|

시장보고서

상품코드

1891776

엔지니어링 플라스틱 시장 : 유형별, 최종 이용 산업별, 지역별 - 예측(-2030년)Engineering Plastics Market by Type (Acrylonitrile Butadiene Styrene (ABS), Polyamide, Polycarbonate, Thermoplastic Polyester (PET & PBT), Polyacetal, and Fluoropolymer), End-use Industry, and Region - Global Forecast to 2030 |

||||||

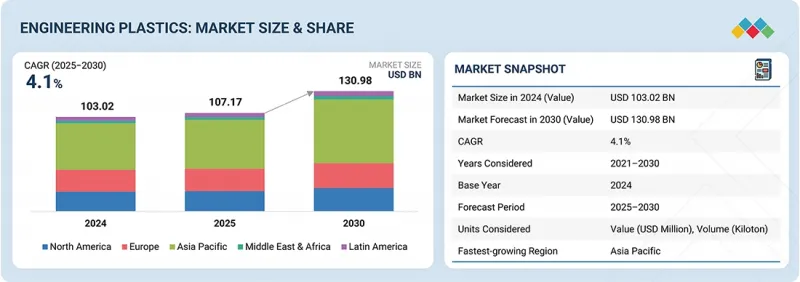

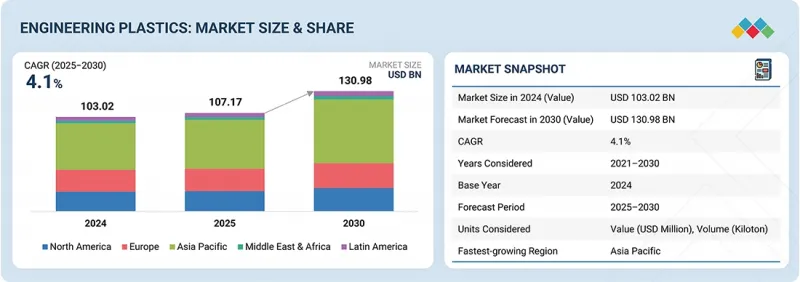

엔지니어링 플라스틱 시장 규모는 예측 기간 동안 4.1%의 CAGR로 성장하여 2025년 1,071억 7,000만 달러에서 2030년에는 1,309억 8,000만 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 유형별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

엔지니어링 플라스틱 산업은 각 산업이 유연성, 내구성, 고성능을 갖춘 재료로 전환하고 있어 앞으로도 꾸준한 성장을 이어갈 것으로 예상됩니다. 소비재, 자동차, 전기 및 전자제품, 의료기기 등 많은 제조업에서 기계적 강도, 열 안정성, 내화학성, 치수 안정성 등의 특성을 바탕으로 고성능 폴리머를 채택하고 있습니다. 미국 식품의약국(FDA), 유럽화학제품청(ECHA), 기타 지방정부 등 규제 당국은 재료의 안전성, 화학제품 적합성, 지속가능성에 대해 엄격한 기준을 적용하고 있습니다. 제조업체들은 보다 효율적이고 환경적으로 지속가능한 운영 요건을 충족시키기 위해 고순도, 난연성, 재활용이 가능한 혁신적인 엔지니어링 플라스틱으로 이 문제를 해결하고 있습니다.

생체적합성 소재를 만들기 위한 새로운 강화 폴리머의 개발과 폴리머 가공의 첨단 기술은 부품의 성능 향상을 실현하는 동시에 부품 재료의 사용량과 환경에 미치는 영향을 줄입니다. 공정 실시간 모니터링, 적층조형, 예측 시뮬레이션 기술을 통해 엔지니어링 플라스틱의 용도에 따른 재료 특성을 정밀하게 최적화할 수 있게 되었습니다. 또한, 재료 성형 및 조형의 고속성과 제어성, 엔지니어링 플라스틱을 이용한 압출 및 사출 성형 시스템의 자동화를 통해 산업 및 소비자 시장의 변화하는 요구에 부응하는 엔지니어링 플라스틱의 지속적인 채택이 이루어지고 있습니다.

2024년 ABS는 자동차, 전기 및 전자, 소비재 등 주요 시장 부문에서 광범위하게 사용되면서 엔지니어링 플라스틱 산업을 이끌었습니다. ABS의 기계적 강도, 내충격성, 성형의 유연성은 다양한 용도와 산업에 적합한 특성을 제공합니다. ABS의 경량성과 연료 효율성은 자동차 산업에서 널리 선호되고 있으며, 최종 용도에서 가장 큰 점유율을 차지했습니다. ABS는 전기기기 케이스, 가전제품, 3D 프린팅에도 사용되어 산업용 및 민수용 애플리케이션에서 다재다능함을 보여주고 있습니다. 지속가능한 고성능 소재와 고분자 가공 기술에 대한 수요 증가로 ABS의 시장 지위가 강화되고 있습니다. 각 분야가 내구성, 비용 효율성, 설계 유연성을 중시하는 가운데 ABS는 계속해서 시장을 선도할 것입니다.

2024년, 자동차 및 운송 장비 산업은 경량화, 고성능, 연비 효율이 높은 차량에 초점을 맞춘 엔지니어링 플라스틱 세계 시장에서 괄목할만한 성장을 이루었습니다. 폴리아미드, PEEK, PPS, PC/ABS 블렌드는 기계적 특성과 내열성 및 내화학성을 겸비하여 엔진 부품, 보닛 아래 부품, 전기 시스템 부품 등 다양한 부품의 공급원이 되었습니다. 전기자동차 및 하이브리드 자동차의 보급 확대에 따라 엔지니어링 폴리머는 성능 향상, 차량 경량화, 연비 효율화를 실현하는 솔루션으로 폭넓게 채택될 가능성이 있습니다. 복합재료의 배합 기술, 재료 개질, 폴리머 설계의 발전으로 그 응용 범위와 수명은 앞으로도 계속 확대될 것입니다. 자동차 및 운송기기 산업은 지속가능성, 비오염성, 연비 효율 향상 규제 대응을 중시하는 OEM 제조업체의 수요가 가장 높기 때문에 엔지니어링 플라스틱은 중요한 소재입니다.

아시아태평양은 산업화 및 도시화의 진전과 자동차, 전기전자, 건설, 기계 분야의 확대로 인해 2024년 엔지니어링 플라스틱 시장을 주도했습니다. 중국, 일본, 인도, 한국은 풍부한 원자재, 저비용 제조, 산업 확대를 위한 정부 지원의 혜택을 받았습니다. 자동차 산업에서는 경량화, 연비 효율화 차량에 대한 폴리아미드, PEEK, PPS의 수요가 증가하였고, 전자 산업에서는 내열성과 내구성을 겸비한 소재가 요구되었습니다. 고분자 합성, 재료 개질, 정밀 가공 기술의 발전으로 성능이 더욱 향상되고 응용 범위가 넓어졌습니다. 환경 규제 강화, 지속가능성 프로그램, 에너지 효율 목표도 첨단 친환경 엔지니어링 플라스틱의 사용을 촉진했습니다. 현지 제조업체 간의 전략적 투자와 제휴를 통해 제조 능력, 제품 품질 및 기술 리더십을 강화하여 아시아태평양의 엔지니어링 플라스틱 시장에서 선도적인 위치를 확고히 하고 있습니다.

대상 기업 : 본 보고서에는 BASF(독일), Covestro AG(독일), Celanese Corporation(미국), DuPont(미국), Syensqo(벨기에), LG Chem(대한민국), SABIC(사우디아라비아), Evonik Industries AG(독일), Mitsubishi Chemical Group Corporation(일본), Envalior(독일)이 포함됩니다.

엔지니어링 플라스틱 시장의 주요 기업에 대해 조사했으며, 기업 개요, 최근 동향, 주요 시장 전략을 포함한 상세한 경쟁 분석을 실시했습니다.

조사 범위

본 조사 보고서는 엔지니어링 플라스틱 시장을 유형별(아크릴로니트릴-부타디엔-스티렌(ABS), 폴리아미드, 폴리카보네이트, 열가소성 폴리에스테르(PET 및 PBT), 폴리아세탈, 불소수지, 기타) 및 최종 이용 산업별(자동차, 운송 기기, 가전제품, 전기/전자, 산업/기계, 포장, 기타 최종 이용 산업)으로 분류하고 있습니다. 이 보고서의 조사 범위는 엔지니어링 플라스틱 시장의 성장에 영향을 미치는 촉진요인, 제약요인, 과제 및 기회에 대한 자세한 정보를 다룹니다. 주요 산업 플레이어에 대한 상세한 분석을 통해 사업 개요, 제품 및 엔지니어링 플라스틱 시장과 관련된 신제품 출시, 제휴, 협업, 합병, 인수, 사업 확장 등 주요 전략에 대한 인사이트를 제공합니다. 본 보고서는 엔지니어링 플라스틱 시장 생태계에서 신흥 스타트업 기업의 경쟁 분석도 다루고 있습니다.

본 보고서 구매의 장점

이 보고서는 시장 리더와 신규 진입자에게 전체 엔지니어링 플라스틱 시장 및 하위 부문의 수익 수치에 대한 가장 정확한 추정치를 제공합니다. 이해관계자들이 경쟁 상황을 이해하고, 자사의 포지셔닝을 강화할 수 있는 인사이트를 키우고, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것입니다. 시장 동향을 파악하고 주요 시장 촉진요인, 제약요인, 과제, 기회요인에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인 분석(경량화 자동차 및 전기자동차 애플리케이션의 엔지니어링 플라스틱 수요 확대, 전자 및 전기 산업 성장, 주요 산업에서 3D 프린팅의 폴리아미드(PA11 및 PA12) 채택 증가), 억제요인(원자재 가격 변동, 대체 소재와의 경쟁, 인프라 제약), 기회(의료기기의 생체적합성 엔지니어링 플라스틱 수요 확대, 고성능 특수 등급 개발, 신흥국 수요 증가), 도전과제(성능, 지속가능성 및 가공성 균형) 제약), 기회(의료기기의 생체적합성 엔지니어링 플라스틱 수요 확대, 고성능 특수 등급 개발, 신흥국 수요 증가), 도전과제(성능 - 지속가능성-가공성 균형, 세계 무역의 불확실성)에 대해 분석하고 있습니다.

- 제품 개발/혁신 : 엔지니어링 플라스틱 시장의 신기술 동향, 연구개발 활동, 제품 및 서비스 출시에 대한 상세한 분석.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 엔지니어링 플라스틱 시장을 분석합니다.

- 시장 다각화 : 엔지니어링 플라스틱 시장의 신제품 및 서비스, 미개척 지역, 최근 동향, 투자에 대한 종합적인 정보를 제공합니다.

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 주요 인사이트

제5장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

제6장 업계 동향

- 고객 비즈니스에 영향을 미치는 동향/혼란

- 생태계 분석

- 밸류체인 분석

- 관세와 규제 상황

- 무역 분석

- 기술 분석

- 특허 분석

- 2025-2026년의 주요 회의와 이벤트

- 사례 연구 분석

- 투자와 자금 조달 시나리오

- 생성형 AI/AI가 엔지니어링 플라스틱 시장에 미치는 영향

- Porter's Five Forces 분석

- 주요 이해관계자와 구입 기준

- 거시경제 분석

- 2025년 미국 관세의 영향 - 엔지니어링 플라스틱 시장

제7장 엔지니어링 플라스틱 시장(유형별)

- 아크릴로니트릴 부타디엔 스티렌

- 폴리아미드

- 폴리카보네이트

- 열가소성 폴리에스테르

- 폴리아세탈

- 불소수지

- 기타

제8장 엔지니어링 플라스틱 시장(최종 이용 산업별)

- 자동차·운송

- 가전제품

- 전기·전자공학

- 산업기계

- 포장

- 기타

제9장 엔지니어링 플라스틱 시장(지역별)

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 대만

- 인도네시아

- 기타

- 유럽

- 독일

- 프랑스

- 이탈리아

- 러시아

- 영국

- 기타

- 북미

- 미국

- 캐나다

- 멕시코

- 중동 및 아프리카

- GCC 국가

- 남아프리카공화국

- 기타

- 남미

- 브라질

- 아르헨티나

- 기타

제10장 경쟁 구도

- 개요

- 주요 진출 기업의 전략

- 시장 점유율 분석

- 매출 분석

- 기업 평가와 재무 지표

- 제품/브랜드 비교

- 기업 평가 매트릭스 : 주요 진출 기업, 2024년

- 기업 평가 매트릭스 : 스타트업/중소기업, 2024년

- 경쟁 시나리오

제11장 기업 개요

- 주요 진출 기업

- BASF

- COVESTRO AG

- CELANESE CORPORATION

- DUPONT

- SYENSQO

- LG CHEM

- SABIC

- EVONIK INDUSTRIES AG

- MITSUBISHI CHEMICAL GROUP CORPORATION

- ENVALIOR

- 기타 기업

- KINGFA SCI.&TECH. CO.,LTD.

- ASAHI KASEI CORPORATION

- ARKEMA

- EASTMAN CHEMICAL COMPANY

- CHIMEI

- DAICEL CORPORATION

- ADVANSIX

- ROCHLING

- TRINSEO

- GRAND PACIFIC PETROCHEMICAL CORPORATION

- GUANGDONG ENGINEERING PLASTICS INDUSTRIES(GROUP) CO., LTD.

- ESTER INDUSTRIES LIMITED

- ENSINGER

- APPL INDUSTRIES LIMITED

- PAR GROUP

- HITEMP POLYMERS PVT. LTD.

- SIMONA PMC

제12장 인접 시장과 관련 시장

제13장 부록

KSM 26.01.05The engineering plastics market is expected to reach USD 130.98 billion by 2030 from USD 107.17 billion in 2025, at a CAGR of 4.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | Type, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

The engineering plastics industry will continue to experience consistent growth because industries are moving toward flexible, durable, and high-performance materials. Many manufacturing industries, such as consumer products, automotive, electrical & electronics, and medical devices, are adopting these high-performance polymers based on mechanical strength, thermal stability, chemical resistance, and dimensional stability. Regulatory authorities, such as the FDA, European Chemicals Agency (ECHA), and other local authorities, are implementing some stringent standards around the safety of materials, compliance with chemicals, and sustainability. Manufacturers are stepping up to the challenge with innovative engineering plastics that are high-purity, flame-retardant, and recyclable to satisfy the operating requirements of being more efficient and environmentally sustainable.

New developments with reinforced polymers to create biocompatible materials, and advanced techniques for processing polymers improve performance outcomes of components while decreasing the volume of component material and the environmental impacts of components. Real-time monitoring of processes, additive manufacturing, and predictive simulation are all enabling fine-tuned optimization of material behavior when using engineering plastics for their applications. Moreover, the combination of speed and controllability of material formation and shaping, automating extrusion and molding systems using engineering plastics, allows for ongoing acceptance of engineering plastics that continue to meet the changing needs of industrial and consumer markets.

"Acrylonitrile butadiene styrene (ABS) accounted for the largest share of the engineering plastics market in 2024."

In 2024, ABS led the engineering plastics industry due to its widespread use in key market segments such as automotive, electrical & electronics, and consumer goods. ABS' mechanical strength, impact resistance, and molding flexibility made it suitable for a variety of uses and industries. ABS' lightweight and fuel-efficient properties have also made it widely popular in the automotive industry, which captured the largest share of end-use applications. ABS is also used in electrical housing, appliances, and 3D printing, demonstrating its versatility in industrial and consumer applications. Growing demand for sustainable and high-performance materials and polymer processing technology has strengthened ABS' market position. ABS will remain a market leader as sectors prioritize durability, cost-effectiveness, and design flexibility.

"Automotive & transportation segment accounted for the largest share of the engineering plastics market in 2024."

In 2024, the automotive & transportation industry experienced significant growth in the global market for engineering plastics with a focus on lightweight, high-performance, fuel-efficient vehicles. Polyamide, PEEK, PPS, and PC/ABS blends provided a multitude of parts in engine parts, under the hood parts, and electrical system components since they contain mechanical properties and thermal and chemical resistance. With the growth in popularity for electric and hybrid cars, engineered polymers could be extensively employed as a solution to provide improved performance, lighter vehicles, and fuel efficiency. Advancements in composite formulations, material modifications, and polymer designs will continue to enhance their application and useful life. Engineered plastics are important materials because the automotive and transportation industries exhibit the highest demand based on original equipment manufacturer (OEM) concern for sustainable, non-polluting, and increased fuel-efficiency regulations.

"Asia Pacific dominated the regional market for engineering plastics in 2024."

Asia Pacific led the engineering plastics market in 2024 due to growing industrialization, urbanization, and automotive, electrical and electronics, construction, and machinery expansion. China, Japan, India, and South Korea benefited from abundant raw materials, cheap manufacturing, and government assistance for industrial expansion. Polyamide, PEEK, and PPS were in high demand in the automobile industry for lightweight, fuel-efficient vehicles, while the electronics industry needed thermally stable and durable materials. Advances in polymer synthesis, material modification, and precision processing further improved performance and increased applications. Stricter environmental legislation, sustainability programs, and energy efficiency goals also spurred the use of sophisticated and environmentally friendly engineering plastics. Strategic investments and partnerships between local manufacturers strengthened manufacturing capacity, product quality, and technological leadership, cementing Asia Pacific's leadership in the engineering plastics market.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Companies Covered: BASF (Germany), Covestro AG (Germany), Celanese Corporation (US), DuPont (US), Syensqo (Belgium), LG Chem (South Korea), SABIC (Saudi Arabia), Evonik Industries AG (Germany), Mitsubishi Chemical Group Corporation (Japan), and Envalior (Germany) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the engineering plastics market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the engineering plastics market based on type (acrylonitrile butadiene styrene (ABS), polyamide, polycarbonate, thermoplastic polyester (PET & PBT), polyacetal, fluoropolymer, and other types) and end-use industry (automotive & transportation, consumer appliances, electrical & electronics, industrial & machinery, packaging, and other end-use industries). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the engineering plastics market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as product launches, partnerships, collaborations, mergers, acquisitions, and expansions, associated with the engineering plastics market. This report covers a competitive analysis of upcoming startups in the engineering plastics market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall engineering plastics market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Analysis of key drivers (growing demand for engineering plastics in lightweight automotive and electric vehicle applications, growth in electronics and electrical industries, and rising adoption of polyamide (PA 11 & PA 12) in 3D printing across key industries ), restraints (fluctuating raw material prices and competition from alternative materials and limited infrastructure), opportunities (growing demand for biocompatible engineering plastics in medical devices, development of high-performance specialty grades, and increasing demand in emerging economies), and challenges (balancing performance, sustainability, and processability and global trade uncertainties).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the engineering plastics market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the engineering plastics market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the engineering plastics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as BASF (Germany), Covestro AG (Germany), Celanese Corporation (US), DuPont (US), Syensqo (Belgium), LG Chem (South Korea), SABIC (Saudi Arabia), Evonik Industries AG (Germany), Mitsubishi Chemical Group Corporation (Japan), and Envalior (Germany), among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS OF STUDY

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of interviews with experts

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 BASE NUMBER CALCULATION

- 2.3.1 DEMAND-SIDE APPROACH

- 2.3.2 SUPPLY-SIDE APPROACH

- 2.4 MARKET FORECAST APPROACH

- 2.4.1 SUPPLY SIDE

- 2.4.2 DEMAND SIDE

- 2.5 DATA TRIANGULATION

- 2.6 FACTOR ANALYSIS

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ENGINEERING PLASTICS MARKET

- 4.2 ASIA PACIFIC: ENGINEERING PLASTICS MARKET, BY END-USE INDUSTRY AND COUNTRY

- 4.3 ENGINEERING PLASTICS MARKET, BY TYPE

- 4.4 ENGINEERING PLASTICS MARKET, BY END-USE INDUSTRY

- 4.5 ENGINEERING PLASTICS MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing demand for engineering plastics in lightweight automotive and electric vehicle applications

- 5.2.1.2 Growth in electronics and electrical industries

- 5.2.1.3 Rising adoption of polyamide (PA 11 & PA 12) in 3D printing across key industries

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fluctuating raw material prices

- 5.2.2.2 Competition from alternative materials and limited infrastructure

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing demand for biocompatible engineering plastics in medical devices

- 5.2.3.2 Development of high-performance specialty grades

- 5.2.3.3 Increasing demand in emerging economies

- 5.2.4 CHALLENGES

- 5.2.4.1 Balancing performance, sustainability, and processability

- 5.2.4.2 Global trade uncertainties

- 5.2.1 DRIVERS

6 INDUSTRY TRENDS

- 6.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.2 ECOSYSTEM ANALYSIS

- 6.3 VALUE CHAIN ANALYSIS

- 6.4 TARIFF AND REGULATORY LANDSCAPE

- 6.4.1 TARIFF ANALYSIS (HS CODE: 390330)

- 6.4.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.4.3 KEY REGULATIONS

- 6.4.3.1 Automotive End-of-life vehicles (ELV) Directive 2000/53/EC

- 6.4.3.2 Food Contact Materials Regulation (EC 1935/2004)

- 6.4.3.3 Toxic Substances Control Act (TSCA)

- 6.4.3.4 CLP Regulation (EC 1272/2008)

- 6.4.3.5 ISO 9001:2015

- 6.4.3.6 ISO 14001:2015

- 6.4.3.7 ISO 14021:2016

- 6.4.3.8 BS 4994:1987

- 6.4.3.9 ASTM D6400-21

- 6.4.4 PRICING ANALYSIS

- 6.4.4.1 Pricing analysis, by product

- 6.4.4.2 Pricing analysis, by region

- 6.5 TRADE ANALYSIS

- 6.5.1 EXPORT SCENARIO (HS CODE 390330)

- 6.5.2 IMPORT SCENARIO (HS CODE 390330)

- 6.5.3 EXPORT SCENARIO (HS CODE 390810)

- 6.5.4 IMPORT SCENARIO (HS CODE 390810)

- 6.6 TECHNOLOGY ANALYSIS

- 6.6.1 KEY TECHNOLOGIES

- 6.6.1.1 Injection molding

- 6.6.1.2 Blow molding

- 6.6.1.3 Extrusion molding

- 6.6.1.4 Compression molding

- 6.6.2 COMPLEMENTARY TECHNOLOGIES

- 6.6.2.1 3D printing/Additive manufacturing

- 6.6.3 ADJACENT TECHNOLOGIES

- 6.6.3.1 Bioplastics and sustainable materials

- 6.6.1 KEY TECHNOLOGIES

- 6.7 PATENT ANALYSIS

- 6.7.1 INTRODUCTION

- 6.7.2 METHODOLOGY

- 6.7.3 PATENT ANALYSIS, 2015-2024

- 6.8 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.9 CASE STUDY ANALYSIS

- 6.9.1 TOYOTA INTRODUCES WORLD-FIRST PLASMA-COATED POLYCARBONATE WINDOW

- 6.9.2 MOLECULAR WEIGHT CHARACTERIZATION OF ENGINEERING PLASTICS USING GEL PERMEATION CHROMATOGRAPHY

- 6.9.3 INJECTION MOLDING BIOCOMPATIBLE FLUOROPOLYMERS FOR MEDICAL DEVICES

- 6.10 INVESTMENT AND FUNDING SCENARIO

- 6.11 IMPACT OF GEN AI/AI ON ENGINEERING PLASTICS MARKET

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREAT OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.13.2 BUYING CRITERIA

- 6.14 MACROECONOMIC ANALYSIS

- 6.14.1 INTRODUCTION

- 6.14.2 GDP TRENDS AND FORECASTS

- 6.15 IMPACT OF 2025 US TARIFF - ENGINEERING PLASTICS MARKET

- 6.15.1 INTRODUCTION

- 6.15.2 KEY TARIFF RATES

- 6.15.3 PRICE IMPACT ANALYSIS

- 6.15.4 IMPACT ON COUNTRY/REGION

- 6.15.4.1 US

- 6.15.4.2 China

- 6.15.4.3 India

- 6.15.5 IMPACT ON END-USE INDUSTRY

7 ENGINEERING PLASTICS MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 ACRYLONITRILE BUTADIENE STYRENE

- 7.2.1 VERSATILITY TO DRIVE ADOPTION

- 7.3 POLYAMIDE

- 7.3.1 SUPERIOR MECHANICAL STRENGTH AND DURABILITY TO DRIVE DEMAND

- 7.3.2 NYLON FOR UNDER-THE-HOOD APPLICATIONS

- 7.4 POLYCARBONATE

- 7.4.1 HIGH IMPACT RESISTANCE AND TRANSPARENCY TO DRIVING DEMAND

- 7.5 THERMOPLASTIC POLYESTER

- 7.5.1 CHEMICAL RESISTANCE AND DIMENSIONAL STABILITY TO SUPPORT MARKET GROWTH

- 7.6 POLYACETAL

- 7.6.1 LOW FRICTION AND WEAR RESISTANCE TO SUPPORTING ADOPTION

- 7.7 FLUOROPOLYMER

- 7.7.1 RISING USE IN AUTOMOTIVE AND AEROSPACE APPLICATIONS TO FUEL MARKET GROWTH

- 7.8 OTHER TYPES

8 ENGINEERING PLASTICS MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- 8.2 AUTOMOTIVE & TRANSPORTATION

- 8.2.1 LIGHTWEIGHTING AND FUEL EFFICIENCY TO DRIVE ADOPTION

- 8.2.2 INTERIOR

- 8.2.3 EXTERIOR

- 8.2.4 POWER TRAIN

- 8.2.5 UNDER-THE-HOOD APPLICATIONS

- 8.3 CONSUMER APPLIANCES

- 8.3.1 DESIGN FLEXIBILITY AND AESTHETIC APPEAL TO PROPEL MARKET

- 8.3.2 AIR CONDITIONERS

- 8.3.3 MOBILES AND COMPUTERS

- 8.3.4 TELEVISION AND MUSIC PLAYERS

- 8.4 ELECTRICAL & ELECTRONICS

- 8.4.1 ELECTRICAL INSULATION AND DIELECTRIC STRENGTH TO DRIVE ADOPTION

- 8.4.2 SEMICONDUCTORS

- 8.4.3 SOCKETS & SWITCHES

- 8.5 INDUSTRIAL & MACHINERY

- 8.5.1 HIGH STRENGTH AND WEAR RESISTANCE TO DRIVE ADOPTION

- 8.5.2 POWER TOOLS

- 8.6 PACKAGING

- 8.6.1 CHEMICAL RESISTANCE TO DRIVE ADOPTION

- 8.6.2 FOOD PACKAGING

- 8.6.3 MEDICAL PACKAGING

- 8.7 OTHER END-USE INDUSTRIES

- 8.7.1 MEDICAL

- 8.7.2 CONSTRUCTION

9 ENGINEERING PLASTICS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 ASIA PACIFIC

- 9.2.1 CHINA

- 9.2.1.1 Rising disposable incomes, urbanization, and industrial modernization to drive market

- 9.2.2 INDIA

- 9.2.2.1 Rapid adoption of consumer electronics, smart devices, and renewable energy solutions to drive market

- 9.2.3 JAPAN

- 9.2.3.1 Technological advancements and sustainability initiatives to support market growth

- 9.2.4 SOUTH KOREA

- 9.2.4.1 Robust automotive and electronics industries to drive demand

- 9.2.5 TAIWAN

- 9.2.5.1 Strong industrial and automotive base to support market growth

- 9.2.6 INDONESIA

- 9.2.6.1 Industrial growth and rise in vehicle production to drive demand

- 9.2.7 REST OF ASIA PACIFIC

- 9.2.1 CHINA

- 9.3 EUROPE

- 9.3.1 GERMANY

- 9.3.1.1 Advanced automotive sector to propel market

- 9.3.2 FRANCE

- 9.3.2.1 Government incentives, supportive policies, and investments in EV infrastructure to drive market

- 9.3.3 ITALY

- 9.3.3.1 Sustainable mobility and advanced manufacturing to fuel demand

- 9.3.4 RUSSIA

- 9.3.4.1 Rising vehicle production and arms exports to drive market

- 9.3.5 UK

- 9.3.5.1 Industrial diversification and sustainability initiatives to boost market growth

- 9.3.6 REST OF EUROPE

- 9.3.1 GERMANY

- 9.4 NORTH AMERICA

- 9.4.1 US

- 9.4.1.1 Strong industrial base and stringent environmental regulations to drive market

- 9.4.2 CANADA

- 9.4.2.1 Sustainability initiatives and technological advancements to boost demand

- 9.4.3 MEXICO

- 9.4.3.1 EV adoption and industrial development to boost demand for engineering plastics

- 9.4.1 US

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.5.1.1 Saudi Arabia

- 9.5.1.1.1 Industrial diversification and automotive growth to drive market

- 9.5.1.2 UAE

- 9.5.1.2.1 Expanding manufacturing base to drive market

- 9.5.1.3 Rest of GCC Countries

- 9.5.1.1 Saudi Arabia

- 9.5.2 SOUTH AFRICA

- 9.5.2.1 Growth in vehicle production to fuel demand

- 9.5.3 REST OF MIDDLE EAST & AFRICA

- 9.5.1 GCC COUNTRIES

- 9.6 SOUTH AMERICA

- 9.6.1 BRAZIL

- 9.6.1.1 Government incentives and industrial growth to boost demand

- 9.6.2 ARGENTINA

- 9.6.2.1 Industrial expansion to drive demand

- 9.6.3 REST OF SOUTH AMERICA

- 9.6.1 BRAZIL

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES

- 10.3 MARKET SHARE ANALYSIS

- 10.4 REVENUE ANALYSIS

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 PRODUCT/BRAND COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 Type footprint

- 10.7.5.4 End-use industry footprint

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.8.5.1 Detailed list of key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 BASF

- 11.1.1.1 Business overview

- 11.1.1.2 Products offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches

- 11.1.1.3.2 Deals

- 11.1.1.3.3 Expansions

- 11.1.1.4 MnM view

- 11.1.1.4.1 Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses & competitive threats

- 11.1.2 COVESTRO AG

- 11.1.2.1 Business overview

- 11.1.2.2 Products offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches

- 11.1.2.3.2 Expansions

- 11.1.2.4 MnM view

- 11.1.2.4.1 Right to win

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses & competitive threats

- 11.1.3 CELANESE CORPORATION

- 11.1.3.1 Business overview

- 11.1.3.2 Products offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Product launches

- 11.1.3.3.2 Deals

- 11.1.3.3.3 Expansions

- 11.1.3.4 MnM view

- 11.1.3.4.1 Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses & competitive threats

- 11.1.4 DUPONT

- 11.1.4.1 Business overview

- 11.1.4.2 Products offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Deals

- 11.1.4.3.2 Expansions

- 11.1.4.4 MnM view

- 11.1.4.4.1 Right to win

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses & competitive threats

- 11.1.5 SYENSQO

- 11.1.5.1 Business overview

- 11.1.5.2 Products offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Product launches

- 11.1.5.3.2 Deals

- 11.1.5.3.3 Expansions

- 11.1.5.4 MnM view

- 11.1.5.4.1 Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses & competitive threats

- 11.1.6 LG CHEM

- 11.1.6.1 Business overview

- 11.1.6.2 Products offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Expansions

- 11.1.6.4 MnM view

- 11.1.7 SABIC

- 11.1.7.1 Business overview

- 11.1.7.2 Products offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Product launches

- 11.1.7.3.2 Expansions

- 11.1.7.4 MnM view

- 11.1.8 EVONIK INDUSTRIES AG

- 11.1.8.1 Business overview

- 11.1.8.2 Products offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Product launches

- 11.1.8.3.2 Deals

- 11.1.8.3.3 Expansions

- 11.1.8.4 MnM view

- 11.1.9 MITSUBISHI CHEMICAL GROUP CORPORATION

- 11.1.9.1 Business overview

- 11.1.9.2 Products offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches

- 11.1.9.3.2 Expansions

- 11.1.9.4 MnM view

- 11.1.10 ENVALIOR

- 11.1.10.1 Business overview

- 11.1.10.2 Products offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Product launches

- 11.1.10.3.2 Expansions

- 11.1.10.4 MnM view

- 11.1.1 BASF

- 11.2 OTHER PLAYERS

- 11.2.1 KINGFA SCI.&TECH. CO.,LTD.

- 11.2.2 ASAHI KASEI CORPORATION

- 11.2.3 ARKEMA

- 11.2.4 EASTMAN CHEMICAL COMPANY

- 11.2.5 CHIMEI

- 11.2.6 DAICEL CORPORATION

- 11.2.7 ADVANSIX

- 11.2.8 ROCHLING

- 11.2.9 TRINSEO

- 11.2.10 GRAND PACIFIC PETROCHEMICAL CORPORATION

- 11.2.11 GUANGDONG ENGINEERING PLASTICS INDUSTRIES (GROUP) CO., LTD.

- 11.2.12 ESTER INDUSTRIES LIMITED

- 11.2.13 ENSINGER

- 11.2.14 APPL INDUSTRIES LIMITED

- 11.2.15 PAR GROUP

- 11.2.16 HITEMP POLYMERS PVT. LTD.

- 11.2.17 SIMONA PMC

12 ADJACENT & RELATED MARKET

- 12.1 INTRODUCTION

- 12.2 LIMITATIONS

- 12.2.1 POLYAMIDE MARKET

- 12.2.1.1 Market definition

- 12.2.1.2 Polyamide market, by type

- 12.2.1.3 Polyamide market, by application

- 12.2.1.4 Polyamide market, by region

- 12.2.1 POLYAMIDE MARKET

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS