|

시장보고서

상품코드

1923694

저전압 직류 차단기 시장 : 유형별, 전압별, 차단 기구별, 최종 사용별, 지역별 예측(-2030년)Low Voltage DC Circuit Breaker Market by Voltage (Below 60V, 60V-120V, 120V-380V, 380V-1.5kV), Type (Air, Molded Case, Others), Breaking Mechanism (Solid-state, Hybrid, Mechanical), End User, and Region - Global Forecast to 2030 |

||||||

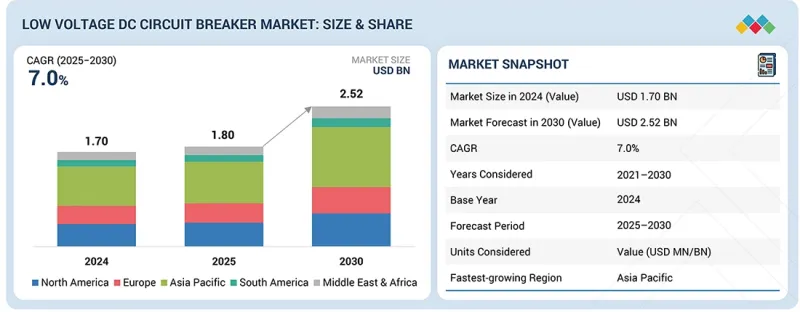

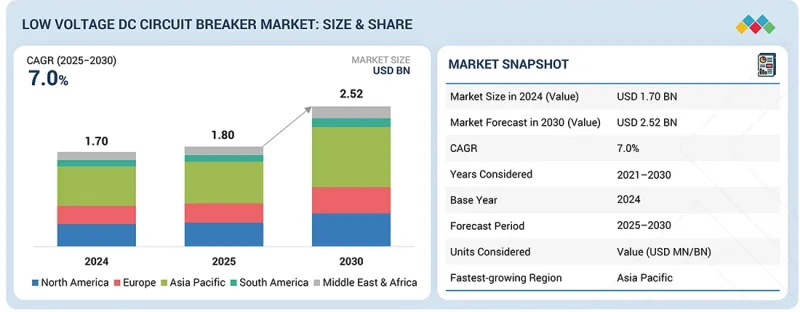

세계의 저전압 직류 차단기 시장 규모는 2025년 18억 달러로 평가되었고, 2030년 25억 2,000만 달러에 이를 것으로 보이며, 예측 기간 동안 CAGR은 7.0%를 나타낼 전망입니다.

저전압 직류 회로 차단기 채택을 촉진하는 주요 요인 중 하나는 에너지, 모빌리티 및 디지털 분야에서 직류 기반 전력 시스템의 도입이 증가하고 있기 때문입니다. 태양광 PV, BESS(배터리 에너지 저장 시스템), EV 충전소 및 데이터 센터의 채택 증가로 인해 높은 효율성과 신뢰성을 제공하는 DC 전력 보호 솔루션에 대한 수요가 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 가치(100만/10억 달러) |

| 부문 | 유형별, 전압별, 차단 기구별, 최종 사용별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동, 아프리카, 남미 |

DC 전력 시스템은 AC 시스템과 달리 자연적인 제로 크로싱 포인트 없이 전류가 지속적으로 흐르는 등 특정 한계가 있어 DC 회로 차단기가 필수적입니다. 전 세계 정부는 재생 에너지 채택 촉진을 위해 저전압 직류 회로 차단기에 대한 수요를 지속적으로 확대하고 있습니다. 또한 산업계가 운영 효율성 증대를 위한 노력을 지속함에 따라 저전압 직류 회로 차단기에 대한 수요는 과소평가할 수 없습니다. 상업, 통신 및 산업 분야의 직류 마이크로그리드는 저전압 직류 회로 차단기에 대한 수요를 지속적으로 보완하고 있습니다.

몰드 케이스 회로 차단기(MCCB)는 적응성, 높은 정격 전류, 우수한 보호 메커니즘 덕분에 예측 기간 동안 저전압 DC 회로 차단기 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. MCCB는 태양광 PV 시스템, 배터리 저장 솔루션, 전기차 충전소, 산업용 DC 전력 분배 시스템 등 고정격 전류과 신뢰성 있는 고장 스위칭이 필요한 다양한 분야에 적용됩니다. MC 시리즈 차단기에 비해 성형 케이스 차단기는 조정 가능하며, 향상된 열적 및 자기적 보호 기능과 진보된 아크 소멸 특성을 제공하여 DC 시스템에 적합합니다. 380-1.5kVDC의 높은 전압 범위 내에서 효율적으로 작동하는 능력은 MCCB 채택을 더욱 촉진합니다. 또한 MCCB는 일반적으로 개폐기 및 전력 전력 분배반 내에 사용되어 소비자가 시스템을 설계하고 유지 관리하기 쉽게 합니다. 이러한 이점들로 인해 MCCB는 대규모 및 중요한 DC 응용 시스템에 선호됩니다.

배터리 에너지 저장 시스템(BESS)은 현대 전력 시스템의 전력 분배 안정화에 필수적인 역할을 수행함에 따라, 예측 기간 동안 저전압 직류 회로 차단기 시장에서 두 번째로 큰 시장 점유율을 차지할 것으로 예상됩니다. 전력망, 상업 및 주거 프로젝트 적용을 위한 BESS 구축이 전 세계적으로 확대되고 있습니다. 배터리 에너지는 본질적으로 직류로 작동하므로, 배터리 스트링, 인버터 또는 직류 버스를 오작동, 과부하 또는 단락으로부터 보호하기 위해 저전압 직류 회로 차단기의 사용이 필수적입니다. 태양광 저장 프로젝트, 전기차 충전소 또는 마이크로그리드에 사용되는 리튬이온 배터리 에너지 저장 솔루션의 증가가 DC 회로 차단기 수요에 크게 기여했습니다. 또한 열폭주 및 고고장 전류와 관련된 문제로 인해 시스템 통합업체들은 고품질 DC 보호 솔루션을 선택해야 했습니다.

중국은 재생 에너지, 전기차, 스마트 그리드 현대화에 대한 막대한 투자로 인해 아시아태평양 저전압 DC 회로 차단기 시장의 선두 주자로 부상할 것입니다. 중국은 전 세계 태양광 PV 에너지 저장 시스템 설치량의 상당 부분을 차지합니다. 이러한 분야들은 주로 방대한 양의 DC 전력을 사용하므로 중국에서 저전압 DC 회로 차단기에 대한 막대한 수요가 발생할 것입니다. 또한 중국에서 스마트 그리드 및 전기차와 같은 청정 에너지 기술에 대한 대규모 지원은 아시아태평양 시장에서 저전압 DC 회로 차단기에 대한 엄청난 수요를 촉진합니다. 더불어 중국은 전기 장치에 대한 잘 발달된 제조 인프라를 보유하고 있어 아시아태평양 시장에서 저전압 DC 회로 차단기의 대량 생산이 용이합니다.

세계의 저전압 직류 차단기 시장은 광범위한 지역적 입지를 확보하고 다양한 제품군을 제공하는 주요 업체들이 주도하고 있습니다. 저전압 DC 회로 차단기 시장의 선도 기업으로는 ABB, 지멘스, 슈나이더 일렉트릭, 이튼, 미쓰비시 전기 등이 있습니다. 이들 기업은 시장 지위 강화를 위해 제품 혁신, 인수합병, 계약 체결, 사업 확장 등의 전략에 주력하고 있습니다. 신제품 출시와 전략적 접근은 변화하는 시장 환경에서 경쟁 우위를 유지하기 위해 이들 기업이 채택하는 핵심 전략입니다.

조사 범위

본 보고서에서는 저전압 직류 차단기 시장을 유형별, 전압별, 차단 기구별, 최종 사용자별, 지역별로 부문화하여 예측을 실시합니다. 또한 시장과 관련된 촉진요인, 억제요인, 기회, 과제에 대해서도 고찰합니다. 북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카(MEA)의 3대 지역에서 시장에 대한 상세한 분석을 제공합니다. 주요 진출기업의 밸류체인 분석 및 저전압 직류 차단기 생태계 분석도 포함되어 있습니다.

이 보고서 구매의 주요 이점

- 주요 촉진요인 분석(배터리 에너지 저장 시스템(BESS)의 급속한 성장, 모든 규모에 걸친 태양광 PV 보급 가속화, 전기차(EV) 급속 충전 인프라 확장), 억제요인(표준의 분산 및 상호 운용성 부족, DC 아크 차단 기술의 높은 비용 및 기술적 복잡성), 기회(하이브리드 및 솔리드 스테이트 DC 차단기 채택 증가, 유틸리티 규모 태양광 및 에너지 저장 통합으로 인한 고급 DC 보호 수요 촉진, 신흥 380VDC 데이터 센터 아키텍처로 인한 고부가가치 수요 창출), 과제(소형 PV 및 주거용 ESS 부문의 가격 민감도, PV, BESS 및 EV OEM과의 긴 인증 주기)를 분석하여 성장에 영향을 미치는 요인을 밝힙니다.

- 제품, 솔루션, 서비스 개발/이노베이션 : 저전압 직류 차단기 시장에 있어서의 미래 기술 동향, 연구 개발 활동에 관한 상세한 인사이트

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보 -이 보고서는 다양한 지역의 저전압 DC 차단기 시장을 분석합니다.

- 시장 다양화 : 미개척 지역의 새로운 반도체 제조 장치, 저전압 직류 차단기 시장의 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁 평가 : AABB, Siemens, Schneider Electric, Eaton, MITSUBHI ELECTRIC CORPORATION 등 주요 업체들의 시장 점유율, 성장 전략, 제공 제품에 대한 자세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 미충족 요구와 공백

- 상호연결된 시장과 분야간 기회

- 새로운 비즈니스 모델과 생태계의 변화

- Tier 1/2/3 참가 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 주요 컨퍼런스 및 이벤트(2026년)

- 고객사업에 영향을 주는 동향/혼란

- 사례 연구 분석

- 미국 관세의 영향(2025년) - 저전압 직류(DC) 차단기 시장

제6장 기술의 진보, AI별 영향, 특허, 혁신 및 미래의 응용

- 주요 신기술

- 보완적 기술

- 인접 기술

- 기술/제품 로드맵

- 특허 분석

- 미래의 응용

- AI/생성형 AI가 저전압 직류 차단기 시장에 미치는 영향

제7장 규제 상황과 지속가능성에 관한 대처

- 지역 규제 및 규정 준수

- 지속가능성에 대한 노력

- 규제 정책이 지속가능성 이니셔티브에 미치는 영향

- 인증, 라벨, 환경 기준

제8장 고객 환경 및 구매행동

- 의사결정 공정

- 구매 공정와 평가 기준에 관련된 주요 이해관계자

- 채택 장벽과 내부 과제

- 다양한 최종 사용의 미충족 요구

- 시장 수익성

제9장 저전압 직류 차단기 시장(유형별)

- 에어 회로 차단기

- 몰드 케이스 회로 차단기

- 기타

제10장 저전압 직류 차단기 시장(전압별)

- 60V 미만

- 60-120V

- 121-380V

- 381-1.5KV

제11장 저전압 직류 차단기 시장(차단 기구별)

- 솔리드 스테이트

- 하이브리드

- 기계

제12장 저전압 직류 차단기 시장(최종 사용별)

- 배터리 에너지 저장 시스템

- 데이터 센터

- 태양광 발전소

- EV 급속 충전 인프라

- 철도 및 지하철

- 산업

- 상업시설 및 주택

제13장 데이터센터용 저전압 직류 차단기 시장(전압별)

- 60V 미만

- 60-120V

- 121-380V

- 381-1.5KV

제14장 저전압 DC 회로 시장(지역별)

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 러시아

- 이탈리아

- 프랑스

- 기타

- 아시아태평양

- 중국

- 인도

- 한국

- 일본

- 기타

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타

제15장 경쟁 구도

- 개요

- 주요 참가 기업의 전략, 강점(2022-2025년)

- 수익 분석(2020-2024년)

- 시장 점유율 분석(2024년)

- 기업평가와 재무재표

- 브랜드 비교

- 기업평가 매트릭스 : 주요 진입기업(2024년)

- 기업평가 매트릭스 : 스타트업, 중소기업(2024년)

- 경쟁 시나리오

제16장 기업 프로파일

- 주요 진출기업

- ABB

- EATON

- SCHNEIDER ELECTRIC

- SIEMENS

- MITSUBISHI ELECTRIC CORPORATION

- LS ELECTRIC CO., LTD.

- CHINT GROUP

- FUJI ELECTRIC CO., LTD.

- ROCKWELL AUTOMATION

- BENY

- LEGRAND

- SECHERON

- CARLING TECHNOLOGIES

- CNC ELECTRIC GROUP CO., LTD.

- ONCCY ELECTRICAL CO., LTD

- 기타 기업

- ENTEC ELECTRIC & ELECTRONIC

- ZHEJIANG AITE ELECTRIC TECHNOLOGY CO., LTD.

- MYERS POWER PRODUCTS, INC.

- NADER

- LETOP

- WENZHOU ZHECHI ELECTRIC CO., LTD.

- ZHEJIANG DABO ELECTRIC CO., LTD.

- IGOYE SOLAR POWER SYSTEM

- GEYA ELECTRICAL EQUIPMENT SUPPLY

- ZHEJIANG GRL ELECTRIC CO., LTD.

제17장 조사 방법

제18장 부록

HBR 26.02.19The global low voltage DC circuit breaker market is expected to reach USD 1.80 billion in 2025 and USD 2.52 billion by 2030, exhibiting a CAGR of 7.0% during the forecast period. One key reason propelling the adoption of low voltage DC circuit breakers is the increasing adoption of DC-based power systems in the energy, mobility, and digital space. The increasing adoption of solar PV, BESS, EV charging stations, and data centers has resulted in growing demand for DC power protection solutions that offer high efficiency and reliability.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Low voltage DC circuit breaker Market by type, voltage, breaking mechanism, end user, and region. |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa and South America |

DC power systems, unlike their counterparts in the AC system, have certain limitations, including uninterrupted current flow with no natural zero crossing points, thereby making DC circuit breakers indispensable. Governments around the world, in their efforts to promote the adoption of renewable energy, continue to augment the demand for low voltage DC circuit breakers. Additionally, with industries continuing their efforts towards increasing the efficiency of their operations, the demand for low voltage DC circuit breakers cannot be overstated. DC microgrids in the commercial, telecom, and industrial space continue to supplement the demand for low voltage DC circuit breakers..

"Molded case circuit breaker in the type segment are expected to hold largest market share in the low voltage DC circuit breaker market during the forecast period"

Molded case circuit breakers (MCCBs) are anticipated to occupy the largest share of the low voltage DC circuit breaker market during the forecast period because of their adaptability, high current rating, and excellent protection mechanisms. MCCBs are applied in various applications like solar PV systems, battery storage solutions, electric vehicle charging stations, and industrial DC distribution systems, where high current ratings and reliable switching of faults are necessary. Compared to MC series circuit breakers, molded case circuit breakers are adjustable, providing improved thermal and magnetic protections along with advanced arc extinguishing properties, making them appropriate for DC systems. Their ability to work efficiently within a high voltage range of 380-1.5kVDC further aids in the adoption of MCCBs. Moreover, MCCBs are generally used within switchgear and-power distribution boards, making it simpler for consumers to design and maintain the system. MCCBs are preferred for large-scale and critical DC application systems because of such benefits.

"Battery energy storage systems in the end user segment to hold second largest market share in the low voltage DC circuit breaker market during the forecast period"

Battery energy storage systems are anticipated to have the second-largest market share in the market for low-voltage DC circuit breakers during the forecast period, owing to the indispensable role of BESS in stabilizing the power distribution of the modern power system. BESS deployment has escalated globally for its application in grids, commercial, and residential projects. Since battery energy inherently works on DC, the use of LV DC circuit breakers has become essential for securing battery strings, inverters, or DC buses against malfunctions, overload, or short circuits. Rising lithium-ion battery energy storage solutions used for solar storage projects, electric vehicle charging stations, or microgrids have contributed considerably to the demand for DC circuit breakers. Moreover, issues regarding thermal runaways and high fault currents have compelled system integrators to choose high-quality DC protection solutions..

"China is likely to dominate the Asia Pacific low voltage DC circuit breaker market during the forecast period"

China would emerge as a leader in the Asia Pacific market for low voltage DC circuit breakers on account of its vast investments in renewable energy, electric vehicles, and smart grid modernization. China accounts for a massive share of global installations in solar PV energy storage systems in the world. These sectors primarily employ vast capacities of DC power, making way for a massive demand for low voltage DC circuit breakers in China. Moreover, massive support for clean energy technologies such as smart grids and electric vehicles in China fuels a huge demand for low voltage DC circuit breakers in the APAC market. Additionally, China has a well-developed manufacturing infrastructure for electrical devices, making it simpler for low voltage DC circuit breakers to be mass-produced in the APAC market.

Breakdown of Primaries

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the biorefinery market.

By Company Type: Tier 1- 65%, Tier 2- 24%, and Tier 3- 11%

By Designation: C-level Executives - 30%, Director Level- 25%, and Others- 45%

By Region: North America - 27%, Europe - 20%, Asia Pacific - 33%, South America - 12%, Middle East & Africa - 8%

Note: Other designations include sales managers, engineers, and regional managers.

Note: tier 1 company-revenue >USD 5 billion, tier 2 company-revenue between USD 1 and USD 5 billion, and tier 3 company-revenue <USD 1 billion.

The global low voltage DC circuit breaker market is dominated by key players that hold a wide regional presence and offer a diverse range of products. Leading companies in the low voltage DC circuit breaker market include ABB, Siemens, Schneider Electric, Eaton, and MITSUBHI ELECTRIC CORPORATION among others. These players focus on strategies such as product innovations, acquisitions, contracts, and expansions to strengthen their market position. New product launches, coupled with strategic, are key approaches adopted by these companies to maintain competitive advantages in the evolving market landscape.

Study Coverage

The report segments the low voltage DC circuit breaker market and forecasts in by type, voltage, breaking mechanism, end user and region. The report also discusses the drivers, restraints, opportunities, and challenges pertaining to the market. It gives a detailed view of the market across three main regions-North America, Europe, Asia Pacific, South America and MEA. The report includes a value chain analysis of the key players and their competitive analysis of the low voltage DC circuit breaker ecosystem.

Key Benefits of Buying the Report

- Analysis of key drivers (Rapid Growth in Battery Energy Storage Systems (BESS), Accelerated Solar PV Deployment Across All Scales, Expansion of EV Fast-Charging Infrastructure), restraints (Fragmented Standards and Lack of Interoperability, Higher Cost and Technical Complexity of DC Arc Interruption ) opportunities (Growing Adoption of Hybrid and Solid-State DC Breakers, Utility-Scale Solar and Energy Storage Integration Driving Advanced DC Protection Demand, Emerging 380 VDC Data Center Architectures Creating High-Value Demand ), and challenges (Price Sensitivity in Small PV and Residential ESS Segments, Long Qualification Cycles with PV, BESS, and EV OEMs ) influencing the growth.

- Products/Solution/Service Development/Innovation: Detailed insights into upcoming technologies, research, and development activities in the low voltage DC circuit breaker market

- Market Development: Comprehensive information about lucrative markets-the report analyses the low voltage DC circuit breaker market across varied regions.

- Market Diversification: Exhaustive information about new semiconductor manufacturing equipment in untapped geographies, recent developments, and investments in the low voltage DC circuit breaker market

- Competitive Assessment: In-depth assessment of market shares and growth strategies and offerings of leading players, such as ABB, Siemens, Schneider Electric, Eaton, and MITSUBHI ELECTRIC CORPORATION among others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN LOW-VOLTAGE DC CIRCUIT BREAKER MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN LOW-VOLTAGE DC CIRCUIT BREAKER MARKET

- 3.2 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY REGION

- 3.3 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY VOLTAGE

- 3.4 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY BREAKING MECHANISM

- 3.5 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY TYPE

- 3.6 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY END USE

- 3.7 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET IN ASIA PACIFIC, BY END USE AND COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Mounting deployment of battery energy storage systems (BESS)

- 4.2.1.2 Increasing installation of solar photovoltaic (PV) systems

- 4.2.1.3 Rapid expansion of EV fast-charging infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 Lack of DC protection standards and production issues

- 4.2.2.2 High costs resulting from technical complexities

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing popularity of hybrid and solid-state DC circuit breakers

- 4.2.3.2 Increasing co-located utility-scale solar PV and BESS projects

- 4.2.3.3 Shifting preference toward 800 VDC power distribution in data centers

- 4.2.4 CHALLENGES

- 4.2.4.1 Price sensitivity in small PV and residential ESS segments

- 4.2.4.2 Long qualification cycles with PV, BESS, and EV OEMs

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 THREATS OF SUBSTITUTES

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN SOLAR PV PLANT INDUSTRY

- 5.2.4 TRENDS IN BATTERY ENERGY STORAGE SYSTEM (BESS) INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF LOW-VOLTAGE DC CIRCUIT BREAKERS, BY VOLTAGE, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF LOW-VOLTAGE DC CIRCUIT BREAKERS, BY REGION, 2021-2024

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 853690)

- 5.6.2 EXPORT SCENARIO (HS CODE 853690)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 EATON'S PVGARD DC MOLDED CASE CIRCUIT BREAKERS HELP COMPLY WITH SAFETY STANDARDS IN SOLAR AND STORAGE SITES

- 5.9.2 ABB'S LV-DC BREAKERS IMPROVE FAULT DETECTION IN INDUSTRIAL PLANTS AND TELECOM FACILITIES

- 5.9.3 IGBT-BASED LV SOLID-STATE DC CIRCUIT BREAKER (SSCB) ENHANCES DC MICROGRID RELIABILITY AND SAFETY

- 5.10 IMPACT OF 2025 US TARIFF - LOW-VOLTAGE DC CIRCUIT BREAKER MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON TYPES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 DC ARC INTERRUPTION AND QUENCHING TECHNOLOGY

- 6.1.2 THERMAL-MAGNETIC AND ELECTRONIC TRIP UNITS (DC-TUNED)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ELECTRONIC AND MICROPROCESSOR-BASED PROTECTION UNITS

- 6.2.2 BIDIRECTIONAL DC INTERRUPTION DESIGN

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 DC POWER CONVERSION SYSTEMS

- 6.3.2 DC MICROGRIDS AND RENEWABLE DC NETWORKS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | DIGITAL & ECO-DESIGN FOUNDATION

- 6.4.2 MID-TERM (2027-2030) | GRID MODERNIZATION & SYSTEM INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | AUTONOMOUS, GRID-INTERACTIVE PROTECTION

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON LOW-VOLTAGE DC CIRCUIT BREAKER MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY OEMS IN LOW-VOLTAGE DC CIRCUIT BREAKER MARKET

- 6.7.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN LOW-VOLTAGE DC CIRCUIT BREAKER MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GEN AI/AI-INTEGRATED LOW-VOLTAGE DC CIRCUIT BREAKERS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF MEDIUM FREQUENCY MAGNETICS

- 7.3 IMPACT OF REGULATORY POLICY ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USES

- 8.5 MARKET PROFITABILITY

9 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 AIR CIRCUIT BREAKERS

- 9.2.1 LARGE-SCALE ELECTRIFICATION AND ENERGY STORAGE PROJECTS TO BOOST SEGMENTAL GROWTH

- 9.3 MOLDED CASE CIRCUIT BREAKERS

- 9.3.1 ABILITY TO ENHANCE SAFETY WHILE ENABLING RELIABLE INTERRUPTION TO EXPEDITE SEGMENTAL GROWTH

- 9.4 OTHERS

10 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY VOLTAGE

- 10.1 INTRODUCTION

- 10.2 BELOW 60 V

- 10.2.1 USAGE TO MINIMIZE ELECTRICAL SHOCK RISK AND ENSURE BASIC FAULT PROTECTION TO FOSTER SEGMENTAL GROWTH

- 10.3 60-120 V

- 10.3.1 RELIABLE INTERRUPTION AND COMPACT FORM FACTORS FOR SPACE-CONSTRAINED INSTALLATIONS TO SPUR DEMAND

- 10.4 121-380 V

- 10.4.1 IMPROVED EFFICIENCY AND REDUCED CURRENT LOSSES TO CONTRIBUTE TO SEGMENTAL GROWTH

- 10.5 381 V-1.5 KV

- 10.5.1 ABILITY TO REDUCE CURRENT FLOW, IMPROVE OVERALL SYSTEM EFFICIENCY, AND LOWER CABLING COSTS TO DRIVE MARKET

11 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY BREAKING MECHANISM

- 11.1 INTRODUCTION

- 11.2 SOLID-STATE

- 11.2.1 INCREASING USE IN DIGITALLY CONTROLLED AND HIGH-AVAILABILITY ENVIRONMENTS TO BOLSTER SEGMENTAL GROWTH

- 11.3 HYBRID

- 11.3.1 ABILITY TO DELIVER FAST RESPONSE WITHOUT FULL RELIANCE ON SEMICONDUCTORS TO FUEL SEGMENTAL GROWTH

- 11.4 MECHANICAL

- 11.4.1 PROVEN DESIGN, EASE OF INSTALLATION, AND STRAIGHTFORWARD OPERATION TO AUGMENT SEGMENTAL GROWTH

12 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET, BY END USE

- 12.1 INTRODUCTION

- 12.2 BATTERY ENERGY STORAGE SYSTEMS

- 12.2.1 FOCUS ON COMPLIANCE WITH EVOLVING FIRE SAFETY AND GRID INTERCONNECTION STANDARDS TO DRIVE MARKET

- 12.3 DATA CENTERS

- 12.3.1 EXPANSION OF HYPERSCALE AND COLOCATION CENTERS TO ACCELERATE SEGMENTAL GROWTH

- 12.4 SOLAR PV PLANTS

- 12.4.1 TRANSITION TOWARD HIGHER-CAPACITY CLEAN ENERGY INSTALLATIONS TO FOSTER SEGMENTAL GROWTH

- 12.5 EV FAST-CHARGING INFRASTRUCTURE

- 12.5.1 NEED TO INTERRUPT STEEP FAULT CURRENTS QUICKLY AND SAFELY TO BOOST SEGMENTAL GROWTH

- 12.6 RAIL TRANSIT & METRO

- 12.6.1 FOCUS ON ENSURING SAFE POWER DISTRIBUTION AND MINIMIZING SERVICE DISRUPTIONS TO EXPEDITE SEGMENTAL GROWTH

- 12.7 INDUSTRIAL

- 12.7.1 EMPHASIS ON PROTECTING SENSITIVE EQUIPMENT FROM ELECTRICAL FAULTS TO BOLSTER SEGMENTAL GROWTH

- 12.8 COMMERCIAL & RESIDENTIAL

- 12.8.1 NEED FOR SAFE INTEGRATION OF DECENTRALIZED ENERGY SYSTEMS TO CONTRIBUTE TO SEGMENTAL GROWTH

13 LOW-VOLTAGE DC CIRCUIT BREAKER MARKET FOR DATA CENTERS, BY VOLTAGE

- 13.1 INTRODUCTION

- 13.2 BELOW 60 V

- 13.2.1 INCREASING AUTOMATION AND DIGITALIZATION OF DATA CENTER OPERATIONS TO FUEL SEGMENTAL GROWTH

- 13.3 60-120 V

- 13.3.1 RISING DEPLOYMENT OF AI SERVERS, HIGH-PERFORMANCE COMPUTING CLUSTERS, AND CLOUD INFRASTRUCTURE TO DRIVE MARKET

- 13.4 121-380 V

- 13.4.1 MOUNTING ADOPTION IN HYPERSCALE AND LARGE COLOCATION DATA CENTERS TO AUGMENT SEGMENTAL GROWTH

- 13.5 381 V-1.5 KV

- 13.5.1 TRANSFORMATION OF HYPERSCALE OPERATORS FROM PILOT IMPLEMENTATIONS TO BROADER ROLLOUTS TO SPUR DEMAND

14 LOW-VOLTAGE DC CIRCUIT MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Large-scale electrification across transportation, energy, and digital infrastructure to expedite market growth

- 14.2.2 CANADA

- 14.2.2.1 Strong commitment to clean energy and electrified transportation to bolster market growth

- 14.2.3 MEXICO

- 14.2.3.1 Increasing EV manufacturing and renewable energy deployment to accelerate market growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Renewable energy transition and industrial electrification to expedite market growth

- 14.3.2 UK

- 14.3.2.1 Push toward digital infrastructure, smart grids, and renewable integration to drive market

- 14.3.3 RUSSIA

- 14.3.3.1 Infrastructure modernization and gradual electrification initiatives to accelerate market growth

- 14.3.4 ITALY

- 14.3.4.1 Increasing solar PV deployment and energy storage investments to fuel market growth

- 14.3.5 FRANCE

- 14.3.5.1 Renewable energy expansion and electrification policies to contribute to market growth

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Mounting demand for battery energy storage systems (BESS) to bolster market growth

- 14.4.2 INDIA

- 14.4.2.1 Grid modernization and data center development to expedite market growth

- 14.4.3 SOUTH KOREA

- 14.4.3.1 Industrial automation and energy storage system adoption to augment market growth

- 14.4.4 JAPAN

- 14.4.4.1 Strong emphasis on smart grid resilience to accelerate market growth

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.5.1.1 Saudi Arabia

- 14.5.1.1.1 Growing emphasis on renewable energy expansion and electrification strategies to support market growth

- 14.5.1.2 UAE

- 14.5.1.2.1 Substantial clean energy commitments to contribute to market growth

- 14.5.1.3 Rest of GCC

- 14.5.1.1 Saudi Arabia

- 14.5.2 SOUTH AFRICA

- 14.5.2.1 Rising integration of utility-scale and commercial PV systems to bolster market growth

- 14.5.3 REST OF MIDDLE EAST & AFRICA

- 14.5.1 GCC

- 14.6 SOUTH AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 High investment in distributed and utility-scale PV projects to support market growth

- 14.6.2 ARGENTINA

- 14.6.2.1 Strong focus on stabilizing national grid and reducing dependence on fossil fuels to boost market growth

- 14.6.3 CHILE

- 14.6.3.1 Rising renewable capacity additions to accelerate market growth

- 14.6.4 REST OF SOUTH AMERICA

- 14.6.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 15.3 REVENUE ANALYSIS, 2020-2024

- 15.4 MARKET SHARE ANALYSIS, 2024

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.6 BRAND COMPARISON

- 15.6.1 EATON

- 15.6.2 SCHNEIDER ELECTRIC

- 15.6.3 ABB

- 15.6.4 SIEMENS

- 15.6.5 MITSUBISHI ELECTRIC CORPORATION

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Type footprint

- 15.7.5.4 Voltage footprint

- 15.7.5.5 End use footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 ABB

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.3.3 Expansions

- 16.1.1.3.4 Other developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses/Competitive threats

- 16.1.2 EATON

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses/Competitive threats

- 16.1.3 SCHNEIDER ELECTRIC

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses/Competitive threats

- 16.1.4 SIEMENS

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses/Competitive threats

- 16.1.5 MITSUBISHI ELECTRIC CORPORATION

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses/Competitive threats

- 16.1.6 LS ELECTRIC CO., LTD.

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.7 CHINT GROUP

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.8 FUJI ELECTRIC CO., LTD.

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.8.3.2 Expansions

- 16.1.9 ROCKWELL AUTOMATION

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.10 BENY

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.11 LEGRAND

- 16.1.11.1 Business overview

- 16.1.11.2 Products/Solutions/Services offered

- 16.1.12 SECHERON

- 16.1.12.1 Business overview

- 16.1.12.2 Products/Solutions/Services offered

- 16.1.13 CARLING TECHNOLOGIES

- 16.1.13.1 Business overview

- 16.1.13.2 Products/Solutions/Services offered

- 16.1.14 CNC ELECTRIC GROUP CO., LTD.

- 16.1.14.1 Business overview

- 16.1.14.2 Products/Solutions/Services offered

- 16.1.15 ONCCY ELECTRICAL CO., LTD

- 16.1.15.1 Business overview

- 16.1.15.2 Products/Solutions/Services offered

- 16.1.1 ABB

- 16.2 OTHER PLAYERS

- 16.2.1 ENTEC ELECTRIC & ELECTRONIC

- 16.2.2 ZHEJIANG AITE ELECTRIC TECHNOLOGY CO., LTD.

- 16.2.3 MYERS POWER PRODUCTS, INC.

- 16.2.4 NADER

- 16.2.5 LETOP

- 16.2.6 WENZHOU ZHECHI ELECTRIC CO., LTD.

- 16.2.7 ZHEJIANG DABO ELECTRIC CO., LTD.

- 16.2.8 IGOYE SOLAR POWER SYSTEM

- 16.2.9 GEYA ELECTRICAL EQUIPMENT SUPPLY

- 16.2.10 ZHEJIANG GRL ELECTRIC CO., LTD.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of key secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 List of primary interview participants

- 17.1.2.3 Key industry insights

- 17.1.2.4 Breakdown of primary interviews

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 17.2.3.1 Demand-side analysis

- 17.2.3.1.1 Demand-side assumptions

- 17.2.3.1.2 Demand-side calculations

- 17.2.3.2 Supply-side analysis

- 17.2.3.2.1 Supply-side assumptions

- 17.2.3.2.2 Supply-side calculations

- 17.2.3.1 Demand-side analysis

- 17.3 MARKET FORECAST APPROACH

- 17.3.1 SUPPLY SIDE

- 17.3.2 DEMAND SIDE

- 17.4 DATA TRIANGULATION

- 17.5 FACTOR ANALYSIS

- 17.6 RESEARCH ASSUMPTIONS AND LIMITATIONS

- 17.7 RISK ANALYSIS

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS