|

시장보고서

상품코드

1942452

뉴트라슈티컬 구미 시장 예측(-2030년) : 유형별, 소비자 유형별, 생산능력별, 원료 유래별, 구미 기반/부형제별, 제품 유형별, 기능성별, 인구통계별, 유통 채널별, 지역별Nutraceutical Gummies Market by Type (B2B, B2C), Product Type (Vitamins, Minerals, Omega-3 Fatty Acids), Consumer Type, Production Capacity, Ingredient Source, Functionality, Demographics, Sales Channel, and Region - Global Forecast to 2030 |

||||||

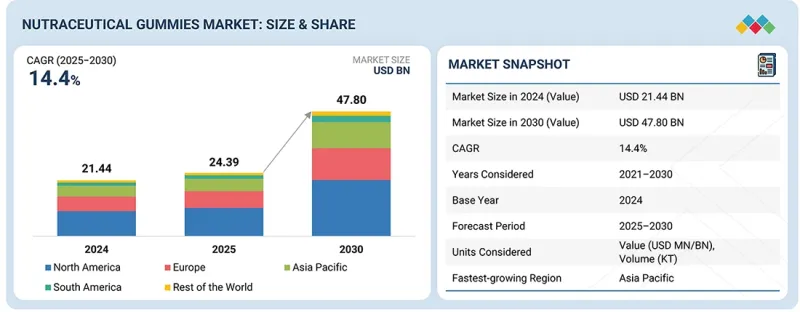

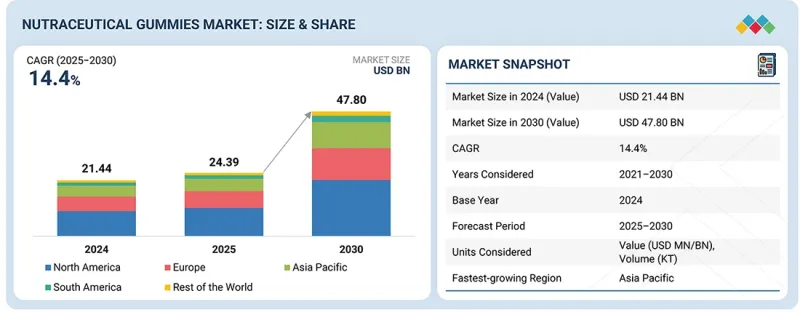

뉴트라슈티컬 구미 시장 규모는 2025년에 243억 9,000만 달러로 추정되며, 2030년까지 CAGR 14.4%로 478억 달러에 달할 것으로 예측됩니다.

세계 뉴트리슈티컬 구미 시장은 비타민 결핍 및 영양 결핍 증가, 예방 의학 및 건강 증진에 대한 관심 증가, 미용 및 건강에 대한 소비자 관심 증가, E-Commerce 및 D2C 채널 확대, 기존 정제 및 캡슐보다 구미 형태의 섭취 방식에 대한 선호도 증가에 따라 구미 형태의 섭취 방식에 대한 선호도 증가를 배경으로 괄목할 만한 성장을 달성하고 있습니다. 또한 식물성 및 무설탕 구미의 성장, 스타트업 기업 및 D2C 브랜드의 턴키 계약 제조에 대한 의존도 증가, 지역별 처방 노하우를 활용한 지역적 확장은 뉴트리슈티컬 구미 시장에서 큰 성장 기회를 창출할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 금액(100만 달러) 및 수량(1,000톤) |

| 부문 | 유형별, 소비자 유형별, 생산능력별, 원료 유래별, 구미 기반/부형제별, 제품 유형별, 기능성별, 인구통계별, 유통 채널별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미 및 기타 지역 |

그러나 높은 생산 비용과 원료의 안정성 문제, 지역별 규제의 복잡성, 배치 간 일관성 및 안정성 유지의 어려움 등이 뉴트리슈티컬 구미 시장이 해결해야 할 과제가 될 것으로 예측됩니다. 또한 전 세계 브랜드 소유자의 감사 요구 사항 증가, 치열한 시장 경쟁, 브랜드 차별화도 기술적 과제로 남아있습니다.

뉴트리슈티컬 구미의 인기는 편리한 모양, 크기, 섭취의 용이성 때문에 더욱 높아지고 있습니다. 면역력 향상에 도움이 되는 종합비타민 구미의 장점도 영양 구미 수요 증가에 중요한 역할을 하고 있습니다. 구미는 비타민-미네랄 보충제 중 가장 높은 성장 잠재력을 가지고 있습니다. 영양이 건강에 미치는 영향과 생활습관 요인을 통해 해결할 수 있는 특정 문제에 대한 인식이 높아짐에 따라 면역 특화 구미 보충제 시장은 성장할 것으로 예측됩니다.

인지도, 수요, 보급률 증가와 함께 뉴트리슈티컬 구미는 주류 시장의 스테디셀러 상품으로 자리 잡았습니다. 이러한 제품에 대한 수요 증가는 온라인과 오프라인 유통 채널을 통해 다양한 국가와 지역에서의 판매 확대로 이어지고 있습니다. 주요 기업은 보다 폭넓은 소비자층에게 제품을 제공하기 위해 유통 채널에 대한 투자를 적극적으로 추진하고 있으며, 그 확장을 추진하고 있습니다. 또한 뉴트리슈티컬 구미 제조 기업은 비점포형 유통 채널의 일환인 온라인 소매 등의 전략을 통해 시장에서의 제품 홍보를 강화하고 있으며, 이는 수요 증가의 요인이 될 것으로 예측됩니다.

이 지역에서 사업을 운영하는 기업은 뉴트리슈티컬 구미 등 건강보조식품 산업 수요 증가에 대응하기 위해 사업 확장 및 인수에 투자하고 있습니다. 유럽에서 뉴트리슈티컬 구미에 대한 수요 증가는 바쁜 라이프스타일, 건강 지향적인 소비자, 도시화 등이 원인으로 꼽힙니다. 2020년에는 유니레버가 미국에 본사를 둔 비타민 및 미네랄 보충제 기업 SmartyPants Vitamins를 인수했습니다. SmartyPants는 지속가능한 방식으로 조달된 생체 이용 효율이 높은 영양소와 유전자 변형이 없는 인증된 원료를 폭넓게 활용하고 있습니다. 이 기업의 제품 라인은 인공 방부제, 감미료, 색소, 향료를 전혀 사용하지 않습니다. 이를 통해 유니레버는 제품 포트폴리오를 확장하고 더 많은 유럽 소비자층에게 서비스를 제공할 수 있게 되었습니다.

시장의 주요 기업으로는 다음 기업을 들 수 있습니다. 브랜드 제조업체로 Church & Dwight Co., Inc.(미국), H&H Group(홍콩), Amway(미국), Bayer AG(독일), Haleon(영국), Nestle(스위스), Unilever(미국), Otsuka Holdings(일본), PharmaCare Laboratories Australia(호주), Swanson(미국), IM Healthcare(인도), SMP Nutra(미국), Nature's Truth(미국), Herbaland Naturals Inc.(캐나다).수탁제조업체로서 Sofgen Pharma(룩셈부르크), Catalent, Inc.(미국), Activ'Inside(프랑스), WinNutra(미국), Makers Nutrition, LLC(미국), Ion Labs(미국), Vitajoy Group(중국), Bliss Lifesciences LLP(인도), Global Widget, LLC(미국), Gummy Worlds(튀르키예), TopGum(이스라엘), MeriCal(미국), Fexmentis Life Sciences(인도), Eagle Labs, Inc.(미국) 등이 포함됩니다.

조사 범위

이 보고서는 뉴트리슈티컬 구미 시장을 유형별, 소비자 유형별, 생산 능력별, 원료 유래별, 구미 베이스/부형제별, 제품 유형별, 기능별, 성별, 인구 통계별, 유통 채널별, 지역별로 분석했습니다.

이 보고서의 연구 범위에는 영양 구미 산업의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 진입업체에 대한 철저한 분석을 통해 각 업체의 사업 내용, 서비스, 주요 전략, 계약, 제휴, 합의, 제품 출시, 인수합병, 최근 뉴트리셔틀 구미 시장 동향에 대한 인사이트을 제공합니다. 이 보고서는 뉴트리슈티컬 구미 시장 생태계의 신생 스타트업 기업에 대한 경쟁 분석을 제공합니다. 또한 기술 분석, 생태계 및 시장 매핑, 특허 및 규제 현황 등 산업별 동향도 조사 대상입니다.

이 보고서 구매 이유

이 보고서는 시장 리더와 신규 시장 진출기업에게 전체 뉴트리슈티컬 구미 시장과 그 하위 부문의 매출 수치에 대한 가장 근접한 추정치에 대한 정보를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 이해하고, 비즈니스를 더 잘 포지셔닝하고, 적절한 시장 진출 전략을 수립할 수 있는 추가 인사이트을 얻을 수 있습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 성장 촉진요인, 시장 성장 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

- 뉴트리슈티컬 구미 시장의 성장에 영향을 미치는 주요 촉진요인(기존 정제나 캡슐보다 구미 제형에 대한 선호도 증가에 따른 생산량 증가), 억제요인(원료 조달의 변동성), 기회요인(스타트업 기업 및 D2C 브랜드의 턴키 계약 제조에 대한 의존도 증가), 기회요인(스타트업 기업 및 D2C 브랜드에 의한 턴키 계약 제조에 대한 의존도 증가), 과제(세계 브랜드 오너의 감사 요구사항 강화) 분석

- 제품 개발/혁신 : 뉴트리슈티컬 구미 시장의 R&D 활동 및 신제품 출시에 대한 상세 분석

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 다양한 지역에서의 뉴트리셔틀 구미 분석

- 시장 다각화 : 영양 구미 시장의 신제품 소스, 미개발 지역, 최근 동향, 투자에 관한 종합적인 정보

- 경쟁사 평가: 주요 진입기업 브랜드 제조업체로는 Church & Dwight Co., Inc.(미국), H&H Group(홍콩), Amway(미국), Bayer AG(독일), Haleon(영국), Nestle(스위스), Unilever(미국), Otsuka Holdings(일본), PharmaCare Laboratories Australia(호주), Swanson(미국), IM Healthcare(인도), SMP Nutra(미국), Nature's Truth(미국), Herbaland Naturals Inc.(캐나다), 그리고 수탁제조업체로서 Sofgen Pharma(룩셈부르크), Catalent, Inc. Labs(미국), Vitajoy Group(중국), Bliss Lifesciences LLP(인도), Global Widget, LLC(미국), Gummy Worlds(튀르키예), TopGum(이스라엘), MeriCal(미국), Fexmentis Life Sciences(인도), Eagle Labs, Inc.(미국) 등이 뉴트리슈티컬 구미 시장의 주요 진출 기업입니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 관한 구상

제8장 고객 상황과 구매 행동

제9장 뉴트라슈티컬 구미 시장(유형별)

제10장 뉴트라슈티컬 구미 시장(소비자 유형별)

제11장 뉴트라슈티컬 구미 시장(생산능력별)

제12장 뉴트라슈티컬 구미 시장(원료 유래별)

제13장 뉴트라슈티컬 구미 시장(구미 기반/첨가제별)

제14장 뉴트라슈티컬 구미 시장(제품 유형별)

제15장 뉴트라슈티컬 구미 시장(기능성별)

제16장 뉴트라슈티컬 구미 시장(인구통계별)

제17장 뉴트라슈티컬 구미 시장(유통 채널별)

제18장 뉴트라슈티컬 구미 시장(지역별)

제19장 경쟁 구도

제20장 기업 개요

제21장 조사 방법

제22장 인접 시장과 관련 시장

제23장 부록

KSA 26.03.09The nutraceutical gummies market is estimated at USD 24.39 billion in 2025 and is projected to reach USD 47.80 billion by 2030, at a CAGR of 14.4%. The global nutraceutical gummies market is experiencing significant growth, driven by rising rates of vitamin deficiency and undernutrition, a growing focus on preventive health and wellness, rising consumer interest in beauty and wellness, expanding e-commerce and DTC channels, and an increasing preference for the gummy delivery format over traditional pills and capsules. Additionally, growth in plant-based and sugar-free gummies, increasing reliance of startups and D2C brands on turnkey contract manufacturing, and geographic expansion with localized formulation expertise are expected to create significant opportunities in the nutraceutical gummies market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (KT) |

| Segments | Type, customer type, production capacity, ingredient source, product type, functionality, demographics, sales channel, and region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Rest of the World (RoW) |

However, high production costs and ingredient stability issues, regulatory complexities across regions, and the complexity of maintaining batch-to-batch consistency and stability are expected to pose challenges in the nutraceutical gummies market. Furthermore, increasing audit expectations from global brand owners and intense market competition and brand differentiation also remain technical challenges.

"Immunity support function is expected to hold a dominant market share during the forecast period."

The popularity of nutraceutical gummies is growing because of their convenient form, size, and ease of consumption. The benefits of multivitamin gummies for boosting immunity also play a key role in the increased demand for nutraceutical gummies. Gummies offer the fastest growth potential for vitamin and mineral supplements. The market for immunity-specific gummy supplements is expected to grow as more people become aware of how nutrition affects their health and of the specific issues that can be addressed through lifestyle factors.

"The online channel segment in the B2C segment is expected to hold a significant market share among the sales channels in the nutraceutical gummies market."

With rising awareness, demand, and traction, nutraceutical gummies have become a mainstream market staple. The increase in demand for these products has led to a rise in sales across various countries and regions, facilitated by both online and offline distribution channels. Key players are increasingly adopting and navigating their investments in distribution channels to make their products available to a wider consumer base. In addition, nutraceutical gummies manufacturing companies are promoting their products in the market through strategies such as online retailing, a part of the non-store-based distribution channel, which is expected to drive demand.

"Europe is expected to hold a significant share in the global nutraceutical gummies market during the forecast period."

Companies operating in this region are also investing in expansions and acquisitions to meet the growing demand from the dietary supplements industry, including nutraceutical gummies. The growing demand for nutraceutical gummies in Europe is attributed to fast-paced lifestyles, health-conscious consumers, and urbanization. In 2020, Unilever acquired SmartyPants Vitamins, a US-based vitamin, mineral & supplement company. SmartyPants utilizes a range of sustainably sourced, bioavailable nutrients and non-GMO-certified ingredients. Its product line is free of artificial preservatives, sweeteners, colors, and flavors. This has made Unilever expand its product portfolio and serve more consumers in Europe.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the nutraceutical gummies market.

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: CXOs - 25%, Managers - 40%, Others - 35%

- By Region: North America - 25%, Europe - 25%, Asia Pacific - 35%, South America - 10%, and Rest of the World -5%

Prominent companies in the market include-Brand Manufacturers: Church & Dwight Co., Inc. (US), H&H Group (Hong Kong), Amway (US), Bayer AG (Germany), Haleon (UK), Nestle (Switzerland), Unilever (US), Otsuka Holdings Co., Ltd. (Japan), PharmaCare Laboratories Australia (Australia), Swanson (US), IM Healthcare (India), SMP Nutra (US), Nature's Truth (US) and Herbaland Naturals Inc. (Canada) and Contract Manufacturers: Sofgen Pharma (Luxembourg), Catalent, Inc. ( US), Activ'Inside ( France), WinNutra (US), Makers Nutrition, LLC (US), Ion Labs (US), Vitajoy Group (China), Bliss Lifesciences LLP (India), Global Widget, LLC (US), Gummy Worlds (Turkey), TopGum (Israel), MeriCal (US), Fexmentis Life Sciences (India), and Eagle Labs, Inc. (US) among others.

Research Coverage

This research report categorizes the nutraceutical gummies market by type (B2B market and B2C market); customer type (B2B) (brand owners and marketing companies, retailers and distributors, healthcare and wellness providers, pharmaceutical companies, and food & beverage companies); production capacity (B2B) (small-scale contract manufacturers (< 10 m units/year), mid-scale manufacturers (10-50 m units/year), and large-scale industrial manufacturers (50 m+ units/year)); ingredient source (B2B) (animal-based source, plant-based source, microbial/fermentation-derived sources, and synthetic/chemically-derived sources); gummy base/excipients (B2B) (gelatin-based gummies, pectin-based gummies, starch-based gummies, agar, carrageenan, and other hydrocolloids); product type (B2C) (vitamins, minerals, omega-3 fatty acids, probiotics and prebiotics, collagen and beauty-from-within, herbal and botanical supplements, dietary fiber, CBD and cannabis-derived, and specialty formulations); functionality (B2C) (immunity support, general health & wellness, bone & joint health, weight management, beauty & skin health, and other functionalities); demographics (B2C) (generation alpha (0-12 years), generation Z (13-28 years), millennials (gen Y) (29-44 years), generation X (45-60 years), and baby boomers & older (61+ years)); sales channel (offline and online); and region (North America, Europe, Asia Pacific, South America, and Rest of the World).

The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, which influence the growth of the nutraceutical gummies industry. A thorough analysis of key industry players has been conducted to provide insights into their businesses, services, key strategies, contracts, partnerships, agreements, product launches, mergers & acquisitions, and recent developments in the nutraceutical gummies market. This report provides a competitive analysis of emerging startups in the nutraceutical gummies market ecosystem. Furthermore, the study covers industry-specific trends, including technology analysis, ecosystem & market mapping, and patent & regulatory landscape, among others.

Reasons to Buy This Report

The report provides market leaders/new entrants with information on the closest approximations of revenue numbers for the overall nutraceutical gummies and their subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (increasing preference for gummy delivery format over traditional pills and capsules, driving production volume), restraints (ingredient sourcing volatility), opportunities (increasing reliance of startups and D2C brands on turnkey contract manufacturing), and challenges (increasing audit expectations from global brand owners), influencing the growth of the nutraceutical gummies market

- Product Development/Innovation: Detailed insights into research & development activities and new product launches in the nutraceutical gummies market

- Market Development: Comprehensive information about lucrative markets-analysis of nutraceutical gummies across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the nutraceutical gummies market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as Brand Manufacturers: Church & Dwight Co., Inc. (US), H&H Group (Hong Kong), Amway (US), Bayer AG (Germany), Haleon (UK), Nestle (Switzerland), Unilever (US), Otsuka Holdings Co., Ltd. (Japan), PharmaCare Laboratories Australia (Australia), Swanson (US), IM Healthcare (India), SMP Nutra (US), Nature's Truth (US) and Herbaland Naturals Inc. (Canada) and Contract Manufacturers: Sofgen Pharma (Luxembourg), Catalent, Inc. (US), Activ'Inside (France), WinNutra (US), Makers Nutrition, LLC (US), Ion Labs (US), Vitajoy Group (China), Bliss Lifesciences LLP (India), Global Widget, LLC (US), Gummy Worlds (Turkey), TopGum (Israel), MeriCal (US), Fexmentis Life Sciences (India), and Eagle Labs, Inc. (US), among other players in the nutraceutical gummies market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNIT CONSIDERED

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN NUTRACEUTICAL GUMMIES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN NUTRACEUTICAL GUMMIES MARKET

- 3.2 B2B NUTRACEUTICAL GUMMIES MARKET, BY PRODUCTION CAPACITY AND REGION

- 3.3 B2C NUTRACEUTICAL GUMMIES MARKET, BY PRODUCT TYPE AND REGION

- 3.4 B2B NUTRACEUTICAL GUMMIES MARKET, BY CUSTOMER TYPE

- 3.5 B2B NUTRACEUTICAL GUMMIES MARKET, BY INGREDIENT SOURCE

- 3.6 B2C NUTRACEUTICAL GUMMIES MARKET, BY DEMOGRAPHICS

- 3.7 B2B NUTRACEUTICAL GUMMIES MARKET, BY COUNTRY

- 3.8 B2C NUTRACEUTICAL GUMMIES MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising rate of vitamin-deficiency diseases and undernutrition

- 4.2.1.2 Growing consumer interest in beauty and wellness

- 4.2.1.3 Innovation in functional formulations

- 4.2.1.4 Growth in gummy supplement launches and custom gummy programs

- 4.2.1.5 Increasing preference for gummy delivery format over traditional pills and capsules

- 4.2.2 RESTRAINTS

- 4.2.2.1 Regulatory complexities across regions

- 4.2.2.2 Sugar content and health concerns

- 4.2.2.3 Ingredient sourcing volatility

- 4.2.2.4 Complexity in maintaining batch-to-batch consistency and stability

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising popularity of plant-based and sugar-free gummies

- 4.2.3.2 Expansion into personalized and AI-driven nutrition

- 4.2.3.3 Increasing reliance of startups and D2C brands on turnkey contract manufacturing

- 4.2.3.4 Geographic expansion with localized formulation expertise

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited bioavailability and nutrient degradation

- 4.2.4.2 Intense market competition and brand differentiation

- 4.2.4.3 Logistics issues: Melting, deformation, and transit stability

- 4.2.4.4 Increasing audit expectations from global brand owners

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN NUTRACEUTICAL GUMMIES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.1.1 Macroeconomic indicators - B2C market

- 5.2.1.1.1 US-China trade tariff fluctuations reshape nutraceutical gummies market

- 5.2.1.1.2 Inflation and raw material costs reshape nutraceutical gummies market

- 5.2.1.1.2.1 Sweeteners and sugar inputs

- 5.2.1.1.2.2 Gelling agents: Gelatin, pectin, and alternatives

- 5.2.1.1.2.3 Vitamins, actives, flavors, and specialty additives

- 5.2.1.1.2.4 Energy, transportation, and packaging inflation

- 5.2.1.2 Macroeconomic indicators - B2B market

- 5.2.1.2.1 Population aging and chronic disease burden influencing preventive health and nutraceutical market expansion

- 5.2.1.1 Macroeconomic indicators - B2C market

- 5.2.1 INTRODUCTION

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL & FUNCTIONAL INGREDIENT SOURCING

- 5.3.2 PRODUCT DEVELOPMENT AND MANUFACTURING

- 5.3.3 QUALITY, SAFETY, AND REGULATORY COMPLIANCE

- 5.3.4 PACKAGING & LABEL CUSTOMIZATION

- 5.3.5 MARKETING AND DISTRIBUTION

- 5.3.6 END USERS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE (ASP) OF NUTRACEUTICAL GUMMIES, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE (ASP) TREND OF NUTRACEUTICAL GUMMIES, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO OF HS CODE 210690, BY KEY COUNTRY, 2020-2024 (MT)

- 5.6.2 IMPORT SCENARIO OF HS CODE 210690, BY KEY COUNTRY, 2020-2024 (MT)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 NESTLE HEALTH SCIENCE - EXPANDED COLLAGEN & FUNCTIONAL PORTFOLIO THROUGH MAJORITY STAKE ACQUISITION OF VITAL PROTEINS

- 5.10.2 SIRIO PHARMA - EXPANDING NUTRACEUTICAL GUMMY AND PLANT-BASED SOFTGEL MANUFACTURING THROUGH ACQUISITION OF BEST FORMULATIONS

- 5.10.3 TOPGUM INDUSTRIES - EXPANDING PHARMA GRADE AND HIGH VOLUME GUMMY MANUFACTURING THROUGH ACQUISITION OF ISLAND ABBEY NUTRITIONALS

- 5.10.4 GILLCO/IFF GRINDSTED - ENHANCING GUMMY GELATION AND PROCESS STABILITY USING SLOW-SET PECTIN

- 5.11 IMPACT OF 2025 US TARIFF - NUTRACEUTICAL GUMMIES MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Gelling and texture technology

- 6.1.1.1.1 Starch-based gelling technology

- 6.1.1.1.2 Starchless gelling technology

- 6.1.1.2 Microencapsulation technology (taste masking & flavor)

- 6.1.1.1 Gelling and texture technology

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Coating technology

- 6.1.2.2 Nutrient stabilization methods

- 6.1.2.3 Flavor release systems

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 3D-printing & personalized dosing platforms

- 6.1.3.2 Plant-based and clean-label ingredient technologies

- 6.1.3.3 Smart packaging

- 6.1.1 KEY TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM | FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM | EXPANSION & STANDARDIZATION

- 6.2.3 LONG-TERM | PRECISION NUTRITION & SMART CALCIUM SOLUTIONS

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 GELATIN-FREE, REDUCED-SUGAR FUNCTIONAL GUMMIES ENRICHED WITH PGH EXTRACT

- 6.4.2 MICROENCAPSULATION OF VITAMIN C FOR IMPROVED STABILITY IN NUTRACEUTICAL GUMMIES

- 6.4.3 3D-PRINTED PATIENT-TAILORED MEDICINAL GUMMIES FOR PEDIATRIC DRUG DELIVERY

- 6.4.4 EDIBLE ACTIVE PACKAGING AS SMART PACKAGING FOR NUTRACEUTICAL GUMMIES

- 6.4.5 IOT-ENABLED SMART MANUFACTURING AND ITS FUTURE APPLICATION IN NUTRACEUTICAL GUMMY PRODUCTION

- 6.5 IMPACT OF GENERATIVE AI ON NUTRACEUTICAL GUMMIES MARKET

- 6.5.1 INTRODUCTION

- 6.5.2 USE OF GENERATIVE AI ON NUTRACEUTICAL GUMMIES MARKET

- 6.5.3 TOP USE CASES AND MARKET POTENTIAL

- 6.5.4 BEST PRACTICES IN NUTRACEUTICAL INDUSTRY

- 6.5.5 CASE STUDIES OF AI IMPLEMENTATION IN NUTRACEUTICAL GUMMIES MARKET

- 6.5.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.7 CLIENTS' READINESS TO ADOPT GENERATIVE AI NUTRACEUTICAL GUMMIES

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 LABELING REQUIREMENTS AND CLAIMS

- 7.1.4 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.4.1 Mandatory validation of bioavailability & functional claims

- 7.1.4.2 Global harmonization of dietary supplement & nutraceutical classifications

- 7.1.4.3 Strengthened safety, contaminant, & additive control regulations

- 7.1.4.4 Digital labeling, traceability & QR-based compliance tracking

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABLE SOURCING

- 7.2.2 CARBON FOOTPRINT REDUCTION INITIATIVES

- 7.2.3 CIRCULAR ECONOMY APPROACHES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS APPLICATION INDUSTRIES ACROSS SUPPLY CHAIN

- 8.5 MARKET PROFITABILITY

- 8.6 REVENUE POTENTIAL

- 8.6.1 COST DYNAMICS

- 8.6.2 MARGIN OPPORTUNITIES, BY TYPE

9 NUTRACEUTICAL GUMMIES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 B2C MARKET

- 9.2.1 ADVANCING CONSUMER HEALTH THROUGH FUNCTIONAL GUMMIES

- 9.3 B2B MARKET

- 9.3.1 POWERING BRANDS WITH SCALABLE, SCIENCE-DRIVEN GUMMY SOLUTIONS

10 NUTRACEUTICAL GUMMIES MARKET (B2B), BY CUSTOMER TYPE

- 10.1 INTRODUCTION

- 10.2 BRAND OWNERS & MARKETING COMPANIES

- 10.2.1 DEMAND FOR DIFFERENTIATED, CLEAN-LABEL, AND TREND-RESPONSIVE GUMMY FORMULATIONS TO BENEFIT CONTRACT MANUFACTURERS AND PRIVATE-LABEL PARTNERS

- 10.3 RETAILERS & DISTRIBUTORS

- 10.3.1 RAPID EXPANSION OF PRIVATE-LABEL SUPPLEMENTS AND OMNICHANNEL RETAIL STRATEGIES TO INCREASE RETAILER DEMAND FOR COST-EFFICIENT, HIGH-QUALITY GUMMY MANUFACTURING PARTNERSHIPS

- 10.4 HEALTHCARE & WELLNESS

- 10.4.1 GROWING INTEGRATION OF NUTRITION INTO PREVENTIVE CARE, PEDIATRICS, AND WELLNESS PROGRAMS TO DRIVE DEMAND FOR CLINICALLY CREDIBLE, COMPLIANCE-FRIENDLY GUMMY SUPPLEMENTS

- 10.5 PHARMACEUTICAL COMPANIES

- 10.5.1 PHARMACEUTICAL PLAYERS LEVERAGE NUTRACEUTICAL GUMMIES TO EXTEND CONSUMER HEALTH PORTFOLIOS BEYOND PRESCRIPTIONS WHILE MAINTAINING CLINICAL CREDIBILITY AND QUALITY DIFFERENTIATION

- 10.6 FOOD & BEVERAGE COMPANIES

- 10.6.1 CONVERGENCE OF INDULGENCE AND FUNCTIONALITY PROMPTING CONFECTIONERY AND FOOD COMPANIES TO EXPLORE FUNCTIONAL GUMMIES

11 NUTRACEUTICAL GUMMIES MARKET (B2B), BY PRODUCTION CAPACITY

- 11.1 INTRODUCTION

- 11.2 SMALL-SCALE CONTRACT MANUFACTURERS (<10 M UNITS/YEAR)

- 11.2.1 GROWING DEMAND FOR LOW-VOLUME, CUSTOMIZED GUMMY FORMULATIONS TO SUPPORT EMERGING NUTRACEUTICAL BRANDS

- 11.3 MID-SCALE MANUFACTURERS (10-50 M UNITS/YEAR)

- 11.3.1 INCREASING NEED FOR SCALABLE PRODUCTION WITH FORMULATION FLEXIBILITY TO SUPPORT BRAND EXPANSION AND REGIONAL MARKET PENETRATION

- 11.4 LARGE-SCALE INDUSTRIAL MANUFACTURERS (50+ M UNITS/YEAR)

- 11.4.1 RISING REQUIREMENT FOR HIGH-VOLUME, STANDARDIZED GUMMY PRODUCTION TO ENSURE SUPPLY CONSISTENCY FOR GLOBAL NUTRACEUTICAL BRANDS

12 NUTRACEUTICAL GUMMIES MARKET (B2B), BY INGREDIENT SOURCE

- 12.1 INTRODUCTION

- 12.2 ANIMAL-BASED SOURCES

- 12.2.1 COLLAGEN EFFICACY KEEPS ANIMAL-BASED INGREDIENTS DOMINANT

- 12.3 PLANT-BASED SOURCES

- 12.3.1 VEGAN AND CLEAN-LABEL DEMAND FUELS PLANT-BASED ADOPTION

- 12.4 MICROBIAL/FERMENTATION-DERIVED SOURCES

- 12.4.1 ADVANCEMENTS IN STABILIZED FERMENTATION TECHNOLOGIES TO EXPANDING ADOPTION OF MICROBIAL-DERIVED ACTIVES IN GUMMY FORMULATIONS

- 12.5 SYNTHETIC/CHEMICALLY-DERIVED SOURCES

- 12.5.1 CONSISTENCY AND SCALE TO SUSTAIN SYNTHETIC INGREDIENT USAGE

13 NUTRACEUTICAL GUMMIES MARKET (B2B), BY GUMMY BASE/EXCIPIENTS

- 13.1 INTRODUCTION

- 13.2 GELATIN-BASED GUMMIES

- 13.2.1 HIGH ACTIVE LOADING AND TEXTURE RELIABILITY TO CONTINUE DRIVING GELATIN USAGE

- 13.3 PECTIN-BASED GUMMIES

- 13.3.1 VEGAN POSITIONING AND CLEAN-LABEL DEMAND TO ACCELERATE PECTIN ADOPTION

- 13.4 STARCH-BASED GUMMIES

- 13.4.1 COST PRESSURE AND LARGE-SCALE PRODUCTION NEEDS TO SUSTAIN STARCH-BASED SYSTEMS

- 13.5 AGAR, CARRAGEENAN, AND OTHER HYDROCOLLOIDS

14 NUTRACEUTICAL GUMMIES MARKET (B2C), BY PRODUCT TYPE

- 14.1 INTRODUCTION

- 14.2 VITAMINS

- 14.2.1 RISING INSTANCES OF VITAMIN DEFICIENCIES TO DRIVE SEGMENT

- 14.2.2 MULTIVITAMINS

- 14.2.3 VITAMIN C

- 14.2.4 VITAMIN D

- 14.2.5 VITAMIN B COMPLEX

- 14.2.6 VITAMIN E AND A

- 14.3 MINERALS

- 14.3.1 MEETING ESSENTIAL MINERAL NEEDS THROUGH CONVENIENT, PALATABLE SUPPLEMENTATION FOR EVERYDAY HEALTH SUPPORT

- 14.3.2 CALCIUM

- 14.3.3 IRON

- 14.3.4 ZINC

- 14.3.5 MAGNESIUM

- 14.4 OMEGA-3 FATTY ACIDS

- 14.5 PROBIOTICS & PREBIOTICS

- 14.5.1 INCREASED INTEREST IN SKIN CARE AMONG CONSUMERS TO BOOST MARKET

- 14.6 COLLAGEN & BEAUTY-FROM-WITHIN

- 14.6.1 INCREASED INTEREST IN SKIN CARE AMONG CONSUMERS TO BOOST MARKET

- 14.7 HERBAL & BOTANICAL

- 14.7.1 RISING CONSUMER PREFERENCE FOR PLANT-BASED NATURAL INGREDIENTS TO DRIVE SEGMENT

- 14.7.2 ASHWAGANDHA

- 14.7.3 TURMERIC/CURCUMIN

- 14.7.4 ELDERBERRY

- 14.7.5 MELATONIN

- 14.7.6 OTHER HERBAL AND BOTANICAL GUMMIES

- 14.8 DIETARY FIBER

- 14.9 CBD & CANNABIS-DERIVED

- 14.10 SPECIALTY FORMULATIONS

- 14.10.1 HEALTH-PROMOTING PROPERTIES TO AUGMENT SEGMENT GROWTH

15 NUTRACEUTICAL GUMMIES MARKET(B2C), BY FUNCTIONALITY

- 15.1 INTRODUCTION

- 15.2 IMMUNITY SUPPORT

- 15.2.1 RISING FOCUS ON IMPROVING IMMUNITY TO DRIVE MARKET

- 15.3 GENERAL HEALTH & WELLNESS

- 15.3.1 GROWING NUTRITIONAL DEFICIENCIES AND PREVENTIVE HEALTHCARE TRENDS TO DRIVE MARKET

- 15.4 BONE & JOINT HEALTH

- 15.4.1 RISING CASES OF OSTEOPOROSIS TO PROPEL MARKET GROWTH

- 15.5 WEIGHT MANAGEMENT

- 15.5.1 RISING PREVALENCE OF OBESITY AND METABOLIC DISORDERS TO DRIVE MARKET

- 15.6 BEAUTY & SKIN HEALTH

- 15.6.1 INCREASING FOCUS ON APPEARANCE AND OVERALL SKIN WELLNESS TO DRIVE MARKET

16 NUTRACEUTICAL GUMMIES MARKET (B2C), BY DEMOGRAPHICS

- 16.1 INTRODUCTION

- 16.2 GENERATION ALPHA (0-12 YEARS)

- 16.2.1 EARLY-LIFE SUPPLEMENTATION AND DIGITAL-FIRST PARENTING TO FUEL DEMAND FOR PEDIATRIC NUTRACEUTICAL GUMMIES

- 16.3 GENERATION Z (13-28 YEARS)

- 16.3.1 FOCUS ON HEALTH AND DAILY SELF-CARE TO FUEL GUMMY SUPPLEMENT DEMAND

- 16.4 MILLENNIALS (GEN Y) (29-44 YEARS)

- 16.4.1 LIFESTYLE-DRIVEN WELLNESS CHOICES TO POWER NUTRACEUTICAL ADOPTION

- 16.5 GENERATION X (45-60 YEARS)

- 16.5.1 WILLINGNESS TO INVEST IN HEALTH-ENHANCING NUTRITION SOLUTIONS TO DRIVE MARKET

- 16.6 BABY BOOMERS AND OLDER (61+ YEARS)

- 16.6.1 HEALTHY AGING PRIORITIES TO DRIVE NUTRACEUTICAL USE

17 NUTRACEUTICAL GUMMIES MARKET (B2C), BY DISTRIBUTION CHANNEL

- 17.1 INTRODUCTION

- 17.2 OFFLINE CHANNELS

- 17.2.1 HYPERMARKETS & SUPERMARKETS

- 17.2.1.1 Preferred purchasing destination and availability of variants to drive growth

- 17.2.2 PHARMACIES & DRUGSTORES

- 17.2.2.1 Wide presence and around-the-clock services to drive growth

- 17.2.3 SPECIALTY HEALTH STORES

- 17.2.3.1 Enabling premium and targeted gummy supplement sales

- 17.2.4 CONVENIENCE STORES

- 17.2.4.1 Preference toward specialized healthcare products to fuel growth

- 17.2.5 MASS MERCHANDISERS AND MULTI-LEVEL MARKETING (MLM)

- 17.2.5.1 High-volume retail and network-based selling drive offline expansion

- 17.2.1 HYPERMARKETS & SUPERMARKETS

- 17.3 ONLINE CHANNELS

18 NUTRACEUTICAL GUMMIES MARKET, BY REGION

- 18.1 INTRODUCTION

- 18.2 NORTH AMERICA

- 18.2.1 US

- 18.2.1.1 Presence of key players and various health trends to boost market

- 18.2.2 CANADA

- 18.2.2.1 Convenience, taste, and health benefits to drive demand for nutraceutical gummies

- 18.2.3 MEXICO

- 18.2.3.1 Rising health-conscious and vegan population to drive market

- 18.2.1 US

- 18.3 EUROPE

- 18.3.1 GERMANY

- 18.3.1.1 Growing interest in health & wellness to drive market

- 18.3.2 UK

- 18.3.2.1 Rising prevalence of diseases to drive market

- 18.3.3 FRANCE

- 18.3.3.1 High healthcare costs and increased demand for dietary supplements to drive market

- 18.3.4 SPAIN

- 18.3.4.1 Adoption of healthy lifestyles to drive market

- 18.3.5 ITALY

- 18.3.5.1 Strong e-commerce system and rising geriatric population to drive market

- 18.3.6 REST OF EUROPE

- 18.3.1 GERMANY

- 18.4 ASIA PACIFIC

- 18.4.1 CHINA

- 18.4.1.1 Large population and increasing prevalence of diseases to drive market

- 18.4.2 JAPAN

- 18.4.2.1 Rising awareness and shifting preferences toward dietary supplements to drive market

- 18.4.3 INDIA

- 18.4.3.1 Rising disposable incomes and growing focus on wellness to drive market

- 18.4.4 AUSTRALIA & NEW ZEALAND

- 18.4.4.1 High demand for dietary supplements, particularly in new formats, to drive market

- 18.4.5 REST OF ASIA PACIFIC

- 18.4.1 CHINA

- 18.5 SOUTH AMERICA

- 18.5.1 BRAZIL

- 18.5.1.1 Increasing consumer preference for convenient and palatable formats in nutrient intake to drive market

- 18.5.2 ARGENTINA

- 18.5.2.1 Growing focus on prevention of micronutrient deficiencies and cardiometabolic risks to drive market

- 18.5.3 REST OF SOUTH AMERICA

- 18.5.1 BRAZIL

- 18.6 REST OF THE WORLD

- 18.6.1 MIDDLE EAST

- 18.6.1.1 Rising disposable incomes and healthcare costs to drive market

- 18.6.2 AFRICA

- 18.6.2.1 Increase in vitamin deficiency and consumer awareness about health supplements to fuel market

- 18.6.1 MIDDLE EAST

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 B2C PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 19.3 REVENUE ANALYSIS (B2C MARKET), 2022-2024

- 19.4 MARKET SHARE ANALYSIS (B2C MARKET), 2024

- 19.5 MARKET SHARE ANALYSIS (B2B MARKET), 2024

- 19.6 BRAND/PRODUCT COMPARISON

- 19.7 COMPANY EVALUATION MATRIX: B2C COMPANIES, 2024

- 19.7.1 STARS

- 19.7.2 EMERGING LEADERS

- 19.7.3 PERVASIVE PLAYERS

- 19.7.4 PARTICIPANTS

- 19.7.5 COMPANY FOOTPRINT: B2C NUTRACEUTICAL GUMMIES COMPANIES, 2024

- 19.7.5.1 Company footprint

- 19.7.5.2 Regional footprint

- 19.7.5.3 Product type footprint

- 19.7.5.4 Functionality footprint

- 19.8 COMPANY EVALUATION MATRIX: B2B COMPANIES, 2024

- 19.8.1 STARS

- 19.8.2 EMERGING LEADERS

- 19.8.3 PERVASIVE PLAYERS

- 19.8.4 PARTICIPANTS

- 19.8.5 COMPETITIVE BENCHMARKING

- 19.8.5.1 Detailed list of B2B key players

- 19.8.6 COMPETITIVE BENCHMARKING: B2B COMPANIES, 2024

- 19.8.6.1 Competitive benchmarking of key B2B companies

- 19.9 COMPANY VALUATION AND FINANCIAL METRICS

- 19.10 COMPETITIVE SCENARIO

- 19.10.1 PRODUCT LAUNCHES

- 19.10.2 DEALS

- 19.10.3 EXPANSIONS

- 19.10.4 OTHER DEVELOPMENTS

20 COMPANY PROFILES

- 20.1 B2C PLAYERS (BRAND MANUFACTURERS)

- 20.1.1 CHURCH & DWIGHT CO., INC.

- 20.1.1.1 Business overview

- 20.1.1.2 Products/Solutions/Services offered

- 20.1.1.3 Recent developments

- 20.1.1.3.1 Product launches

- 20.1.1.4 MnM view

- 20.1.1.4.1 Key strengths

- 20.1.1.4.2 Strategic choices

- 20.1.1.4.3 Weaknesses and competitive threats

- 20.1.2 H&H GROUP

- 20.1.2.1 Business overview

- 20.1.2.2 Products/Solutions/Services offered

- 20.1.2.3 Recent developments

- 20.1.2.3.1 Deals

- 20.1.2.3.2 Expansions

- 20.1.2.3.3 Other developments

- 20.1.2.4 MnM view

- 20.1.2.4.1 Key strengths

- 20.1.2.4.2 Strategic choices

- 20.1.2.4.3 Weaknesses and competitive threats

- 20.1.3 AMWAY

- 20.1.3.1 Business overview

- 20.1.3.2 Products/Solutions/Services offered

- 20.1.3.3 Recent developments

- 20.1.3.3.1 Product launches

- 20.1.3.3.2 Deals

- 20.1.3.4 MnM view

- 20.1.3.4.1 Key strengths

- 20.1.3.4.2 Strategic choices

- 20.1.3.4.3 Weaknesses and competitive threats

- 20.1.4 BAYER AG

- 20.1.4.1 Business overview

- 20.1.4.2 Products/Solutions/Services offered

- 20.1.4.3 Recent developments

- 20.1.4.3.1 Product launches

- 20.1.4.4 MnM view

- 20.1.4.4.1 Key strengths

- 20.1.4.4.2 Strategic choices

- 20.1.4.4.3 Weaknesses and competitive threats

- 20.1.5 HALEON GROUP OF COMPANIES

- 20.1.5.1 Business overview

- 20.1.5.2 Products/Solutions/Services offered

- 20.1.5.3 Recent developments

- 20.1.5.3.1 Product launches

- 20.1.5.3.2 Deals

- 20.1.5.3.3 Expansions

- 20.1.5.4 MnM view

- 20.1.5.4.1 Key strengths

- 20.1.5.4.2 Strategic choices

- 20.1.5.4.3 Weaknesses and competitive threats

- 20.1.6 NESTLE

- 20.1.6.1 Business overview

- 20.1.6.2 Products/Solutions/Services offered

- 20.1.6.3 Recent developments

- 20.1.6.3.1 Product launches

- 20.1.6.3.2 Deals

- 20.1.6.4 MnM view

- 20.1.6.4.1 Key strengths

- 20.1.6.4.2 Strategic choices

- 20.1.6.4.3 Weaknesses and competitive threats

- 20.1.7 UNILEVER

- 20.1.7.1 Business overview

- 20.1.7.2 Products/Solutions/Services offered

- 20.1.7.3 Recent developments

- 20.1.7.3.1 Product launches

- 20.1.7.3.2 Deals

- 20.1.7.3.3 Expansions

- 20.1.7.4 MnM view

- 20.1.7.4.1 Key strengths

- 20.1.7.4.2 Strategic choices

- 20.1.7.4.3 Weaknesses and competitive threats

- 20.1.8 OTSUKA HOLDINGS CO., LTD.

- 20.1.8.1 Business overview

- 20.1.8.2 Products/Solutions/Services offered

- 20.1.8.3 Recent developments

- 20.1.8.3.1 Product launches

- 20.1.8.3.2 Expansions

- 20.1.8.4 MnM view

- 20.1.8.4.1 Key strengths

- 20.1.8.4.2 Strategic choices

- 20.1.8.4.3 Weaknesses and competitive threats

- 20.1.9 PHARMACARE LABORATORIES

- 20.1.9.1 Business overview

- 20.1.9.2 Products/Solutions/Services offered

- 20.1.9.3 Recent developments

- 20.1.9.3.1 Expansions

- 20.1.9.4 MnM view

- 20.1.10 SWANSON

- 20.1.10.1 Business overview

- 20.1.10.2 Products/Solutions/Services offered

- 20.1.10.3 Recent developments

- 20.1.10.3.1 Product launches

- 20.1.10.4 MnM view

- 20.1.11 IM HEALTHCARE

- 20.1.11.1 Business overview

- 20.1.11.2 Products/Solutions/Services offered

- 20.1.11.3 Recent developments

- 20.1.11.4 MnM view

- 20.1.12 SMP NUTRA

- 20.1.12.1 Business overview

- 20.1.12.2 Products/Solutions/Services offered

- 20.1.12.3 Recent developments

- 20.1.12.4 MnM view

- 20.1.13 NATURE'S TRUTH

- 20.1.13.1 Business overview

- 20.1.13.2 Products/Solutions/Services offered

- 20.1.13.3 Recent developments

- 20.1.13.3.1 Other developments

- 20.1.13.4 MnM view

- 20.1.14 HERBALAND NATURALS INC.

- 20.1.14.1 Business overview

- 20.1.14.2 Products/Solutions/Services offered

- 20.1.14.3 Recent developments

- 20.1.14.4 MnM view

- 20.1.15 BOSCOGEN, INC.

- 20.1.15.1 Business overview

- 20.1.15.2 Products/Solutions/Services offered

- 20.1.15.3 Recent developments

- 20.1.15.4 MnM view

- 20.1.1 CHURCH & DWIGHT CO., INC.

- 20.2 B2B PLAYERS (CONTRACT MANUFACTURERS)

- 20.2.1 SOFGEN PHARMA

- 20.2.1.1 Business overview

- 20.2.1.2 Products/Services/Solutions offered

- 20.2.1.3 Recent developments

- 20.2.1.3.1 Expansions

- 20.2.1.4 MnM view

- 20.2.1.4.1 Key strengths

- 20.2.1.4.2 Strategic choices

- 20.2.1.4.3 Weaknesses & competitive threats

- 20.2.2 CATALENT, INC.

- 20.2.2.1 Business overview

- 20.2.2.2 Products/Services/Solutions offered

- 20.2.2.3 Recent developments

- 20.2.2.3.1 Deals

- 20.2.2.4 MnM view

- 20.2.2.4.1 Key strengths

- 20.2.2.4.2 Strategic choices

- 20.2.2.4.3 Weaknesses & competitive threats

- 20.2.3 ACTIV'INSIDE

- 20.2.3.1 Business overview

- 20.2.3.2 Products/Services/Solutions offered

- 20.2.3.3 Recent developments

- 20.2.3.4 MnM view

- 20.2.3.4.1 Key strengths

- 20.2.3.4.2 Strategic choices

- 20.2.3.4.3 Weaknesses & competitive threats

- 20.2.4 SIRIO PHARMA CO., LTD.

- 20.2.4.1 Business overview

- 20.2.4.2 Products/Services/Solutions offered

- 20.2.4.3 Recent developments

- 20.2.4.3.1 Product launches

- 20.2.4.4 MnM view

- 20.2.5 WIN NUTRA

- 20.2.5.1 Business overview

- 20.2.5.2 Products/Services/Solutions offered

- 20.2.5.3 Recent developments

- 20.2.5.4 MnM view

- 20.2.6 MAKERS NUTRITION, LLC

- 20.2.6.1 Business overview

- 20.2.6.2 Products/Services/Solutions offered

- 20.2.6.3 Recent developments

- 20.2.6.4 MnM view

- 20.2.7 ION LABS

- 20.2.7.1 Business overview

- 20.2.7.2 Products/Services/Solutions offered

- 20.2.7.3 Recent developments

- 20.2.7.3.1 Expansions

- 20.2.7.3.2 Deals

- 20.2.7.4 MnM view

- 20.2.8 VITAJOY GROUP

- 20.2.8.1 Business overview

- 20.2.8.2 Products/Services/Solutions offered

- 20.2.8.3 Recent developments

- 20.2.8.4 MnM view

- 20.2.9 BLISS LIFESCIENCES LLP

- 20.2.9.1 Business overview

- 20.2.9.2 Products/Services/Solutions offered

- 20.2.9.3 Recent developments

- 20.2.9.4 MnM view

- 20.2.10 GLOBAL WIDGET

- 20.2.10.1 Business overview

- 20.2.10.2 Products/Services/Solutions offered

- 20.2.10.3 Recent developments

- 20.2.10.3.1 Product launches

- 20.2.10.3.2 Deals

- 20.2.10.3.3 Expansions

- 20.2.10.4 MnM view

- 20.2.11 GUMMY WORLDS

- 20.2.12 TOPGUM

- 20.2.13 MERICAL

- 20.2.14 FERMENTIS LIFE SCIENCES

- 20.2.15 EAGLE LABS, INC.

- 20.2.1 SOFGEN PHARMA

21 RESEARCH METHODOLOGY

- 21.1 RESEARCH DATA

- 21.1.1 SECONDARY DATA

- 21.1.1.1 Key data from secondary sources

- 21.1.2 PRIMARY DATA

- 21.1.2.1 Key industry insights

- 21.1.2.2 Breakdown of primary interviews

- 21.1.2.3 Primary sources

- 21.1.1 SECONDARY DATA

- 21.2 MARKET SIZE ESTIMATION

- 21.2.1 NUTRACEUTICAL GUMMIES MARKET SIZE ESTIMATION: SUPPLY SIDE

- 21.2.2 NUTRACEUTICAL GUMMIES MARKET SIZE ESTIMATION: DEMAND SIDE

- 21.2.3 NUTRACEUTICAL GUMMIES MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 21.2.4 NUTRACEUTICAL GUMMIES MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 21.3 DATA TRIANGULATION

- 21.4 RESEARCH ASSUMPTIONS

- 21.5 RESEARCH LIMITATIONS

22 ADJACENT & RELATED MARKETS

- 22.1 INTRODUCTION

- 22.2 LIMITATIONS

- 22.3 NUTRACEUTICAL INGREDIENTS MARKET

- 22.3.1 MARKET DEFINITION

- 22.3.2 MARKET OVERVIEW

- 22.4 DIETARY SUPPLEMENTS MARKET

- 22.4.1 MARKET DEFINITION

- 22.4.2 MARKET OVERVIEW

23 APPENDIX

- 23.1 DISCUSSION GUIDE

- 23.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 23.3 CUSTOMIZATION OPTIONS

- 23.4 RELATED REPORTS

- 23.5 AUTHOR DETAILS