|

시장보고서

상품코드

1887992

고온 단열재 시장 : 재질별, 온도 폭별, 최종 이용 산업별, 지역별 - 예측(-2030년)High Temperature Insulation Materials Market by Material Type (Ceramic Fibers, Insulating Firebricks, Calcium Silicate), End-use Industry (Petrochemical, Ceramic, Glass, Iron & Steel, Cement), Temperature Range, and Region - Global Forecast to 2030 |

||||||

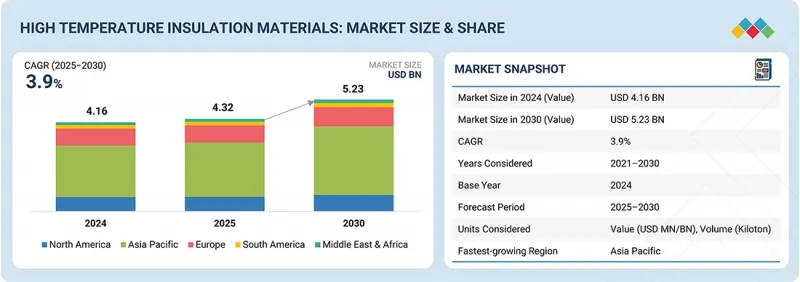

고온 단열재 시장 규모는 예측 기간 동안 CAGR 3.9%로 성장할 전망이며, 2025년 43억 2,000만 달러에서 2030년에는 52억 3,000만 달러에 이를 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러) 및 킬로톤 |

| 부문 | 재질별, 온도 폭별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

고온 단열재는 인도의 에너지 효율국(Bureau of Energy Efficiency) 등 조직에 의한 엄격한 안전 및 에너지 효율 규제와 ASTM International의 재료 규격에 의해 야금, 시멘트, 유리, 석유화학 등의 중공업 분야에서 꾸준히 사용되고 있습니다. 세라믹 섬유 담요, 규산 칼슘 보드, 내화 벽돌 등의 재료는 600°C-1,500°C 이상의 작동 온도 폭에서 치수 안정성, 낮은 열 전도도 및 내구성을 제공하기 위해 제조됩니다. 이들은 산업용 로의 라이닝, 공정 장비의 단열, 고온 덕트 공사, 복잡한 제조 시스템의 열 보호를 지원합니다.

또한 NASA의 평가에 따르면 이러한 재료는 극단적인 복사열 흐름을 견디며 우주 원자력 시스템에서 신뢰할 수 있는 성능을 발휘합니다. 미국 에너지부 가이드라인은 고온 공정에서 산업 에너지 손실을 최대 20%까지 줄이는 역할을 한다고 밝혔습니다.

세라믹 섬유는 탁월한 내열성, 낮은 열전도율, 우수한 에너지 효율로 예측 기간 동안 고온 단열재 시장에서 가장 빠르게 확대되는 재료 카테고리가 될 전망입니다. 이러한 섬유는 1,700℃를 넘는 극한의 고온을 견딜 수 있기 때문에 석유화학처리, 철강 생산, 발전, 고온로 등 다양하며 중요한 용도로 사용되고 있습니다. 경량성 및 시공의 용이성은 효율성을 향상시키는 동시에 전반적인 유지보수 비용 절감에도 기여합니다. 섬유화학의 진보, 생분해성 배합의 개발, 내구성의 한층 더 향상에 의해 안전하고 효율적이고 환경 규제에 적합한 단열 솔루션을 요구하는 산업 분야에서의 용도 범위가 확대되어, 시장의 강력한 성장을 견인하고 있습니다.

예측 기간 동안 시멘트 부문은 고온 단열재 시장에서 가장 빠르게 성장하는 최종 이용 산업이 될 전망입니다. 이것은 세계 건설 활동 증가 및 에너지 효율에 대한 관심 증가가 주요 요인입니다. 시멘트의 제조 공정에서는 1,450℃를 넘는 고온에서의 킬른 조작이 행해져, 열 손실을 저감하고, 연료 효율을 확보해, 내화 벽돌의 수명을 연장하는 고성능 단열재 수요를 견인하고 있습니다. 또한 시멘트 공장의 현대화, 배출 감축을 목적으로 하는 규제, 환경 친화적인 제조 동향은 시장에서 세라믹 섬유, 단열 내화 벽돌, 규산 칼슘 제품의 사용을 촉진하는 주요 요인이 될 전망입니다. 고온 단열재는 운용 비용 절감, 열성능 향상, 탈탄소화 촉진에 중요한 역할을 하여 시멘트 산업의 고온 단열재 시장 전체가 급속한 성장을 이룰 것으로 예측됩니다.

아시아태평양은 고온 단열재 시장에서 가장 빠른 성장이 예상됩니다. 급속한 산업화 및 시멘트, 석유화학, 금속, 유리 산업의 대규모 확대가 이 지역의 급성장을 가져오는 주요 요인입니다. 보다 엄격한 에너지 효율 기준 시행, 인프라 투자 증가, 열 손실 및 CO2 배출량 저감을 위한 고성능 단열재에 대한 수요 증가가 채용을 뒷받침하고 있습니다. 게다가 지속적인 생산능력 확대 및 경쟁력 있는 제조 기반 등 성장 전망이 밝은 배경에는 다른 요인도 존재합니다.

대상 기업 : 본 보고서에서는 3M(US), Morgan Advanced Materials plc(UK), RHI Magnesita GmbH(Austria), Luyang Energy-saving Materials(China), Etex Group(Belgium), Calderys(France), Alkegen(US), SHINAGAWA REFRA(Japan), IBIDEN NUTEC(Mexico)를 다루고 있습니다.

이 보고서는 고온 단열재 시장에서 이러한 주요 기업에 대해 기업 프로파일, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 제공합니다.

조사 범위

본 조사 보고서에서는 고온 단열재 시장을 재질별, 온도 폭별, 최종 이용 산업별로 분류하고 있습니다. 이 보고서의 조사 범위는 고온 단열재 시장의 성장에 영향을 미치는 촉진요인, 억제요인, 과제 및 기회에 대한 자세한 정보를 다룹니다. 주요 업계 진출 기업의 상세한 분석을 실시해, 사업 개요, 제공 제품 및 고온 단열재 시장과 관련된 합병 및 인수, 제품 발매, 사업 확대 등의 주요 전략에 관한 인사이트를 제공합니다. 이 보고서는 고온 단열재 시장 생태계의 신흥 신생 기업의 경쟁 분석을 다루고 있습니다.

이 보고서를 구입하는 이유

이 보고서는 시장 리더 및 신규 진출기업에게 고온 단열재 시장 전체 및 하위 부문의 수익 수치에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자는 경쟁 구도를 이해하고, 자사의 포지셔닝 강화를 위한 인사이트를 깊게 하고, 적절한 시장 진출 전략을 입안할 수 있게 됩니다. 이 보고서는 시장 동향을 파악하고 주요 시장 성장 촉진요인, 시장 성장 억제요인, 과제 및 기회에 대한 정보를 이해 관계자에게 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인 분석(고온 및 중공업 분야에서 수요 증가, 엄격화하는 에너지 효율 및 배출 규제, '항공우주 및 자동차' 산업에서의 경량이고 고성능인 단열 솔루션에 대한 수요 증가), 제약 요인(건강, 안전 및 환경 규제별 컴플라이언스 비용 증가, 공급망 불안정성 및 고자본 비용에 의한 시장 확대의 저해), 시장 기회(신흥 경제국에서의 산업 확대, 탈탄소화, 개수 및 에너지 절약 프로젝트에서의 수요 증가), 시장 과제(가혹한 복합 재해 환경하에서의 성능 열화 및 기술적 복잡성, 재료 채용을 저해하는 인증 및 시험의 병목)에 대해서 분석했습니다.

- 제품 개발 및 이노베이션 : 고온 단열재 시장에서의 향후 기술 동향, 연구개발 활동, 제품 및 서비스 투입에 관한 상세한 분석.

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보-이 보고서는 다양한 지역의 고온 단열재 시장을 분석합니다.

- 시장 다양화 : 고온 단열재 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보.

- 경쟁 평가 : 주요 기업 3M(US), Morgan Advanced Materials plc(UK), RHI Magnesita GmbH(Austria), Luyang Energy-saving Materials(China), Etex Group(Belgium), Calderys(France), Alkegen(US), SHINAGAWA REFRA(Japan), IBIDEN

Grupo NUTEC(Mexico) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 언멧 요구와 공백

- 상호접속된 시장 및 분야 간 기회

- 티어별 전략적 움직임-Tier 1/2/3 기업

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 분석

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 주된 회의 및 이벤트(2025-2026년)

- 고객 사업에 영향을 주는 동향 및 혼란

- 투자 및 자금조달 시나리오

- 사례 연구 분석

- 미국 관세가 고온 단열재 시장에 미치는 영향(2025년)

제6장 기술, 특허, 디지털 및 AI 도입별 전략적 파괴

- 주요 신기술

- 보완적 기술

- 기술 및 제품 로드맵

- 특허 분석

- 미래 용도

- AI 및 생성형 AI가 고온 단열재 시장에 미치는 영향

- 성공 사례 및 실세계에 대한 용도

제7장 지속가능성 및 규제 상황

- 지역 규제 및 규정 준수

- 지속가능성에 대한 노력

- 지속가능성에 미치는 영향 및 규제 정책의 노력

- 인증, 라벨, 환경 기준

제8장 고객 정세 및 구매 행동

- 의사 결정 프로세스

- 구매자의 이해관계자 및 구매 평가 기준

- 채용 장벽 및 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 요구

- 시장 수익성

제9장 고온 단열재 시장 : 재질별

- 세라믹 섬유

- 단열 내화 벽돌

- 규산칼슘

- 기타

제10장 고온 단열재 시장 : 온도 폭별

- 600°C-1100°C(1112°F-2012°F)

- 1100°C-1500°C(2012°F-2732°F)

- 1500°C-1700°C(2732°F-3092°F)

- 1700°C(3092°F) 이상

제11장 고온 단열재 시장 : 최종 이용 산업별

- 석유화학 제품

- 세라믹

- 유리

- 알루미늄

- 철강

- 시멘트

- 내열 재료

- 분말 야금

- 기타

제12장 고온 단열재 시장 : 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타

- 유럽

- 독일

- 프랑스

- 튀르키예

- 러시아

- 영국

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타

- 중동 및 아프리카

- GCC 국가

- 남아프리카

- 기타

제13장 경쟁 구도

- 개요

- 주요 진입기업의 전략

- 시장 점유율 분석

- 수익 분석

- 기업 평가 및 재무지표

- 브랜드 비교

- 기업 평가 매트릭스 : 주요 진입기업(2024년)

- 기업 평가 매트릭스 : 스타트업 및 중소기업(2024년)

- 경쟁 시나리오

제14장 기업 프로파일

- 주요 진출기업

- 3M

- MORGAN ADVANCED MATERIALS PLC

- RHI MAGNESITA GMBH

- LUYANG ENERGY-SAVING MATERIALS CO., LTD.

- ETEX GROUP

- CALDERYS

- ALKEGEN

- SHINAGAWA REFRA CO., LTD.

- IBIDEN

- GRUPO NUTEC

- 기타 기업

- PYROTEK

- RATH-GROUP

- MAFTEC CO., LTD.

- BNZ MATERIALS

- COTRONICS CORP.

- ADL INSULFLEX, INC.

- ME SCHUPP INDUSTRIEKERAMIK GMBH

- YESO INSULATING PRODUCTS COMPANY LIMITED

- ZIRCAR CERAMICS

- FIBRECAST INC.

- MINERAL SEAL CORPORATION

- REFMON

- VITCAS

- FIRWIN CORPORATION

- TECHNO WORLD CORPORATION

제15장 조사 방법

제16장 부록

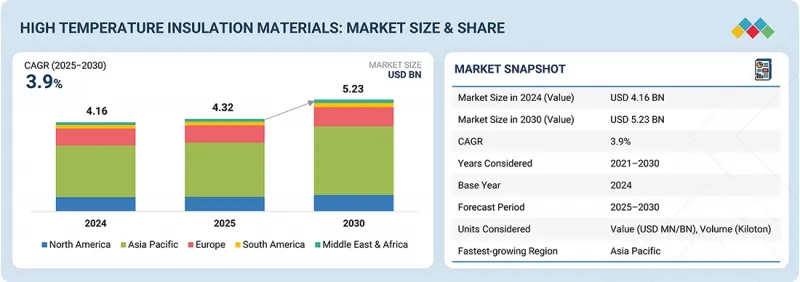

AJY 25.12.24The high temperature insulation materials market is projected to reach USD 5.23 billion by 2030 from USD 4.32 billion in 2025, at a CAGR of 3.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Material Type, Temperature Range, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

High temperature insulation materials are being steadily used in heavy industries such as metallurgy, cement, glass, and petrochemicals, due to stringent safety and energy-efficiency regulations from organizations like the Bureau of Energy Efficiency (India) and material standards from ASTM International. Materials such as ceramic fiber blankets, calcium silicate boards, and refractory bricks are manufactured to offer dimensional stability, low thermal conductivity, and durability at operating temperatures ranging from 600°C to over 1,500°C. They support lining in industrial furnaces, insulation of process equipment, high-temperature ductwork, and thermal protection in complex manufacturing systems.

Further, according to NASA evaluations, these materials enable reliable performance in space nuclear systems by withstanding extreme radiant heat fluxes. The US Department of Energy guidelines place their role as reducing industrial energy losses by up to 20% in high-heat processes.

"Ceramic fibers are projected to be the fastest-growing material type in the high temperature insulation materials market during the forecast period."

Ceramic fibers are expected to be the most rapidly expanding material category in the high temperature insulation materials market during the forecast period, due to their exceptional thermal resistance, low thermal conductivity, and outstanding energy efficiency. These fibers can withstand extremely high temperatures of more than 1,700°C and, therefore, are used in various critical applications, such as petrochemical processing, iron & steel production, power generation, and high-temperature furnaces. The low weight and ease of installation improve the efficiency while also decreasing the overall maintenance costs. Developments in fiber chemistry, biodegradable formulations, and further enhancements in durability are expanding their application areas in industries seeking safer, efficient, and environmentally compliant insulation solutions, driving strong market growth.

"Cement is projected to be the fastest-growing end-use industry in the high temperature insulation materials market during the forecast period."

During the forecast period, the cement segment is expected to be the fastest-growing end-use industry in the high-temperature insulation materials market, driven by rising global construction activities and an increased focus on energy efficiency. The manufacturing process for cement involves kiln operations at temperatures exceeding 1,450°C, driving demand for high-performance insulation materials that reduce heat loss, ensure fuel efficiency, and extend the lifespan of refractory bricks. Additionally, the modernization of cement plants, regulations aimed at reducing emissions, and the growing trend towards environmentally friendly manufacturing are all expected to be major factors driving the use of ceramic fibers, insulating firebricks, and calcium silicate products in the market. High-temperature insulation materials will be instrumental in lowering operational costs, enhancing thermal performance, and facilitating decarbonization, thereby allowing the total high-temperature insulation materials market in the cement industry to grow at a rapid pace.

"Asia Pacific is projected to be the fastest-growing region in the high temperature insulation materials market during the forecast period."

Asia Pacific is expected to have the fastest growth in the high temperature insulation materials market. Quick industrialization and a large-scale rise in the cement, petrochemical, metal, and glass industries are the main factors that are resulting in the rapid growth of the area. Adoption is being buoyed by the implementation of stricter regulatory energy-efficiency standards, more infrastructure investment, and the rising demand for high-performance insulation to reduce heat loss and CO2 emissions. There are also further reasons for the positive growth outlook, including ongoing capacity increases and a competitive manufacturing base.

By Company Type: Tier 1: 40%, Tier 2: 30%, and Tier 3: 30%

By Designation: Directors: 30%, Managers: 20%, and Others: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and the Middle East & Africa 20%

Notes: Others include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 Million-1 Billion; and Tier 3: <USD 500 Million

Companies Covered: 3M (US), Morgan Advanced Materials plc (UK), RHI Magnesita GmbH (Austria), Luyang Energy-saving Materials Co., Ltd. (China), Etex Group (Belgium), Calderys (France), Alkegen (US), SHINAGAWA REFRA Co., Ltd. (Japan), IBIDEN (Japan), and Grupo NUTEC (Mexico) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the high temperature insulation materials market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the high temperature insulation materials market based on material type (ceramic fibers, insulating fire bricks, calcium silicate, and other types), temperature range [600-1,100°C (1,112-2,012°F), 1,100-1,500°C (2,012-2,732°F), 1,500-1,700°C (2,732-3,092°F), and 1,700°C (3,092°F) and above], and end-use industry (petrochemical, ceramic, glass, aluminum, iron & steel, cement, refractory, powder metallurgy, and other end-use industries). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the high temperature insulation materials market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as mergers, acquisitions, product launches, and expansions, associated with the high temperature insulation materials market. This report covers a competitive analysis of upcoming startups in the high temperature insulation materials market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall high temperature insulation materials market and the subsegments. It will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points.

- Analysis of key drivers (rising demand from high-heat and heavy industries, stringent energy efficiency and emission regulations, growing demand for lightweight and high-performance insulation solutions in the aerospace and automotive industries), restraints (health, safety, and environmental regulations increasing compliance costs, supply chain volatility and high capital costs limiting market expansion), opportunities (industrial expansion in emerging economies, rising demand from decarbonization, retrofit, and energy-efficiency projects), and challenges (performance degradation and technical complexity in extreme multi-hazard environments, certification and testing bottlenecks hindering material adoption ).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the high temperature insulation materials market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the high temperature insulation materials market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the high temperature insulation materials market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as 3M (US), Morgan Advanced Materials plc (UK), RHI Magnesita GmbH (Austria), Luyang Energy-saving Materials Co., Ltd. (China), Etex Group (Belgium), Calderys (France), Alkegen (US), SHINAGAWA REFRA Co., Ltd. (Japan), IBIDEN (Japan), and

Grupo NUTEC (Mexico), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIONS SHAPING HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 3.2 ASIA PACIFIC: HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY TYPE AND COUNTRY

- 3.3 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY MATERIAL TYPE

- 3.4 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY TEMPERATURE RANGE

- 3.5 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY END-USE INDUSTRY

- 3.6 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY KEY COUNTRIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Expanding demand from high-heat and heavy industries

- 4.2.1.2 Stringent energy efficiency and emission regulations

- 4.2.1.3 Growing demand for lightweight and high-performance insulation solutions in aerospace and automotive industries

- 4.2.2 RESTRAINTS

- 4.2.2.1 Health, safety, and environmental regulations increasing compliance costs

- 4.2.2.2 Supply chain volatility and high capital costs limiting market expansion

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Industrial expansion in emerging economies

- 4.2.3.2 Rising demand from decarbonization, retrofit, and energy-efficiency projects

- 4.2.4 CHALLENGES

- 4.2.4.1 Performance degradation and technical complexity in extreme multi-hazard environments

- 4.2.4.2 Certification and testing bottlenecks hindering material adoption

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER - 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING ANALYSIS BASED ON MATERIAL TYPE

- 5.5.2 PRICING ANALYSIS BASED ON REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 690220)

- 5.6.2 IMPORT SCENARIO (HS CODE 690220)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ENERGY SAVINGS AND PERFORMANCE IMPROVEMENT IN STEEL LADLES USING WDS MICROPOROUS INSULATION

- 5.10.2 CONVERTING DIVERTER DAMPERS FROM STONE WOOL TO SUPERWOOL PLUS BLANKET

- 5.10.3 SUPERWOOL PRIME FOR EXPANSION JOINTS IN ANODE BAKING FURNACE

- 5.11 IMPACT OF 2025 US TARIFF ON HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON KEY COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 China

- 5.11.4.3 Europe

- 5.11.4.4 Mexico

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ALUMINA-ENHANCED AEROGELS AND MULLITE COMPOSITES

- 6.1.2 PHONONIC NANO-STRUCTURED AND HOLLOW MICROSPHERE BOARDS

- 6.1.3 HIGH-ENTROPY OXIDE FIBERS AND PYROCHLORE STRUCTURES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 HIGH-TEMPERATURE SENSORS AND EMBEDDED MONITORING SYSTEMS

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | PERFORMANCE STABILIZATION & EARLY DIGITIZATION

- 6.3.2 MID-TERM (2027-2030) | TECHNOLOGY SCALING & ADVANCED SYSTEM INTEGRATION

- 6.3.3 LONG-TERM (2030-2035+) | NEXT-GENERATION MATERIALS & FULLY DIGITAL THERMAL ENVIRONMENTS

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 INSIGHTS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 THERMAL PROTECTION SYSTEMS (TPS) FOR NEXT-GEN AEROSPACE & SPACECRAFT

- 6.5.2 HIGH-TEMPERATURE INSULATION FOR HYDROGEN PRODUCTION & STORAGE

- 6.5.3 ADVANCED THERMAL MANAGEMENT FOR ELECTRIC VEHICLES (EVS)

- 6.6 IMPACT OF AI/GEN AI ON HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN HIGH-TEMPERATURE INSULATION MATERIALS PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN HIGH-TEMPERATURE INSULATION MATERIALS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 AEROSPACE THERMAL PROTECTION: SPACE SHUTTLE AND BEYOND

- 6.7.2 AUTOMOTIVE EXHAUST SYSTEMS: FORD'S HIGH-PERFORMANCE ENGINE INSULATION

- 6.7.3 INDUSTRIAL KILN OPTIMIZATION: OVERSEAS CERAMIC MANUFACTURING PROJECT

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF HIGH-TEMPERATURE INSULATION MATERIALS

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF HIGH-TEMPERATURE INSULATION MATERIALS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY APPLICATION

9 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY MATERIAL TYPE

- 9.1 INTRODUCTION

- 9.2 CERAMIC FIBERS

- 9.2.1 REFRACTORY CERAMIC FIBER (RCF)

- 9.2.1.1 Growing demand for high-efficiency, high-temperature insulation to drive market

- 9.2.2 LOW BIOPERSISTENT CERAMIC FIBERS

- 9.2.2.1 Regulatory push toward safer, eco-friendly insulation materials supporting adoption

- 9.2.3 POLYCRYSTALLINE CERAMIC FIBERS

- 9.2.3.1 Demand for ultra-high-temperature insulation solutions to drive market

- 9.2.1 REFRACTORY CERAMIC FIBER (RCF)

- 9.3 INSULATING FIREBRICKS

- 9.3.1 ACIDIC REFRACTORY BRICKS

- 9.3.1.1 Demand for refractories resistant to acidic slag and atmospheres to fuel market growth

- 9.3.2 NEUTRAL REFRACTORY BRICKS

- 9.3.2.1 Increasing use of multipurpose refractories for mixed chemical environments to support market growth

- 9.3.3 BASIC REFRACTORY BRICKS

- 9.3.3.1 Adoption in alkaline slag environments to support market growth

- 9.3.1 ACIDIC REFRACTORY BRICKS

- 9.4 CALCIUM SILICATE

- 9.4.1 LIGHTWEIGHT CALCIUM SILICATE

- 9.4.1.1 Increasing demand for low thermal conductivity backup insulation to drive market

- 9.4.2 MEDIUM DENSE CALCIUM SILICATE

- 9.4.2.1 Rising adoption of asbestos-free, high-stability insulation solutions to drive demand

- 9.4.3 DENSE CALCIUM SILICATE

- 9.4.3.1 Need for high-strength, high-performance components in molten metal handling to fuel adoption

- 9.4.1 LIGHTWEIGHT CALCIUM SILICATE

- 9.5 OTHER TYPES

- 9.5.1 PERLITE

- 9.5.2 VERMICULITE

- 9.5.3 MICROPOROUS MATERIALS

10 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY TEMPERATURE RANGE

- 10.1 INTRODUCTION

- 10.2 600°C-1100°C (1112°F-2012°F)

- 10.2.1 WIDE MATERIAL COMPATIBILITY AND HIGH ADOPTION IN MID-TEMPERATURE INDUSTRIAL APPLICATIONS TO DRIVE DEMAND

- 10.3 1100°C-1500°C (2012°F-2732°F)

- 10.3.1 INCREASED DEMAND IN PETROCHEMICAL AND METAL PROCESSING TO DRIVE MARKET

- 10.4 1500°C-1700°C (2732°F-3092°F)

- 10.4.1 GROWING ADOPTION IN METAL PROCESSING, CERAMICS, CEMENT, AND IRON & STEEL INDUSTRIES DRIVING DEMAND

- 10.5 1700°C (3092°F) AND ABOVE

- 10.5.1 RISING NEED FOR ULTRA-HIGH-TEMPERATURE REFRACTORIES IN GLASS, STEEL, AND SOLAR POWER APPLICATIONS TO FUEL DEMAND

11 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 PETROCHEMICALS

- 11.2.1 RISING ENERGY DEMAND AND EMISSION CONTROL DRIVING INSULATION MATERIAL ADOPTION

- 11.3 CERAMIC

- 11.3.1 HIGH ENERGY DEPENDENCE AND EMISSION REGULATIONS FUELING ADOPTION

- 11.4 GLASS

- 11.4.1 HIGH-TEMPERATURE OPERATIONS AND DECARBONIZATION EFFORTS TO DRIVE MARKET GROWTH

- 11.5 ALUMINUM

- 11.5.1 DEMAND FOR HIGH THERMAL EFFICIENCY TO SUPPORT MARKET GROWTH

- 11.6 IRON & STEEL

- 11.6.1 ENERGY EFFICIENCY IMPERATIVES DRIVING INSULATION ADOPTION IN STEELMAKING

- 11.7 CEMENT

- 11.7.1 HIGH ENERGY INTENSITY AND EMISSION REDUCTION TARGETS FUELING ADOPTION

- 11.8 REFRACTORY

- 11.8.1 DEMAND FOR HIGH-EFFICIENCY FURNACE DESIGNS BOOSTING ADOPTION

- 11.9 POWDER METALLURGY

- 11.9.1 RISING ADOPTION OF HIGH-TEMPERATURE SINTERING FOR ADVANCED POWDERED METAL PARTS TO DRIVE MARKET

- 11.10 OTHER END-USE INDUSTRIES

12 HIGH-TEMPERATURE INSULATION MATERIALS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 ASIA PACIFIC

- 12.2.1 CHINA

- 12.2.1.1 Industrial capacity expansion accelerating demand for advanced high-temperature insulation

- 12.2.2 INDIA

- 12.2.2.1 Government-led industrial expansion and energy-efficiency mandates accelerating insulation adoption

- 12.2.3 JAPAN

- 12.2.3.1 Strong energy-efficiency mandates sustaining demand

- 12.2.4 SOUTH KOREA

- 12.2.4.1 K-Green New Deal and 2050 net-zero commitments fueling demand

- 12.2.5 REST OF ASIA PACIFIC

- 12.2.1 CHINA

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Strong industrial base and advanced manufacturing to drive demand

- 12.3.2 FRANCE

- 12.3.2.1 Rising energy costs and industrial modernization strengthening demand

- 12.3.3 TURKEY

- 12.3.3.1 Export competitiveness and decarbonization policies to drive demand

- 12.3.4 RUSSIA

- 12.3.4.1 Industrial resilience, energy security pressures, and import-substitution policies to drive demand

- 12.3.5 UK

- 12.3.5.1 Industrial decarbonization pressures and efficiency upgrades accelerating demand

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 NORTH AMERICA

- 12.4.1 US

- 12.4.1.1 Expanding energy-intensive industries and strong regulatory push for thermal efficiency supporting market growth

- 12.4.2 CANADA

- 12.4.2.1 Rising industrial decarbonization pressures to propel market growth

- 12.4.3 MEXICO

- 12.4.3.1 Industrial recovery and thermal-efficiency regulations accelerating adoption

- 12.4.1 US

- 12.5 SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 Rising cement production & sales to drive demand for advanced kiln insulation

- 12.5.2 ARGENTINA

- 12.5.2.1 Rising clinker output and furnace modernization to boost adoption

- 12.5.3 REST OF SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

- 12.6.1.1 Saudi Arabia

- 12.6.1.1.1 Massive petrochemical and refining capacity expansion driving demand

- 12.6.1.2 UAE

- 12.6.1.2.1 Expanding metals, petrochemicals, and cement production driving adoption

- 12.6.1.3 Rest of GCC Countries

- 12.6.1.1 Saudi Arabia

- 12.6.2 SOUTH AFRICA

- 12.6.2.1 Growing demand for energy efficiency and furnace modernization across high-heat industries to fuel market growth

- 12.6.3 REST OF MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES

- 13.3 MARKET SHARE ANALYSIS

- 13.4 REVENUE ANALYSIS

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Material type footprint

- 13.7.5.4 Temperature range footprint

- 13.7.5.5 End-use industry footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 3M

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 MnM view

- 14.1.1.3.1 Key strengths

- 14.1.1.3.2 Strategic choices

- 14.1.1.3.3 Weaknesses and competitive threats

- 14.1.2 MORGAN ADVANCED MATERIALS PLC

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 RHI MAGNESITA GMBH

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Deals

- 14.1.3.3.2 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 LUYANG ENERGY-SAVING MATERIALS CO., LTD.

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 ETEX GROUP

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Deals

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 CALDERYS

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Deals

- 14.1.6.4 MnM view

- 14.1.7 ALKEGEN

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 MnM view

- 14.1.8 SHINAGAWA REFRA CO., LTD.

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.8.3.2 Expansions

- 14.1.8.4 MnM view

- 14.1.9 IBIDEN

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 MnM view

- 14.1.10 GRUPO NUTEC

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches

- 14.1.10.3.2 Expansions

- 14.1.10.4 MnM view

- 14.1.1 3M

- 14.2 OTHER PLAYERS

- 14.2.1 PYROTEK

- 14.2.2 RATH-GROUP

- 14.2.3 MAFTEC CO., LTD.

- 14.2.4 BNZ MATERIALS

- 14.2.5 COTRONICS CORP.

- 14.2.6 ADL INSULFLEX, INC.

- 14.2.7 M.E. SCHUPP INDUSTRIEKERAMIK GMBH

- 14.2.8 YESO INSULATING PRODUCTS COMPANY LIMITED

- 14.2.9 ZIRCAR CERAMICS

- 14.2.10 FIBRECAST INC.

- 14.2.11 MINERAL SEAL CORPORATION

- 14.2.12 REFMON

- 14.2.13 VITCAS

- 14.2.14 FIRWIN CORPORATION

- 14.2.15 TECHNO WORLD CORPORATION

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.2.3 Breakdown of interviews with experts

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 DEMAND-SIDE APPROACH

- 15.3.2 SUPPLY-SIDE APPROACH

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS