|

시장보고서

상품코드

1936067

아닐린 시장 : 기술별, 용도별, 최종사용자별, 지역별 - 세계 예측(-2030년)Aniline Market by Technology (Vapor Phase Process and Liquid Phase Process), End User (Building & Construction, Automotive, Rubber, Healthcare), Application (Rubber Chemicals, Fuel Additives, Dyes & Pigments), and Region - Global Forecast to 2030 |

||||||

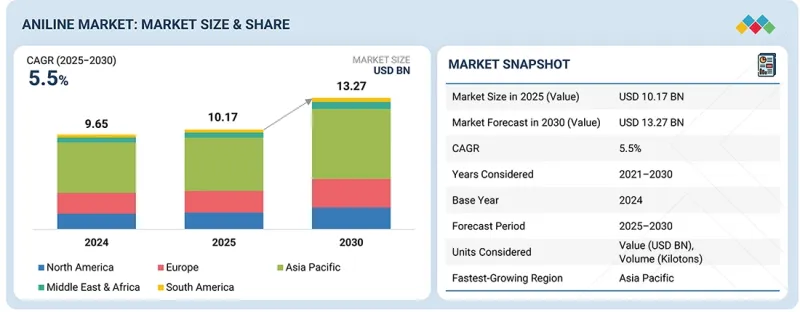

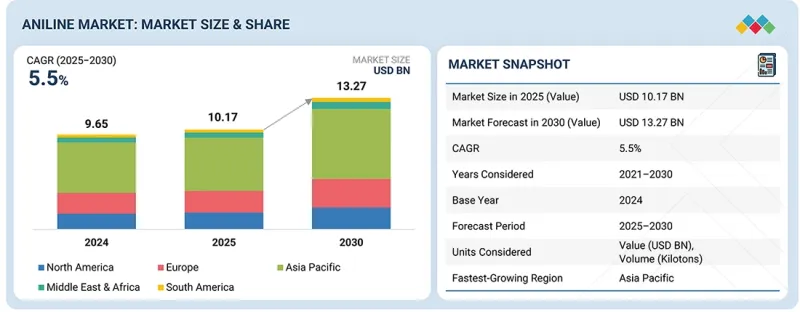

아닐린 시장 규모는 예측 기간 동안 CAGR 5.5%로 성장하여 2025년 101억 7,000만 달러에서 2030년까지 132억 7,000만 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러), 킬로톤 |

| 부문 | 기술별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

예측 기간 동안 기체상 공정은 아닐린 시장에서 두 번째로 빠르게 성장하는 기술이 될 것으로 예상됩니다. 전 세계 대부분의 기존 아닐린 생산시설은 기체상 기술을 채택하고 있으며, 현재의 개보수 작업, 촉매 업그레이드, 공정 최적화 노력을 통해 효율과 수율 향상 및 환경적 이점을 얻을 수 있습니다. 소규모 증산을 저비용으로 실현하고자 하는 생산자에게 기체상 공정은 간단한 반응기 설계와 적은 용매 처리가 필요하면서도 안정적인 운영 성능을 제공하기 때문에 매력적인 선택입니다. 유럽과 북미의 화학 산업 인프라는 MDI 생산, 고무 화학제품 제조 및 중간체 처리 요구에 대한 일관된 지원을 제공함으로써 기체상 유닛의 수익성 있는 운영을 가능하게 합니다. 첨단 촉매 및 열 통합 시스템 개발을 통해 에너지 사용량을 줄이면서 제품 품질을 향상시키고 있습니다. 신규 생산능력 증가는 액상 공정이 주도하고 있지만, 기존 플랜트의 지속적인 시스템 업데이트와 생산능력 확장으로 기체상 시스템은 성장률 2위 기술로서의 지위를 유지하고 있습니다.

자동차 부문은 예측 기간 동안 아닐린의 최종사용자로서 두 번째로 높은 성장률을 보일 것으로 예상됩니다. 이는 주로 자동차 제조에서 고성능 소재와 첨단 코팅에 대한 수요 증가에 기인합니다. 아닐린 유도체는 고무 가공 화학제품, 에폭시 수지, 폴리우레탄 부품 제조에 필수적인 재료로 작용합니다. 신흥시장의 자동차 생산 증가와 경량화, 내구성, 친환경 소재에 대한 수요 확대가 결합하여 아닐린계 중간체 수요를 견인하고 있습니다.

고무 화학 부문은 아닐린의 두 번째 주요 용도입니다. 고성능 타이어, 산업용 고무 제품, 자동차 부품에 대한 수요 증가가 아닐린계 고무 화학제품의 소비를 주도하고 있습니다. 자동차 생산의 확대와 신흥 시장의 산업 성장이 결합하여 고무에 대한 높은 수요를 창출하고 있습니다.

유럽은 두 번째로 큰 아닐린 시장으로 자리매김하고 있습니다. 독일, 프랑스, 이탈리아에서는 고무, 화학제품, 페인트, 염료, 특수 화학제품 생산을 위한 아닐린 유도체 소비가 높은 수준을 보이고 있습니다. 유럽의 엄격한 규제 요건으로 인해 기업은 고순도 아닐린 제품을 조달해야 합니다. 지속적인 산업 혁신, 정비된 인프라, 연구 개발 자금으로 시장은 지원을 받고 있습니다.

이 보고서는 기업 프로파일에 대한 종합적인 분석을 제공합니다:

주요 기업으로는 BASF SE(독일), Dow(미국), Covestro AG(독일), Lanxess(독일), Huntsman Corporation(미국), China Risun Group Limited(중국), Sinopec(중국), Sumitomo Chemical(일본), Tosoh Corporation(일본), Wanhua Chemical Group(중국) 등이 있습니다.

조사 범위

이 보고서는 아닐린 시장을 기술, 최종사용자, 용도, 지역별로 분류하고 있습니다. 이 보고서의 연구 범위에는 아닐린 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 산업 플레이어에 대한 철저한 조사를 통해 사업 개요, 솔루션 서비스, 주요 전략, 계약, 제휴 및 합의에 대한 인사이트를 제공합니다. 제품 출시, 인수합병, 아닐린 시장의 최근 동향도 다루고 있습니다. 본 보고서에는 아닐린 시장 생태계의 신생 스타트업 기업들에 대한 경쟁 분석도 포함되어 있습니다.

본 보고서 구매 이유:

이 보고서는 시장 리더와 신규 진입자에게 전체 아닐린 시장의 수익 규모에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 사업 포지셔닝을 최적화하고 적절한 시장 진입 전략을 수립하는 데 도움이 되는 인사이트를 얻을 수 있습니다. 또한, 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(염료 및 안료 산업 수요 확대, 자동차 및 산업용 고무제품용 고무 가공 화학제품 수요 증가), 억제요인(엄격한 환경 및 산업안전 규제, 벤젠 가격 변동에 따른 비 MDI 유도체 생산 경제성 영향), 기회 요인(전기자동차 타이어 및 산업용 벨트용 고성능 고무 화학제품 수요 증가, 디지털 인쇄 및 포장용 특수 고무 화학제품의 수요 증가) 증가, 디지털 인쇄 및 포장용 특수 염료, 안료, 잉크 배합의 성장), 과제(다운스트림 공정에서 안전한 취급, 보관, 운송 확보, 아닐린계 중간체를 보다 안전한 대체품으로 대체해야 한다는 규제 압력)에 대해 분석하고 있습니다.

- 제품 개발/혁신 : 아닐린 시장의 향후 기술 동향, 연구개발 활동, 서비스 전개에 대한 상세한 분석.

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 아닐린 시장을 분석합니다.

- 시장 다각화 : 아닐린 시장의 서비스, 미개척 지역, 최근 동향, 투자에 관한 종합적인 정보

- 경쟁사 평가 : BASF SE(독일), Dow(미국), Covestro AG(독일), Lanxess(독일), Huntsman Corporation(미국), China Risun Group Limited(중국), Sinopec(중국), Sumitomo Chemical(일본), Tosoh Corporation(일본), Wanhua Chemical Group(중국) 등 아닐린 시장의 주요 업체들의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 아닐린 시장(기술별)

제10장 아닐린 시장(용도별)

제11장 아닐린 시장(최종사용자별)

제12장 아닐린 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.03.05The aniline market is projected to grow from USD 10.17 billion in 2025 to USD 13.27 billion by 2030, at a CAGR of 5.5% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million), Volume (Kilotons) |

| Segments | By Technology, End User, Application, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

The vapor phase process is projected to be the second-fastest growing technology in the aniline market during the forecast period. The majority of existing aniline production facilities throughout the world, which operate on vapor phase technology, experience efficiency and yield improvements along with environmental benefits from their current revamp operations, catalyst upgrades, and process optimization efforts. Producers who want to increase their capacity in small amounts without spending much money find vapor phase processes attractive because they use simpler reactor designs and require less solvent handling while providing stable operational performance. The chemical industry infrastructure in Europe and North America permits vapor phase units to operate profitably because they provide consistent support for MDI production, rubber chemical manufacturing, and intermediate processing needs. The development of advanced catalysts together with heat-integration systems leads to better product quality while decreasing energy usage. The liquid phase process leads all new capacity additions, but the vapor phase system maintains its status as the second-fastest rising technology because of ongoing system updates and capacity expansion work at its existing plants.

''Based on end user, automotive is the second-fastest growing segment in the aniline market during the forecast period.''

The automotive segment is projected to be the second-fastest growing end user of aniline during the forecast period, primarily due to the increasing demand for high-performance materials and advanced coatings in vehicle manufacturing. Aniline derivatives serve as essential materials for producing rubber processing chemicals, epoxy resins, and polyurethane components. The automotive production increase in emerging markets, together with the growing demand for lightweight, durable, and eco-friendly materials, drives aniline-based intermediates requirements.

"Based on application, the rubber chemicals segment is estimated to account for the second-largest market during the forecast period."

The rubber chemicals segment is the second-largest application of aniline. The rising demand for high-performance tires, together with industrial rubber products and automotive components, drives the consumption of aniline-based rubber chemicals. The expansion of automotive production, together with industrial Growth in emerging markets, creates high demand for rubber.

"Europe is the second-largest market for aniline in 2025, in terms of value."

Europe stands as the second-largest aniline market. Germany, France, and Italy demonstrate high consumption levels of aniline derivatives for the production of rubber, chemicals, coatings, dyes, and specialty chemicals. The strict regulatory requirements of Europe create a need for businesses to acquire high-purity aniline products. The market receives support through ongoing industrial innovations, developed infrastructure, and research and development funding.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 60%, Tier 2- 20%, and Tier 3- 20%

- By Designation- C Level- 33%, Director Level- 33%, and Managers- 34%

- By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Middle East & Africa- 15%, and Latin America- 15%

The report provides a comprehensive analysis of company profiles:

Prominent companies in the market include BASF SE (Germany), Dow (US), Covestro AG (Germany), Lanxess (Germany), Huntsman Corporation (US), China Risun Group Limited (China), Sinopec (China), Sumitomo Chemical Co., Ltd. (Japan), Tosoh Corporation (Japan), and Wanhua Chemical Group Co., Ltd. (China).

Research Coverage

This research report categorizes the aniline market by technology (vapor phase process and liquid phase process), end user (building & construction, automotive, rubber, consumer goods & packaging, healthcare, and other end users), application (rubber chemicals, fuel additives, dyes & pigments, pharmaceuticals, MDI, and other applications), and region (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The scope of the report includes detailed information about the major factors influencing the growth of the aniline market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions, and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers & acquisitions, and recent developments in the aniline market are all covered. This report includes a competitive analysis of upcoming startups in the aniline market ecosystem.

Reasons to Buy this Report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall aniline market. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing demand in dyes & pigments industry and Growing demand for rubber processing chemicals in automotive and industrial rubber goods), restraints (Stringent environmental and occupational safety regulations and Fluctuating benzene prices, impacting production economics for non-MDI derivatives), opportunities (Increasing demand for high performance rubber chemicals in EV tires and industrial belts and Growth of specialty dyes, pigments, and ink formulations for digital printing & packaging), and challenges (Ensuring safe handling storage, and transport across downstream and Regulatory pressure to replace aniline based intermediates with safer alternatives).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the aniline market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the aniline market across varied regions.

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the aniline market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like BASF SE (Germany), Dow (US), Covestro AG (Germany), Lanxess (Germany), Huntsman Corporation (US), China Risun Group Limited (China), Sinopec (China), Sumitomo Chemical Co., Ltd. (Japan), Tosoh Corporation (Japan), and Wanhua Chemical Group Co., Ltd. (China) among others, in the aniline market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ANILINE MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ANILINE MARKET

- 3.2 ANILINE MARKET, BY TECHNOLOGY AND REGION

- 3.3 ANILINE MARKET, BY APPLICATION

- 3.4 ANILINE MARKET, BY END USER

- 3.5 ANILINE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing demand in dyes & pigments industry

- 4.2.1.2 Growing demand for rubber processing chemicals in automotive and industrial rubber goods

- 4.2.1.3 Rising consumption of agrochemicals and pharmaceuticals

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent environmental and occupational safety regulations

- 4.2.2.2 Fluctuating benzene prices impacting production economies for non-MDI derivatives

- 4.2.2.3 Limited acceptance in consumer-facing applications

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing demand for high-performance rubber chemicals in EV tires and industrial belts

- 4.2.3.2 Demand for specialty dyes, pigments, and ink formulations for digital printing & packaging

- 4.2.4 CHALLENGES

- 4.2.4.1 Ensuring safe handling, storage, and transport across downstream

- 4.2.4.2 Regulatory pressure to replace aniline-based intermediates with safer alternatives

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ANILINE MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 MANUFACTURERS

- 5.3.3 DISTRIBUTORS

- 5.3.4 END USERS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 292141)

- 5.6.2 EXPORT SCENARIO (HS CODE 292141)

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 COVESTRO'S BIO-BASED ANILINE FOR POLYURETHANE INSULATION

- 5.10.2 ANILINE IN RUBBER ACCELERATORS FOR AUTOMOTIVE TIRES

- 5.11 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Asia Pacific

- 5.11.4.3 Europe

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED CATALYTIC HYDROGENATION AND PROCESS INTENSIFICATION

- 6.1.2 GREEN AND CIRCULAR MANUFACTURING TECHNOLOGIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 MDI (METHYLENE DIPHENYL DISOCYANATE) PRODUCTION TECHNOLOGY

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM ROADMAP: PROCESS OPTIMIZATION & DIGITAL FOUNDATIONS

- 6.3.2 MID-TERM ROADMAP: PROCESS INTENSIFICATION & AUTOMATION

- 6.3.3 LONG-TERM ROADMAP: SUSTAINABLE, INTEGRATED & LOW-CARBON PRODUCTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 LEGAL STATUS OF PATENTS

- 6.4.3 JURISDICTION ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 ADVANCED RUBBER CHEMICALS FOR EV & GREEN MOBILITY

- 6.5.2 LOW-TOXICITY & SUSTAINABLE DYE INTERMEDIATES

- 6.5.3 PHARMACEUTICAL & SPECIALTY CHEMICAL INTERMEDIATES

- 6.5.4 AGROCHEMICAL INTERMEDIATES FOR PRECISION FARMING

- 6.5.5 BIO-BASED & LOW-CARBON ANILINE PRODUCTION

- 6.6 IMPACT OF AI/GEN AI ON ANILINE MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN ANILINE PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN ANILINE MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI/GENERATIVE AI IN ANILINE MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 LIST OF POTENTIAL/EXISTING CUSTOMERS OF ANILINE

9 ANILINE MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 VAPOR PHASE PROCESS

- 9.2.1 RISING POLYURETHANE DEMAND DRIVING EFFICIENT VAPOR PHASE ANILINE PRODUCTION

- 9.3 LIQUID PHASE PROCESS

- 9.3.1 DEMAND FOR COST-EFFECTIVE PRODUCTION FUELING ADOPTION

10 ANILINE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 RUBBER CHEMICALS

- 10.2.1 GROWING GLOBAL TIRE PRODUCTION DRIVING DEMAND FOR RUBBER ADDITIVES

- 10.3 FUEL ADDITIVES

- 10.3.1 RISING TRANSPORTATION FUEL CONSUMPTION SUSTAINING ANILINE USE IN PERFORMANCE ADDITIVES

- 10.4 DYES & PIGMENTS

- 10.4.1 EXPANDING TEXTILE AND COLORANT MANUFACTURING BOOSTING ANILINE-BASED DYE PRODUCTION

- 10.5 PHARMACEUTICALS

- 10.5.1 INCREASING PHARMACEUTICAL PRODUCTION DRIVING DEMAND FOR HIGH-PURITY ANILINE INTERMEDIATES

- 10.6 MDI (METHYLENE DIPHENYL DIISOCYANATE)

- 10.6.1 RAPID DEMAND FOR POLYURETHANE FOAMS ACCELERATING ANILINE CONSUMPTION

- 10.7 OTHER APPLICATIONS

11 ANILINE MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 BUILDING & CONSTRUCTION

- 11.2.1 INCREASING DEMAND FOR ENERGY-EFFICIENT BUILDING INSULATION DRIVING MARKET

- 11.3 AUTOMOTIVE

- 11.3.1 RISING VEHICLE PRODUCTION AND LIGHTWEIGHTING TRENDS BOOSTING DEMAND

- 11.4 RUBBER

- 11.4.1 GROWING TIRE MANUFACTURING FUELING DEMAND FOR ANILINE-BASED RUBBER CHEMICALS

- 11.5 CONSUMER GOODS & PACKAGING

- 11.5.1 INCREASING CONSUMPTION OF PACKAGED AND HOUSEHOLD PRODUCTS SUPPORTING MARKET GROWTH

- 11.6 HEALTHCARE

- 11.6.1 EXPANDING PHARMACEUTICAL MANUFACTURING DRIVING DEMAND FOR HIGH-PURITY ANILINE

- 11.7 OTHER END USERS

12 ANILINE MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Expanding polyurethane and automotive manufacturing driving demand

- 12.2.2 CANADA

- 12.2.2.1 Energy-efficient construction and North American supply chain integration fueling demand

- 12.2.3 MEXICO

- 12.2.3.1 Automotive manufacturing expansion and industrialization driving market growth

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Strong polyurethane and automotive manufacturing supporting market growth

- 12.3.2 FRANCE

- 12.3.2.1 Energy-efficient construction and demand for specialty chemicals driving market

- 12.3.3 UK

- 12.3.3.1 Demand in pharmaceutical and automotive applications driving market

- 12.3.4 ITALY

- 12.3.4.1 Furniture, automotive components, and construction sectors driving demand

- 12.3.5 SPAIN

- 12.3.5.1 Recovery of construction sector and expansion of automotive manufacturing supporting growth

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Massive polyurethane capacity expansion driving aniline consumption

- 12.4.2 JAPAN

- 12.4.2.1 High-purity chemical manufacturing sustaining specialty aniline demand

- 12.4.3 INDIA

- 12.4.3.1 Rapid industrialization and infrastructure growth accelerating market

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Advanced polymer manufacturing supporting steady market growth

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 Saudi Arabia

- 12.5.1.1.1 Vision 2030-led petrochemical expansion powering market growth

- 12.5.1.1 Saudi Arabia

- 12.5.2 REST OF GCC

- 12.5.2.1 Infrastructure-led industrialization accelerating market growth

- 12.5.3 SOUTH AFRICA

- 12.5.3.1 Strong automotive and industrial manufacturing sectors driving demand

- 12.5.4 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 SOUTH AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Strong automotive manufacturing and petrochemical capacity driving demand

- 12.6.2 ARGENTINA

- 12.6.2.1 Recovery of automotive and construction sectors fueling demand

- 12.6.3 REST OF SOUTH AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS, 2022-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.4.1 WANHUA CHEMICAL GROUP

- 13.4.2 BASF SE

- 13.4.3 COVESTRO AG

- 13.4.4 HUNTSMAN CORPORATION

- 13.4.5 CHINA RISUN GROUP LIMITED

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.6 BRAND/PRODUCT COMPARISON

- 13.6.1 WANHUA CHEMICAL GROUP

- 13.6.2 BASF SE

- 13.6.3 COVESTRO AG

- 13.6.4 HUNTSMAN CORPORATION

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Technology footprint

- 13.7.5.4 Application footprint

- 13.7.5.5 End user footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 DEALS

- 13.9.2 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 BASF SE

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 MnM view

- 14.1.1.3.1 Key strengths

- 14.1.1.3.2 Strategic choices

- 14.1.1.3.3 Weaknesses and competitive threats

- 14.1.2 LANXESS

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 MnM view

- 14.1.2.3.1 Key strengths

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses and competitive threats

- 14.1.3 DOW

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 COVESTRO AG

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 SUMITOMO CHEMICAL CO., LTD.

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Key strengths

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses and competitive threats

- 14.1.6 HUNTSMAN CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 MnM view

- 14.1.6.3.1 Key strengths

- 14.1.6.3.2 Strategic choices

- 14.1.6.3.3 Weaknesses and competitive threats

- 14.1.7 WANHUA CHEMICAL GROUP

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Expansions

- 14.1.7.4 MnM view

- 14.1.8 SINOPEC

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Expansions

- 14.1.8.4 MnM view

- 14.1.9 TOSOH CORPORATION

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 MnM view

- 14.1.10 CHINA RISUN GROUP LIMITED

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Deals

- 14.1.10.4 MnM view

- 14.1.11 BONDALTI

- 14.1.11.1 Business overview

- 14.1.11.2 Products/Solutions/Services offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Expansions

- 14.1.11.4 MnM view

- 14.1.1 BASF SE

- 14.2 OTHER PLAYERS

- 14.2.1 ATAMAN KIMYA

- 14.2.2 EMCO DYESTUFF

- 14.2.3 ZHENGZHOU ALFA CHEMICAL CO., LTD.

- 14.2.4 AARTI INDUSTRIES

- 14.2.5 ANHUI BAYI CHEMICAL CO., LTD.

- 14.2.6 GUJARAT NARMADA VALLEY FERTILIZERS & CHEMICALS LIMITED

- 14.2.7 R K SYNTHESIS LIMITED

- 14.2.8 HENAN GP CHEMICALS CO., LTD.

- 14.2.9 DONGYING RICH CHEMICAL CO., LTD.

- 14.2.10 PANOLI INTERMEDIATES INDIA PVT. LTD.

- 14.2.11 ANHUI XIANGLONG CHEMICAL CO., LTD.

- 14.2.12 JIANGSU KANGHENG CHEMICAL CO., LTD.

- 14.2.13 INDUSTRIAL SOLVENTS & CHEMICALS PVT. LTD.

- 14.2.14 CAYMAN CHEMICAL COMPANY

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key primary interview participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 FORECAST NUMBER CALCULATION

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS