and verifying market sizes for multiple segments and subsegments, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

- By Company Type: Tier 1 - 69%, Tier 2 - 23%, and Tier 3 - 8%

- By Designation: - Director Level - 27%, C-Level - 25%, and Others - 48%

- By Region: North America - 32%, Europe - 28%, Asia Pacific - 21%, South America - 12%, and Middle East & Africa - 7%

The key market players profiled in the report include Albemarle Corporation (US), LANXESS AG (Germany), BASF SE (Germany), Israel Chemicals Ltd. (Israel), Huber Engineered Materials (US), Clariant AG (Switzerland), Nabaltec AG (Germany), Italmatch Chemicals S.p.A (Italy), RTP Company (US), and Chemische Fabrik Budenheim KG (Germany).

Research Coverage

This report segments the market for flame retardants for engineering resins based on type, application, end-use industry, and region, and provides estimations for the overall value (USD million) of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisitions associated with the market for flame retardants for engineering resins.

Reasons to Buy this Report

This research report is focused on various levels of analysis-industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape; emerging and high-growth segments of the flame retardants for engineering resins; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Global rise in fire incidents, Stringent fire safety regulations, Increasing demand for engineering plastics in various industries), restraints (High loading levels of mineral-based flame retardants, Harmful chemicals used in flame retardants, Fluctuation in raw materials cost), opportunities (Introduction of more effective synergist compounds, Rising demand in consumer electronics), and challenges (Emphasis on environmental protection, Health risks associated with flame retardant chemicals)

- Market Penetration: Comprehensive information on the flame retardants for engineering resins offered by top players in the global flame retardants for engineering resins market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the flame retardants for engineering resins market.

- Market Development: Comprehensive information about lucrative emerging markets-the report analyzes the markets for flame retardants for engineering resins across regions

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global flame retardants for engineering resins market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the flame retardants for engineering resins market

- Impact of recession on the flame retardants for engineering resins market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key primary interview participants

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 GROWTH FORECAST

- 2.4.1 SUPPLY-SIDE ANALYSIS

- 2.4.2 DEMAND-SIDE ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLAME RETARDANTS FOR ENGINEERING RESINS MARKET

- 4.2 FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY REGION

- 4.3 NORTH AMERICA FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY END-USE INDUSTRY AND COUNTRY

- 4.4 REGIONAL FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY TYPE

- 4.5 FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 High rate of fire incidents worldwide

- 5.2.1.2 Implementation of stringent fire safety standards and regulations

- 5.2.1.3 Increasing demand for engineering plastics in various industries

- 5.2.2 RESTRAINTS

- 5.2.2.1 High loading levels of mineral-based flame retardants

- 5.2.2.2 Use of harmful chemicals in flame retardants

- 5.2.2.3 Fluctuation of raw materials costs

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Introduction of synergist compounds with high efficacy

- 5.2.3.2 Rising demand for consumer electronics

- 5.2.4 CHALLENGES

- 5.2.4.1 Emphasis on environmental protection

- 5.2.4.2 Health risks associated with flame retardant chemicals

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 MACROECONOMIC INDICATORS

- 5.5.1 GDP TRENDS AND FORECAST FOR MAJOR ECONOMIES

6 INDUSTRY TRENDS

- 6.1 SUPPLY CHAIN ANALYSIS

- 6.2 PRICING ANALYSIS

- 6.2.1 AVERAGE SELLING PRICE, BY KEY PLAYERS, 2024

- 6.2.2 AVERAGE SELLING PRICE TREND OF FLAME RETARDANTS FOR ENGINEERING RESINS, BY REGION, 2022-2030

- 6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 CASE STUDY ANALYSIS

- 6.5.1 ENHANCING SAFETY AND DURABILITY IN FLUID LEVEL MONITORING WITH RTP COMPANY'S FLAME RETARDANT COMPOUND

- 6.5.2 SUSTAINABLE FLAME RETARDANCY IN POLYOLEFIN FILM AND SHEET PRODUCTION WITH CLARIANT AG'S ADDWORKS LXR 920

- 6.6 TECHNOLOGY ANALYSIS

- 6.6.1 KEY TECHNOLOGIES

- 6.6.1.1 Halogenated flame retardants (HFRs)

- 6.6.1.2 Phosphorus-based flame retardants for engineering resins

- 6.6.2 COMPLIMENTARY TECHNOLOGIES

- 6.6.2.1 Synergists

- 6.6.1 KEY TECHNOLOGIES

- 6.7 TRADE ANALYSIS

- 6.7.1 IMPORT SCENARIO (HS CODE 382490)

- 6.7.2 EXPORT SCENARIO (HS CODE 382490)

- 6.8 REGULATORY LANDSCAPE

- 6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.8.2 REGULATORY FRAMEWORK

- 6.8.2.1 ISO 16000-31:2010

- 6.8.2.2 EU Regulation (EU) No 2019/1021 - Persistent Organic Pollutants (POPs)

- 6.9 KEY CONFERENCES AND EVENTS

- 6.10 INVESTMENT AND FUNDING SCENARIO

- 6.11 PATENT ANALYSIS

- 6.11.1 APPROACH

- 6.11.2 DOCUMENT TYPES

- 6.11.3 TOP APPLICANTS

- 6.11.4 JURISDICTION ANALYSIS

- 6.12 IMPACT OF 2025 US TARIFF - OVERVIEW

- 6.12.1 INTRODUCTION

- 6.12.2 KEY TARIFF RATES

- 6.12.3 PRICE IMPACT ANALYSIS

- 6.12.4 IMPACT ON COUNTRIES/REGIONS

- 6.12.4.1 US

- 6.12.4.2 Europe

- 6.12.4.3 Asia Pacific

- 6.12.5 IMPACT ON END-USE INDUSTRIES

- 6.13 IMPACT OF AI/GEN AI ON FLAME RETARDANTS FOR ENGINEERING RESINS MARKET

7 FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 BROMINATED FLAME RETARDANTS

- 7.2.1 WIDE ADOPTION IN VARIOUS APPLICATIONS FUELING MARKET GROWTH

- 7.2.2 BROMINATED EPOXY OLIGOMER

- 7.2.3 TETRABROMOBISPHENOL A

- 7.2.4 BROMINATED CARBONATE OLIGOMERS

- 7.2.5 1,2-BIS (2,4,6-TRIBROMOPHENOXY) ETHANE

- 7.2.6 DECABROMODIPHENYL ETHANE (DBDPE)

- 7.2.7 DECABROMODIPHENYL ETHER

- 7.2.8 TETRADECABROMODIPHENYL OXIDE

- 7.2.9 TETRADECABROMODIPHENOXY BENZENE

- 7.2.10 POLYDIBROMOSTYRENE (PDBS)

- 7.2.11 2,4,6 TRIS(2,4,6 TRIBROMOPHONXY)1,3,5 TRIAZINE

- 7.2.12 ETHYLENE BIS (TETRABROMOPHTHALTMIDE)

- 7.3 PHOSPHORUS FLAME RETARDANTS

- 7.3.1 HIGH THERMAL STABILITY AND LOW TOXICITY FUELING INCREASED ADOPTION

- 7.3.2 PHOSPHATE

- 7.3.3 PHOSPHINATE

- 7.3.4 RED PHOSPHORUS

- 7.3.5 PHOSPHITE

- 7.3.6 PHOSPHONATE

- 7.4 OTHER FLAME RETARDANTS

- 7.4.1 ANTIMONY OXIDE

- 7.4.2 CHLORINATED FLAME RETARDANTS

- 7.4.3 OTHERS

8 FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 POLYAMIDE

- 8.2.1 GROWING DEMAND FROM TRANSPORTATION SECTOR TO DRIVE MARKET

- 8.3 ABS

- 8.3.1 VERSATILITY OF ABS FUELING ADOPTION IN VARIOUS END-USE INDUSTRIES

- 8.4 PET & PBT

- 8.4.1 HIGH STABILITY AND EXCELLENT PROCESSING CHARACTERISTICS TO DRIVE DEMAND IN AUTOMOTIVE INDUSTRY

- 8.5 POLYCARBONATE

- 8.5.1 EXPANSION OF MEDICAL AND AUTOMOTIVE INDUSTRIES TO DRIVE DEMAND

- 8.6 PC/ABS BLENDS

- 8.6.1 GOOD MISCIBILITY AND HEAT-RESISTANT PROPERTIES TO DRIVE SEGMENTAL GROWTH

- 8.7 OTHER APPLICATIONS

9 FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY END-USE INDUSTRY

- 9.1 INTRODUCTION

- 9.2 ELECTRICAL & ELECTRONICS

- 9.2.1 GROWING USE OF PLASTIC PARTS TO DRIVE DEMAND DURING FORECAST PERIOD

- 9.3 AUTOMOTIVE & TRANSPORTATION

- 9.3.1 INCREASING FOCUS ON LIGHTWEIGHT AND FIRE-SAFE COMPONENTS TO BOOST DEMAND

- 9.4 OTHER END-USE INDUSTRIES

10 FLAME RETARDANTS FOR ENGINEERING RESINS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 ASIA PACIFIC

- 10.2.1 CHINA

- 10.2.1.1 Large presence of local manufacturers and distributors catering to growing international demand to drive market

- 10.2.2 JAPAN

- 10.2.2.1 Rising demand from automotive sector to support market growth

- 10.2.3 INDIA

- 10.2.3.1 Rising industrialization to drive demand

- 10.2.4 SOUTH KOREA

- 10.2.4.1 Growth of automotive industry to drive market

- 10.2.1 CHINA

- 10.3 NORTH AMERICA

- 10.3.1 US

- 10.3.1.1 Presence of dynamic electronics industry to support market growth

- 10.3.2 CANADA

- 10.3.2.1 Increased automotive sales to drive demand

- 10.3.3 MEXICO

- 10.3.3.1 Rising industrialization to drive market growth

- 10.3.1 US

- 10.4 EUROPE

- 10.4.1 GERMANY

- 10.4.1.1 Rising government expenditure on manufacturing sector to drive market

- 10.4.2 FRANCE

- 10.4.2.1 Expansion of electronics industry to be key driver for market growth

- 10.4.3 UK

- 10.4.3.1 Growth in automotive and construction industries to drive demand

- 10.4.4 ITALY

- 10.4.4.1 Strong automotive industry to drive market growth

- 10.4.5 RUSSIA

- 10.4.5.1 Rising demand from automotive sector to drive market

- 10.4.1 GERMANY

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 GCC

- 10.5.1.1 Saudi Arabia

- 10.5.1.1.1 Government investments in infrastructure development to drive market

- 10.5.1.1 Saudi Arabia

- 10.5.1 GCC

- 10.6 SOUTH AMERICA

- 10.6.1 BRAZIL

- 10.6.1.1 Increase in domestic automotive sales to drive demand

- 10.6.1 BRAZIL

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYERS' STRATEGIES

- 11.3 MARKET SHARE ANALYSIS

- 11.4 REVENUE ANALYSIS

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Type footprint

- 11.5.5.4 Application footprint

- 11.5.5.5 End-use industry footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUP/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.6.5.1 Detailed list of key startups/SMES

- 11.6.5.2 Competitive benchmarking of key startups/SMEs

- 11.7 COMPANY VALUATION AND FINANCIAL METRICS

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 PRODUCT LAUNCHES

- 11.9.2 DEALS

- 11.9.3 EXPANSIONS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 ALBEMARLE CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products/Solutions/Services offered

- 12.1.1.3 MnM view

- 12.1.1.3.1 Key strengths

- 12.1.1.3.2 Strategic choices

- 12.1.1.3.3 Weaknesses and competitive threats

- 12.1.2 CLARIANT AG

- 12.1.2.1 Business overview

- 12.1.2.2 Products/Solutions/Services offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Expansions

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 LANXESS AG

- 12.1.3.1 Business overview

- 12.1.3.2 Products/Solutions/Services offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 BASF SE

- 12.1.4.1 Business overview

- 12.1.4.2 Products/Solutions/Services offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.4 MnM View

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 ISRAEL CHEMICALS LTD.

- 12.1.5.1 Business overview

- 12.1.5.2 Products/Solutions/Services offered

- 12.1.5.3 MnM view

- 12.1.5.3.1 Key strengths

- 12.1.5.3.2 Strategic choices

- 12.1.5.3.3 Weaknesses and competitive threats

- 12.1.6 NABALTEC AG

- 12.1.6.1 Business overview

- 12.1.6.2 Products/Solutions/Services offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Expansions

- 12.1.6.4 MnM view

- 12.1.6.4.1 Key strengths

- 12.1.6.4.2 Strategic choices

- 12.1.6.4.3 Weaknesses and competitive threats

- 12.1.7 HUBER ENGINEERED MATERIALS

- 12.1.7.1 Business overview

- 12.1.7.2 Products/Solutions/Services offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.7.4 MnM view

- 12.1.7.4.1 Key strengths

- 12.1.7.4.2 Strategic choices

- 12.1.7.4.3 Weaknesses and competitive threats

- 12.1.8 ITALMATCH CHEMICALS S.P.A.

- 12.1.8.1 Business overview

- 12.1.8.2 Products/Solutions/Services offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Expansions

- 12.1.9 RTP COMPANY

- 12.1.9.1 Business overview

- 12.1.9.2 Products/Solutions/Services offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Expansions

- 12.1.10 CHEMISCHE FABRIK BUDENHEIM KG

- 12.1.10.1 Business overview

- 12.1.10.2 Products/Solutions/Services offered

- 12.1.11 ARKEMA S.A.

- 12.1.11.1 Business overview

- 12.1.11.2 Products/Solutions/Services offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Deals

- 12.1.1 ALBEMARLE CORPORATION

- 12.2 OTHER PLAYERS

- 12.2.1 GREENCHEMICALS SRL

- 12.2.2 STAHL HOLDINGS B.V.

- 12.2.3 GULEC CHEMICALS GMBH

- 12.2.4 FRX POLYMERS, INC.

- 12.2.5 CELANESE CORPORATION

- 12.2.6 AMFINE CHEMICAL CORPORATION

- 12.2.7 THOR GROUP LTD.

- 12.2.8 AXIPOLYMER INC.

- 12.2.9 DONGYING JINGDONG CHEMICAL CO., LTD.

- 12.2.10 OTSUKA CHEMICAL CO., LTD.

- 12.2.11 POLYPLASTICS CO., LTD.

- 12.2.12 CENTURY MULTECH, INC.

- 12.2.13 PRESAFER (QINGYUAN) PHOSPHOR CHEMICAL CO., LTD.

- 12.2.14 QINGDAO FUNDCHEM CO., LTD.

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 LIMITATION

- 13.3 FLAME RETARDANTS MARKET

- 13.3.1 MARKET DEFINITION

- 13.3.2 MARKET OVERVIEW

- 13.4 FLAME RETARDANTS MARKET, BY REGION

- 13.4.1 ASIA PACIFIC

- 13.4.2 NORTH AMERICA

- 13.4.3 WESTERN EUROPE

- 13.4.4 CENTRAL & EASTERN EUROPE

- 13.4.5 MIDDLE EAST & AFRICA

- 13.4.6 SOUTH AMERICA

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS