|

시장보고서

상품코드

1876461

적외선 검출기 시장 : 유형별, 기술별, 파장별, 용도별, 지역별 예측(-2030년)Infrared Detector Market by Type (Thermal Detector, Photodetector ),Technology, Wavelength, Application and Region - Global Forecast to 2030 |

||||||

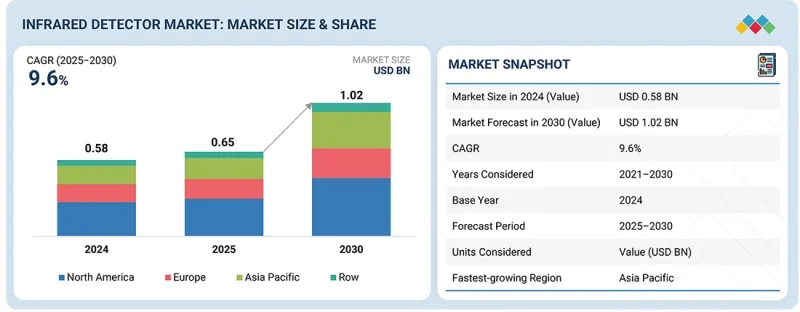

세계의 적외선 검출기 시장 규모는 2025년 6억 5,000만 달러에서 2030년까지 10억 2,000만 달러에 이를 것으로 예상되며, 예측 기간에 CAGR로 9.6%를 나타낼 것으로 전망됩니다.

안전 및 보안 수요 증가, 방위 근대화, 스마트 시티 구상, 자동차용 ADAS(첨단 운전자 보조 시스템), 의료용 서모그래피, 스마트 홈 디바이스에 있어서 검출기 활용의 확대가 시장의 성장을 가속하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 10억 달러 |

| 부문 | 유형, 기술, 용도, 산업, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양 및 기타 지역 |

게다가 비냉각식 검출기 기술의 진보, 소형화, IoT/AI와의 통합으로 적외선 센서의 저렴함과 확장성이 높아져 산업용도와 소비자용도에 있어서 채용이 더욱 가속화되고 있습니다.

"비산업/기관/서비스 지향(직접 소비) 부문은 예측 기간 동안 산업/제조(프로세스/제품에 B2B 통합) 부문보다 높은 CAGR로 성장할 것으로 예측됩니다."

산업별로는 비산업/제조 부문이 예측 기간에 산업/제조 부문을 초과하는 CAGR을 나타낼 것으로 예측됩니다. 이 예측된 부문 성장은 주택 및 상업용 건물, 의료시설 및 과학 연구 응용 분야에서 검출기 채택 증가에 의해 지원됩니다. 또한 스마트 홈 및 빌딩 자동화에 대한 수요 증가가 적외선 센서의 모션 감지, 방화 및 에너지 관리 시스템에 통합을 촉진하고 있습니다. 의료 부문에서는 진단 정확성과 환자의 안전성 향상에 기여하기 때문에 비접촉 서모그래피, 환자 모니터링 및 생체 의료 영상에서 검출기 사용이 증가하고 있습니다. 게다가 연구기관에서는 분광법, 천문학, 선진재료 연구에 있어서 적외선 검출기가 채용되어, 종래의 산업용도를 넘은 이용이 확대되고 있습니다. 이러한 요인 외에도 공공안전과 학술연구개발에 대한 투자가 증가하여 비산업/제조 부문이 예측 기간에 상당한 성장을 이룰 전망입니다.

"서모파일 부문이 예측 기간에 적외선 검출기 시장에서 큰 점유율을 차지할 전망입니다."

열 검출기 유형별로 서모 파일 부문이 예측 기간에 가장 큰 점유율을 차지할 것으로 예측됩니다. 이러한 예측된 부문 성장은 써모파일 검출기의 저비용, 내구성, 냉각이 필요 없는 작동 능력으로 인한 것으로 여겨지며, 이는 가전, 스마트 디바이스, 산업 모니터링 시스템에 통합하기에 이상적이기 때문입니다. 게다가 컴팩트한 사이즈와 높은 에너지 효율로부터 온도 측정, 스마트 가전, HVAC 시스템에의 채용이 진행되고 있습니다. 또한 신뢰성과 비접촉 측정 능력으로 가스 검출, 환경 모니터링, 의료용 온도계에 서모 파일 검출기의 채용이 증가하고 있습니다. 자동차의 차내 모니터링과 휴대용 의료기기에서 저렴한 적외선 솔루션에 대한 수요 증가도 그 보급을 더욱 뒷받침하고 있습니다. 이러한 장점을 통해 서모파일은 높은 범용성을 발휘하여 대중 시장에서 전문용도까지 폭넓게 선택되는 것을 확실히 하고 있습니다.

"캐나다가 2025-2030년에 적외선 검출기 시장에서 가장 높은 성장률을 나타낼 것으로 예측됩니다."

캐나다의 강력한 시장 성장은 방위 근대화, 국경 경비, 공공 안전 시책에 대한 투자 증가로 인한 것이며, 이들은 감시·이미징 용도에 있어서 적외선 검출기의 채용을 촉진하고 있습니다. 이 나라의 스마트 인프라와 빌딩 자동화에 대한 주목의 확대도 수요에 기여하고 있으며, 화재 검출, 에너지 관리, 점유율 모니터링 시스템에 적외선 센서의 통합이 진행되고 있습니다. 또한 의료 진단, 환경 모니터링, 산업 자동화에 있어서 적외선 이미징의 채용 확대가 그 응용 범위를 넓혀가고 있습니다. 지원 정부 프로그램과 캐나다 연구 기관과 세계 제조업체 간의 파트너십도 기술 채택을 가속화하고 캐나다를 가장 성장하는 시장 중 하나로 삼고 있습니다.

이 보고서는 세계의 적외선 검출기 시장에 대한 조사 분석을 통해 주요 성장 촉진요인 및 억제요인, 경쟁 구도, 미래 동향 등의 정보를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

- 적외선 검출기 시장에서 기업에게 매력적인 기회

- 적외선 검출기 시장 : 열 검출기 유형별

- 적외선 검출기 시장 : 지역별

- 적외선 검출기 시장 : 광 검출기 유형별

- 보안 및 감시 : 적외선 검출기 시장, 기술별

제5장 시장 개요

- 서론

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 고객사업에 영향을 주는 동향/혼란

- 가격 설정 분석

- 열 검출기 유형의 평균 판매 가격 : 주요 기업별

- 열 검출기 유형의 평균 판매 가격 동향(2021-2024년)

- 열 검출기 유형의 가격대 : 지역별

- 밸류체인 분석

- 생태계 분석

- 기술 분석

- 주요 기술

- 보완 기술

- 인접 기술

- 특허 분석

- 무역 분석

- 수입 데이터

- 수출 데이터

- 주요 컨퍼런스 및 이벤트(2025-2026년)

- 사례 연구 분석

- INFRATEC GMBH(독일)

- MURATA MANUFACTURING CO., LTD.(일본)

- TELEDYNE FLIR LLC(미국)

- MURATA MANUFACTURING CO., LTD.(일본)

- 투자 및 자금조달 시나리오

- 규제 상황

- 규제기관, 정부기관, 기타 조직

- 표준

- Porter's Five Forces 분석

- 주요 이해관계자와 구매 기준

- 적외선 검출기 시장에 대한 생성형 AI/AI의 영향

- 적외선 검출기 시장에 대한 미국 관세의 영향(2025년)

- 서론

- 주요 관세율

- 가격의 영향 분석

- 국가/지역에 미치는 영향

- 용도에 대한 영향

제6장 적외선 검출기 시장 : 용도별

- 서론

- 사람 및 동작 감지

- 온도 측정

- 보안 및 감시

- 가스 및 화재 감지

- 분광학 및 생체의학 영상

- 기타 용도

제7장 적외선 검출기 시장 : 기술별

- 서론

- 냉각식

- 비냉각식

제8장 적외선 검출기 시장 : 유형별

- 서론

- 열 검출기

- 열전소자

- 열전소자

- 마이크로볼로미터

- 광검출기

- 수은 카드뮴 텔루라이드

- 인듐 갈륨 비소

- 기타 광검출기

제9장 적외선 검출기 시장 : 업계별

- 서론

- 산업

- 비산업

- 군사 및 방위

- 주택 및 상업

- 의료

- 과학연구

제10장 적외선 검출기 시장 : 파장별

- 서론

- NIR

- SWIR

- MWIR

- LWIR

제11장 적외선 검출기 시장 : 지역별

- 서론

- 북미

- 북미의 거시경제 전망

- 미국

- 캐나다

- 멕시코

- 유럽

- 유럽의 거시경제 전망

- 독일

- 영국

- 프랑스

- 이탈리아

- 네덜란드

- 폴란드

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 아시아태평양의 거시경제 전망

- 일본

- 중국

- 대만

- 한국

- 인도

- 호주

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 기타 아시아태평양

- 기타 지역

- 기타 지역의 거시경제 전망

- 중동

- 아프리카

- 남미

제12장 경쟁 구도

- 개요

- 주요 참가 기업의 전략/강점(2020-2025년)

- 시장 점유율 분석(2024년)

- 수익 분석(2021-2024년)

- 기업평가와 재무지표(2025년)

- 브랜드 비교

- 기업평가 매트릭스 : 주요 기업(2024년)

- 기업평가 매트릭스 : 스타트업/중소기업(2024년)

- 경쟁 시나리오

제13장 기업 프로파일

- 주요 기업

- TELEDYNE TECHNOLOGIES INCORPORATED

- TEXAS INSTRUMENTS INCORPORATED

- EXCELITAS TECHNOLOGIES CORP.

- MURATA MANUFACTURING CO., LTD.

- LYNRED

- HONEYWELL INTERNATIONAL INC.

- HAMAMATSU PHOTONICS KK

- NIPPON CERAMIC CO., LTD.

- OMRON CORPORATION

- TE CONNECTIVITY

- 기타 기업

- INFRATEC GMBH

- LASER COMPONENTS

- DRAGERWERK AG & CO. KGAA

- VIGO PHOTONICS SA

- FAGUS-GRECON

- THORLABS, INC.

- SEMITEC CORPORATION

- IRNOVA AB

- GLOBAL SENSOR TECHNOLOGY CO., LTD.

- DIAS INFRARED GMBH

- DETECTOR ELECTRONICS, LLC.

- INFRARED MATERIALS, INC.

- IR-TEC INTERNATIONAL LTD.

- AMPHENOL ADVANCED SENSORS

- INFRARED ASSOCIATES, INC.

- 최종 장비 제조업체

- RTX

- TELEDYNE FLIR LLC

- LEONARDO ELECTRONICS US INC.

- BOSCH LIMITED

- ELBIT SYSTEMS LTD.

제14장 부록

KTH 25.11.28The global infrared detector market is projected to grow from USD 0.65 billion in 2025 to USD 1.02 billion by 2030, at a CAGR of 9.6% during the forecast period. Rising safety and security needs, defense modernization, smart city initiatives, and the increasing use of detectors in automotive ADAS, healthcare thermography, and smart home devices fuel the market's growth.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, Technology, Application, Vertical and Region |

| Regions covered | North America, Europe, APAC, RoW |

Additionally, advancements in uncooled detector technology, miniaturization, and IoT/AI integration are making infrared sensors more affordable and scalable, further accelerating their adoption across industrial and consumer applications.

"The non-industrial/institutional/service-oriented (direct consumption) segment is projected to grow at a higher CAGR than the industrial/manufacturing (B2B integration into processes/products) segment during the forecast period."

By vertical, the non-industrial/manufacturing segment is projected to achieve a higher CAGR than the industrial/manufacturing segment during the forecast period. This projected segment growth is supported by the increasing adoption of detectors in residential & commercial buildings, healthcare facilities, and scientific research applications. Additionally, the rising demand for smart homes and building automation is driving the integration of infrared sensors in motion detection, fire safety, and energy management systems. In the healthcare sector, detectors are increasingly used for non-contact thermography, patient monitoring, and biomedical imaging, as they help improve diagnostic accuracy and patient safety. Moreover, research institutions are adopting infrared detectors in spectroscopy, astronomy, and advanced material studies, expanding their use beyond traditional industrial applications. These factors, combined with growing investments in public safety and academic R&D initiatives, position the non-industrial/manufacturing segment to achieve significant growth during the forecast period.

"The thermopile segment is projected to account for a significant share in the infrared detector market during the forecast period."

The thermopile segment is projected to account for the largest share during the forecast period by thermal detector type. This projected segment growth can be attributed to the low cost of thermopile detectors, their durability, and their ability to operate without cooling, making them ideal for integration into consumer electronics, smart devices, and industrial monitoring systems. Additionally, their compact size and energy efficiency are driving their adoption in temperature measurement, smart appliances, and HVAC systems. Moreover, thermopile detectors are being increasingly deployed in gas detection, environmental monitoring, and medical thermometers, owing to their reliability and non-contact measurement capabilities. This growing demand for affordable infrared solutions in automotive cabin monitoring and portable medical devices further boosts their uptake. These advantages make thermopiles highly versatile and ensure they remain preferred across mass-market and specialized applications.

"Canada is projected to register the highest growth in the infrared detector market between 2025 and 2030."

Canada is projected to register the highest CAGR in the infrared detector market during the forecast period. Canada's strong market growth is driven by increasing investments in defense modernization, border security, and public safety initiatives, which are boosting the adoption of infrared detectors in surveillance and imaging applications. The country's expanding focus on smart infrastructure and building automation further contributes to demand, integrating infrared sensors into fire detection, energy management, and occupancy monitoring systems. Additionally, the growing adoption of infrared imaging in medical diagnostics, environmental monitoring, and industrial automation is widening the scope of applications. Supportive government programs and partnerships between Canadian research institutions and global manufacturers are also accelerating technological adoption and positioning Canada as one of the fastest-growing markets.

Extensive primary interviews were conducted with key industry experts in the infrared detector market space to determine and verify the market size for various segments and subsegments gathered through secondary research.

The breakdown of primary participants for the report is given below:

- By Company Type: Tier 1 - 20%, Tier 2 - 45%, Tier 3 - 35%

- By Designation: C-level Executives - 35%, Directors - 25%, Others - 40%

- By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, RoW - 10%

The infrared detector market is dominated by a few globally established players, such as Teledyne Technologies (US), Texas Instruments Incorporated (US), Excelitas Technologies Corp. (US), Murata Manufacturing Co., Ltd. (Japan), and Lynred (France). The study includes an in-depth competitive analysis of key players in the infrared detector market and their company profiles, recent developments, and key market strategies.

Study Coverage:

The report segments the infrared detector market and forecasts its size by type (Thermal detector, photodetector), technology (cooled, uncooled), wavelength (Near-Infrared (NIR), short-wave infrared (SWIR), mid-wave infrared (MWIR), long-wave infrared (LWIR), vertical (industrial, non-industrial), application (People & motion sensing, temperature measurement, security & surveillance, gas & fire detection, spectroscopy & biomedical imaging, and other applications).

The report discusses the market's drivers, restraints, opportunities, and challenges, and provides a detailed view of the market across North America, Europe, Asia Pacific, and the Rest of the World. It includes a supply chain analysis of the key players and their competitive analysis in the infrared detector market ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (Demand acceleration for thermal imaging across mission-critical defense, automotive, industrial, and healthcare ecosystems; operational excellence fueled by cost-efficient uncooled infrared modules across industrial and smart manufacturing sectors), restraints (High cost & complexity of cooled detectors; regulatory hurdles and complexities, including export controls in defense and aerospace sectors), opportunities (Adoption of SWIR/NIR modules fueling precision inspection and automotive safety innovation, material innovation with quantum dots and CMOS-compatible IR redefining cost economics), challenges (Long-term performance risks from thermal instability impacting mission-critical sensing)

- Product Development/Innovation: Detailed insights into upcoming technologies, research and development activities, and product launches in the infrared detector market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the infrared detector market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players, such as Teledyne Technologies (US), Texas Instruments Incorporated (US), Excelitas Technologies Corp. (US), Murata Manufacturing Co., Ltd. (Japan), and Lynred (France), in the infrared detector market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 INTRODUCTION

- 2.2 RESEARCH DATA

- 2.2.1 SECONDARY DATA

- 2.2.1.1 List of major secondary sources

- 2.2.1.2 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 List of primary interview participants

- 2.2.2.2 Breakdown of primaries

- 2.2.2.3 Key data from primary sources

- 2.2.2.4 Key industry insights

- 2.2.1 SECONDARY DATA

- 2.3 FACTOR ANALYSIS

- 2.3.1 SUPPLY-SIDE ANALYSIS

- 2.3.2 DEMAND-SIDE ANALYSIS

- 2.4 MARKET SIZE ESTIMATION METHODOLOGY

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 2.4.2 TOP-DOWN APPROACH

- 2.4.2.1 Approach to arrive at market size using top-down approach (supply side)

- 2.4.1 BOTTOM-UP APPROACH

- 2.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

- 2.8 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INFRARED DETECTOR MARKET

- 4.2 INFRARED DETECTOR MARKET FOR THERMAL DETECTORS, BY TYPE

- 4.3 INFRARED DETECTOR MARKET, BY REGION

- 4.4 INFRARED DETECTOR MARKET FOR PHOTODETECTORS, BY TYPE

- 4.5 SECURITY & SURVEILLANCE: INFRARED DETECTOR MARKET, BY TECHNOLOGY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Demand across mission-critical defense, automotive, industrial, and healthcare ecosystems

- 5.2.1.2 Operational excellence fueled by cost-efficient uncooled infrared modules across industrial and smart manufacturing sectors

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost & complexity of cooled detectors

- 5.2.2.2 Regulatory hurdles and complexities, including export controls in defense and aerospace

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Adoption of SWIR/NIR modules fueling precision inspection and automotive safety innovation

- 5.2.3.2 Materials innovation with quantum dots and CMOS-compatible IR redefining cost economics

- 5.2.4 CHALLENGES

- 5.2.4.1 Long-term performance risks from thermal instability

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF THERMAL DETECTOR TYPES, BY KEY PLAYER

- 5.4.2 AVERAGE SELLING PRICE TREND OF THERMAL DETECTOR TYPES, 2021-2024

- 5.4.3 PRICING RANGE OF THERMAL DETECTOR TYPES, BY REGION

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Quantum dot infrared photodetectors (QDIP)

- 5.7.1.2 Indium antimonide (InSb) detectors

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Sensor fusion (IR + visible/radar/LiDAR)

- 5.7.2.2 Edge AI/ML analytics

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Automotive night vision

- 5.7.3.2 Environmental monitoring (OGI for Methane/CO2)

- 5.7.3.3 Industrial predictive maintenance

- 5.7.1 KEY TECHNOLOGIES

- 5.8 PATENT ANALYSIS

- 5.9 TRADE ANALYSIS

- 5.9.1 IMPORT DATA

- 5.9.2 EXPORT DATA

- 5.10 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 INFRATEC GMBH (GERMANY)

- 5.11.2 MURATA MANUFACTURING CO., LTD. (JAPAN)

- 5.11.3 TELEDYNE FLIR LLC (US)

- 5.11.4 MURATA MANUFACTURING CO., LTD. (JAPAN)

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.2 STANDARDS

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 IMPACT OF GEN AI/AI ON INFRARED DETECTOR MARKET

- 5.16.1 INTRODUCTION

- 5.17 IMPACT OF 2025 US TARIFF ON INFRARED DETECTOR MARKET

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 IMPACT ON COUNTRIES/REGIONS

- 5.17.4.1 US

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON APPLICATIONS

6 INFRARED DETECTOR MARKET, APPLICATION

- 6.1 INTRODUCTION

- 6.2 PEOPLE & MOTION SENSING

- 6.2.1 RISING ADOPTION DUE TO DEMAND FOR SMART SECURITY AND AUTOMATION SOLUTIONS

- 6.3 TEMPERATURE MEASUREMENT

- 6.3.1 GROWING DEMAND IN INDUSTRIAL AND MEDICAL MONITORING APPLICATIONS TO BOOST GROWTH

- 6.4 SECURITY & SURVEILLANCE

- 6.4.1 INCREASING DEPLOYMENT FOR RELIABLE ALL-WEATHER MONITORING SYSTEMS TO DRIVE SEGMENT

- 6.5 GAS & FIRE DETECTION

- 6.5.1 RISING IMPLEMENTATION ENHANCES DEMAND FOR SAFETY AND HAZARD PREVENTION SOLUTIONS

- 6.6 SPECTROSCOPY & BIOMEDICAL IMAGING

- 6.6.1 GROWING APPLICATION FOR NON-INVASIVE DIAGNOSTICS AND ANALYTICAL TOOLS TO DRIVE SEGMENT

- 6.7 OTHER APPLICATIONS

- 6.7.1 INCREASING NEED FOR ENERGY EFFICIENCY AND INTELLIGENT BUILDING MANAGEMENT TO BOOST DEMAND

7 INFRARED DETECTOR MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 COOLED

- 7.2.1 GROWING USE OF INFRARED IMAGING IN DEFENSE TO BOOST DEMAND

- 7.3 UNCOOLED

- 7.3.1 RISING INTEGRATION OF UNCOOLED DETECTORS IN AUTOMOTIVE SYSTEMS TO PROPEL DEMAND

8 INFRARED DETECTOR MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 THERMAL DETECTORS

- 8.2.1 GROWING USE TO PROPEL SMART INFRARED MONITORING SOLUTIONS

- 8.3 PYROELECTRIC

- 8.3.1 RISING DEMAND IN PEOPLE & MOTION SENSING

- 8.4 THERMOPILE

- 8.4.1 NON-CONTACT TEMPERATURE MEASUREMENT, GAS ANALYSIS, AND THERMAL IMAGING - KEY APPLICATIONS

- 8.5 MICROBOLOMETER

- 8.5.1 RISING DEMAND IN MEDICAL IMAGING, ENVIRONMENTAL MONITORING, AND INDUSTRIAL INSPECTION

- 8.6 PHOTODETECTORS

- 8.6.1 RISING DEPLOYMENT TO BOOST SECURITY, SURVEILLANCE, AND DEFENSE SYSTEMS

- 8.7 MERCURY CADMIUM TELLURIDE

- 8.7.1 HIGH DEMAND IN TEMPERATURE & MEASUREMENT APPLICATIONS

- 8.8 INDIUM GALLIUM ARSENIDE

- 8.8.1 INCREASED DEMAND IN IMAGING APPLICATIONS ATTRIBUTED TO LOW NOISE FEATURE

- 8.9 OTHER PHOTODETECTORS

9 INFRARED DETECTOR MARKET, VERTICAL

- 9.1 INTRODUCTION

- 9.1.1 INDUSTRIAL

- 9.1.1.1 Automotive

- 9.1.1.1.1 Growing use in automotive safety and assistance to enhance vehicle performance

- 9.1.1.2 Aerospace

- 9.1.1.2.1 Rising deployment for situational awareness and monitoring to boost demand

- 9.1.1.3 Semiconductor & electronics

- 9.1.1.3.1 Growing integration in semiconductor and electronics processes to enhance device reliability

- 9.1.1.4 Oil & gas

- 9.1.1.4.1 Rising adoption in oil & gas operations to enhance safety and process efficiency

- 9.1.1.5 Other industrial verticals

- 9.1.1.1 Automotive

- 9.1.2 NON-INDUSTRIAL

- 9.1.3 MILITARY & DEFENSE

- 9.1.3.1 Rising implementation to enhance surveillance and targeting capabilities to boost demand

- 9.1.4 RESIDENTIAL & COMMERCIAL

- 9.1.4.1 Growing use for energy efficiency and security to propel demand

- 9.1.5 MEDICAL

- 9.1.5.1 Rising application in patient monitoring and diagnostics to drive segment

- 9.1.6 SCIENTIFIC RESEARCH

- 9.1.6.1 Enhancement of observational and analytical capabilities to drive growth

- 9.1.1 INDUSTRIAL

10 INFRARED DETECTOR MARKET, WAVELENGTH

- 10.1 INTRODUCTION

- 10.2 NIR

- 10.2.1 GROWING INDUSTRIAL AUTOMATION REQUIREMENTS TO DRIVE NIR-BASED MONITORING DEMAND

- 10.3 SWIR

- 10.3.1 GROWING INVESTMENT IN ADVANCED SWIR TECHNOLOGIES PROPEL AUTOMOTIVE AND ROBOTICS APPLICATIONS

- 10.4 MWIR

- 10.4.1 WIDE-SCALE APPLICATIONS IN SECURITY & SURVEILLANCE TO BOOST SEGMENT

- 10.5 LWIR

- 10.5.1 SURGING DEMAND FOR LWIR DETECTORS IN MILITARY & DEFENSE VERTICAL

- 10.5.1.1 Key properties of LWIR

- 10.5.1 SURGING DEMAND FOR LWIR DETECTORS IN MILITARY & DEFENSE VERTICAL

11 INFRARED DETECTOR MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 US

- 11.2.2.1 Growing defense and industrial integration propelling infrared detector innovation

- 11.2.3 CANADA

- 11.2.3.1 Rising focus on environmental and industrial safety to boost adoption of infrared detectors

- 11.2.4 MEXICO

- 11.2.4.1 Expanding security and industrial applications to drive infrared detector demand

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 GERMANY

- 11.3.2.1 Growing industrial and automotive innovation support infrared detector deployment

- 11.3.3 UK

- 11.3.3.1 Expanding defense and industrial modernization to boost infrared detector adoption

- 11.3.4 FRANCE

- 11.3.4.1 Rising defense and aerospace programs enhance infrared detector development

- 11.3.5 ITALY

- 11.3.5.1 Growing aerospace and energy sector needs to drive infrared detector applications

- 11.3.6 NETHERLANDS

- 11.3.6.1 Rising focus on high-tech and smart infrastructure support infrared detector use

- 11.3.7 POLAND

- 11.3.7.1 Increasing defense modernization and industrial safety boosting infrared detector demand

- 11.3.8 NORDIC COUNTRIES

- 11.3.8.1 Growing sustainability and defense priorities to enable infrared detector innovation

- 11.3.9 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 JAPAN

- 11.4.2.1 Growing automotive and robotics innovation to propel infrared detector advancements

- 11.4.3 CHINA

- 11.4.3.1 Expanding defense, smart cities, and consumer electronics to drive large-scale infrared detector adoption

- 11.4.4 TAIWAN

- 11.4.4.1 Growing semiconductor ecosystem and defense priorities to support infrared detector relevance

- 11.4.5 SOUTH KOREA

- 11.4.5.1 Expanding defense and electronics innovation to drive infrared detector integration

- 11.4.6 INDIA

- 11.4.6.1 Rising defense and industrial modernization to propel infrared detector demand

- 11.4.7 AUSTRALIA

- 11.4.7.1 Growing reliance on IR detectors for defense and environmental monitoring to drive niche applications

- 11.4.8 INDONESIA

- 11.4.8.1 Need for IR sensors in electronics and industrial monitoring to boost adoption across key sectors

- 11.4.9 MALAYSIA

- 11.4.9.1 Expansion of IR detector usage in industrial automation and security propelling electronics sector growth

- 11.4.10 THAILAND

- 11.4.10.1 Growing adoption in industrial and surveillance applications to drive market penetration

- 11.4.11 VIETNAM

- 11.4.11.1 Rising use of IR detectors in consumer electronics and security to drive emerging market growth

- 11.4.12 REST OF ASIA PACIFIC

- 11.5 ROW

- 11.5.1 MACROECONOMIC OUTLOOK FOR ROW

- 11.5.2 MIDDLE EAST

- 11.5.2.1 Bahrain

- 11.5.2.1.1 Growing focus on infrastructure safety to boost infrared detector adoption

- 11.5.2.2 Kuwait

- 11.5.2.2.1 Rising energy and defense priorities to propel infrared detector integration

- 11.5.2.3 Oman

- 11.5.2.3.1 Expanding homeland security and industrial needs to support infrared detector demand

- 11.5.2.4 Qatar

- 11.5.2.4.1 Growing smart city and energy initiatives to boost infrared detector deployment

- 11.5.2.5 Saudi Arabia

- 11.5.2.5.1 Rising defense and oil sector modernization to propel infrared detector usage

- 11.5.2.6 UAE

- 11.5.2.6.1 Expanding smart infrastructure and defense priorities to drive adoption

- 11.5.2.7 Rest of Middle East

- 11.5.2.1 Bahrain

- 11.5.3 AFRICA

- 11.5.3.1 South Africa

- 11.5.3.1.1 Rising defense and industrial safety initiatives to propel infrared detector adoption

- 11.5.3.2 Rest of Africa

- 11.5.3.1 South Africa

- 11.5.4 SOUTH AMERICA

- 11.5.4.1 Brazil

- 11.5.4.1.1 Expanding defense, energy, and environmental programs to driving demand

- 11.5.4.2 Argentina

- 11.5.4.2.1 Growing industrial and security modernization to boost market

- 11.5.4.3 Rest of South America

- 11.5.4.1 Brazil

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2025

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 REVENUE ANALYSIS, 2021-2024

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS, 2025

- 12.6 BRAND COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Type footprint

- 12.7.5.4 Application footprint

- 12.7.5.5 Wavelength footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 TELEDYNE TECHNOLOGIES INCORPORATED

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 TEXAS INSTRUMENTS INCORPORATED

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Services/Solutions offered

- 13.1.2.3 MnM view

- 13.1.2.3.1 Right to win

- 13.1.2.3.2 Strategic choices

- 13.1.2.3.3 Weaknesses & competitive threats

- 13.1.3 EXCELITAS TECHNOLOGIES CORP.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 MURATA MANUFACTURING CO., LTD.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 LYNRED

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 HONEYWELL INTERNATIONAL INC.

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.7 HAMAMATSU PHOTONICS K.K.

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.8 NIPPON CERAMIC CO., LTD.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches

- 13.1.9 OMRON CORPORATION

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.10 TE CONNECTIVITY

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.1 TELEDYNE TECHNOLOGIES INCORPORATED

- 13.2 OTHER PLAYERS

- 13.2.1 INFRATEC GMBH

- 13.2.2 LASER COMPONENTS

- 13.2.3 DRAGERWERK AG & CO. KGAA

- 13.2.4 VIGO PHOTONICS S.A.

- 13.2.5 FAGUS-GRECON

- 13.2.6 THORLABS, INC.

- 13.2.7 SEMITEC CORPORATION

- 13.2.8 IRNOVA AB

- 13.2.9 GLOBAL SENSOR TECHNOLOGY CO., LTD.

- 13.2.10 DIAS INFRARED GMBH

- 13.2.11 DETECTOR ELECTRONICS, LLC.

- 13.2.12 INFRARED MATERIALS, INC.

- 13.2.13 IR-TEC INTERNATIONAL LTD.

- 13.2.14 AMPHENOL ADVANCED SENSORS

- 13.2.15 INFRARED ASSOCIATES, INC.

- 13.3 END-DEVICE MANUFACTURERS

- 13.3.1 RTX

- 13.3.2 TELEDYNE FLIR LLC

- 13.3.3 LEONARDO ELECTRONICS US INC.

- 13.3.4 BOSCH LIMITED

- 13.3.5 ELBIT SYSTEMS LTD.

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 CUSTOMIZATION OPTIONS

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS