|

시장보고서

상품코드

1872636

시맨틱 웹 시장 : 제공별, 기술별, 용도별 - 예측(-2030년)Semantic Web Market by Offering (Knowledge Graph Platforms, Data Integration Tools, Reasoners & Inference Engines), Technology (RDF, OWL, SPARQL, Ontologies), Application (Data Interoperability & Integration, Digital Assets) - Global Forecast to 2030 |

||||||

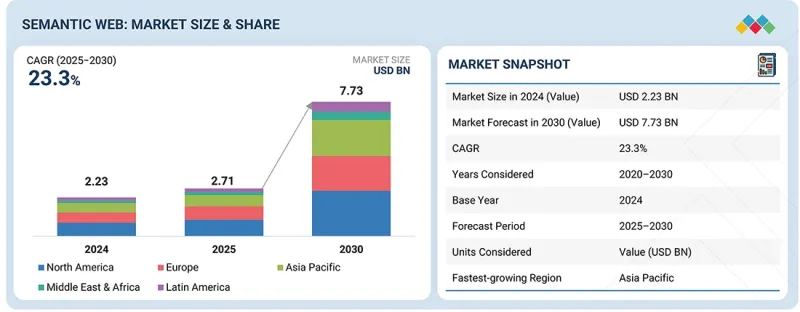

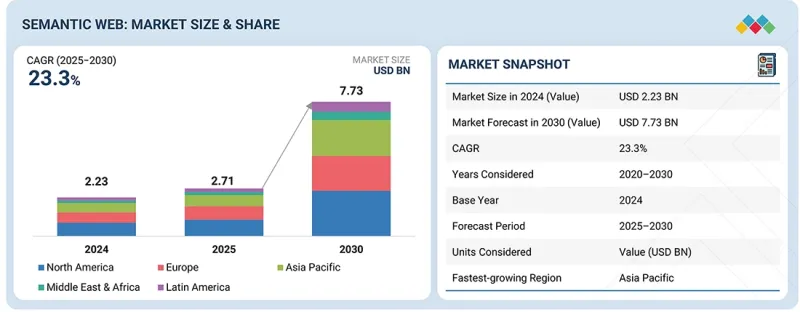

세계의 시맨틱 웹 시장 규모는 2025년 27억 1,000만 달러에서 2030년까지 77억 3,000만 달러에 이를 것으로 예측되며, CAGR로 23.3%를 나타낼 것으로 예상됩니다.

시장 성장은 디지털 에코시스템 전반에서 일관성, 상호 운용성 및 기계 가독성을 보장하는 구조화되고 설명 가능한 데이터 인프라에 기업의 주목을 받고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 100만/10억 달러 |

| 부문 | 제공, 기술, 용도, 산업, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동, 아프리카, 라틴아메리카 |

조직은 지식 그래프 플랫폼과 온톨로지 기반 프레임워크를 채택하여 분산된 데이터 소스 통합, 컨텍스트 검색 강화, AI 및 애널리틱스 워크플로우 전체에서 정확한 추론을 실현하고 있습니다. 금융 서비스, 의료 및 공공 부문의 규제 압력도 이러한 전환을 뒷받침하고 있으며, 데이터 투명성, 계보 추적 및 증거를 기반으로 한 의사 결정이 컴플라이언스 전략의 핵심입니다.

클라우드 기반 그래프 관리 온톨로지 호스팅 플랫폼은 시맨틱 기술에 대한 액세스를 확대하고, 인프라 복잡성을 줄이고, 멀티클라우드 환경에서 확장 가능한 배포를 지원합니다. 시맨틱 모델링과 AI와 자연 언어 이해의 융합은 데이터 분석과 인사이트 생성을 변화시켜 실시간 분석, 자율 시스템, 지능형 자동화에 새로운 기회를 창출하고 있습니다. 강력한 Linked Data 통합, SPARQL 쿼리 및 스키마 진화 기능을 제공하는 공급업체는 기업이 기존 데이터 관리에서 민첩성, 거버넌스 및 대규모 설명 가능한 AI를 지원하는 시맨틱 데이터 아키텍처로 전환하면서 경쟁 우위를 확보할 것으로 예측됩니다.

"컨텍스트에 추가된 데이터를 태깅하면 기업 전반에 걸친 시맨틱 웹 기술 채택이 가속화됩니다."

컨텍스트 인식 데이터 관리에 대한 관심이 높아짐에 따라 기계가 정보를 보다 정확하게 해석, 추론 및 행동할 수 있게 해주는 주석 기반 프레임워크의 급속한 채택이 진행되고 있습니다. 조직은 단편화 된 데이터 세트 통합, 상호 운용성 향상 및 AI 분석의 설명 가능성을 향상시키기 위해 시맨틱 태깅을 데이터 워크 플로우에 통합하는 경우가 증가하고 있습니다. 표준화된 어휘와 온톨로지 참조를 데이터 자산에 포함함으로써 기업은 부서와 시스템 간의 일관성을 보장하고 의료, 금융, 제조 등 부서에서 정확한 인사이트와 규정 준수를 준수하는 의사 결정을 지원할 수 있습니다.

자연 언어 처리와 온톨로지 정렬 기술을 통한 자동 태깅의 발전은 수작업 부하를 줄이면서 주석 품질을 향상시킵니다. 각 공급업체는 현재 데이터 팀이 시각적인터페이스와 코드 기반 사용자 정의를 통해 주석을 설정할 수 있는 모듈형 플랫폼을 제공합니다. 클라우드 네이티브 배포 모델은 실시간 업데이트, 대규모 확장성, 기존 데이터 레이크 및 지식 그래프 플랫폼과의 통합을 지원합니다. 데이터 양과 처리 빈도에 따른 가격 체계는 유연성을 유지하면서 단계적 채택을 촉진합니다. 기업이 투명성, 거버넌스, 의미적 일관성을 우선시 하는 중, 멀티클라우드 환경과 엔터프라이즈 환경 전체에서 AI 대응, 상호 운용성, 자기 기술성을 갖춘 데이터 에코시스템을 구축하는데 있어서, 주석 기술은 필수가 되고 있습니다.

"상호 운용성 수요와 거버넌스 중시의 전개에 의해 지식·데이터 관리가 2025년에 채용을 주도합니다"

지식 및 데이터 관리 용도는 시맨틱 웹 시장에서 가장 큰 점유율을 차지하며, 이는 복잡한 디지털 에코시스템 전반의 데이터 연계, 구조화 및 거버넌스에 대한 기업의 관심 증가를 반영합니다. 조직은 단편화된 데이터 소스의 통합, 발견성 향상 및 정확한 추론의 실현을 위해 시맨틱 모델, 온톨로지, 지식 그래프를 점점 활용하고 있습니다. 이러한 도구를 사용하면 데이터를 컨텍스트 머신에서 읽을 수 있으므로 분석, AI 추천 및 엔터프라이즈 검색의 신뢰성이 향상됩니다. 금융서비스, 의료, 정부 등의 규제부문에서는 시맨틱 데이터 관리가 투명성이 높은 리니지 추적에 의한 컴플라이언스 확보, 설명 가능한 인사이트의 제공, 근거에 근거한 의사결정 프로세스의 촉진을 실현합니다.

이 보고서는 세계의 시맨틱 웹 시장에 대한 조사 분석을 통해 주요 성장 촉진요인과 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 핵심 인사이트

- 시맨틱 웹의 상승

- 시맨틱 웹 이해 : 범위와 프레임워크

- 포장 및 상업 모델

- KPI와 가치 실현

- 의사결정자를 위한 전략적 필수요건

- 전망과 다음 지평

제5장 시장 개요

- 서론

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 수요(Unmet Needs)와 화이트 스페이스

- 시맨틱 웹 시장의 미충족 수요(Unmet Needs)

- 화이트 스페이스의 기회

- 상호 연결된 시장과 부문 간 기회

- 상호연결된 시장

- 부문 간 기회

- Tier 1/2/3 기업의 전략적 움직임

제6장 업계 동향

- 시맨틱 웹의 진화

- Porter's Five Forces 분석

- 공급망 분석

- 생태계 분석

- 지식 그래프 플랫폼 제공업체

- 온톨로지 매니지먼트 제공업체

- RDF 데이터 관리 제공업체

- 시맨틱 주석 제공업체

- 추론기 및 추론 엔진 제공업체

- Linked Data 플랫폼 제공업체

- 서비스 제공업체

- 가격 설정 분석

- 평균 판매 가격(2025년) : 주요 기업별

- 용도의 평균 판매 가격(2025년)

- 주요 컨퍼런스 및 이벤트(2025-2026년)

- 고객사업에 영향을 주는 동향/혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세의 영향(2025년) - 시맨틱 웹 시장

- 서론

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 미치는 영향

- 최종 이용 산업에 대한 영향

제7장 전략적 파괴 : 특허, 디지털, AI 채용

- 주요 신기술

- RDF(Resource Description Framework)

- OWL(Web Ontology Language)

- SPARQL

- RDFS 및 SHACL

- 지식 그래프 플랫폼

- 보완 기술

- 자연언어처리(NLP)

- Linked Data 및 JSON-LD

- 온톨로지 관리 도구

- API 통합 및 미들웨어

- 메타데이터 관리 및 데이터 카탈로그

- 인접 기술

- AI 및 머신러닝

- 빅데이터 및 클라우드 인프라

- 블록체인 및 분산형 아이덴티티

- 엣지 및 IoT

- 기술 로드맵

- 단기(2025-2027년) : 기반 구축 및 표준화 단계

- 중기(2028-2030년) : 컨버전스 및 자동화 단계

- 장기(2031-2035년) : 자율형 및 인지형 상호 운용성 단계

- 특허 분석

- 조사 방법

- 특허 출원수 : 서류 유형별(2016-2025년)

- 혁신과 특허출원

- 미래의 응용

- 지능형 데이터 패브릭 : 기업 전체의 상호 운용성

- 자율형 디지털 트윈 : 인지 시스템의 표현

- AI 오케스트레이션을 통한 지식 네트워크 : 컨텍스트 인식 엔터프라이즈 인텔리전스

- 의료 및 생명 과학 온톨로지 : 정밀 지식 통합

- 시맨틱 IoT 및 에지 시스템 : 머신 투 머신 이해

- 시맨틱 웹 시장에 대한 생성형 AI의 영향

- 지능형 지식 그래프 생성

- 온톨로지 생성 및 관리

- 컨텍스트 인식 시맨틱 검색

- 자동추론 및 인사이트 생성

- 데이터의 상호 운용성 및 표준화

- 시맨틱 강화 및 데이터 주석

제8장 규제 상황

- 지역 규제 및 규정 준수

- 규제기관, 정부기관, 기타 조직

- 주요 규제

제9장 고객정세와 구매행동

- 의사결정 프로세스

- 구매자 이해관계자와 구매평가 기준

- 채용 장벽과 내부 과제

- 다양한 업계의 미충족 수요(Unmet Needs)

제10장 시맨틱 웹 시장 : 제공별

- 서론

- 소프트웨어

- 서비스

제11장 시맨틱 웹 시장 : 기술별

- 서론

- 시맨틱 웹의 핵심 기술

- 인접 기술

제12장 시맨틱 웹 시장 : 용도별

- 서론

- 지식 및 데이터 관리

- 데이터 상호 운용성 및 통합

- IoT 및 스마트 환경

- 시맨틱 주석

- 웹 및 디지털 주석

- 기타 용도

제13장 시맨틱 웹 시장 : 업계별

- 서론

- BFSI

- 소매 및 E-Commerce

- 의료 및 생명과학

- 미디어 및 엔터테인먼트

- 통신

- 물류

- 에너지 및 유틸리티

- 정부 및 공공 부문

- 기타 산업

제14장 시맨틱 웹 시장 : 지역별

- 서론

- 북미

- 북미의 시맨틱 웹 시장 성장 촉진요인

- 북미의 거시경제 전망

- 미국

- 캐나다

- 유럽

- 유럽의 시맨틱 웹 시장 성장 촉진요인

- 유럽의 거시경제 전망

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 북유럽

- 기타 유럽

- 아시아태평양

- 아시아태평양의 시맨틱 웹 시장 성장 촉진요인

- 아시아태평양의 거시경제 전망

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동 및 아프리카의 시맨틱 웹 시장 성장 촉진요인

- 중동 및 아프리카의 거시경제 전망

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 튀르키예

- 카타르

- 기타 중동 및 아프리카

- 라틴아메리카

- 라틴아메리카의 시맨틱 웹 시장 성장 촉진요인

- 라틴아메리카의 거시경제 전망

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

제15장 경쟁 구도

- 개요

- 주요 참가 기업의 전략(2020-2025년)

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 제품 비교 분석

- 제품 비교 분석 : 온톨로지 매니지먼트 툴별

- 제품 비교 분석 : 지식 그래프 플랫폼별

- 제품 비교 분석 : 시맨틱 주석 툴별

- 기업 평가 매트릭스 : 주요 기업

- 기업 평가 매트릭스 : 스타트업 기업/중소기업

- 기업 평가 및 재무 지표

- 경쟁 시나리오

제16장 기업 프로파일

- 서론

- 주요 기업

- IBM

- AMAZON WEB SERVICES(AWS)

- ORACLE

- MICROSOFT

- SAP

- DASSAULT SYSTEMES

- ALTAIR(SIEMENS)

- PROGRESS SOFTWARE

- HUAWEI

- OPENTEXT

- INFORMATICA

- YEXT

- GLEAN

- ZIFO RND SOLUTIONS

- COLLIBRA

- TIBCO

- QLIK

- SAS INSTITUTE

- 스타트업/중소기업

- NEO4J

- CHAINALYSIS

- PENTAHO(HITACHI VANTARA)

- FLUREE

- SCIBITE(ELSEVIER)

- DATA GRAPHS

- NOETICA AI

- VEEZOO

- DATAVID

- WRITER

- ALATION

- STARDOG

- ONTOTEXT(GRAPHWISE)

- SEMANTIC WEB COMPANY(GRAPHWISE)

- METAPHACTS

- FRANZ INC.

- ECCENCA

- OPENLINK SOFTWARE

- TOPQUADRANT

- SYNAPTICA(SQUIRRO)

- TIMBR

- OXFORD SEMANTIC TECHNOLOGIES(SAMSUNG)

- BIOBOX ANALYTICS

제17장 인접 시장과 관련 시장

- 서론

- 지식 그래프 시장 - 세계 예측(-2030년)

- 시장 정의

- 시장 개요

- 그래프 데이터베이스 시장 - 세계 예측(-2030년)

- 시장 정의

- 시장 개요

제18장 부록

KTH 25.11.26The global semantic web market size is projected to grow from USD 2.71 billion in 2025 to USD 7.73 billion by 2030, at a CAGR of 23.3%. Market growth is driven by the increasing enterprise focus on structured and explainable data infrastructure to ensure consistency, interoperability, and machine readability across digital ecosystems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD Million/Billion |

| Segments | Offering, Technology, Application, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Organizations are adopting knowledge graph platforms and ontology-driven frameworks to unify disparate data sources, enhance contextual search, and enable accurate reasoning across AI and analytics workflows. Regulatory pressure in the financial services, healthcare, and public sectors is reinforcing this shift, as data transparency, lineage tracking, and evidence-based decision-making become central to compliance strategies.

Cloud-based graph management and ontology hosting platforms are expanding access to semantic technologies, reducing infrastructure complexity, and supporting scalable deployments across multi-cloud environments. The convergence of semantic modeling with AI and natural language understanding is transforming data interpretation and insight generation, creating new opportunities in real-time analytics, autonomous systems, and intelligent automation. Vendors that offer robust linked data integration, SPARQL querying, and schema evolution capabilities are expected to gain a competitive advantage as enterprises transition from traditional data management to semantic data architectures that support agility, governance, and explainable AI at scale.

"Context-enriched data tagging accelerates adoption of semantic web technologies across enterprises"

The growing focus on context-aware data management is driving rapid adoption of annotation-based frameworks that enable machines to interpret, reason, and act on information with greater precision. Organizations are increasingly integrating semantic tagging into their data workflows to unify fragmented datasets, improve interoperability, and enhance the explainability of AI-driven analytics. By embedding standardized vocabularies and ontological references into data assets, enterprises can ensure consistency across departments and systems, supporting accurate insights and compliant decision-making in sectors such as healthcare, finance, and manufacturing.

Advancements in automated tagging powered by natural language processing and ontology alignment are reducing manual effort while improving annotation quality. Vendors now offer modular platforms that allow data teams to configure annotations through both visual interfaces and code-based customization. Cloud-native deployment models support real-time updates, large-scale scalability, and integration with existing data lakes and knowledge graph platforms. Pricing structures based on data volume and processing frequency encourage incremental adoption while maintaining flexibility. As businesses prioritize transparency, governance, and semantic consistency, annotation technologies are becoming essential for building AI-ready, interoperable, and self-describing data ecosystems across multi-cloud and enterprise environments.

"Knowledge and data management leads adoption in 2025, driven by interoperability demands and governance-focused deployments"

Knowledge and data management applications account for the largest share of the semantic web market, reflecting enterprises' growing focus on connecting, structuring, and governing data across complex digital ecosystems. Organizations are increasingly leveraging semantic models, ontologies, and knowledge graphs to unify fragmented data sources, enhance discoverability, and enable accurate reasoning. These tools enable data to be contextualized and machine-readable, thereby enhancing the reliability of analytics, AI-driven recommendations, and enterprise search. In regulated sectors such as financial services, healthcare, and government, semantic data management ensures compliance through transparent lineage tracking, provides explainable insights, and facilitates evidence-based decision-making processes.

Vendors such as Oracle, IBM, and SAP are expanding their offerings to integrate semantic capabilities into existing data platforms, enabling enterprises to model relationships between entities, automate data mapping, and maintain consistent schemas across systems. Knowledge graph-powered solutions are increasingly being embedded within cloud, analytics, and AI platforms, enabling dynamic updates and real-time data synchronization. Demand is further supported by large-scale digital transformation programs and the shift toward AI-ready infrastructure. As enterprises prioritize governance, interoperability, and knowledge reuse, semantic knowledge and data management remain the foundational layer for intelligent, connected, and compliant data ecosystems.

"North America will have the largest market share in 2025, and Asia Pacific is slated to grow at the highest rate during the forecast period"

North America is expected to maintain the largest share of the semantic web market in 2025, led by the United States with strong contributions from Canada. The region's dominance is driven by enterprise-wide adoption of knowledge graphs, ontology-driven data management, and semantic integration frameworks that support regulatory compliance, interoperability, and explainable AI. Financial services, healthcare, and government sectors are driving adoption as organizations seek traceable, transparent, and machine-readable data for informed decision-making and automation. Major technology vendors, including Microsoft, IBM, Oracle, and AWS, are embedding semantic layers into their data and AI platforms, thereby enhancing discoverability and contextual analytics. The region also benefits from the presence of advanced cloud infrastructure and a strong ecosystem of data management providers, system integrators, and research institutions. Continued investment in AI standardization, linked data architectures, and digital governance is reinforcing North America's position as the core hub for semantic web innovation and enterprise-scale deployment.

Asia Pacific is projected to record the fastest growth in the semantic web market during the forecast period, supported by rapid digital transformation and expanding cloud ecosystems across India, China, Japan, and South Korea. Enterprises are deploying semantic frameworks to unify diverse data environments, improve real-time analytics, and meet emerging regulatory expectations around data transparency. Governments and large enterprises are promoting linked data initiatives for smart cities, digital healthcare, and financial interoperability, fueling demand for ontology-based and graph-powered solutions. The region's growth is further driven by accelerated adoption of AI, IoT, and 5G, which require structured and machine-interpretable data models. Vendors are localizing offerings with multilingual knowledge graphs, regional ontologies, and data residency compliance options. Strategic partnerships among hyperscalers, universities, and regional consultancies are fostering innovation and enabling organizations to operate semantic web technologies on a larger scale, positioning Asia Pacific as a key growth catalyst in the global market.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the semantic web market.

- By Company: Tier I - 31%, Tier II - 42%, and Tier III - 27%

- By Designation: Directors - 29%, Managers - 44%, and others - 27%

- By Region: North America - 40%, Europe - 22%, Asia Pacific - 26%, Middle East & Africa - 5%, and Latin America - 7%

The report includes the study and in-depth company profiles of key players offering semantic web software and services. The major players in the semantic web market include IBM (US), AWS (US), Oracle (US), Microsoft (US), SAP (Germany), Dassault Systems (France), Altair (Siemens) (US), Progress Software (US), Huawei (China), OpenText (Canada), Informatica (US), Yext (US), Glean (US), Zifo RnD Solutions (India), Collibra (Belgium), TIBCO (US), Qlik (US), SAS Institute (US), Neo4j (US), Chainalysis (US), Pentaho (Hitachi Vantara) (US), Fluree (US), SciBite (Elsevier) (US), Data Graphs (UK), Noetica AI (US), Veezoo (Switzerland), Datavid (UK), Writer (US), Alation (US), Stardog (US), Ontotext (GraphWise) (Bulgaria), Semantic Web Company (GraphWise) (Austria), Metaphacts (Germany), Franz Inc. (US), eccenca (Germany), OpenLink Software (US), TopQuadrant (US), Synaptica (Squirro) (US), Timbr (Israel), Oxford Semantic Technologies (Samsung) (UK), and BioBox Analytics (Canada).

Research Coverage

This research report categorizes the Semantic Web market by offering, technology, application, and vertical. The offering segment is split into semantic web software and semantic web services. The software segment is further split into ontology management tools, RDF data management systems, reasoners & inference engines, linked data platforms, semantic annotation tools, knowledge graph platforms, and other software. The services segment comprises training & consulting services, integration & deployment services, blockchain auditing services, semantic web development services, and semantic web streaming services. The technology segment is divided into core semantic web technologies and adjacent technologies. The semantic web core technologies include RDF, RDFS, OWL, SPARQL, URIs, ontologies, linked data principles, and semantic annotations. The adjacent technologies include AI & machine learning, edge computing, cloud & big data, and blockchain. The application segment spans knowledge & data management, data interoperability & integration, IoT & smart environments, semantic annotations, web & digital annotations, and other applications (digital assets, DAOS & decentralized governance, and decentralized identity & privacy). The vertical segment is split into BFSI, retail & e-commerce, healthcare & life sciences, IT & software, media & entertainment, telecommunications, logistics, energy & utilities, government, and other verticals. The regional analysis of the market covers North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America.

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the semantic web market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, solutions, and services, as well as key strategies, contracts, partnerships, agreements, product & service launches, mergers and acquisitions, and recent developments associated with the semantic web market. This report provides a competitive analysis of emerging startups in the semantic web market ecosystem.

Key Benefits of Buying the Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall semantic web market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Analysis of key drivers (Growing use of knowledge graphs fuels demand for structured, explainable data infrastructure, W3C standard updates are improving interoperability and driving enterprise confidence in long-term adoption, Stringent mandates on 'FAIR' data across regulated sectors are pushing organizations toward semantic data models, Expanding cloud-based graph and ontology services is lowering entry barriers and broadening commercial uptake), restraints (Persistent shortage of ontology and reasoning talent slowing project delivery and increasing deployment costs, Performance constraints in reasoning and inference limit real-time scalability and reduce enterprise readiness), opportunities (Domain-specific ontologies in healthcare, finance, and energy create high-value semantic solutions, Neural-symbolic integration allows vendors to extend semantic reasoning into Gen AI and hybrid AI platforms, Linked-data commercialization enables monetization of curated semantic datasets through APIs and marketplaces, Semantic extensions in BI and data catalogs expand adoption by embedding ontology layers in existing enterprise tools), and challenges (Maintaining ontology consistency across federated and evolving datasets remains a technical barrier to scale, Integrating semantic and relational systems without adding latency or redundancy remains a key engineering challenge)

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the semantic web market

Market Development: Comprehensive information about lucrative markets - analysis of the semantic web market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the semantic web market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of IBM (US), AWS (US), Oracle (US), Microsoft (US), SAP (Germany), Dassault Systems (France), Altair (Siemens) (US), Progress Software (US), Huawei (China), OpenText (Canada), Informatica (US), Yext (US), Glean (US), Zifo RnD Solutions (India), Collibra (Belgium), TIBCO (US), Qlik (US), SAS Institute (US), Neo4j (US), Chainalysis (US), Pentaho (Hitachi Vantara) (US), Fluree (US), SciBite (Elsevier) (US), Data Graphs (UK), Noetica AI (US), Veezoo (Switzerland), Datavid (UK), Writer (US), Alation (US), Stardog (US), Ontotext (GraphWise) (Bulgaria), Semantic Web Company (GraphWise) (Austria), Metaphacts (Germany), Franz Inc. (US), eccenca (Germany), OpenLink Software (US), TopQuadrant (US), Synaptica (Squirro) (US), Timbr (Israel), Oxford Semantic Technologies (Samsung) (UK), and BioBox Analytics (Canada), among others, in the semantic web market. The report also helps stakeholders understand the pulse of the semantic web market, providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 STUDY LIMITATIONS

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIVE TRENDS SHAPING MARKET

- 3.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 3.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 RISE OF SEMANTIC WEB

- 4.1.1 EVOLUTION FROM METADATA TO KNOWLEDGE GRAPHS

- 4.1.2 STANDARDIZATION OF RDF, OWL, AND LINKED DATA FRAMEWORKS

- 4.1.3 GROWING ROLE IN ENTERPRISE AI AND CONTEXTUAL INTELLIGENCE

- 4.2 UNDERSTANDING SEMANTIC WEB: SCOPE AND FRAMEWORKS

- 4.2.1 KNOWLEDGE GRAPHS VS. DATA FABRICS VS. ONTOLOGY-DRIVEN SYSTEMS

- 4.2.2 INTEROPERABILITY, FAIR DATA, AND DATA PROVENANCE MODELS

- 4.2.3 ROLE OF SEMANTIC STANDARDS IN AI EXPLAINABILITY AND GOVERNANCE

- 4.3 PACKAGING AND COMMERCIAL MODELS

- 4.3.1 STANDALONE PLATFORMS VS. INTEGRATED SEMANTIC LAYERS

- 4.3.2 PRIMARY PRICING METRICS: QUERY VOLUME, NODES, STORAGE, AND SEATS

- 4.3.3 CLOUD-NATIVE, ON-PREMISES, AND HYBRID DEPLOYMENT MODELS

- 4.4 KPIS AND VALUE REALIZATION

- 4.4.1 KNOWLEDGE UNIFICATION RATE, QUERY LATENCY, AND ONTOLOGY ACCURACY

- 4.4.2 GOVERNANCE, COMPLIANCE, AND DATA QUALITY METRICS

- 4.4.3 ROI FROM LINKED DATA, AUTOMATION EFFICIENCY, AND AI GROUNDING

- 4.5 STRATEGIC IMPERATIVES FOR DECISION-MAKERS

- 4.5.1 CHOOSING RIGHT SEMANTIC STACK FOR ENTERPRISE WORKLOADS

- 4.5.2 ALIGNING ONTOLOGIES WITH DATA GOVERNANCE AND POLICY FRAMEWORKS

- 4.5.3 INTEGRATING SEMANTICS WITH AI, ML, AND GENERATIVE MODELS

- 4.5.4 BUILDING ENTERPRISE KNOWLEDGE GRAPH MATURITY ROADMAPS

- 4.6 OUTLOOK AND NEXT HORIZONS

- 4.6.1 AI-SEMANTIC CONVERGENCE AND HYBRID REASONING MODELS

- 4.6.2 SEMANTIC WEB IN REGULATED AND MISSION-CRITICAL ENVIRONMENTS

- 4.6.3 RISE OF AUTONOMOUS KNOWLEDGE SYSTEMS AND SELF-LEARNING ONTOLOGIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing use of knowledge graphs fuels demand for structured, explainable data infrastructure

- 5.2.1.2 W3C standard updates improving interoperability and driving enterprise confidence in long-term adoption

- 5.2.1.3 Stringent mandates on 'FAIR' data across regulated sectors pushing organizations toward semantic data models

- 5.2.1.4 Expanding cloud-based graph and ontology services lowering entry barriers and broadening commercial uptake

- 5.2.2 RESTRAINTS

- 5.2.2.1 Persistent shortage of ontology and reasoning talent slowing project delivery and increasing deployment costs

- 5.2.2.2 Performance constraints in reasoning and inference limit real-time scalability and reduce enterprise readiness

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Domain-specific ontologies in healthcare, finance, and energy create high-value semantic solutions

- 5.2.3.2 Neural-symbolic integration allows vendors to extend semantic reasoning into Gen AI and Hybrid AI platforms

- 5.2.3.3 Linked-data commercialization enables monetization of curated semantic datasets through APIs and marketplaces

- 5.2.3.4 Semantic extensions in BI and data catalogs expand adoption by embedding ontology layers in existing enterprise tools

- 5.2.4 CHALLENGES

- 5.2.4.1 Maintaining ontology consistency across federated and evolving datasets remains technical barrier to scale

- 5.2.4.2 Integrating semantic and relational systems without adding latency or redundancy remains key engineering challenge

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN SEMANTIC WEB MARKET

- 5.3.2 WHITE SPACE OPPORTUNITIES

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 5.5.1 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

6 INDUSTRY TRENDS

- 6.1 EVOLUTION OF SEMANTIC WEB

- 6.2 PORTER'S FIVE FORCES ANALYSIS

- 6.2.1 THREAT OF NEW ENTRANTS

- 6.2.2 THREAT OF SUBSTITUTES

- 6.2.3 BARGAINING POWER OF SUPPLIERS

- 6.2.4 BARGAINING POWER OF BUYERS

- 6.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.3 SUPPLY CHAIN ANALYSIS

- 6.4 ECOSYSTEM ANALYSIS

- 6.4.1 KNOWLEDGE GRAPH PLATFORM PROVIDERS

- 6.4.2 ONTOLOGY MANAGEMENT PROVIDERS

- 6.4.3 RDF DATA MANAGEMENT PROVIDERS

- 6.4.4 SEMANTIC ANNOTATION PROVIDERS

- 6.4.5 REASONERS & INFERENCE ENGINE PROVIDERS

- 6.4.6 LINKED DATA PLATFORM PROVIDERS

- 6.4.7 SERVICE PROVIDERS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE OF OFFERINGS, BY KEY PLAYER, 2025

- 6.5.2 AVERAGE SELLING PRICE OF APPLICATIONS, 2025

- 6.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.8 INVESTMENT AND FUNDING SCENARIO

- 6.9 CASE STUDY ANALYSIS

- 6.9.1 NOVO NORDISK ENHANCED CLINICAL STUDY DATA MANAGEMENT WITH NEO4J

- 6.9.2 ASTRAZENECA ACCELERATED R&D WITH FAIR DATA STRATEGY POWERED BY ECCENCA CORPORATE MEMORY

- 6.9.3 SLOANE LAB AND METAPHACTS BRIDGED FRAGMENTED HISTORICAL COLLECTIONS USING KNOWLEDGE GRAPHS

- 6.9.4 NASA STREAMLINED MISSION-CRITICAL ENGINEERING DECISIONS WITH STARDOG'S KNOWLEDGE GRAPH SOLUTION

- 6.9.5 US COUNTY GOVERNMENT AUTOMATED RECORD MANAGEMENT AND EMAIL CLASSIFICATION WITH OPENTEXT

- 6.9.6 BOOKER ENHANCED DIGITAL PRESENCE WITH YEXT, ACHIEVING 38% GROWTH IN UNBRANDED SEARCH VISIBILITY

- 6.10 IMPACT OF 2025 US TARIFF - SEMANTIC WEB MARKET

- 6.10.1 INTRODUCTION

- 6.10.1.1 Tariff/Trade Policy Updates (Aug-Sep 2025)

- 6.10.2 KEY TARIFF RATES

- 6.10.3 PRICE IMPACT ANALYSIS

- 6.10.3.1 Strategic shifts and emerging trends

- 6.10.4 IMPACT ON COUNTRY/REGION

- 6.10.4.1 US

- 6.10.4.2 China

- 6.10.4.3 Europe

- 6.10.4.4 Asia Pacific (excluding China)

- 6.10.5 IMPACT ON END-USE INDUSTRIES

- 6.10.5.1 BFSI

- 6.10.5.2 Retail & E-commerce

- 6.10.5.3 Healthcare & Life Sciences

- 6.10.5.4 IT & Software

- 6.10.5.5 Government & Public Sector

- 6.10.5.6 Media & Entertainment

- 6.10.5.7 Other Verticals

- 6.10.1 INTRODUCTION

7 STRATEGIC DISRUPTION: PATENTS, DIGITAL, AND AI ADOPTIONS

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 RDF (RESOURCE DESCRIPTION FRAMEWORK)

- 7.1.2 OWL (WEB ONTOLOGY LANGUAGE)

- 7.1.3 SPARQL

- 7.1.4 RDFS & SHACL

- 7.1.5 KNOWLEDGE GRAPH PLATFORMS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 NATURAL LANGUAGE PROCESSING (NLP)

- 7.2.2 LINKED DATA & JSON-LD

- 7.2.3 ONTOLOGY MANAGEMENT TOOLS

- 7.2.4 API INTEGRATION & MIDDLEWARE

- 7.2.5 METADATA MANAGEMENT & DATA CATALOGS

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 7.3.2 BIG DATA AND CLOUD INFRASTRUCTURE

- 7.3.3 BLOCKCHAIN AND DECENTRALIZED IDENTITY

- 7.3.4 EDGE AND INTERNET OF THINGS (IOT)

- 7.4 TECHNOLOGY ROADMAP

- 7.4.1 SHORT TERM (2025-2027): FOUNDATION AND STANDARDIZATION PHASE

- 7.4.2 MID TERM (2028-2030): CONVERGENCE AND AUTOMATION PHASE

- 7.4.3 LONG TERM (2031-2035): AUTONOMOUS AND COGNITIVE INTEROPERABILITY PHASE

- 7.5 PATENT ANALYSIS

- 7.5.1 METHODOLOGY

- 7.5.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2025

- 7.5.3 INNOVATION AND PATENT APPLICATIONS

- 7.6 FUTURE APPLICATIONS

- 7.6.1 INTELLIGENT DATA FABRICS: ENTERPRISE-WIDE INTEROPERABILITY

- 7.6.2 AUTONOMOUS DIGITAL TWINS: COGNITIVE SYSTEM REPRESENTATION

- 7.6.3 AI-ORCHESTRATED KNOWLEDGE NETWORKS: CONTEXT-AWARE ENTERPRISE INTELLIGENCE

- 7.6.4 HEALTHCARE & LIFE SCIENCES ONTOLOGIES: PRECISION KNOWLEDGE INTEGRATION

- 7.6.5 SEMANTIC IOT AND EDGE SYSTEMS: MACHINE-TO-MACHINE UNDERSTANDING

- 7.7 IMPACT OF GENERATIVE AI ON SEMANTIC WEB MARKET

- 7.7.1 INTELLIGENT KNOWLEDGE GRAPH GENERATION

- 7.7.2 ONTOLOGY CREATION AND MANAGEMENT

- 7.7.3 CONTEXT-AWARE SEMANTIC SEARCH

- 7.7.4 AUTOMATED REASONING AND INSIGHT GENERATION

- 7.7.5 DATA INTEROPERABILITY AND STANDARDIZATION

- 7.7.6 SEMANTIC ENRICHMENT AND DATA ANNOTATION

8 REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 KEY REGULATIONS

- 8.1.2.1 North America

- 8.1.2.1.1 Federal Data Strategy and Open Government Data Act (United States)

- 8.1.2.1.2 Federal Data Interoperability and Information Management Policy, Directive on Service and Digital (Canada)

- 8.1.2.1.3 Personal Information Protection and Electronic Documents Act, PIPEDA (Canada)

- 8.1.2.2 Europe

- 8.1.2.2.1 Data Governance Act, Regulation (EU) 2022/868 (European Union)

- 8.1.2.2.2 Open Data Directive, Directive (EU) 2019/1024 on Open Data and the Reuse of Public Sector Information (European Union)

- 8.1.2.2.3 European Interoperability Framework, EIF (European Union)

- 8.1.2.2.4 European Health Data Space Proposal, COM (2022) 197 (European Union)

- 8.1.2.2.5 Gaia X Trust Framework and Federation Services Policy Rules (European Union)

- 8.1.2.2.6 National Data Strategy under the Data Institute Act draft (Germany)

- 8.1.2.2.7 National Artificial Intelligence Strategy and National Interoperability Framework ENS (Spain)

- 8.1.2.3 Asia Pacific

- 8.1.2.3.1 Data Governance Framework and Smart Nation Open Data Policy (Singapore)

- 8.1.2.3.2 Industrial Structure Council Reference Architecture for Data Collaboration, including IVI and Manufacturing Data Spaces (Japan)

- 8.1.2.3.3 Personal Data Protection Act and Public Sector Data Sharing Framework (Singapore)

- 8.1.2.3.4 National Digital Public Infrastructure and India Data Accessibility & Use Policy (India)

- 8.1.2.3.5 Digital Government Data Sharing and Government Data Interoperability Standards under Digital Government Blueprint (Australia)

- 8.1.2.4 Middle East & Africa

- 8.1.2.4.1 National Data Management and Personal Data Protection Standards (Saudi Arabia)

- 8.1.2.4.2 Digital Government Authority Interoperability Policy (Saudi Arabia)

- 8.1.2.4.3 Federal Data Protection Law and Emirates Data Management Law for Open Data and Data Exchange (United Arab Emirates)

- 8.1.2.4.4 National Open Data Policy and Government-Wide Enterprise Architecture (United Arab Emirates)

- 8.1.2.4.5 Protection of Personal Information Act, POPIA (South Africa)

- 8.1.2.4.6 National AI and Data Strategy and Open Data Portal Framework (Qatar)

- 8.1.2.5 Latin America

- 8.1.2.5.1 LGPD and Brazilian National Data Sharing Decree for Citizen Data Interoperability (Brazil)

- 8.1.2.5.2 National Digital Government and Interoperability Framework (Peru)

- 8.1.2.5.3 National Digital Transformation Strategy and Interoperability Policy for Public Sector Data Exchange (Chile)

- 8.1.2.5.4 Cloud First and Interoperability Technical Standard (Mexico)

- 8.1.2.5.5 Government Open Data Law and National Catalog of Public Information Reuse, Decreto 117/2016 (Uruguay)

- 8.1.2.1 North America

9 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 9.2.1 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 9.4 UNMET NEEDS FROM VARIOUS INDUSTRY VERTICALS

10 SEMANTIC WEB MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.1.1 OFFERING: SEMANTIC WEB MARKET DRIVERS

- 10.2 SOFTWARE

- 10.2.1 ONTOLOGY MANAGEMENT TOOLS

- 10.2.1.1 Growth driven by enterprise need for semantic governance, AI explainability, and cross-domain data standardization

- 10.2.1.2 Ontology editors

- 10.2.1.3 Ontology validators

- 10.2.1.4 Ontology versioning

- 10.2.1.5 Ontology alignment

- 10.2.2 RDF DATA MANAGEMENT SYSTEMS

- 10.2.2.1 Expansion fueled by adoption of data fabrics and open standards enabling interoperability and linked data publishing

- 10.2.2.2 Triple stores

- 10.2.2.3 Quad stores

- 10.2.2.4 SPARQL endpoints

- 10.2.3 REASONERS & INFERENCE ENGINES

- 10.2.3.1 Accelerating demand for explainable AI driving reasoning tools adoption in enterprise knowledge systems

- 10.2.3.2 OWL DL reasoners

- 10.2.3.3 Rule-based reasoners

- 10.2.3.4 Hybrid reasoners

- 10.2.3.5 Distributed reasoners

- 10.2.4 LINKED DATA PLATFORMS

- 10.2.4.1 Growing momentum from government open-data mandates and corporate interoperability initiatives under FAIR principles

- 10.2.4.2 Data publishing frameworks

- 10.2.4.3 Data linking

- 10.2.4.4 Data consumption

- 10.2.4.5 Data transformation

- 10.2.5 SEMANTIC ANNOTATION TOOLS

- 10.2.5.1 Rising use of Gen AI and LLMs requiring ontology-based contextual tagging for grounding and accuracy

- 10.2.5.2 Text annotation

- 10.2.5.3 Entity extraction

- 10.2.5.4 Ontology linking

- 10.2.5.5 Metadata management

- 10.2.6 KNOWLEDGE GRAPH PLATFORMS

- 10.2.6.1 Rapid adoption as enterprises build context-aware AI, digital twins, and decision intelligence systems

- 10.2.6.2 Graph databases

- 10.2.6.3 Data integration

- 10.2.6.4 Query languages

- 10.2.6.5 Visualization tools

- 10.2.7 OTHER SOFTWARE

- 10.2.1 ONTOLOGY MANAGEMENT TOOLS

- 10.3 SERVICES

- 10.3.1 INTEGRATION & DEPLOYMENT SERVICES

- 10.3.1.1 Increasing enterprise need for seamless ontology-driven integration across hybrid data fabrics and AI ecosystems

- 10.3.2 TRAINING & CONSULTING SERVICES

- 10.3.2.1 Rising demand for skilled professionals and strategic advisory to operationalize semantic architectures and AI governance frameworks

- 10.3.3 SEMANTIC WEB DEVELOPMENT SERVICES

- 10.3.3.1 Rising enterprise demand for custom semantic applications that integrate reasoning, AI, and linked data for contextual automation

- 10.3.4 BLOCKCHAIN AUDITING SERVICES

- 10.3.4.1 Accelerating need for transparent, ontology-based blockchain auditing frameworks to ensure provenance, and ESG accountability

- 10.3.5 SEMANTIC WEB STREAMING SERVICES

- 10.3.5.1 Surging enterprise adoption of ontology-driven reasoning frameworks for adaptive AI, and digital twin operations

- 10.3.1 INTEGRATION & DEPLOYMENT SERVICES

11 SEMANTIC WEB MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.1.1 TECHNOLOGY: SEMANTIC WEB MARKET DRIVERS

- 11.2 SEMANTIC WEB CORE TECHNOLOGIES

- 11.2.1 RDF

- 11.2.1.1 Enabling unified and intelligent data ecosystems to drive enterprise automation

- 11.2.2 RDF SCHEMA (RDFS)

- 11.2.2.1 Enabling semantic hierarchies and schema standardization to drive interoperable knowledge systems

- 11.2.3 OWL

- 11.2.3.1 Enhancing knowledge modeling and automated reasoning to drive intelligent decision-making

- 11.2.4 SPARQL

- 11.2.4.1 Enabling advanced semantic querying and data-driven insights to drive enterprise intelligence

- 11.2.5 URIS

- 11.2.5.1 Establishing unique data identification and connectivity to drive knowledge integration

- 11.2.6 ONTOLOGIES

- 11.2.6.1 Structuring domain knowledge and enabling intelligent insights to drive enterprise decision-making

- 11.2.7 LINKED DATA PRINCIPLES

- 11.2.7.1 Connecting distributed data sources to drive scalable knowledge integration

- 11.2.8 SEMANTIC ANNOTATIONS

- 11.2.8.1 Enhancing content discoverability and knowledge-driven insights across enterprises

- 11.2.1 RDF

- 11.3 ADJACENT TECHNOLOGIES

- 11.3.1 AI & MACHINE LEARNING

- 11.3.1.1 Accelerating intelligent insights and data accuracy across enterprise systems

- 11.3.2 EDGE COMPUTING

- 11.3.2.1 Accelerating real-time semantic insights and distributed knowledge processing

- 11.3.3 CLOUD & BIG DATA

- 11.3.3.1 Scaling knowledge graphs and semantic analytics for enterprise efficiency

- 11.3.4 BLOCKCHAIN

- 11.3.4.1 Ensuring trusted and verifiable knowledge with blockchain-enabled semantic frameworks

- 11.3.1 AI & MACHINE LEARNING

12 SEMANTIC WEB MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.1.1 APPLICATION: SEMANTIC WEB MARKET DRIVERS

- 12.2 KNOWLEDGE & DATA MANAGEMENT

- 12.2.1 DRIVING AI-ENHANCED FRAMEWORKS FOR SCALABLE AND CONTEXT-AWARE DATA SOLUTIONS

- 12.2.2 KNOWLEDGE GRAPHS

- 12.2.3 SEMANTIC SEARCH

- 12.2.4 METADATA/CONTENT MANAGEMENT

- 12.3 DATA INTEROPERABILITY & INTEGRATION

- 12.3.1 ENABLING SEAMLESS DATA CONNECTIVITY TO DRIVE INTEGRATED AND INTELLIGENT ENTERPRISE OPERATIONS

- 12.3.2 CROSS-DATASET QUERYING

- 12.3.3 LINKED DATA PUBLISHING AND CONSUMPTION

- 12.3.4 SEMANTIC DATA FUSION

- 12.4 IOT & SMART ENVIRONMENTS

- 12.4.1 ENABLING INTELLIGENT AND CONTEXT-AWARE CONNECTIVITY TO DRIVE SMARTER OPERATIONAL ECOSYSTEMS

- 12.4.2 DEVICE & ASSET DATA LINKING

- 12.4.3 SMART CITIES & INDUSTRY 4.0 INTEGRATION

- 12.5 SEMANTIC ANNOTATIONS

- 12.5.1 EMBEDDING CONTEXTUAL INTELLIGENCE TO DRIVE ENHANCED DISCOVERABILITY AND INSIGHT GENERATION

- 12.6 WEB & DIGITAL ANNOTATIONS

- 12.6.1 ENHANCING DIGITAL CONTENT WITH SEMANTIC INTELLIGENCE TO DRIVE SMARTER DISCOVERY AND AUTOMATION

- 12.6.2 DIGITAL LIBRARIES & ARCHIVES

- 12.6.3 PERSONALIZATION & RECOMMENDATION ENGINES

- 12.7 OTHER APPLICATIONS

- 12.7.1 DIGITAL ASSETS

- 12.7.2 DAOS & DECENTRALIZED GOVERNANCE

- 12.7.3 DECENTRALIZED IDENTITY & PRIVACY

13 SEMANTIC WEB MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 VERTICAL: SEMANTIC WEB MARKET DRIVERS

- 13.2 BFSI

- 13.2.1 SEMANTIC REASONING AND AI-GROUNDED KNOWLEDGE GRAPHS ARE REDEFINING REGULATORY TRANSPARENCY

- 13.2.2 RISK ANALYTICS

- 13.2.3 FRAUD DETECTION

- 13.2.4 CUSTOMER KNOWLEDGE GRAPHS

- 13.2.5 OTHER BFSI USE CASES

- 13.3 RETAIL & E-COMMERCE

- 13.3.1 ONTOLOGY-DRIVEN PRODUCT HARMONIZATION TRANSFORMING RETAIL INTO CONTEXT-AWARE, DATA-INTELLIGENT ECOSYSTEM

- 13.3.2 PRODUCT DATA HARMONIZATION

- 13.3.3 PERSONALIZED RECOMMENDATIONS

- 13.3.4 OTHER RETAIL & E-COMMERCE USE CASES

- 13.4 HEALTHCARE & LIFE SCIENCES

- 13.4.1 ONTOLOGY-LED INTEROPERABILITY IS TRANSFORMING HEALTHCARE & LIFE SCIENCES INTO UNIFIED, INTELLIGENT DATA ECOSYSTEMS

- 13.4.2 PATIENT DATA INTEGRATION

- 13.4.3 CLINICAL DECISION SUPPORT

- 13.4.4 DRUG DISCOVERY ONTOLOGIES

- 13.4.5 CLINICAL TRIAL DATA HARMONIZATION

- 13.4.6 OTHER HEALTHCARE & LIFE SCIENCES USE CASES

- 13.5 MEDIA & ENTERTAINMENT

- 13.5.1 SEMANTIC INTELLIGENCE REDEFINING MEDIA OPERATIONS BY LINKING CREATIVE ASSETS AND MONETIZATION FRAMEWORKS

- 13.5.2 CROSS-PLATFORM CONTENT RECOMMENDATION

- 13.5.3 CONTENT RIGHTS & LICENSING MANAGEMENT

- 13.5.4 DYNAMIC CONTENT LINKING

- 13.5.5 OTHER MEDIA & ENTERTAINMENT USE CASES

- 13.6 TELECOMMUNICATIONS

- 13.6.1 SEMANTIC MODELING IS MODERNIZING TELECOM INFRASTRUCTURE BY CREATING SELF-OPTIMIZING NETWORK ECOSYSTEMS

- 13.6.2 NETWORK ASSET MANAGEMENT

- 13.6.3 CUSTOMER INTELLIGENCE MAPPING

- 13.6.4 SERVICE CATALOG STANDARDIZATION

- 13.6.5 OTHER TELECOMMUNICATIONS USE CASES

- 13.7 LOGISTICS

- 13.7.1 SHIPMENTS, ASSETS, AND INTELLIGENCE BEING LINKED INTO UNIFIED DATA FABRIC VIA SEMANTIC MODELLING

- 13.7.2 END-TO-END SHIPMENT VISIBILITY

- 13.7.3 SMART ASSET TRACKING

- 13.7.4 OPTIMIZED ROUTE PLANNING

- 13.7.5 OTHER LOGISTICS USE CASES

- 13.8 ENERGY & UTILITIES

- 13.8.1 SEMANTIC INTELLIGENCE ENABLING PREDICTIVE, AND SUSTAINABLE ENERGY ECOSYSTEMS ACROSS SMART GRIDS

- 13.8.2 SMART GRID INTEROPERABILITY

- 13.8.3 ASSET LIFECYCLE OPTIMIZATION

- 13.8.4 ENERGY MARKET DATA SHARING

- 13.8.5 OTHER ENERGY & UTILITIES USE CASES

- 13.9 GOVERNMENT & PUBLIC SECTOR

- 13.9.1 SEMANTIC FRAMEWORKS ARE ENABLING UNIFIED, DATA-DRIVEN GOVERNANCE BY LINKING CITIZENS, SERVICES, AND POLICIES

- 13.9.2 INTEGRATED CITIZEN SERVICES

- 13.9.3 CROSS-AGENCY ANALYTICS

- 13.9.4 OTHER GOVERNMENT & PUBLIC SECTOR USE CASES

- 13.10 OTHER VERTICALS

14 SEMANTIC WEB MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: SEMANTIC WEB MARKET DRIVERS

- 14.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 14.2.3 US

- 14.2.3.1 Accelerating semantic integration for healthcare and enterprise analytics

- 14.2.4 CANADA

- 14.2.4.1 Advancing data harmonization across energy, industry, and research sectors

- 14.3 EUROPE

- 14.3.1 EUROPE: SEMANTIC WEB MARKET DRIVERS

- 14.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 14.3.3 UK

- 14.3.3.1 Advancing interoperable knowledge frameworks for public and research data

- 14.3.4 GERMANY

- 14.3.4.1 Harnessing semantic knowledge networks for industrial and research excellence

- 14.3.5 FRANCE

- 14.3.5.1 Leveraging semantic technologies for public and industrial innovation

- 14.3.6 ITALY

- 14.3.6.1 Accelerating semantic integration for industry 4.0 and research innovation

- 14.3.7 SPAIN

- 14.3.7.1 Expanding semantic web adoption for cultural heritage and industrial efficiency

- 14.3.8 NORDICS

- 14.3.8.1 Driving sustainable operations and research excellence through semantic frameworks

- 14.3.9 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: SEMANTIC WEB MARKET DRIVERS

- 14.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 14.4.2.1 Driving smart city and industrial innovation through semantic web adoption

- 14.4.3 INDIA

- 14.4.3.1 Accelerating digital governance and citizen service efficiency through semantic integration

- 14.4.4 JAPAN

- 14.4.4.1 Enhancing industrial innovation and research collaboration through knowledge graph adoption

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Driving smart healthcare and transport optimization through semantic frameworks

- 14.4.6 AUSTRALIA & NEW ZEALAND

- 14.4.6.1 Leveraging cloud-native platforms for scalable, low-latency processing

- 14.4.7 ASEAN

- 14.4.7.1 Leveraging cloud-native platforms for scalable, low-latency processing

- 14.4.8 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: SEMANTIC WEB MARKET DRIVERS

- 14.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 14.5.3 SAUDI ARABIA

- 14.5.3.1 Building semantic foundations for Vision 2030 and data sovereignty

- 14.5.4 UAE

- 14.5.4.1 Advancing data interoperability and AI-enabled governance through linked knowledge infrastructure

- 14.5.5 SOUTH AFRICA

- 14.5.5.1 Driving transformation and data interoperability through semantic integration frameworks

- 14.5.6 TURKEY

- 14.5.6.1 Accelerating digital governance and Industry 4.0 through semantic data integration

- 14.5.7 QATAR

- 14.5.7.1 Leveraging knowledge graphs and semantic frameworks for data-driven governance

- 14.5.8 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: SEMANTIC WEB MARKET DRIVERS

- 14.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 14.6.3 BRAZIL

- 14.6.3.1 Driving data integration and insight generation across government and research

- 14.6.4 MEXICO

- 14.6.4.1 Accelerating interoperable data platforms to enable AI-driven insights across sectors

- 14.6.5 ARGENTINA

- 14.6.5.1 Leveraging interoperable data frameworks to accelerate AI-driven decision-making

- 14.6.6 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 STRATEGIES ADOPTED BY KEY PLAYERS, 2020-2025

- 15.3 REVENUE ANALYSIS, 2020-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.4.1 MARKET RANKING ANALYSIS, 2024

- 15.5 PRODUCT COMPARATIVE ANALYSIS

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS, BY ONTOLOGY MANAGEMENT TOOL

- 15.5.1.1 IBM (IBM Watson Discovery)

- 15.5.1.2 AWS (Amazon Neptune)

- 15.5.1.3 TopQuadrant (TopBraid EDG)

- 15.5.1.4 Franz Inc (AllegroGraph)

- 15.5.1.5 Metaphacts (Metaphactory)

- 15.5.2 PRODUCT COMPARATIVE ANALYSIS, BY KNOWLEDGE GRAPH PLATFORM

- 15.5.2.1 SAP (SAP HANA Cloud Knowledge Graph)

- 15.5.2.2 Microsoft (Azure Cosmos DB)

- 15.5.2.3 Oracle (RDF Semantic Graph)

- 15.5.2.4 Altair (Siemens) (Altair Graph Studio)

- 15.5.2.5 eccenca (Corporate Memory)

- 15.5.3 PRODUCT COMPARATIVE ANALYSIS, BY SEMANTIC ANNOTATION TOOL

- 15.5.3.1 Progress Software (Progress Semaphore)

- 15.5.3.2 OpenLink Software (Virtuoso Universal Server)

- 15.5.3.3 Synaptica (Synaptica Graphite)

- 15.5.3.4 Oxford Semantic Technologies (RDFox)

- 15.5.3.5 Franz Inc (AllegroGraph)

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS, BY ONTOLOGY MANAGEMENT TOOL

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.6.5.1 Company footprint

- 15.6.5.2 Regional footprint

- 15.6.5.3 Offering footprint

- 15.6.5.4 Technology footprint

- 15.6.5.5 Application footprint

- 15.6.5.6 Vertical footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS

- 16.2.1 IBM

- 16.2.1.1 Business overview

- 16.2.1.2 Products/Solutions/Services offered

- 16.2.1.3 Recent developments

- 16.2.1.3.1 Product launches and enhancements

- 16.2.1.3.2 Deals

- 16.2.1.4 MnM view

- 16.2.1.4.1 Key strengths

- 16.2.1.4.2 Strategic choices

- 16.2.1.4.3 Weaknesses and competitive threats

- 16.2.2 AMAZON WEB SERVICES (AWS)

- 16.2.2.1 Business overview

- 16.2.2.2 Products/Solutions/Services offered

- 16.2.2.3 Recent developments

- 16.2.2.3.1 Product launches and enhancements

- 16.2.2.3.2 Deals

- 16.2.2.4 MnM view

- 16.2.2.4.1 Key strengths

- 16.2.2.4.2 Strategic choices

- 16.2.2.4.3 Weaknesses and competitive threats

- 16.2.3 ORACLE

- 16.2.3.1 Business overview

- 16.2.3.2 Products/Solutions/Services offered

- 16.2.3.3 Recent developments

- 16.2.3.3.1 Product launches and enhancements

- 16.2.3.4 MnM view

- 16.2.3.4.1 Key strengths

- 16.2.3.4.2 Strategic choices

- 16.2.3.4.3 Weaknesses and competitive threats

- 16.2.4 MICROSOFT

- 16.2.4.1 Business overview

- 16.2.4.2 Products/Solutions/Services offered

- 16.2.4.3 Recent developments

- 16.2.4.3.1 Product launches and enhancements

- 16.2.4.3.2 Deals

- 16.2.4.4 MnM view

- 16.2.4.4.1 Key strengths

- 16.2.4.4.2 Strategic choices

- 16.2.4.4.3 Weaknesses and competitive threats

- 16.2.5 SAP

- 16.2.5.1 Business overview

- 16.2.5.2 Products/Solutions/Services offered

- 16.2.5.3 Recent developments

- 16.2.5.3.1 Product launches and enhancements

- 16.2.5.3.2 Deals

- 16.2.5.4 MnM view

- 16.2.5.4.1 Key strengths

- 16.2.5.4.2 Strategic choices

- 16.2.5.4.3 Weaknesses and competitive threats

- 16.2.6 DASSAULT SYSTEMES

- 16.2.6.1 Business overview

- 16.2.6.2 Products/Solutions/Services offered

- 16.2.6.3 Recent developments

- 16.2.6.3.1 Product launches and enhancements

- 16.2.6.4 MnM view

- 16.2.6.4.1 Key strengths

- 16.2.6.4.2 Strategic choices

- 16.2.6.4.3 Weaknesses and competitive threats

- 16.2.7 ALTAIR (SIEMENS)

- 16.2.7.1 Business overview

- 16.2.7.2 Products/Solutions/Services offered

- 16.2.7.3 Recent developments

- 16.2.7.3.1 Product launches and enhancements

- 16.2.8 PROGRESS SOFTWARE

- 16.2.8.1 Business overview

- 16.2.8.2 Products/Solutions/Services offered

- 16.2.8.3 Recent developments

- 16.2.8.3.1 Product launches and enhancements

- 16.2.8.3.2 Deals

- 16.2.9 HUAWEI

- 16.2.9.1 Business overview

- 16.2.9.2 Products/Solutions/Services offered

- 16.2.9.3 Recent developments

- 16.2.9.3.1 Product launches and enhancements

- 16.2.10 OPENTEXT

- 16.2.10.1 Business overview

- 16.2.10.2 Products/Solutions/Services offered

- 16.2.10.3 Recent developments

- 16.2.10.3.1 Product launches and enhancements

- 16.2.11 INFORMATICA

- 16.2.11.1 Business overview

- 16.2.11.2 Products/Solutions/Services offered

- 16.2.11.3 Recent developments

- 16.2.11.3.1 Product launches and enhancements

- 16.2.11.3.2 Deals

- 16.2.12 YEXT

- 16.2.13 GLEAN

- 16.2.14 ZIFO RND SOLUTIONS

- 16.2.15 COLLIBRA

- 16.2.16 TIBCO

- 16.2.17 QLIK

- 16.2.18 SAS INSTITUTE

- 16.2.1 IBM

- 16.3 STARTUPS/SMES

- 16.3.1 NEO4J

- 16.3.2 CHAINALYSIS

- 16.3.3 PENTAHO (HITACHI VANTARA)

- 16.3.4 FLUREE

- 16.3.5 SCIBITE (ELSEVIER)

- 16.3.6 DATA GRAPHS

- 16.3.7 NOETICA AI

- 16.3.8 VEEZOO

- 16.3.9 DATAVID

- 16.3.10 WRITER

- 16.3.11 ALATION

- 16.3.12 STARDOG

- 16.3.13 ONTOTEXT (GRAPHWISE)

- 16.3.14 SEMANTIC WEB COMPANY (GRAPHWISE)

- 16.3.15 METAPHACTS

- 16.3.16 FRANZ INC.

- 16.3.17 ECCENCA

- 16.3.18 OPENLINK SOFTWARE

- 16.3.19 TOPQUADRANT

- 16.3.20 SYNAPTICA (SQUIRRO)

- 16.3.21 TIMBR

- 16.3.22 OXFORD SEMANTIC TECHNOLOGIES (SAMSUNG)

- 16.3.23 BIOBOX ANALYTICS

17 ADJACENT AND RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 KNOWLEDGE GRAPH MARKET - GLOBAL FORECAST TO 2030

- 17.2.1 MARKET DEFINITION

- 17.2.2 MARKET OVERVIEW

- 17.2.2.1 Knowledge Graph Market, By Offering

- 17.2.2.2 Knowledge Graph Market, By Application

- 17.2.2.3 Knowledge Graph Market, By Vertical

- 17.2.2.4 Knowledge Graph Market, By Region

- 17.3 GRAPH DATABASE MARKET - GLOBAL FORECAST TO 2030

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.3.2.1 Graph Database Market, By Offering

- 17.3.2.2 Graph Database Market, By Model Type

- 17.3.2.3 Graph Database Market, By Application

- 17.3.2.4 Graph Database Market, By Vertical

- 17.3.2.5 Graph Database Market, By Region

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS