|

시장보고서

상품코드

1942447

플로트 유리 시장 규모 예측(-2030년) : 두께별, 제품별, 최종 용도 산업별, 지역별Float Glass Market Size by Thickness, Product, End-Use Industry, and Region - Global Forecast To 2030 |

||||||

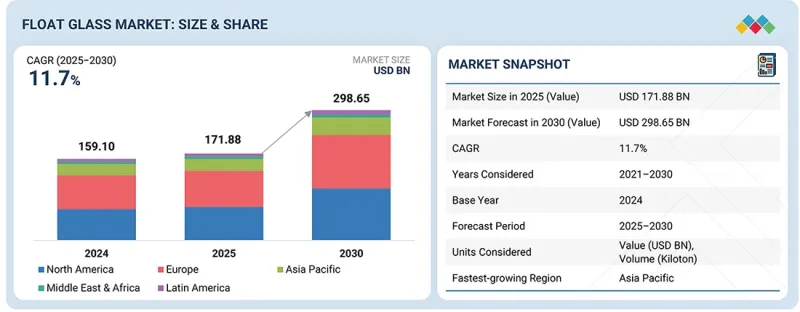

플로트 유리 시장 규모는 2025년에 약 1,718억 8,000만 달러로 평가되며, 2030년에는 2,986억 5,000만 달러에 달할 것으로 예측됩니다.

2025-2030년 연평균 성장률(CAGR)은 11.7%로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 가치(10억 달러), 킬로톤 |

| 부문 | 두께별, 제품별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

예측 기간 중 자동차 및 운송 산업은 차량 수 증가, 차량 당 유리 사용량 증가 및 유리 솔루션의 급속한 보급으로 인해 두 번째로 높은 성장률을 보이는 최종 용도 산업이 될 것으로 예측됩니다. 모든 신차에는 대형 전면 유리, 파노라마 선루프, 쿼터 글라스, 리어 글라스가 장착되어 미관, 탑승자의 시인성 및 편안함, 경량화를 통한 연비 향상을 실현했습니다. 특히 전기자동차, 고급 승용차, 2세대 상용차에서 이러한 경향이 두드러지며, 높은 안전 성능, 방음, 열 제어를 실현하는 고성능 유리가 요구되고 있습니다. 규제 당국의 승객 안전에 대한 관심은 접합유리, 강화유리 등 고가의 고급 자동차 유리의 채택을 촉진하여 시장 전체의 가치 향상에 기여하고 있습니다. 철도, 지하철, 대중교통의 확대는 교통 인프라에서 내구성과 안전 기준을 충족하는 유리의 필요성을 강조하고 있습니다. 자동차 생산량은 주기적으로 변동이 있을 수 있지만, 고사양 유리 수요에 따른 꾸준한 가치 성장은 견고하며, 자동차 및 운송 분야는 향후 예측 기간 중 성장률 2위를 기록할 것으로 예측됩니다.

가치 측면에서 접합유리는 다양한 최종 사용 산업에서 수요가 증가하고 있는 높은 안전, 보안 및 성능 특성으로 인해 예측 기간 중 두 번째로 높은 성장률을 보일 것으로 예측됩니다. 접합유리는 여러 장의 유리 층을 중간막으로 접착한 구조로 충격 강도, 방음성 및 충격 후 파손에 대한 안전성을 높입니다. 따라서 인명 및 재산 보호가 필요한 장소에서 사용하기에 적합합니다. 자동차 앞유리, 상업시설, 공항, 쇼핑몰, 고급 주택 개발에서의 사용 증가는 안전 규제 및 성능 기준의 상향 조정과 함께 성장을 가속하고 있습니다. 또한 접합유리는 가공 강도가 높고 특수 중간막과 커스터마이징이 가능하므로 일반 플로트 유리보다 훨씬 비싸고, 이것이 가치 향상을 촉진하고 있습니다. 또한 보안에 대한 관심 증가, 혹독한 기상 조건, 소음 공해로 인해 방풍-방음-방범 기능을 갖춘 접합유리의 사용 범위가 확대되고 있습니다. 이 모든 것이 견고한 가치 성장에 기여하고, 예측 기간 중 강화유리는 강화유리의 주요 촉진제 중 하나가 될 것으로 예측됩니다.

북미는 높은 리노베이션 활동, 인프라 투자, 고성능 유리 제품 사용 증가에 힘입어 예측 기간 중 가치 기준으로 두 번째로 빠르게 성장하는 지역 시장이 될 것으로 예측됩니다. 북미의 성장은 가치 기반인 반면, 신흥 시장은 주로 신규 건설 물량, 교체 수요, 에너지 효율 향상, 엄격한 건축 기준에 의해 주도되고 있습니다. 이 지역에서는 저방사율 유리, 접합유리, 단열유리, 안전유리 등 현대적 유리 솔루션의 보급률이 높으며, 모두 플로트 유리를 원료로 하여 프리미엄 가격대로 제공되고 있습니다. 전기자동차의 생산 증가와 교통 인프라의 현대화는 고성능 특성을 가진 자동차 및 운송용 유리 수요를 지속적으로 견인하고 있습니다. 또한 미국과 캐나다의 태양광발전소 확대는 태양광 등급 플로트 유리에 대한 수요를 촉진하고 있습니다. 북미는 세계 플로트 유리 시장에서 두 번째로 빠르게 성장하는 지역으로, 품질, 컴플라이언스, 지속가능성을 중시하는 성숙한 시장 구조로 고부가가치 성장을 창출하고 있습니다.

본 조사는 전 세계 업계 전문가를 대상으로 한 1차 인터뷰를 통해 검증되었습니다. 이러한 1차 정보는 다음 세 가지 범주로 분류됩니다.

이 보고서는 기업 개요에 대한 종합적인 분석을 제공

주요 기업으로는 TAIWAN GLASS IND. CORP.(대만), CSG HOLDING(중국), Fuyao Group(중국), Nippon Sheet Glass(일본), Saint-Gobain(프랑스), Sisecam(튀르키예), Central Glass(일본), AGC Inc.(일본), Trulite(조지아), SCHOTT(독일), Vitro(멕시코), Flat Glass Group(중국), Xinyi Glass Holdings Limited(중국), Guardian Industries(미국), Cevital(알제리) 등을 들 수 있습니다.

조사 범위

이 보고서는 플로트 유리 시장 규모를 두께별, 제품별, 최종 용도 산업별, 지역별로 분류하여 2030년까지 전 세계 시장 규모를 예측했습니다. 이 조사 범위에는 플로트 유리 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 과제, 기회)에 대한 종합적인 정보가 포함되어 있습니다. 주요 업계 참여 기업에 대한 종합적인 검토를 통해 각 기업의 사업 개요, 솔루션 서비스, 주요 전략, 계약, 제휴, 합의사항에 대한 인사이트을 제공합니다. 신제품 및 서비스 출시, 인수합병, 플로트 글라스 시장의 최신 동향도 다루고 있습니다. 이 보고서에는 플로트 글라스 산업 생태계에서 신생 스타트업의 경쟁에 대한 인사이트도 포함되어 있습니다.

이 보고서 구매의 장점:

이 보고서는 전체 플로트 글라스 시장과 그 하위 부문의 예상 매출 규모를 제공함으로써 시장 리더와 신규 시장 진출기업에게 도움이 될 것입니다. 이해관계자들이 경쟁 구도를 이해하고, 더 심층 인사이트을 얻고, 자사의 포지셔닝을 강화하고, 적절한 시장 진출 전략을 수립하는 데 도움이 될 수 있습니다. 또한 시장 동향을 파악하고 주요 시장 성장 촉진요인, 제약요인, 과제, 기회요인에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

- 플로트 유리 시장의 성장에 영향을 미치는 주요 촉진요인(건설 및 인프라 분야의 플로트 유리 수요 증가, 자동차 및 운송 분야의 성장), 억제요인(높은 생산 비용 및 에너지 비용), 기회(태양광 및 재생에너지 응용 분야 성장), 과제(첨단 기술의 높은 비용) 비용) 분석

- 제품 개발/혁신 : 플로트 유리 시장의 신기술 동향, 연구개발 활동, 신제품 및 서비스 출시에 대한 상세 분석

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 플로트 유리 시장을 분석합니다.

- 시장 다각화 : 플로트 유리 시장의 신제품 및 서비스, 미개발 지역, 최근 동향, 투자에 관한 종합적인 정보

- 경쟁사 평가: TAIWAN GLASS IND. CORP.(대만), CSG HOLDING(중국), Fuyao Group(중국), Nippon Sheet Glass(일본), Saint-Gobain(프랑스), Sisecam(튀르키예), Central Glass(일본), AGC Inc. AGC Inc.(일본), SCHOTT(독일), Vitro(멕시코), Flat Glass Group(중국), Xinyi Glass Holdings Limited(중국), Guardian Industries(미국) 등

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 플로트 유리 시장(두께별)

제10장 플로트 유리 시장(제품별)

제11장 플로트 유리 시장(최종 용도 산업별)

제12장 플로트 유리 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.03.09The float glass market size was valued at approximately USD 171.88 billion in 2025 and is expected to reach USD 298.65 billion in 2030, a CAGR of 11.7% between 2025 and 2030.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion), Volume (Kiloton) |

| Segments | By Product, By Thickness, By End-Use Industry |

| Regions covered | Europe, North America, Asia Pacific, Latin America, Middle East, and Africa |

"In terms of value, the automotive & transportation segment by end-use industry is expected to be the second fastest-growing market for the forecast period."

The second-fastest-growing end-use industry in the forecast period will be the automotive & transportation industry, driven by vehicle growth, increased glass per vehicle, and the rapid adoption of glazing solutions. All new cars have been fitted with large windshields, panoramic sunroofs, quarter glass, and rear glazing to enhance aesthetics, passenger visibility and comfort, and fuel savings through light weighting. This is particularly high in electric cars, luxury passenger cars, and second-generation commercial cars, which will need high-performance glass that delivers strong safety performance, acoustic insulation, and thermal control. The regulatory authorities' focus on passenger safety is also driving the adoption of advanced automotive glass, such as laminated and tempered options, which are pricier and boost the overall market value. The expansion of rail, metro, and mass transportation also underscores the need for durable, safety-compliant glass in transportation infrastructure. Though automotive volumes can experience cyclical changes, the value growth, which has been steadily increasing due to the high glass specification, makes it strong, ranking automotive & transportation as the second-fastest-growing segment in the forthcoming forecast.

''In terms of value, the laminated glass by product segment is expected to be the second fastest-growing market for the forecast period.''

In terms of value, the laminated glass is likely to be the second fastest-expanding product segment in the forecast period because of its high safety, security, and performance properties, which are on the increase in various end-use industries. Laminated glass is a system of several layers of glass bonded together with interlayers, which increase impact strength, acoustic insulation, and safety against breakage after impact, and thus it is suitable for use where human life and property protection are needed. Its increasing use in car windshields, commercial premises, airports, shopping malls, and high-end residential developments is driving growth as safety regulations and performance standards are raised. Value development is also facilitated by laminated glass, which offers greater processing intensity, specialty interlayers, and customization, making it much more expensive than plain float glass. Also, growing security concerns, severe weather conditions, and noise pollution are broadening the use of laminated glass for storm-resistant, acoustic, and security glazing. All these are favorable to a robust value growth, making laminated glass one of the major growth drivers of tempered glass throughout the forecast period.

"In terms of region, North America is expected to be the second fastest-growing market for the forecast period."

The North American region is projected to be the second-fastest-growing regional market throughout the forecast period in terms of value, driven by high renovation activity, infrastructure investment, and rising use of high-performance glass products. North American growth is value-based, whereas emerging markets are mainly driven by new construction volume and supported by replacement demand, energy efficiency upgrades, and strict building codes. The region is highly penetrated by modern glazing solutions such as low-emissivity, laminated, insulated, and safety glass, all of which are made from float glass and are priced at premium rates. The increased production of electric vehicles and the modernization of transportation infrastructure continue to drive demand for automotive and transportation glass with higher performance characteristics. Also, the growth of solar energy plants in the United States and Canada is driving demand for solar-grade float glass. North America is the second-fastest-growing region in the global float glass market, with a mature market structure that is keen on quality, compliance, and sustainability, thereby generating high-value growth.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type- Tier 1- 35%, Tier 2- 25%, and Tier 3- 40%

- By Designation- C Level- 35%, Director Level- 30%, and Others- 35%

- By Region- North America- 20%, Europe- 25%, Asia Pacific- 25%, Latin America- 10%, Middle East & Africa (MEA)-20%

The report provides a comprehensive analysis of company profiles:

Prominent companies include TAIWAN GLASS IND. CORP. (Taiwan), CSG HOLDING CO., LTD. (China), Fuyao Group (China), Nippon Sheet Glass Co., Ltd (Japan), Saint-Gobain (France), Sisecam (Turkey), Central Glass Co., Ltd. (Japan), AGC Inc. (Japan), Trulite (Georgia), SCHOTT (Germany), Vitro (Mexico), Flat glass Group Co., Ltd (China), Xinyi Glass Holdings Limited (China), Guardian Industries (US), and Cevital (Algeria) among others.

Research Coverage

This research report categorizes the Float Glass Market Size by Thickness (<5 mm, 5-10 mm, 10> mm), Product (Clear float glass, Tempered float glass, Tinted float glass, Laminated float glass), End-Use Industry (Construction & Infrastructure, Automotive & Transportation, Solar Energy), and Region - Global Forecast To 2030. The scope of the study includes comprehensive information on the key factors impacting the growth of the float glass market, including drivers, restraints, challenges, and opportunities. A comprehensive review of the top industry participants has been conducted to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. New product and service launches, mergers and acquisitions, and current developments in the float glass market are all covered. The report includes a competitive study of upcoming startups in the float glass industry ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market by providing approximate revenue figures for the overall float glass market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Growing demand for float glass in construction & Infrastructure sector, Growth in automotive & transportation sector), restraints (High production & energy cost), opportunities (Growth in solar energy and renewable applications), and challenges (High cost of advanced technologies) influencing the growth of the float glass market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the float glass market

- Market Development: Comprehensive information about lucrative markets - the report analyses the float glass market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the float glass market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like TAIWAN GLASS IND. CORP. (Taiwan), CSG HOLDING CO., LTD. (China), Fuyao Group (China), Nippon Sheet Glass Co., Ltd (Japan), Saint-Gobain (France), Sisecam (Turkey), Central Glass Co., Ltd. (Japan), AGC Inc. (Japan), SCHOTT (Germany), Vitro (Mexico), Flat glass Group Co., Ltd (China), Xinyi Glass Holdings Limited (China), and Guardian Industries (US) among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLOAT GLASS MARKET

- 3.2 FLOAT GLASS MARKET, BY END-USE INDUSTRY AND REGION

- 3.3 FLOAT GLASS MARKET, BY PRODUCT

- 3.4 FLOAT GLASS MARKET, BY THICKNESS

- 3.5 FLOAT GLASS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing demand for float glass in construction & infrastructure industry

- 4.2.1.2 Growth in automotive & transportation sector

- 4.2.2 RESTRAINTS

- 4.2.2.1 High production and energy costs

- 4.2.2.2 Stringent carbon emissions regulation

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth in solar energy and renewable applications

- 4.2.3.2 Rising adoption in emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 High cost of advanced technologies

- 4.2.4.2 Volatility in raw material prices

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN FLOAT GLASS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL CONSTRUCTION & INFRASTRUCTURE INDUSTRY

- 5.2.4 TRENDS IN SOLAR ENERGY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY KEY PLAYERS

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO FOR HS CODE 7005

- 5.6.2 IMPORT SCENARIO FOR HS CODE 7005

- 5.7 KEY CONFERENCES & EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SAINT-GOBAIN & EASTMAN COLLABORATION FOR LOW-CARBON GLASS IN ARCHITECTURE

- 5.10.2 VITRO ARCHITECTURAL GLASS AND NATIONAL AVIARY PARTNERSHIP

- 5.10.3 ADOPTION OF ENERGY-EFFICIENT GLASS IN COMMERCIAL BUILDINGS BY SAINT-GOBAIN

- 5.11 IMPACT OF 2025 US TARIFF ON FLOAT GLASS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ROLLING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ATMOSPHERIC PLASMA DEPOSITION (APD)

- 6.2.2 MAGNETRON SPUTTERING

- 6.2.3 SOL-GEL COATINGS

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPES

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 ADVANCED ARCHITECTURAL & SMART BUILDING SYSTEMS

- 6.5.2 AUTOMOTIVE GLAZING

- 6.5.3 SOLAR ENERGY & RENEWABLE POWER INFRASTRUCTURE

- 6.5.4 INFRASTRUCTURE, SAFETY & PROTECTIVE GLAZING

- 6.5.5 INDUSTRIAL MACHINERY AND ROBOTICS: HIGH-PRECISION FRAMES AND AUTOMATION STRUCTURES

- 6.6 IMPACT OF AI/GEN AI ON FLOAT GLASS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN FLOAT GLASS PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN FLOAT GLASS MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN FLOAT GLASS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 SAINT-GOBAIN: AI-ENABLED ARCHITECTURAL AND SMART GLAZING SOLUTIONS

- 6.7.2 FLOAT GLASS GROUP: ADVANCED SOLAR GLASS MANUFACTURING WITH AI-DRIVEN QUALITY AND YIELD OPTIMIZATION

- 6.7.3 FUYAO GLASS INDUSTRY GROUP: AI-ENABLED AUTOMOTIVE GLAZING FOR ADVANCED MOBILITY APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF FLOAT GLASS

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF FLOAT GLASS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 FLOAT GLASS MARKET, BY THICKNESS

- 9.1 INTRODUCTION

- 9.2 <5 MM

- 9.2.1 RAPID EXPANSION OF SOLAR PHOTOVOLTAIC (PV) INSTALLATIONS AND ENERGY-EFFICIENT BUILDING SOLUTIONS

- 9.3 5-10 MM

- 9.3.1 SUSTAINED EXPANSION OF CONSTRUCTION AND INFRASTRUCTURE DEVELOPMENT

- 9.4 >10 MM

- 9.4.1 GROWING DEMAND FROM TRANSPORTATION, MARINE, AND SPECIALTY INDUSTRIAL APPLICATIONS THAT REQUIRE HIGH STRUCTURAL INTEGRITY AND DURABILITY.

10 FLOAT GLASS MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- 10.2 CLEAR FLOAT GLASS

- 10.2.1 COST-EFFECTIVE, VERSATILE, AND WIDELY AVAILABLE

- 10.3 TEMPERED FLOAT GLASS

- 10.3.1 INCREASING EMPHASIS ON SAFETY AND DURABILITY IN CONSTRUCTION AND AUTOMOTIVE INDUSTRIES

- 10.4 TINTED FLOAT GLASS

- 10.4.1 PROTECTION AGAINST UV RAYS TO BOOST DEMAND

- 10.5 LAMINATED GLASS

- 10.5.1 RISING DEMAND FOR SAFETY AND SECURITY IN VARIOUS INDUSTRIES

- 10.6 OTHER PRODUCTS

11 FLOAT GLASS MARKET, BY END-USE INDUSTRY

- 11.1 INTRODUCTION

- 11.2 CONSTRUCTION & INFRASTRUCTURE

- 11.2.1 RAPID URBANIZATION AND SMART CITY DEVELOPMENT TO DRIVE MARKET

- 11.3 AUTOMOTIVE & TRANSPORTATION

- 11.3.1 GROWING DEMAND FOR LIGHTWEIGHT & ENERGY-EFFICIENT VEHICLES

- 11.4 SOLAR ENERGY

- 11.4.1 ADOPTION OF RENEWABLE ENERGY AND INSTALLATION OF SOLAR PANELS

- 11.5 OTHER END-USE INDUSTRIES

12 FLOAT GLASS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Presence of well-established manufacturers to drive market

- 12.2.2 CANADA

- 12.2.2.1 Growing demand from various end-use industries to fuel demand

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Booming automotive & transportation industry to drive market

- 12.3.2 UK

- 12.3.2.1 Increasing demand for float glass in construction & infrastructure industry to drive market

- 12.3.3 FRANCE

- 12.3.3.1 Presence of major float glass manufacturers to propel market

- 12.3.4 ITALY

- 12.3.4.1 Diversified industrial base and luxury automotive makers to fuel market growth

- 12.3.5 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 JAPAN

- 12.4.1.1 Growing advancements by leading manufacturers to drive market

- 12.4.2 CHINA

- 12.4.2.1 Expanding automotive & transportation industry to drive market

- 12.4.3 INDIA

- 12.4.3.1 Rapid urbanization and infrastructure development to fuel market growth

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Rising demand from automotive and electronics to boost market growth

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 JAPAN

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.5.1.1 UAE

- 12.5.1.1.1 Expansion of construction & infrastructure industry to drive market

- 12.5.1.2 Saudi Arabia

- 12.5.1.2.1 Booming construction & infrastructure industry to drive market

- 12.5.1.3 Rest of GCC countries

- 12.5.1.1 UAE

- 12.5.2 SOUTH AFRICA

- 12.5.2.1 Expanding automotive industry to fuel market growth

- 12.5.3 REST OF MIDDLE EAST & AFRICA

- 12.5.1 GCC COUNTRIES

- 12.6 LATIN AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 High import taxes to fuel market growth

- 12.6.2 MEXICO

- 12.6.2.1 Rising focus on energy efficiency and green buildings to propel market

- 12.6.3 REST OF LATIN AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS

- 13.5 BRAND COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Thickness footprint

- 13.6.5.4 Product footprint

- 13.6.5.5 End-use industry footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2024

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPANY VALUATION AND FINANCIAL METRICS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

- 13.9.4 OTHERS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 TAIWAN GLASS IND. CORP.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 MnM view

- 14.1.1.3.1 Key strengths/Right to win

- 14.1.1.3.2 Strategic choices

- 14.1.1.3.3 Weaknesses and competitive threats

- 14.1.2 CSG HOLDING CO. LTD.

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 MnM view

- 14.1.2.3.1 Key strengths/Right to win

- 14.1.2.3.2 Strategic choices

- 14.1.2.3.3 Weaknesses/Competitive threats

- 14.1.3 FUYAO GROUP

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strength/Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses/Competitive threats

- 14.1.4 NIPPON SHEET GLASS CO., LTD.

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Expansions

- 14.1.4.3.2 Others

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strength/Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses/Competitive threats

- 14.1.5 SAINT-GOBAIN

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Expansions

- 14.1.5.3.2 Deals

- 14.1.5.3.3 Others

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths/Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses/Competitive threats

- 14.1.6 SISECAM

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.3.2 Expansions

- 14.1.6.3.3 Others

- 14.1.6.4 MnM view

- 14.1.6.4.1 Key strengths/Right to win

- 14.1.6.4.2 Strategic choices

- 14.1.6.4.3 Weaknesses/Competitive threats

- 14.1.7 CENTRAL GLASS CO., LTD.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 MnM view

- 14.1.7.3.1 Key strengths/Right to win

- 14.1.7.3.2 Strategic choices

- 14.1.7.3.3 Weaknesses/Competitive threats

- 14.1.8 AGC INC.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.3.2 Deals

- 14.1.8.3.3 Others

- 14.1.8.4 MnM view

- 14.1.8.4.1 Key strengths/Right to win

- 14.1.8.4.2 Strategic choices

- 14.1.8.4.3 Weaknesses/Competitive threats

- 14.1.9 TRULITE

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.9.4 MnM view

- 14.1.9.4.1 Right to win

- 14.1.9.4.2 Strategic choices

- 14.1.9.4.3 Weaknesses/Competitive threats

- 14.1.10 SCHOTT

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Expansions

- 14.1.10.4 MnM view

- 14.1.10.4.1 Key strengths/Right to win

- 14.1.10.4.2 Strategic choices

- 14.1.10.4.3 Weaknesses/Competitive threats

- 14.1.11 VITRO

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Expansions

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Others

- 14.1.11.4 MnM view

- 14.1.11.4.1 Key strengths/Right to win

- 14.1.11.4.2 Strategic choices

- 14.1.11.4.3 Weaknesses/Competitive threats

- 14.1.12 FLAT GLASS GROUP CO., LTD.

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 MnM view

- 14.1.12.3.1 Key strengths/Right to win

- 14.1.12.3.2 Strategic choices

- 14.1.12.3.3 Weaknesses/Competitive threats

- 14.1.13 XINYI GLASS HOLDINGS LIMITED

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Expansions

- 14.1.13.4 MnM view

- 14.1.13.4.1 Key strengths/Right to win

- 14.1.13.4.2 Strategic choices

- 14.1.13.4.3 Weaknesses/Competitive threats

- 14.1.14 GUARDIAN INDUSTRIES

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches

- 14.1.14.3.2 Deals

- 14.1.14.3.3 Expansions

- 14.1.14.3.4 Others

- 14.1.14.4 MnM view

- 14.1.14.4.1 Key strengths/Right to win

- 14.1.14.4.2 Strategic choices

- 14.1.14.4.3 Weaknesses/Competitive threats

- 14.1.15 CEVITAL

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 MnM view

- 14.1.15.3.1 Key strengths/Right to win

- 14.1.15.3.2 Strategic choices

- 14.1.15.3.3 Weaknesses/Competitive threats

- 14.1.1 TAIWAN GLASS IND. CORP.

- 14.2 OTHER PLAYERS

- 14.2.1 BEHRENBERG GLASS CO.

- 14.2.2 GOLD PLUS GROUP

- 14.2.3 PHOENICIA

- 14.2.4 CARDINAL GLASS INDUSTRIES, INC

- 14.2.5 GILLINDER BROTHERS, INC.

- 14.2.6 INDEPENDENT GLASS CO.

- 14.2.7 GSC GLASS LTD

- 14.2.8 VELUX GROUP

- 14.2.9 EMERGE GLASS

- 14.2.10 SCHEUTEN GLASS

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key primary interview participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Key industry insights

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 BASE NUMBER CALCULATION

- 15.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 15.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 15.4 MARKET FORECAST APPROACH

- 15.4.1 SUPPLY SIDE

- 15.4.2 DEMAND SIDE

- 15.5 DATA TRIANGULATION

- 15.6 FACTOR ANALYSIS

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS