|

시장보고서

상품코드

2062343

저철분 유리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Low Iron Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

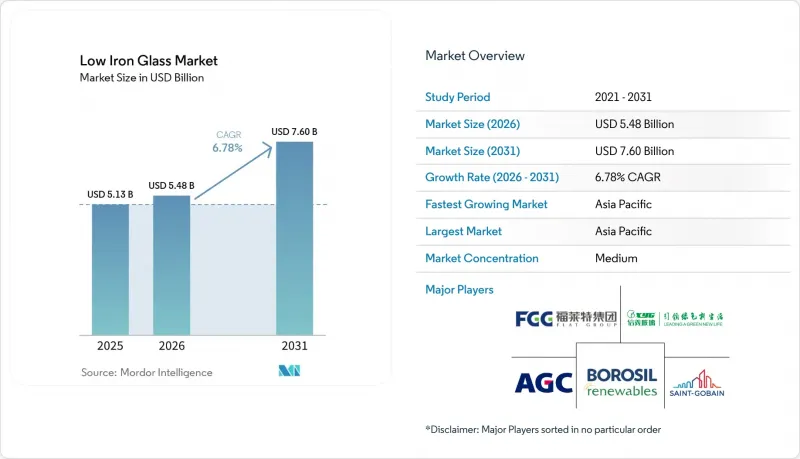

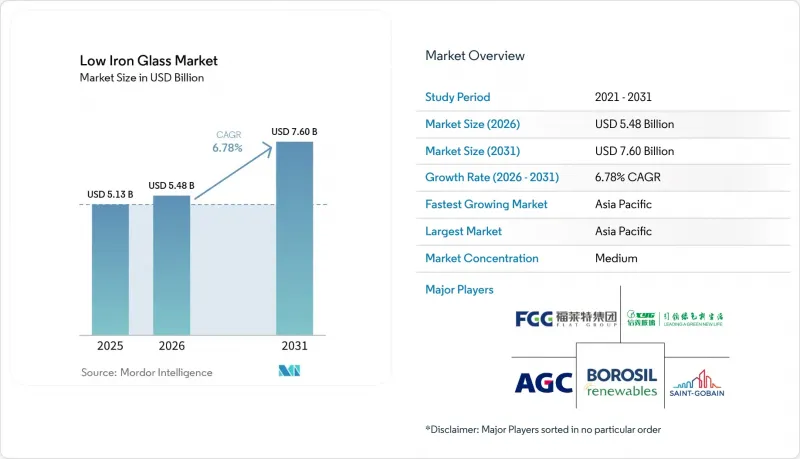

Mordor Intelligence에 의하면, 저철분 유리 시장 규모는 2025년에 51억 3,000만 달러, 2026년에 54억 8,000만 달러가 되어, 2031년까지 76억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.78%로 성장할 것으로 전망됩니다.

본 보고서는 제품 유형(투명 저철분 유리, 착색 저철분 유리 등), 용도(건축용 파사드, 태양광 발전 모듈 및 BIPV 등), 최종 사용자 산업(재생 에너지 및 태양광 발전 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 저철분 유리 시장 동향 및 분석

건축용 유리의 뛰어난 투명성과 광투과율

개발사는 LEED(Leadership in Energy and Environmental Design) 버전 5 및 BREEAM(Building Research Establishment Environmental Assessment Method) 2024의 채광 기준을 충족하기 위해 가시광선 투과율 91% 이상을 지정하고 있으며, 이것이 저철분 유리 시장 수요를 견인하고 있습니다. 예를 들어, 런던의 62층짜리 ‘8 Bishopsgate’ 타워에는 Sedak사의 isopure 저철분 유리 유닛이 채택되어 72%의 투광률과 0.7 W/m²-K의 U-값을 달성함으로써 연간 난방·환기·공조(HVAC) 비용을 18% 절감했습니다. 마찬가지로, 중층 건물의 리모델링 공사에서도 저철분 유리가 사용되고 있습니다. Vitro사의 ‘Solarban Acuity’ 시리즈는 73%의 광투과율과 0.23의 태양열 획득 계수를 자랑하며, 북미에서는 이 제품을 채택한 프로젝트가 유틸리티회사로부터 리베이트를 받을 수 있습니다. 시애틀의 ‘더 잭’ 빌딩에 사용된 AGC사의 Clearvision(클리어비전) 유리는 68%의 광투과율과 0.28의 열취득계수를 달성하여, 초고투명 기판이 거주자의 쾌적성을 얼마나 높여주는지를 입증했습니다. 친환경 건축 기준이 강화됨에 따라 건축가들이 커튼월, 채광창, 아트리움에 저철분 유리를 채택하는 사례가 늘어나고 있으며, 이는 전 세계적인 수요를 더욱 부추기고 있습니다.

태양광 발전(PV) 및 BIPV 모듈의 적용 확대

양면 수광형 및 탠덤형 페로브스카이트-실리콘 태양전지에는 91.5% 이상의 전면 유리 투과율이 요구되지만, 이는 표준 소다-라임 플로트 유리로는 달성할 수 없기 때문에 재생에너지 분야에서의 저철분 유리의 역할이 확고해지고 있습니다. 2024년에 출시된 PURE Solar사의 변환 효율 25% BIPV 패널은 저철분 기판을 사용함으로써 발전량이 3-4% 포인트 향상된 것으로 입증되었습니다. 프라운호퍼 태양에너지 시스템 연구소(ISE)의 MorphoColor 코팅은 착색된 저철분 유리 위에서 블랙 셀과 동등한 90-96%의 효율을 유지하고 있어, 미관이 성능을 저해하지 않음을 입증하고 있습니다. 2025년, 중국은 3,274만 1,000톤의 태양광 발전용 유리를 생산했으며, 이후 저철분 배합으로의 전환을 진행하지 않는 한 신규 용해로 설치를 제한하고 있습니다. 한편, 인도가 태양광 발전용 유리에 부과한 5년간의 반덤핑 관세는 보로실 리뉴어블스(Borosil Renewables)사의 생산 능력을 하루 600톤으로 확대하는 계기가 되었으며, 이러한 정책 조치가 국내 생산 능력을 얼마나 강화하고 있는지를 여실히 보여주고 있습니다.

표준 플로트 유리에 비해 높은 생산 비용

저철분 유리는 철 실리카 함량이 60ppm 미만이며, 용융 주기가 길어지고 더 엄격한 조성 관리가 필요하기 때문에 표준 플로트 유리보다 25-40% 비쌉니다. 이러한 가격 프리미엄으로 인해, 비용 효율성을 중시하는 창유리 용도에서는 저철분 유리의 사용이 제한되고 있습니다. 예를 들어, 대만글라스(Taiwan Glass)는 2025년에 9억 6,000만 대만 달러(3,021만 달러)의 손실을 기록했으며, 평판유리의 이익률 하락에 대응하기 위해 전자용 유리 섬유 직물 사업에 대한 투자를 강화했습니다. 박물관 전시 케이스나 수족관 등에 사용되는 필킨턴 옵티화이트는 소량 구매 시 1제곱미터(m²)당 120달러에 판매되지만, 일반적인 플로트 유리는 1제곱미터당 50달러이므로, 이 유리의 사용은 높은 투명도가 요구되는 프로젝트로 제한되어 있습니다. 또한, 저철분 유리에 대한 강화 및 접합 유리 가공 공정에서는 태양열 흡수율이 낮아지기 때문에 가마 일정을 재검토해야 하며, 이로 인해 가공 비용이 10-15% 증가합니다.

부문별 분석

코팅된 저철분 유리는 2031년까지 연평균 성장률(CAGR) 7.38%를 기록하며 성장할 것으로 예상되며, 2025년 매출의 43.78%를 차지했던 무색 유리의 성장률을 상회할 것으로 전망됩니다. 반사 방지(AR) 및 투명 전도성 산화물(TCO) 코팅은 모듈의 출력을 2-3% 포인트 향상시킵니다. 광과학연구소(ICFO)와 코닝(Corning)의 리소그래피가 필요 없는 AR 공정은 99% 미만의 투과율을 달성했으며, 2024년에 시범 생산에 들어갔습니다. 라미네이트 제품은 헤드업 디스플레이(HUD)나 증강현실(AR)용 도파관에 사용되고 있으며, 이스트먼의 ‘Saflex Horizon Vision’ 중간막은 저철분 유리 기판과 결합함으로써 고스트 이미지의 분리 거리를 0.3mm 미만으로 억제하는 데 성공했습니다. 착색 유리는 색이 진해질수록 투과율이 떨어지기 때문에 보급에는 한계가 있습니다. 그러나 저철분 유리에 MorphoColor 필름을 적용함으로써 블랙셀 효율 90-96%를 유지하며, 파사드 용도로 사용할 때 미적 선택지를 제공합니다. 비용 효율을 중시하는 창유리 용도에서는 여전히 투명 유리가 주류를 이루고 있지만, 코팅 유리의 가격 차이가 줄어들면서 시장 점유율을 잃고 있으며, 저철분 유리 시장 내에서 대체가 진행되고 있습니다.

연구 개발 활동은 나노 구조 코팅에 주력하고 있습니다. 중국의 제조업체들은 이산화규소(SiO₂) 졸-겔 필름을 상품화했으며, 이는 코팅되지 않은 기판에 비해 15% 미만의 추가 비용으로 94-96%의 투과율을 실현하여 대규모 태양광 발전 분야에서의 채택을 촉진하고 있습니다. 반사율 0.1%, 투과율 94%를 실현하는 롤-투-롤(R2R) 방식의 자외선(UV) 나노 임프린트 기술을 활용한 나방 눈 구조는 2028년까지 생산 수율이 95%를 넘어서면 채택이 확대될 가능성이 있습니다. 이러한 기술적 진보는 최종 사용자에게 제공하는 가치를 강화하고, 제조업체가 수익성을 유지할 수 있도록 돕습니다.

지역별 분석

아시아태평양은 2025년에 시장 가치의 48.02%를 차지하며 연평균 성장률(CAGR) 7.32%를 기록해 저철분 유리 시장에서의 입지를 유지할 것으로 예측됩니다. 중국에서는 생산 능력 교환 규제의 영향으로 가마를 저철분 배합으로 업그레이드하고 있는 반면, 인도의 반덤핑 관세가 보로실(Bharosil)과 비샤카(Vishaka)의 사업 확장을 뒷받침하고 있습니다. 인도네시아 바탕 자유무역지대에는 신이(Sinyi)와 KCC로부터 118억 달러가 넘는 투자가 유치되어, 이 지역의 수출 거점이 확립되었습니다. 일본과 한국은 증강현실(AR) 및 OLED 광학 용도를 지원하기 위해 코팅 유리 및 디스플레이용 유리의 기술 혁신에 주력하고 있습니다.

북미에서는 생산의 국내 복귀(리쇼어링)가 진행되고 있습니다. NSG의 오하이오 주 공장과 코닝사가 3억 1,500만 달러를 투자한 캔턴 공장 확장 계획은 퍼스트 솔라(First Solar) 및 극자외선(EUV) 리소그래피 공급망을 뒷받침하고 있습니다. 푸야오(Fuyao)사의 4억 달러 규모 일리노이주 프로젝트와 솔라사이클(Solarcycle)사의 조지아주 재활용 시설은 순환형 공급망을 강화하고 있습니다. 멕시코는 미국-멕시코-캐나다 협정(USMCA)을 통한 시장 접근성을 활용하고 있으며, 비트로(Vitro)사의 파트너십 프로그램은 기능성 유리 제품의 공동 개발을 촉진하고 있습니다. 단, 정보원의 신뢰성을 유지하기 위해 민간 조사 기관의 데이터는 제외되었습니다.

유럽에서는 높은 에너지 비용과 유럽연합 배출권 거래 제도(ETS) 4단계의 탄소 비용에 대한 대응이 진행되고 있어, 유리 제조업체들은 하이브리드 용광로 기술 도입을 검토해야 하는 상황에 놓여 있습니다. AGC와 생고뱅이 체코에서 추진 중인 ‘볼타’ 시범 프로젝트는 2028년까지 전력 50%, 산소 연료 50%로 구성된 용융 공정의 실증을 목표로 하고 있습니다. 시세캄은 튀르키예, 이탈리아, 불가리아에 총 3억 8,900만 달러를 투자했으며, 한편 NSG가 폴란드에 건설하여 2027년 가동을 예정하고 있는 새로운 코팅 라인은 자동차 및 건축 시장을 대상으로 할 예정입니다. 재활용은 여전히 과제로 남아 있으며, 건축용 판유리 중 용해로에서 재사용 가능한 칼렛으로 회수되는 비율은 고작 5%에 불과합니다. 그러나 네덜란드에서는 75%의 회수율을 달성하고 있어, 저철분 유리 업계 내의 현저한 격차와 전략적 차이가 두드러지게 드러나고 있습니다. 중동에서는 1차 생산 능력이 확대되고 있습니다. 신이(Xinyi)가 3억 8,600만 달러를 투자한 사우디아라비아 생산 라인과 가디언(Guardian)의 코터 플러스 플로트(Coater Plus Float) 확장 프로젝트는 2028년까지 걸프 지역의 전기변색 및 건축일체형 태양광(BIPV) 프로젝트에 제품을 공급할 것으로 기대됩니다. 남미에서는 시장 규모가 여전히 작지만, 브라질과 칠레가 태양광 패널 함량 요건을 도입함에 따라 새로운 기회가 생겨나고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the low iron glass market size is projected to be USD 5.13 billion in 2025, USD 5.48 billion in 2026, and reach USD 7.60 billion by 2031, growing at a CAGR of 6.78% from 2026 to 2031.

This report is Segmented by Product Type (Clear Low-Iron Glass, Tinted Low-Iron Glass, and More), Application (Architectural Facades, Solar PV Modules and BIPV, and More), End-User Industry (Renewable Energy and Solar and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Low Iron Glass Market Trends and Insights

Superior Clarity and Light Transmission in Architectural Glazing

Developers are specifying visible-light transmission above 91% to meet Leadership in Energy and Environmental Design (LEED) version 5 and Building Research Establishment Environmental Assessment Method (BREEAM) 2024 daylighting standards, driving demand in the low-iron glass market. For example, the 62-story 8 Bishopsgate tower in London utilized Sedak isopure low-iron glass units, achieving 72% light transmission and a U-value of 0.7 W/m2-K, which reduced annual heating, ventilation, and air conditioning (HVAC) costs by 18%. Similarly, mid-rise retrofits are adopting low-iron glass; Vitro's Solarban Acuity line offers 73% transmission and a 0.23 solar heat-gain coefficient, qualifying projects in North America for utility rebates. AGC Inc. Clearvision glazing, used in The Jack building in Seattle, achieved 68% transmission and a 0.28 heat-gain coefficient, demonstrating how ultra-clear substrates enhance occupant comfort. As green building codes become stricter, architects are increasingly incorporating low-iron glass in curtain walls, skylights, and atria, further driving global demand.

Growing Adoption in Solar PV and BIPV Modules

Bifacial and tandem perovskite-silicon solar cells require front-glass transmittance of greater than or equal to 91.5%, which standard soda-lime float glass cannot achieve, solidifying the role of low-iron glass in renewable energy applications. PURE Solar's 25% efficient BIPV panel, launched in 2024, demonstrated a 3-4 percentage-point yield improvement using low-iron substrates. Fraunhofer Institute for Solar Energy Systems (ISE)'s MorphoColor coatings maintain 90-96% of black-cell efficiency on colored low-iron glass, proving that aesthetics do not compromise performance. In 2025, China produced 32.741 million tons of photovoltaic glass and has since imposed restrictions on new kilns unless they upgrade to low-iron formulations. Meanwhile, India's five-year anti-dumping duties on solar glass have accelerated Borosil Renewables' expansion to 600 tons per day, highlighting how policy measures are bolstering domestic production capacity.

Higher Production Cost Versus Standard Float Glass

Low-iron glass units are priced 25-40% higher than standard float glass due to the use of sub-60 parts per million (ppm) iron silica, extended melting cycles, and stricter composition controls. This price premium limits the adoption of low-iron glass in cost-sensitive fenestration applications. For example, Taiwan Glass reported a TWD 960 million (USD 30.21 million) loss in 2025 and shifted its focus to electronic-grade fiberglass cloth to address declining flat-glass margins. Pilkington Optiwhite, used in applications such as museum cases and aquariums, is priced at USD 120 per square meter (m2) in small quantities, compared to USD 50 per m2 for standard float glass, restricting its use to projects requiring high clarity. Additionally, tempering and laminating processes for low-iron glass require recalibrated furnace schedules due to reduced solar absorption, which increases processing costs by 10-15%.

Other drivers and restraints analyzed in the detailed report include:

- Integration with Electrochromic and Smart-Facade Systems

- Emerging Demand from High-Resolution Display and AR/VR Cover Glass

- Volatile High-Purity Silica-Sand Supply and Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated low-iron glass is expected to grow at a CAGR of 7.38% through 2031, surpassing the growth of clear formulations, which accounted for 43.78% of revenue in 2025. Anti-reflective (AR) and transparent conductive oxide (TCO) coatings improve module output by 2-3 percentage points. The Institute of Photonic Sciences (ICFO) and Corning's lithography-free AR process achieved transmittance levels below 99% and entered pilot production in 2024. Laminated products are used in heads-up displays (HUDs) and augmented reality (AR) waveguides, with Eastman's Saflex Horizon Vision interlayer achieving ghost-image separations of less than 0.3 millimeters when combined with low-iron substrates. Tinted glass has limited adoption due to reduced transmission with deeper colors. However, MorphoColor films on low-iron glass maintained 90-96% of black-cell efficiency, offering aesthetic options for facade applications. Clear glass continues to dominate cost-sensitive fenestration applications but is losing market share as coated glass narrows price gaps, encouraging substitution within the low-iron glass market.

Research and development efforts are focused on nanostructured coatings. Chinese manufacturers have commercialized silicon dioxide (SiO2) sol-gel films that deliver 94-96% transmission at premiums of less than 15% compared to uncoated substrates, driving adoption in utility-scale solar applications. Roll-to-roll ultraviolet (UV) nanoimprint moth-eye structures, which promise 0.1% reflectance and 94% transmission, could gain adoption if production yields exceed 95% by 2028. These technological advancements enhance value propositions for end-users and support manufacturers in maintaining profit margins.

Geography Analysis

Asia-Pacific is expected to hold 48.02% market value in 2025, with a CAGR of 7.32%, maintaining its position in the low iron glass market. China is upgrading kilns to low-iron formulations under capacity-swap regulations, while India's anti-dumping duties are driving expansions by Borosil and Vishakha. Indonesia's Batang free-trade zone has attracted investments from Xinyi and KCC, exceeding USD 11.8 billion, establishing a regional export hub. Japan and South Korea are focusing on coated and display-grade innovations to support augmented reality (AR) and organic light-emitting diode (OLED) optics applications.

North America is advancing reshoring efforts. NSG's Ohio plant and Corning's USD 315 million Canton extension are supporting First Solar and extreme ultraviolet (EUV) lithography supply chains. Fuyao's USD 400 million Illinois project and Solarcycle's recycling facility in Georgia are strengthening circular supply chains. Mexico is leveraging the United States-Mexico-Canada Agreement (USMCA) access, with Vitro's partnership program encouraging the co-development of functional glazing. However, data from commercial research firms has been excluded to maintain source integrity.

Europe is addressing high energy tariffs and European Union Emissions Trading System (ETS) Phase 4 carbon costs, prompting glassmakers to explore hybrid furnace technologies. AGC and Saint-Gobain's Volta pilot project in the Czech Republic aims to test a 50% electric and 50% oxyfuel melting process by 2028. Sisecam has invested USD 389 million across Turkey, Italy, and Bulgaria, while NSG's new coating line in Poland, set to launch in 2027, will cater to automotive and architectural markets. Recycling remains a challenge, with only 5% of construction flat glass being returned as furnace-ready cullet. However, the Netherlands achieves a 75% collection rate, highlighting a significant disparity and a strategic gap in the low-iron glass industry. The Middle East is increasing primary production capacity. Xinyi's USD 386 million Saudi Arabia line and Guardian's coater-plus-float expansion are expected to supply Gulf electrochromic and building-integrated photovoltaic (BIPV) projects by 2028. In South America, while the market remains smaller, opportunities are emerging as Brazil and Chile introduce solar-content requirements.

- AGC Inc.

- borosilrenewables

- Corning Incorporated

- CSG Holding Co., Ltd.

- Flat Glass Group Co., Ltd.

- Fuyao Glass Industry Group

- Guardian Industries Holdings

- HORN Glass Industries AG

- Huihua Glass Co.,Limited.

- Jinjing (Group) Co., Ltd.

- Lumon Group

- Nippon Sheet Glass Co., Ltd.

- Saint-Gobain Glass

- Sisecam

- Taiwan Glass Ind. Corp.

- Trakya Glass and Aluminum Industry & Trade Inc.

- Vitro Architectural Glass

- Xinyi Glass Holdings Limited

- Zibo Huaxing Chemical Equipment Factory

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Superior clarity and light-transmission in architectural glazing

- 4.2.2 Growing adoption in solar PV and BIPV modules

- 4.2.3 Integration with electrochromic and smart-facade systems

- 4.2.4 Emerging demand from high-resolution display and AR/VR cover glass

- 4.2.5 Domestic content mandates fueling regional solar-glass manufacturing

- 4.3 Market Restraints

- 4.3.1 Higher production cost vs. standard float glass

- 4.3.2 Volatile high-purity silica-sand supply and pricing

- 4.3.3 Limited specialty-glass recycling infrastructure

- 4.3.4 Energy-intensity exposure to carbon pricing schemes

- 4.4 ValueChain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Clear Low-Iron Glass

- 5.1.2 Tinted Low-Iron Glass

- 5.1.3 Coated Low-Iron Glass

- 5.1.4 Laminated Low-Iron Glass

- 5.2 By Application

- 5.2.1 Architectural and Building Facades

- 5.2.2 Solar PV Modules and BIPV

- 5.2.3 Display Glass (TV, Monitor, Smartphone, AR/VR)

- 5.2.4 Furniture and Interior Decoration

- 5.2.5 Automotive Optical Glass

- 5.2.6 Aquarium and Horticulture Lighting

- 5.3 By End-user Industry

- 5.3.1 Renewable Energy and Solar

- 5.3.2 Construction and Commercial Buildings

- 5.3.3 Electronics and Display Manufacturing

- 5.3.4 Furniture and Interior Design

- 5.3.5 Automotive and Transportation

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AGC Inc.

- 6.4.2 borosilrenewables

- 6.4.3 Corning Incorporated

- 6.4.4 CSG Holding Co., Ltd.

- 6.4.5 Flat Glass Group Co., Ltd.

- 6.4.6 Fuyao Glass Industry Group

- 6.4.7 Guardian Industries Holdings

- 6.4.8 HORN Glass Industries AG

- 6.4.9 Huihua Glass Co.,Limited.

- 6.4.10 Jinjing (Group) Co., Ltd.

- 6.4.11 Lumon Group

- 6.4.12 Nippon Sheet Glass Co., Ltd.

- 6.4.13 Saint-Gobain Glass

- 6.4.14 Sisecam

- 6.4.15 Taiwan Glass Ind. Corp.

- 6.4.16 Trakya Glass and Aluminum Industry & Trade Inc.

- 6.4.17 Vitro Architectural Glass

- 6.4.18 Xinyi Glass Holdings Limited

- 6.4.19 Zibo Huaxing Chemical Equipment Factory

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment