|

시장보고서

상품코드

1961006

황산암모늄 시장 예측(-2030년) : 유형별, 용도별, 지역별Ammonium Sulfate Market by Type (Solid, Liquid), Application (Fertilizers, Pharmaceuticals, Food & Feed Additives, Water Treatment, Textile Dyeing, Other Applications), and Region - Global Forecast to 2030 |

||||||

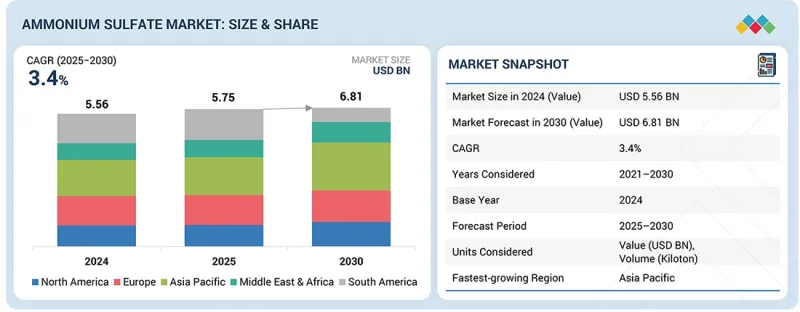

황산암모늄 시장 규모는 예측 기간 중 CAGR 3.4%로 성장하며, 2025년 57억 5,000만 달러에서 2030년까지 68억 1,000만 달러에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 대상 단위 | 가치(10억 달러) 양(킬로톤) |

| 부문 | 유형별, 용도별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

환경 규제 강화, 효율적인 영양 관리에 대한 관심 증가, 황 및 질소 기반 투입물에 대한 산업 수요 증가는 농업, 화학, 수처리, 배출가스 제어 분야에서 황산암모늄에 대한 지속적인 수요를 촉진하고 있습니다.

고체 부문은 예측 기간 중 황산암모늄 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 이는 주로 취급의 용이성, 저장 용량 및 대량 배송 시스템에 대한 적합성 때문입니다. 고체 황산암모늄은 각 봉지마다 일관된 영양소 함량을 제공하고 다른 제품과 쉽게 혼합할 수 있으므로 농업 및 산업 분야 모두에서 선호되는 선택입니다. 또한 잘 구축된 물류 인프라와 전 세계 소비자의 광범위한 수용성은 예측 기간 중 지속적이고 큰 폭 수요 성장을 가속할 것입니다.

식품 및 사료첨가제 부문은 식품 등급 산도 조절제, 반죽 개량제, 효모 영양 공급원으로서의 용도에 힘입어 예측 기간 중 두 번째 시장 점유율을 차지할 것으로 예측됩니다. 또한 황산암모늄은 동물 영양 분야에서 단백질 합성을 촉진하고, 사료 효율을 개선하며, 동물의 종합적인 생산성을 향상시키는 데 활용되고 있습니다. 축산물 생산 증가와 고품질 규제 준수에 대한 지속적인 노력에 힘입어 가공식품 시장의 성장은 식품 및 사료첨가제 시장에서 황산암모늄에 대한 수요를 증가시킬 것입니다.

아시아태평양은 급속한 인구 증가, 식량 섭취량 증가, 식품 및 사료용 동물의 대규모 생산에 따른 농가, 식품 가공업체 및 다양한 산업 분야의 사용자로부터의 큰 수요로 인해 예측 기간 중 황산암모늄 시장에서 가장 큰 점유율을 차지할 것으로 예측됩니다. 또한 화학, 섬유, 수처리, 배출가스 제어 산업 등 비농업 사용자로부터도 질소와 황에 대한 큰 수요가 예상됩니다. 다수의 생산자를 보유하고 저렴한 원료를 효율적으로 조달할 수 있는 능력을 갖춘 아시아태평양은 황산암모늄의 세계 최대 시장으로서 지배적인 지위를 유지할 것입니다.

대상 기업 - BASF(독일), Evonik Industries AG(독일), LANXESS(독일), AdvanSix(미국), Sumitomo Chemical(일본), OCI Global(네덜란드), Domo Chemicals(벨기에), Nutrien Ltd.(캐나다), China Petrochemical Development Corporation(중국), Martin Midstream Partners(미국)

황산암모늄(Ammonium Sulfate) 시장의 주요 기업에 대해 기업 개요, 최근 동향, 주요 시장 전략 등 상세한 경쟁 분석을 실시했습니다.

조사 대상

이 보고서는 황산암모늄 시장을 유형(고체, 액체), 용도(비료, 의약품, 식품 및 사료첨가제, 수처리, 섬유 염색, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)에 따라 분류하여 조사했습니다. 이 보고서의 조사 범위는 황산암모늄 시장의 성장에 영향을 미치는 촉진요인, 제약 요인, 과제 및 성장 기회에 대한 자세한 정보를 다룹니다. 주요 산업 기업에 대한 상세한 분석을 실시하여 사업 개요, 제공 제품 및 황산암모늄 시장과 관련된 제휴 및 협력 관계, 제품 출시, 사업 확장, 인수 등의 주요 전략에 대한 인사이트을 제공합니다. 이 보고서는 황산암모늄 시장 생태계의 신흥 스타트업 기업의 경쟁 분석도 다루고 있습니다.

이 보고서 구매 이유

이 보고서는 시장 리더와 신규 시장 진출기업에게 전체 황산암모늄 시장 및 하위 부문의 매출 수치에 대한 가장 정확한 추정치를 제공합니다. 이해관계자들이 경쟁 구도를 이해하고, 자사의 포지셔닝에 대한 인사이트을 높이고, 적절한 시장 진출 전략을 수립하는 데 도움이 될 것입니다. 시장 동향을 파악하고, 주요 시장 성장 촉진요인, 억제요인, 과제, 기회에 대한 정보를 제공합니다.

이 보고서는 다음 사항에 대한 인사이트을 제공

주요 촉진요인 분석(영양 균형 개선 프로그램에 따른 황 함유 질소 비료로의 구조적 전환, 카프로락탐 및 나일론 6 밸류체인의 지속적인 수요, 산업용 수처리 및 폐수 관리에서의 사용 확대), 억제요인(생산 경로 간 품질 변동, 혼합 및 맞춤형 복합 비료와의 경쟁), 기회(과립화 및 압축을 통한 지역 특화 질소-황 비율 개발, 단백질 정제를 위한 제약 및 생명공학용 황산암모늄 공급), 과제(비료, 화학물질, 환경 규제 프레임워크의 분절적 규제 대응, 업스트림 원료 가격 및 산업 연계에 따른 가격 변동성)에 대해 분석했습니다. 분석합니다.

- 제품 개발/혁신 : 황산암모늄 시장의 향후 기술 동향, 연구개발 활동, 제품 및 서비스 출시에 대한 상세한 분석.

- 시장 개발: 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 황산암모늄 시장을 분석합니다.

시장 다각화 : 황산암모늄 시장의 신제품 및 서비스, 미개발 지역, 최근 동향, 투자에 대한 종합적인 정보.

- 경쟁 평가 : BASF(독일), Evonik Industries AG(독일), LANXESS(독일), AdvanSix(미국), Sumitomo Chemical Co., Ltd.(일본), OCI Global(네덜란드), Domo Chemicals(벨기에), Nutrien Ltd.(캐나다), China Petrochemical Development Corporation(중국), Martin Midstream Partners(미국) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대해 상세한 평가를 시행합니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털, AI의 도입에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 황산암모늄 시장(유형별)

제10장 황산암모늄 시장(용도별)

제11장 황산암모늄 시장(지역별)

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

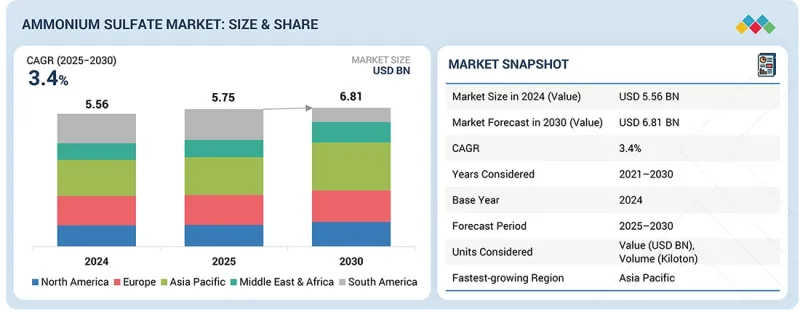

KSA 26.03.23The ammonium sulfate market is projected to grow from USD 5.75 billion in 2025 to USD 6.81 billion by 2030, at a CAGR of 3.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) Volume (Kiloton) |

| Segments | Type, Application, and Region |

| Regions covered | North America, Asia Pacific, Europe, Middle East & Africa, and South America |

Rising environmental regulations, increased focus on efficient nutrient management, and growing industrial demand for sulfur- and nitrogen-based inputs are driving sustained demand for ammonium sulfate across agricultural, chemical, water treatment, and emissions-control applications.

"Solid segment is projected to account for the largest market share during the forecast period."

The solid segment is anticipated to hold the largest share of the ammonium sulfate market during the forecast period. This is primarily due to its ease of handling, storage capabilities, and suitability for bulk delivery systems. Solid ammonium sulfate offers a consistent nutrient content in each bag and can be easily blended with other products, making it the preferred choice for both agricultural and industrial applications. Additionally, its established logistics infrastructure and widespread consumer acceptance worldwide will drive significant and sustained demand growth throughout the forecast period.

"Food & feed additives segment to account for the second-largest market share during the forecast period."

The food & feed additives segment is projected to account for the second-largest market share during the forecast period, driven by its use as a food-grade acidity regulator, dough conditioner, and yeast nutrient. Additionally, ammonium sulfate is used in animal nutrition to increase protein synthesis, feed efficiency, and overall animal performance. The growth of the processed food market, driven by increased livestock production and a constant push for higher quality regulatory compliance, will boost the demand for ammonium sulfate in food and feed additive markets.

"In terms of value, the Asia Pacific is projected to account for the largest market share during the forecast period."

Asia Pacific is projected to account for the largest share in the ammonium sulfate market during the forecast period due to significant demand from farmers, processors of food, and users in a variety of industrial sectors as a result of rapid population growth, increased food intake, and large-scale production of animals for food or feed. Also, there will be significant demand for nitrogen and sulfur from non-agricultural users in the chemical, textile, water treatment, and emission control industries. With its large number of producers and the capability to efficiently source inexpensive materials for production, the Asia Pacific will maintain its dominant status as the largest global market for ammonium sulfate.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Note: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 billion; Tier 2: USD 500 million-1 billion; and Tier 3: <USD 500 million.

Companies Covered: BASF (Germany), Evonik Industries AG (Germany), LANXESS (Germany), AdvanSix (US), Sumitomo Chemical Co., Ltd. (Japan), OCI Global (Netherlands), Domo Chemicals (Belgium), Nutrien Ltd. (Canada), China Petrochemical Development Corporation (China), and Martin Midstream Partners (US), among others, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the ammonium sulfate market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the ammonium sulfate market based on type (solid, liquid), application (fertilizers, pharmaceuticals, food & feed additives, water treatment, textile dyeing, other applications), and region (Asia Pacific, North America, Europe, South America, Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the ammonium sulfate market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, products offered, and key strategies, including partnerships, collaborations, product launches, expansions, and acquisitions, associated with the ammonium sulfate market. This report covers a competitive analysis of upcoming startups in the ammonium sulfate market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall ammonium sulfate market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (structural shift toward sulfur-containing nitrogen fertilizers under nutrient imbalance correction programs, sustained demand from caprolactam and nylon-6 value chains, expanding use in industrial water treatment and wastewater management), restraints (quality variability across production routes, competition from blended and customized multi-nutrient fertilizers), opportunities (development of region-specific nitrogen-sulfur ratios through granulation and compaction, supplying pharmaceutical- and biotech-grade ammonium sulfate for protein purification), and challenges (fragmented regulatory treatment across fertilizers, chemicals, and environmental frameworks, volatile price formation driven by upstream raw material and industrial linkage).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the ammonium sulfate market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the ammonium sulfate market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the ammonium sulfate market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as BASF (Germany), Evonik Industries AG (Germany), LANXESS (Germany), AdvanSix (US), Sumitomo Chemical Co., Ltd. (Japan), OCI Global (Netherlands), Domo Chemicals (Belgium), Nutrien Ltd. (Canada), China Petrochemical Development Corporation (China), and Martin Midstream Partners (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF STRATEGIC CHANGES IN MARKET

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AMMONIUM SULFATE MARKET

- 3.2 AMMONIUM SULFATE MARKET, BY TYPE AND REGION

- 3.3 AMMONIUM SULFATE MARKET, BY APPLICATION

- 3.4 AMMONIUM SULFATE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Structural shift toward sulfur-containing nitrogen fertilizers under nutrient imbalance correction programs

- 4.2.1.2 Sustained demand from caprolactam and nylon-6 value chains

- 4.2.1.3 Expanding use in industrial water treatment and wastewater management

- 4.2.1.4 Functional role in food processing, fermentation, and industrial biotechnology

- 4.2.2 RESTRAINTS

- 4.2.2.1 Quality variability across production routes

- 4.2.2.2 Competition from blended and customized multi-nutrient fertilizers

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development of region-specific nitrogen-sulfur ratios through granulation and compaction

- 4.2.3.2 Supplying pharmaceutical- and biotech-grade ammonium sulfate for protein purification

- 4.2.3.3 As functional additive in flame-retardant and fire-resistant materials

- 4.2.4 CHALLENGES

- 4.2.4.1 Fragmented regulatory treatment across fertilizer, chemical, and environmental frameworks

- 4.2.4.2 Volatile price formation driven by upstream raw material and industrial linkage

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 COST-EFFICIENT PRODUCTION OF HIGH-PURITY AMMONIUM SULFATE WITHOUT DEPENDENCE ON BY-PRODUCT SUPPLY CHAINS

- 4.3.2 ENHANCED NUTRIENT EFFICIENCY AMMONIUM SULFATE FOR HIGH-INTENSITY AND PRECISION AGRICULTURE SYSTEMS

- 4.3.3 APPLICATION-SPECIFIC AMMONIUM SULFATE GRADES FOR SENSITIVE INDUSTRIAL AND PHARMACEUTICAL USES REQUIRING STRINGENT IMPURITY CONTROL

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: STRATEGIC INITIATIVES IN AMMONIUM SULFATE MARKET

- 4.5.1.1 BASF

- 4.5.1.2 Nutrien Ltd.

- 4.5.2 TIER 2 PLAYERS: KEY STRATEGIC MOVES AND INNOVATIONS

- 4.5.2.1 LANXESS AG

- 4.5.2.2 Yara International ASA

- 4.5.3 TIER 3 PLAYERS: EMERGING STRATEGIES AND REGIONAL POSITIONING

- 4.5.3.1 UBE Industries & Regional Producers

- 4.5.3.2 Localized Asian and Emerging Producers (e.g., Sinopec, KuibyshevAzot, Jilin Chemical)

- 4.5.1 TIER 1 PLAYERS: STRATEGIC INITIATIVES IN AMMONIUM SULFATE MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES' ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 NATURAL GAS & ENERGY PRICE DYNAMICS

- 5.2.3 GLOBAL FERTILIZER PRICE STABILIZATION

- 5.2.4 ACCELERATED PUBLIC INVESTMENT IN WATER & WASTEWATER INFRASTRUCTURE

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA RELATED TO HS CODE 310221, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.6.2 EXPORT DATA RELATED TO HS CODE 310221, BY COUNTRY, 2020-2024 (USD THOUSAND)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 MAXIMIZING SOYBEAN YIELD WITH ADVANSIX SULF-N FIELD TRIALS

- 5.10.2 IMPROVING CROP OUTPUT AND STEEL QUALITY USING STEEL GRADE AMMONIUM SULFATE

- 5.10.3 RECOVERING AMMONIUM SULFATE FROM PAPER MILL EFFLUENT WITH CONDORCHEM TECHNOLOGY

- 5.11 IMPACT OF 2025 US TARIFF ON AMMONIUM SULFATE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 KEY IMPACT ON VARIOUS REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 END-USE INDUSTRY IMPACT

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 NEUTRALIZATION REACTOR TECHNOLOGY (NH3 + H2SO4)

- 6.1.2 BY-PRODUCT RECOVERY & CONVERSION (CAPROLACTAM STREAM PROCESSING)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 FLUIDIZED BED & GRANULATION SYSTEMS

- 6.2.2 CENTRIFUGATION & DRYING EQUIPMENT

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 AMMONIA RECOVERY & NUTRIENT RECYCLING TECHNOLOGIES

- 6.3.2 WASTE VALORIZATION & INDUSTRIAL FEEDSTOCK CONVERSION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | PROCESS OPTIMIZATION & PERFORMANCE STABILIZATION PHASE

- 6.4.2 MID-TERM (2027-2030) | PROCESS INTEGRATION & RESOURCE EFFICIENCY PHASE

- 6.4.3 LONG-TERM (2030-2035+): SUSTAINABLE AND HIGH-EFFICIENCY PRODUCTION PHASE

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 APPROACH

- 6.5.3 TOP APPLICANTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 SELF-DEGRADING AGRICULTURAL MULCH FILMS

- 6.6.2 WATER TREATMENT AND ALGAE CONTROL AGENTS

- 6.6.3 SELF-HEALING CONCRETE SYSTEMS

- 6.7 IMPACT OF AI/GEN AI ON AAMONIUM SULFATE MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN AMMONIUM SULFATE

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN AMMONIUM SULFATE MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN AMMONIUM SULFATE MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF AMMONIUM SULFATE

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF AMMONIUM SULFATE

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS APPLICATIONS

- 8.5 MARKET PROFITIBILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES BY APPLICATION

9 AMMONIUM SULFATE MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 SOLID

- 9.2.1 SOLID AMMONIUM SULFATE DELIVERS PREDICTABLE PERFORMANCE, LOGISTICAL EFFICIENCY, AND LONG-TERM INDUSTRIAL RELIABILITY

- 9.3 LIQUID

- 9.3.1 LIQUID AMMONIUM SULFATE ENABLES PRECISE REAL-TIME CONTROL WITHIN CONTINUOUS INDUSTRIAL PROCESSING SYSTEMS

10 AMMONIUM SULFATE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 FERTILIZERS

- 10.2.1 AMMONIUM SULFATE SUPPORTS BALANCED FERTILIZATION STRATEGIES AMID RISING GLOBAL FERTILIZER DEMAND AND PRICE PRESSURE

- 10.3 PHARMACEUTICALS

- 10.3.1 AMMONIUM SULFATE ENSURES CONTROLLED PROTEIN PURIFICATION AND PROCESS INTEGRITY IN PHARMACEUTICAL MANUFACTURING

- 10.4 FOOD & FEED ADDITIVES

- 10.4.1 AMMONIUM SULFATE ENSURES SAFE NUTRITIONAL ENHANCEMENT AND PROCESS STABILITY IN FOOD AND FEED PRODUCTION

- 10.5 WATER TREATMENT

- 10.5.1 AMMONIUM SULFATE IMPROVES WATER TREATMENT EFFICIENCY AMID RISING GLOBAL DEMAND AND INADEQUATE WASTEWATER MANAGEMENT

- 10.6 TEXTILE DYEING

- 10.6.1 AMMONIUM SULFATE OPTIMIZES DYE FIXATION AND UNIFORMITY IN COTTON AND CELLULOSIC TEXTILE PROCESSES

- 10.7 OTHER APPLICATIONS

11 AMMONIUM SULFATE MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Expanding agricultural, industrial, and infrastructure activities reinforcing demand

- 11.2.2 CANADA

- 11.2.2.1 Agricultural intensification and expanding industrial driving demand

- 11.2.3 MEXICO

- 11.2.3.1 Domestic fertilizer expansion and diversified industrial growth to drive consumption

- 11.2.1 US

- 11.3 ASIA PACIFIC

- 11.3.1 CHINA

- 11.3.1.1 Export-oriented manufacturing growth and infrastructure upgrades to accelerate demand

- 11.3.2 INDIA

- 11.3.2.1 Integrated agricultural, industrial, and environmental expansion accelerating consumption

- 11.3.3 JAPAN

- 11.3.3.1 Industrial and agricultural modernization continues to structurally reinforce demand

- 11.3.4 VIETNAM

- 11.3.4.1 Expanding agri exports, industrial processing, and infrastructure upgrades driving demand

- 11.3.5 INDONESIA

- 11.3.5.1 Subsidized agricultural products, industrial scale-up, and infrastructure to accelerate demand

- 11.3.6 REST OF ASIA PACIFIC

- 11.3.1 CHINA

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Integrated agri-industrial and environmental systems driving demand

- 11.4.2 FRANCE

- 11.4.2.1 Integrated agricultural, industrial, and environmental systems sustaining demand growth

- 11.4.3 ITALY

- 11.4.3.1 Diversified agri-industrial and process sectors to lift demand

- 11.4.4 UK

- 11.4.4.1 Integrated nutrient management and industrial expansion reinforcing demand

- 11.4.5 NETHERLANDS

- 11.4.5.1 Integrated agricultural, industrial, and environmental systems driving demand

- 11.4.6 RUSSIA

- 11.4.6.1 Structural industrial expansion and environmental modernization to increase demand

- 11.4.7 UKRAINE

- 11.4.7.1 Rising fertilizer demand driven by agriculture and industrial growth

- 11.4.8 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Import dependence and expanding agribusiness ecosystems accelerating ammonium sulfate demand

- 11.5.2 ARGENTINA

- 11.5.2.1 Import-led fertilizer growth and expanding industrial demand increasing use of ammonium sulfate

- 11.5.3 REST OF SOUTH AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

- 11.6.1.1 Saudi Arabia

- 11.6.1.1.1 Strategic agricultural growth and population pressures drive ammonium sulfate demand

- 11.6.1.2 UAE

- 11.6.1.2.1 Economic growth and agriculture sectors increasing demand

- 11.6.1.3 Rest of GCC Countries

- 11.6.1.1 Saudi Arabia

- 11.6.2 SOUTH AFRICA

- 11.6.2.1 Rising ammonium sulfate demand driven by agriculture and livestock growth

- 11.6.3 REST OF MIDDLE EAST & AFRICA

- 11.6.1 GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.4.1 MARKET RANKING ANALYSIS

- 12.5 PRODUCT COMPARISON

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.6.5.1 Company footprint

- 12.6.5.2 Region footprint

- 12.6.5.3 Type footprint

- 12.6.5.4 Application footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.7.5.1 Detailed list of key startups/SMEs

- 12.7.5.2 Competitive benchmarking of key startups/SMEs

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.8.1 COMPANY VALUATION

- 12.8.2 FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 BASF SE

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 EVONIK INDUSTRIES AG

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 LANXESS

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.3.2 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 ADVANSIX

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.3.2 Expansions

- 13.1.4.3.3 Other developments

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 SUMITOMO CHEMICAL CO., LTD.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.3.2 Expansions

- 13.1.5.3.3 Other developments

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 OCI

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.6.3.4 Other developments

- 13.1.6.4 MnM view

- 13.1.7 DOMO CHEMICALS

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Expansions

- 13.1.7.4 MnM view

- 13.1.8 NUTRIEN

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Deals

- 13.1.8.3.2 Expansions

- 13.1.8.3.3 Other developments

- 13.1.8.4 MnM view

- 13.1.9 CHINA PETROCHEMICAL DEVELOPMENT CORPORATION (CPDC)

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 MnM view

- 13.1.10 MARTIN MIDSTREAM PARTNERS L.P.

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Deals

- 13.1.10.3.2 Other developments

- 13.1.10.4 MnM view

- 13.1.1 BASF SE

- 13.2 OTHER PLAYERS

- 13.2.1 UBE CORPORATION

- 13.2.2 GUJARAT STATE FERTILIZERS AND CHEMICALS LIMITED

- 13.2.3 JOST CHEMICAL CO.

- 13.2.4 KANTO CHEMICAL CO., INC.

- 13.2.5 KISHIDA CHEMICAL CO., LTD.

- 13.2.6 AMERICAN PLANT FOOD CORPORATION

- 13.2.7 GREENWAY BIOTECH INC.

- 13.2.8 THE DALLAS GROUP OF AMERICA

- 13.2.9 RAVENSDOWN

- 13.2.10 VINIPUL INORGANICS PVT. LTD.

- 13.2.11 YARA INTERNATIONAL ASA

- 13.2.12 GRODNO AZOT

- 13.2.13 SHANDONG HAILI CHEMICAL INDUSTRY CO., LTD.

- 13.2.14 ANQORE

- 13.2.15 SUJATA CHEMICALS

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.1.2 List of secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key primary participants

- 14.1.2.2 Key data from primary sources

- 14.1.2.3 Breakdown of interviews with experts

- 14.1.2.4 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 BOTTOM-UP APPROACH

- 14.2.2 TOP-DOWN APPROACH

- 14.3 BASE NUMBER CALCULATION

- 14.3.1 SUPPLY-SIDE APPROACH

- 14.4 GROWTH FORECAST

- 14.5 DATA TRIANGULATION

- 14.6 RESEARCH ASSUMPTIONS

- 14.7 FACTOR ANALYSIS

- 14.8 RESEARCH LIMITATIONS

- 14.9 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS