|

시장보고서

상품코드

1950784

알레르기 진단 시장 : 제품 및 서비스별, 검사 유형별, 알레르겐별, 최종 사용자별, 지역별 예측(-2031년)Allergy Diagnostic Market by Product & Service (Consumables, Instruments [Immunoassay Analyzers, Luminometers]), Test Type (In Vivo Tests, In Vitro Tests), Allergen (Food Allergens), End User (Hospital-Based Laboratories) - Global Forecast to 2031 |

||||||

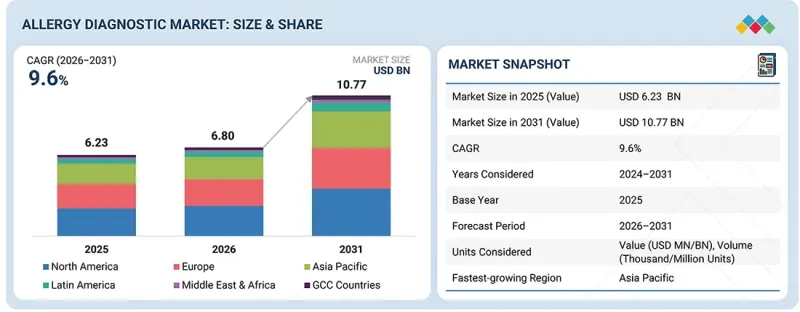

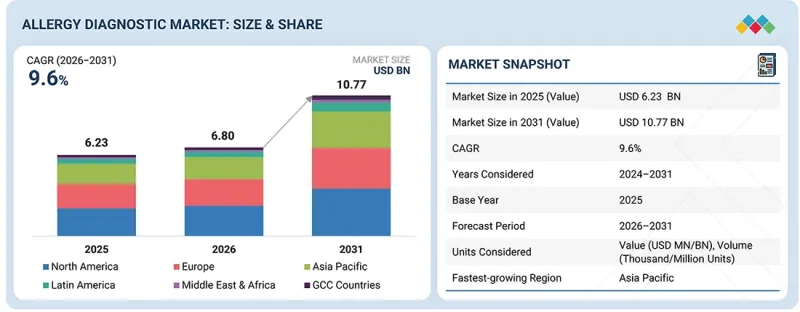

알레르기 진단 시장 규모는 예측 기간 동안 CAGR 9.6%로 성장할 전망이며, 2025년 68억 달러에서 2030년에는 107억 7,000만 달러에 이를 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 서비스별, 검사 유형별, 알레르겐별, 최종 사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

알레르기 진단의 기술 혁신은 성장의 주요 추진력이며 검사를 보다 정확하고 신속하며 종합적으로 하고 있습니다. 피부 프릭 테스트(SPT) 및 단일 알레르겐 혈청 IgE 검사와 같은 기존의 진단 방법은 여전히 유용하지만, 다중 면역 측정법, 성분 분해 진단(CRD), 분자 알레르로지 등과 같은 첨단 플랫폼은 여러 측면에서 이들을 능가하고 있습니다. 멀티플렉스 플랫폼은 단일 시료에서 수십, 심지어 수백 알레르겐에 대한 IgE 반응을 동시에 감지하여 환자의 시간, 비용 및 노력을 줄일 수 있습니다. CRD는 한 걸음 더 나아가 감작을 일으키는 알레르겐에서 정확한 단백질 분자를 확인합니다. 이것은 검사의 임상적 유용성과 위험 계층화를 향상시킵니다. 예를 들어 무해한 꽃가루 감작과 심각한 반응의 예측 인자가 되는 교차 반응성을 구별할 수 있습니다.

분자 진단은 맞춤형 의료에서도 중요한 역할을 합니다. 개별 감작 프로파일 맵을 생성하고 의사가 면역 요법의 맞춤형 치료에 활용합니다. 자동화 및 전자건강기록의 디지털 연계는 임상실의 업무 프로세스를 효율화하고 대규모 스크리닝 프로그램을 실시하는 데도 도움이 됩니다. 의사의 진료소와 약국에서 신속한 결과를 제공하는 POC(Point of Care) 기술 혁신은 환자의 편의성 및 의료 효율성을 향상시킵니다. 또한 복잡한 알레르겐 프로파일의 해석을 지원하는 AI 탑재 해석 툴의 개발도 진행되고 있습니다. 이러한 기술 혁신은 검사 성능과 환자 경험을 향상시킬 뿐만 아니라 진단 정밀도가 표준 치료가 되는 장기적인 시장 확대를 의미합니다.

제품 및 서비스별로 보면 알레르기 질환의 세계 증가가 알레르기 진단 시장에서 소모품이 주요 점유율을 차지하는 이유로 꼽힙니다. 도시의 폭발적 성장, 환경 악화, 생활 양식의 변화, 식습관의 변천, 지구 온난화 등의 복합 요인에 의해 음식 알레르기, 알레르기성 비염, 천식, 아토피 피부염 증가가 초래되고 있습니다. 이에 따라 환자 수가 증가함에 따라 특히 소모품에 대한 의존도가 높은 실험실 기반 체외 진단 검사를 중심으로 진단 검사 건수가 증가하고 있습니다. 각 진단 에피소드에는 많은 시약과 알레르겐 특이적 키트가 필요하므로 소모품에 대한 수요가 더욱 증가합니다. 게다가 소아 및 노인층은 알레르기의 영향을 가장 받기 쉽고 반복 검사 및 확정 검사가 필요한 경우가 많기 때문에 소모품은 세계적으로 특히 아시아태평양과 신흥 시장에서 질병 부담이 증대하는 가운데 가장 직접적인 영향을 받고 가장 빠르게 성장하는 수익원으로 계속되고 있습니다.

검사 유형별로 생체내 검사의 보급을 강력하게 뒷받침하는 요인 중 하나는 환자가 1회의 방문으로 15-30분 이내에 검사 결과를 얻을 수 있다는 것입니다. 이러한 즉각적인 피드백을 통해 의사는 알레르기를 확인하고, 환자에게 조언을 하며, 치료 계획을 즉시 시작할 수 있습니다. 생체 내 검사는 검사실에서의 처리를 필요로 하고 더 긴 소요시간을 필요로 하는 생체외 검사와 비교하여 신속한 진단을 수반하는 훨씬 효율적인 워크플로우를 제공합니다. 환자 만족도 외에 신속한 진단은 환자의 재방문을 줄이는 점에서도 중요하며, 이러한 요인이 외래 진료소와 병원 환경에서의 검사의 매력을 높여 결과적으로 이러한 검사의 이용률과 시장 점유율의 향상으로 이어지고 있습니다.

알레르기 진단 시장에서 북미는 가장 큰 점유율을 차지합니다. 북미는 진보된 의료 생태계를 가지고 있으며, 알레르기 진단의 광범위한 활용을 강력하게 추진하고 있습니다. 이 지역에는 첨단 검사 장비를 갖춘 다양한 병원, 전문 알레르기 클리닉, 진단실험실, 기준 검사실이 충실합니다. 자동 면역 측정 장치, 다중 검사 시스템, 집중 검사 서비스의 존재는 높은 검사 정확성 및 신속성을 보장합니다. 또한 진단이 임상 워크플로에 매우 잘 통합되어 있기 때문에 의사는 표준 치료로 알레르기 검사를 쉽게 지시할 수 있어 시장 리더의 이점을 뒷받침합니다.

알레르기 진단 시장의 주요 기업으로는 Thermo Fisher Scientific Inc.(US), Siemens Healthineers AG(Germany), Danaher Corporatio(US), Minaris Medical America, Inc.(US), Omega Diagnostics Group Plc(UK), bioMerieux SA(France), Romer Labs Division Holding (Austria), EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG (Germany), HollisterStier Allergy (US), Eurofins Scientific (Luxembourg) 및 Stallergenes Greer (UK) 등이 있습니다.

조사 대상

이 보고서는 알레르기 진단 시장을 평가하고 제품 및 서비스, 검사 유형, 알레르기 항원, 최종 사용자, 지역 등 다양한 부문에서의 규모 및 미래 성장 가능성을 추정합니다. 또한 이 시장에서 주요 기업의 경쟁 분석, 기업 프로파일, 제품 제공, 최근 동향, 주요 시장 전략에 대해 설명합니다.

이 보고서를 구입하는 이유

이 보고서는 전체 알레르기 진단 시장 및 그 하위 부문의 예상 수익 금액에 대한 귀중한 데이터를 제공하며 시장의 리더 기업 및 신규 진출 기업 모두에게 유용합니다. 이해관계자는 경쟁 환경을 이해하고, 비즈니스를 효과적으로 배치하며, 적절한 시장 진출 전략을 수립하는 인사이트를 얻는 데 도움이 됩니다. 또한 이 보고서는 시장의 주요 촉진요인, 과제, 장애, 기회 등 시장 동향에 대한 이해를 이해 관계자에게 제공합니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(알레르기 질환의 높은 이환율 및 무거운 경제적 부담, 알레르기에 대한 인식의 고조, 환경 오염 수준 상승, 건강 보험 제도에 있어서 알레르기 진단의 적용 범위) 분석, 제약 요인(알레르기 진단 기기의 고액의 비용, 알레르기 검사 방법에 관한 지식 부족 및 실시 미비, 의료 서비스에 대한 액세스 제한), 기회(의료 서비스에 대한 액세스 제한, 알레르기 진단에 있어서 인공지능 통합), 과제(알레르기 전문의의 부족 및 연수 프로그램 부족, 알레르기 환자에 있어서 진단상의 과제)

- 제품 강화 및 혁신 : 세계의 알레르기 진단 시장에 있어서 제품 발매의 상세 정보 및 예측되는 동향

- 시장 개발 : 제품 및 서비스별, 검사종별, 알레르겐별, 최종 사용자별, 지역별로 수익성이 높은 성장 시장에 대한 상세한 지견 및 분석

- 시장 다양화 : 세계의 알레르기 진단 시장에서 신제품 출시, 시장 확대, 최신 동향, 투자 동향에 관한 종합적인 정보

- 경쟁 평가 : 세계의 알레르기 진단 시장에서 주요 경쟁사 시장 점유율, 성장 계획, 제공 제품, 생산 능력에 대한 철저한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 중요 인사이트

제4장 시장 개요

- 시장 역학

- 성장 촉진요인

- 성장 억제요인

- 기회

- 과제

- 미충족 요구 및 화이트 스페이스

- 상호접속된 시장 및 분야 간 기회

- Tier 1/2/3 기업의 전략적 움직임

제5장 업계 동향

- Porter's Five Forces 분석

- 거시경제 전망

- 공급망 분석

- 밸류체인 분석

- 생태계 분석

- 가격 분석

- 무역 분석

- 주된 회의 및 이벤트(2026-2027년)

- 고객의 비즈니스에 영향을 미치는 동향 및 혼란

- 투자 및 자금 조달 시나리오

- 사례 연구 분석

- 미국 관세가 알레르기 진단 시장에 미치는 영향(2025년)

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 장래 용도

- 주요 신기술

- 보완적 기술

- 기술 및 제품 로드맵

- 특허 분석

- 미래의 용도

- AI 및 생성형 AI가 알레르기 진단 시장에 미치는 영향

제7장 규제 상황

- 지역 규제 및 규정 준수

- 규제 기관, 정부 기관, 기타 조직

- 업계 표준

제8장 고객 정세 및 구매 행동

- 의사결정 프로세스

- 주요 이해관계자 및 구매 평가 기준

- 채용 장벽 및 내부 과제

- 다양한 최종 이용 산업으로부터의 미충족 요구

- 시장 수익성

제9장 알레르기 진단 시장 : 제품 및 서비스별

- 소모품

- 장치

- 서비스

제10장 알레르기 진단 시장 : 검사 유형별

- 생체내 검사

- 체외 검사

제11장 알레르기 진단 시장 : 알레르겐별

- 흡입 알레르겐

- 식품 알레르겐

- 약물 알레르겐

- 기타

제12장 알레르기 진단 시장 : 최종 사용자별

- 원내 검사실

- 진단실험실

- 학술연구기관

- 기타

제13장 알레르기 진단 시장 : 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타

- 라틴아메리카

- 브라질

- 멕시코

- 기타

- 중동 및 아프리카

- GCC 국가

- 의료비 증가가 시장 성장 가속

제14장 경쟁 구도

- 주요 진입 기업의 전략 및 강점

- 수익 분석(2021-2025년)

- 시장 점유율 분석

- 기업 평가 매트릭스 : 주요 진입 기업(2025년)

- 경쟁력 평가 매트릭스 : 스타트업 및 중소기업(2025년)

- 기업 평가 및 재무지표

- 브랜드 및 제품 비교

- 경쟁 시나리오

제15장 기업 프로파일

- 주요 진출기업

- THERMO FISHER SCIENTIFIC INC.

- DANAHER CORPORATION

- SIEMENS HEALTHINEERS AG

- CANON, INC.(MINARIS MEDICAL AMERICA, INC.)

- REVVITY, INC.(EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG)

- EUROFINS SCIENTIFIC

- BIOMERIEUX SA

- DSM ROYAL(ROMER LABS DIVISION HOLDING GMBH)

- HOLLISTERSTIER ALLERGY(JUBILANT PHARMA)

- OMEGA DIAGNOSTICS GROUP PLC

- STALLERGENES GREER LTD.

- 기타 기업

- HOB BIOTECH GROUP CORP., LTD.

- HYCOR BIOMEDICAL

- LINCOLN DIAGNOSTICS, INC.

- R-BIOPHARM AG

- ASTRA BIOTECH GMBH

- ERBA GROUP

- AESKU.GROUP GMBH

- ACON LABORATORIES, INC.

- ALCIT INDIA PVT. LTD.

- BIOPANDA REAGENTS LTD.

- BIOSIDE SRL

- CREATIVE DIAGNOSTIC MEDICARE PVT. LTD.

- DST DIAGNOSTISCHE SYSTEME & TECHNOLOGIEN GMBH

- DR. FOOKE LABORATORIEN GMBH

제16장 조사 방법

제17장 부록

AJY 26.03.05The allergy diagnostic market is projected to reach USD 10.77 billion by 2030 from USD 6.80 billion in 2025, at a CAGR of 9.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product & Service, Test Type, Allergen, End user, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

Technological innovation in allergy diagnostics is a key driver of growth, making testing more accurate, faster, and comprehensive. Traditional diagnostic methods such as skin prick tests (SPT) and single, allergen blood IgE tests are still of use, but the advanced platforms like multiplex immunoassays, component resolved diagnostics (CRD), and molecular allergology have surpassed them in a variety of ways. Multiplex platforms allow simultaneous detection of IgE responses to dozens or even hundreds of allergens in a single sample, thereby decreasing the time, cost, and effort for the patient. CRD is a step further in that it pinpoints the exact protein molecules within the allergens that are the cause of sensitization, thus increasing how clinically relevant the test is and risk stratification; e.g. , it can differentiate between innocent pollen sensitization and cross-reactivity that is a predictor of severe reactions.

Molecular diagnostics are also instrumental in personalized medicine-they generate the individual sensitization profile map, which doctors use for the personalization of immunotherapy treatments. Automation and digital integration with electronic health records facilitate the working processes in clinical laboratories and are also of assistance when it comes to undertaking large-scale screening programs. Point-of-care (POC) innovations that deliver quick results right in doctors' or pharmacies' offices enhance patients' convenience and the effectiveness of medical care. Apart from that, AI-powered interpretation tools are being developed to help doctors make sense of complicated allergen profiles. Such technological innovations not only improve test performance and patient experience but also represent a long-term market expansion in which diagnostic precision becomes the standard of care.

Based on product & service: The global increase in allergic diseases is a significant factor that explains why consumables have the leading share in the allergy diagnostic market. A combination of factors such as the explosive growth of cities, the deterioration of the environment, alterations in lifestyles, changes in diet, and global warming has, among other things, led to a rise in food allergies, allergic rhinitis, asthma, and atopic dermatitis. Correspondingly, the growing patient population results in higher diagnostic testing volumes, particularly laboratory-based in vitro tests, which are highly dependent on consumables. Numerous reagents and allergen-specific kits are required for each diagnostic episode; thus, the demand for consumables is further increased. Besides that, both children and elderly pediatric and geriatric populations are among the most susceptible to allergies and, therefore, often necessitate repeated and confirmatory tests. Consumables remain the most directly affected and fastest-growing source of revenue as the disease burden escalates worldwide, especially in the Asia Pacific and emerging markets.

Based on test type: A powerful incentive for the widespread adoption of in vivo testing, among other things, is the possibility of delivering test results within 15-30 minutes during a single patient visit. Such instant feedback enables doctors to identify allergies, advise patients, and start therapy plans right away. In vivo tests offer a workflow that is much more efficient, with rapid diagnosis compared to in vitro tests, which are subjected to laboratory processing and require a longer turnaround time. Besides patient satisfaction, fast diagnosis is important because it reduces patient revisits, both of which factors make the tests more appealing to outpatient clinics and hospital settings, thereby leading to higher utilization and market share for these tests.

North America holds the largest market share in the allergy diagnostic market. The North American region has a sophisticated healthcare ecosystem that strongly promotes the use of allergy diagnostics at scale. The area is well-equipped with a variety of hospitals, specialty allergy clinics, diagnostic laboratories, and reference labs equipped with advanced testing equipment. The presence of automated immunoassay analyzers, multiplex testing systems, and centralized lab services ensures high test accuracy and speed. In addition, the diagnostics are so well integrated into clinical workflows that doctors can easily order allergy tests as standard of care, thereby supporting the market leader's dominance.

A breakdown of the primary participants (supply-side) for the allergy diagnostic market referred to in this report is provided below:

- By Company Type: Tier 1: 34%, Tier 2: 38%, and Tier 3: 28%

- By Designation: C-level: 26%, Director Level: 35%, and Others: 39%

- By Region: North America: 35%, Europe: 30%, Asia Pacific: 25%, Latin America: 6%, Middle East & Africa: 2%, GCC Countries: 3%

Prominent players in the allergy diagnostic market are Thermo Fisher Scientific Inc. (US), Siemens Healthineers AG (Germany), Danaher Corporation (US), Minaris Medical America, Inc. (US), Omega Diagnostics Group Plc (UK), bioMerieux SA (France), Romer Labs Division Holding (Austria), EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG (Germany), HollisterStier Allergy (US), Eurofins Scientific (Luxembourg), and Stallergenes Greer (UK), among others.

Research Coverage

The report evaluates the allergy diagnostic market and estimates its size and future growth potential across various segments, including product & service, test type, allergen, end user, and region. The report also includes a competitive analysis of the major players in this market, along with company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report provides valuable data on estimated revenue figures for the overall allergy diagnostic market and its subsegments, benefiting both market leaders and new entrants. It helps stakeholders understand the competitive landscape and gain insights for effectively positioning their businesses and developing appropriate go-to-market strategies. Additionally, the report offers stakeholders an understanding of market trends, including key drivers, challenges, obstacles, and opportunities within the market.

This report provides insights into the following points:

- Analysis of key drivers (High incidence and heavy economic burden of allergic diseases, Increasing awareness about allergies, Rising environmental pollution levels, Coverage of allergy diagnosis under health insurance schemes), restraints (Premium cost of allergy diagnostic instruments, Lack of adequate knowledge and poor implementation of allergy testing methods, Limited access to healthcare services), opportunities (Limited access to healthcare services, Integration of artificial intelligence in allergy diagnosis), and challenges (Shortage of allergists and lack of training programs, Diagnostic challenges in allergic patients)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global allergy diagnostic market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product & service, test type, allergen, end user, and region

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global allergy diagnostic market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global allergy diagnostic market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ALLERGY DIAGNOSTIC MARKET OVERVIEW

- 3.2 ASIA PACIFIC: ALLERGY DIAGNOSTIC MARKET, BY END USER AND COUNTRY

- 3.3 ALLERGY DIAGNOSTIC MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 ALLERGY DIAGNOSTIC MARKET: REGIONAL MIX

- 3.5 ALLERGY DIAGNOSTIC MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 High incidence and heavy economic burden of allergic diseases

- 4.2.1.2 Increasing awareness about allergies

- 4.2.1.3 Rising environmental pollution levels

- 4.2.1.4 Coverage of allergy diagnosis under health insurance schemes

- 4.2.2 RESTRAINTS

- 4.2.2.1 Premium cost of allergy diagnostic instruments

- 4.2.2.2 Lack of adequate knowledge and poor implementation of allergy testing methods

- 4.2.2.3 Limited access to healthcare services

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Use of mHealth in allergy diagnosis

- 4.2.3.2 Integration of artificial intelligence in allergy diagnosis

- 4.2.4 CHALLENGES

- 4.2.4.1 Shortage of allergists and lack of training programs

- 4.2.4.2 Diagnostic challenges in allergic patients

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS IN ALLERGY DIAGNOSTIC MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL IVD INDUSTRY

- 5.2.4 TRENDS IN GLOBAL IMMUNOASSAY INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF ALLERGY DIAGNOSTIC PRODUCTS, BY PRODUCT & SERVICE, 2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF ALLERGY DIAGNOSTIC PRODUCTS, BY REGION, 2024-2026

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 902750, 2020-2024

- 5.7.2 EXPORT DATA FOR HS CODE 902750, 2020-2024

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 EXPANDING ACCESS TO ALLERGY DIAGNOSTICS IN EMERGING MARKETS

- 5.11.2 SCALING HIGH-THROUGHPUT ALLERGY TESTING IN CENTRALIZED LABORATORIES

- 5.11.3 IMPROVING PEDIATRIC ALLERGY DIAGNOSIS THROUGH MULTIPLEX TESTING

- 5.12 IMPACT OF 2025 US TARIFF ON ALLERGY DIAGNOSTIC MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 END-USE INDUSTRY IMPACT

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 SPECIFIC IGE IMMUNOASSAYS

- 6.1.2 SKIN PRICK TESTING (SPT)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED IMMUNOASSAY ANALYZERS

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 ADVANCED MULTIPLEX AND PERSONALIZED ALLERGY DIAGNOSTICS

- 6.5.2 DIGITAL & AI-ENABLED ALLERGY MONITORING PLATFORMS

- 6.5.3 AI-INTEGRATED DIGITAL SURGICAL ECOSYSTEMS FOR IOLS

- 6.6 IMPACT OF AI/GEN AI ON ALLERGY DIAGNOSTIC MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 CASE STUDIES OF AI IMPLEMENTATION

- 6.6.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 ALLERGY DIAGNOSTIC MARKET, BY PRODUCT & SERVICE

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 RECURRENT USE OF CONSUMABLES FOR ALLERGY DIAGNOSTICS TO DRIVE MARKET

- 9.3 INSTRUMENTS

- 9.3.1 IMMUNOASSAY ANALYZERS

- 9.3.1.1 High preference for testing to boost market demand

- 9.3.2 LUMINOMETERS

- 9.3.2.1 Convenience and ease of use to propel market growth

- 9.3.3 OTHER INSTRUMENTS

- 9.3.1 IMMUNOASSAY ANALYZERS

- 9.4 SERVICES

- 9.4.1 RISING NEED TO ENSURE EFFECTIVE UTILIZATION OF ALLERGY DIAGNOSTIC PRODUCTS TO SUPPORT MARKET GROWTH

10 ALLERGY DIAGNOSTIC MARKET, BY TEST TYPE

- 10.1 INTRODUCTION

- 10.2 IN VIVO TESTS

- 10.2.1 SKIN PRICK TESTS

- 10.2.1.1 Skin prick tests to be most widely preferred in vivo allergy tests

- 10.2.2 PATCH TESTS

- 10.2.2.1 Rapid diagnosis of contact dermatitis to boost market demand

- 10.2.3 OTHER IN VIVO TESTS

- 10.2.1 SKIN PRICK TESTS

- 10.3 IN VITRO TESTS

- 10.3.1 ABILITY TO IDENTIFY ALLERGEN-SPECIFIC IGE MOLECULES IN PATIENT SERUM TO DRIVE MARKET

11 ALLERGY DIAGNOSTIC MARKET, BY ALLERGEN

- 11.1 INTRODUCTION

- 11.2 INHALED ALLERGENS

- 11.2.1 HIGH INCIDENCE OF ASTHMA TO BOOST MARKET GROWTH

- 11.3 FOOD ALLERGENS

- 11.3.1 HIGH PREVALENCE OF FOOD-RELATED ALLERGIES AMONG YOUNG CHILDREN TO SUPPORT MARKET GROWTH

- 11.4 DRUG ALLERGENS

- 11.4.1 INCREASING INCIDENCE OF DRUG ALLERGIES AND ADVERSE REACTIONS TO DRIVE MARKET

- 11.5 OTHER ALLERGENS

12 ALLERGY DIAGNOSTIC MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITAL-BASED LABORATORIES

- 12.2.1 HOSPIATAL-BASED LABORATORIES TO BE MORE ACCESSIBLE TO PATIENTS AND OFFER RAPID RESULTS

- 12.3 DIAGNOSTIC LABORATORIES

- 12.3.1 DIAGNOSTIC LABORATORIES TO PIVOTAL FOR DIAGNOSIS AND MANAGEMENT OF ALLERGIES

- 12.4 ACADEMIC RESEARCH INSTITUTES

- 12.4.1 RISING NUMBER OF INSTITUTES FOR ALLERGY TESTING TRAINING TO SUPPORT MARKET GROWTH

- 12.5 OTHER END USERS

13 ALLERGY DIAGNOSTIC MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 US to dominate North American allergy diagnostic market

- 13.2.2 CANADA

- 13.2.2.1 Rising funding activities in allergy diagnostics to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Increasing prevalence of allergic conditions and rising presence of allergy diagnostic product manufacturers to aid market growth

- 13.3.2 UK

- 13.3.2.1 Increasing prevalence of food anaphylaxis to support market growth

- 13.3.3 FRANCE

- 13.3.3.1 Increasing reimbursements for allergy testing to spur market growth

- 13.3.4 ITALY

- 13.3.4.1 Presence of allergy diagnostic organizations to support increased demand for products

- 13.3.5 SPAIN

- 13.3.5.1 Government initiatives and healthcare infrastructural development to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rising allergy prevalence and growing research activities to augment market growth

- 13.4.2 JAPAN

- 13.4.2.1 Increasing prevalence of allergies among children to propel demand for allergy diagnostics

- 13.4.3 INDIA

- 13.4.3.1 Limited awareness regarding allergy management to limit market growth

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Rising allergy burden and high diagnostic uptake to fuel South Korean market growth

- 13.4.5 AUSTRALIA

- 13.4.5.1 High prevalence of food allergies and major lifestyle changes to drive market

- 13.4.6 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 High prevalence of childhood asthma to augment market growth

- 13.5.2 MEXICO

- 13.5.2.1 Growing focus on awareness training programs to boost market demand

- 13.5.3 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.7 GCC COUNTRIES

- 13.7.1 RISING HEALTHCARE SPENDING TO SPUR MARKET GROWTH

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Product & service footprint

- 14.5.5.4 Test type footprint

- 14.5.5.5 Allergen footprint

- 14.6 COMPETITIVE EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.6.5.1 Detailed list of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of startups/SMEs

- 14.7 COMPANY VALUATION & FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.8 BRAND/PRODUCT COMPARISON

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES & APPROVALS

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches & approvals

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 DANAHER CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 MnM view

- 15.1.2.3.1 Right to win

- 15.1.2.3.2 Strategic choices

- 15.1.2.3.3 Weaknesses & competitive threats

- 15.1.3 SIEMENS HEALTHINEERS AG

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 MnM view

- 15.1.3.3.1 Right to win

- 15.1.3.3.2 Strategic choices

- 15.1.3.3.3 Weaknesses & competitive threats

- 15.1.4 CANON, INC. (MINARIS MEDICAL AMERICA, INC.)

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 REVVITY, INC. (EUROIMMUN MEDIZINISCHE LABORDIAGNOSTIKA AG)

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 EUROFINS SCIENTIFIC

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Expansions

- 15.1.7 BIOMERIEUX SA

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.8 DSM ROYAL (ROMER LABS DIVISION HOLDING GMBH)

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 HOLLISTERSTIER ALLERGY (JUBILANT PHARMA)

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.10 OMEGA DIAGNOSTICS GROUP PLC

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.11 STALLERGENES GREER LTD.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.2 OTHER PLAYERS

- 15.2.1 HOB BIOTECH GROUP CORP., LTD.

- 15.2.2 HYCOR BIOMEDICAL

- 15.2.3 LINCOLN DIAGNOSTICS, INC.

- 15.2.4 R-BIOPHARM AG

- 15.2.5 ASTRA BIOTECH GMBH

- 15.2.6 ERBA GROUP

- 15.2.7 AESKU.GROUP GMBH

- 15.2.8 ACON LABORATORIES, INC.

- 15.2.9 ALCIT INDIA PVT. LTD.

- 15.2.10 BIOPANDA REAGENTS LTD.

- 15.2.11 BIOSIDE S.R.L.

- 15.2.12 CREATIVE DIAGNOSTIC MEDICARE PVT. LTD.

- 15.2.13 DST DIAGNOSTISCHE SYSTEME & TECHNOLOGIEN GMBH

- 15.2.14 DR. FOOKE LABORATORIEN GMBH

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Objectives of primary research

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of primaries

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 SUPPLY-SIDE ANALYSIS (REVENUE SHARE ANALYSIS)

- 16.2.2 COMPANY INVESTOR PRESENTATIONS AND PRIMARY INTERVIEWS

- 16.2.3 TOP-DOWN APPROACH

- 16.2.4 DEMAND-SIDE ANALYSIS

- 16.3 DATA TRIANGULATION

- 16.4 MARKET SHARE ESTIMATION

- 16.5 STUDY ASSUMPTIONS

- 16.6 RISK ANALYSIS

- 16.7 RESEARCH LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS. SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS