|

시장보고서

상품코드

2062281

포타슘 휴메이트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Potassium Humate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

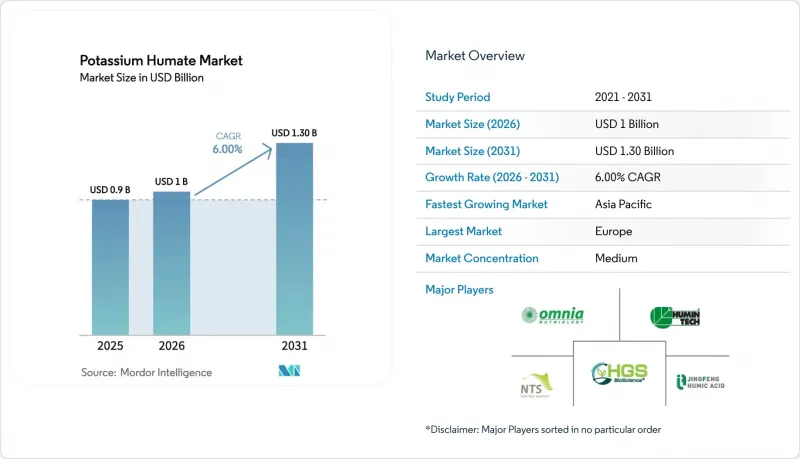

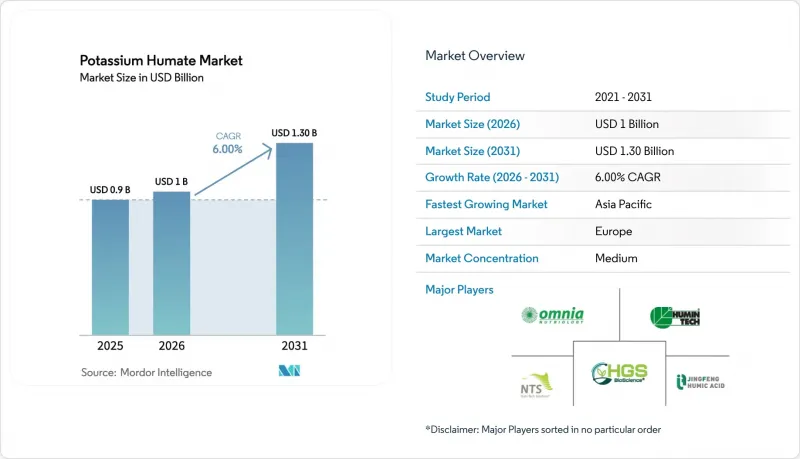

포타슘 휴메이트 시장 규모는 2025년에 9억 달러로 평가되었고 예측 기간(2026-2031년) CAGR 6.0%를 나타내 2026년 10억 달러에서 2031년에는 13억 달러에 이를 것으로 추정되고 있습니다.

본 보고서는 형태별(분말, 과립/플레이크, 액상 농축액), 용도별(밭작물, 원예·과수, 수경재배·온실재배), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 포타슘 휴메이트 시장 동향 및 분석

지속 가능한 농업 자재에 대한 수요 증가

기업의 지속가능성 방침에 따라, 조달 예산이 합성비료에서만 질소 의존도를 낮추는 토양 개량제로 전환되고 있습니다. 유럽의 ‘팜 투 포크(Farm to Fork)’ 전략은 2030년까지 비료 사용량을 20% 감축하는 것을 목표로 하고 있으며, 이 목표 덕분에 생산자들은 부식산 칼륨이 함유된 제품으로 눈을 돌리고 있습니다. 이 제품은 수확량을 저하시키지 않으면서 영양분 이용 효율을 높여줍니다. 포타슘 휴메이트은 토양 유기물을 증강하고 미생물의 활동을 촉진함으로써 탄소 고정을 돕고, 기업의 스코프 3 배출량 감축 목표와 부합합니다. 주요 농업 관련 기업과 식품 기업들은 재생형 농업 자재의 도입을 확대하고 있으며, 이에 따라 지속가능한 조달 이니셔티브에서 후민산계 제품의 매력이 높아지고 있습니다.

전 세계 유기농업 면적의 확대

FiBL의 통계에 따르면, 2023년 인증 유기농 경지 면적은 9,890만 헥타르에 달하고, 전년 대비 2.6% 증가했습니다. 면적 면에서는 유럽이 1위를 차지하고 있지만, 아시아·태평양 지역이 생산자 수 증가율에서 가장 높은 수치를 기록하고 있으며, 이는 인도, 중국, 인도네시아의 소규모 농가들이 유기농으로 전환하고 있는 추세를 반영한 것입니다. 스페인에서만 299만 헥타르가 유기농 기준에 따라 관리되고 있지만, 후민산의 채택률은 광활한 곡물 농지보다 집약적인 채소 재배 시스템에서 여전히 더 높은 임베디드니다. 포타슘 휴메이트은 천연 레오나르다이트에서 채굴되며, 최소한의 가공만 거쳤기 때문에 전 세계 유기질 자재 목록의 요건을 충족합니다. 주요 경쟁 상대는 농장 내 퇴비이지만, 원료가 풍부하고 인건비가 저렴하다는 장점이 있는 반면, 청결한 점적 관개 시스템이나 신속한 영양분 방출이 필수적인 상황에서는 후민산이 우위를 점하고 있습니다.

미생물성 바이오자극제와의 경쟁

미생물성 바이오 자극제는 농가에 토양의 비옥도, 영양분 흡수, 식물 생장을 개선하는 대안 솔루션을 제공함으로써 포타슘 휴메이트 시장에 미치는 영향력을 확대되고 있습니다. 이러한 제품들은 종종 친환경적이거나 바이오 유래라는 특징을 내세워 판매되고 있습니다. 이러한 추세는 대체 압력을 초래하여 포타슘 휴메이트 수요를 감소시킬 가능성이 있는 한편, 생산자들에게는 가격 측면의 문제도 야기하고 있습니다. 일부 미생물 혼합제는 후민산계 제품에 비해 더 적은 시비량으로도 높은 수확량을 달성하고 있어, 가격 경쟁을 더욱 치열하게 만들고 있습니다. 미생물 제품에는 보존 기간이 짧거나 pH 변동에 민감하다는 등의 한계가 있으며, 이러한 문제는 화학적으로 안정된 후민산계 제품에서는 찾아볼 수 없는 문제입니다. 이에 대응하기 위해 공급업체는 고객을 유지하기 위해 후민산과 미생물 제품을 배합하고 있습니다. 이 전략은 경쟁 압력을 어느 정도 완화할 수는 있겠지만, 포타슘 휴메이트 시장이 직면한 과제를 완전히 해소하는 것은 아닙니다.

부문별 분석

2025년 기준으로, 분말 유형이 포타슘 휴메이트 시장 점유율의 47%를 차지하며 최대 부문이 되었습니다. 이는 현재 보호재배를 주도하고 있는 자동 시비 시스템과의 호환성을 반영한 것입니다. 이러한 장점은 그 범용성, 장기 보존성 및 운송의 용이성에서 비롯됩니다. 농가에서는 다른 고형 비료와 혼합할 수 있고, 광대한 농지 전체에 고르게 살포할 수 있다는 점 때문에 대규모 포장 살포 시에는 분말 형태의 부식산 칼륨을 선호하는 경향이 있습니다. 또한, 분말 형태의 제품은 일반적으로 톤당 비용 효율이 높기 때문에 주요 농업 지역에서 이루어지는 기존의 토양 개량 작업에 있어 실용적인 대안이 되고 있습니다.

액상 농축액 시장은 가장 빠르게 성장하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.4%로 확대될 것으로 전망됩니다. 이러한 성장은 비료 시비, 관개, 엽면 시비 등 정밀 농업 기술의 도입 확대에 힘입은 것으로, 이러한 기술들은 보다 목표가 명확하고 효율적인 영양분 공급을 가능하게 합니다. 액체 농축액은 자동 관개 시스템과의 호환성과 영양분 흡수를 촉진하는 능력 덕분에 고부가가치 작물, 온실 재배 시스템, 수경 재배 설비에서 특히 선호되고 있습니다.

지역별 분석

2025년 기준으로, 칼륨 후식산 시장 규모의 34%를 차지하며 유럽이 1위를 차지했습니다. 이러한 지역적 경쟁력은 확립된 농업 인프라, 지속 가능한 토양 관리 기법에 대한 높은 인식, 그리고 토양 개량제 및 특수 비료 사용을 장려하는 규제 체계에 의해 뒷받침되고 있습니다. 유럽의 농가들은 토양 비옥도 향상, 작물 생산성 증대, 토양 건강 기준 준수를 목적으로 부식산 칼륨의 사용을 확대하고 있으며, 이로 인해 해당 지역에서 안정적인 수요가 확보되고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 11.9%를 나타낼 것으로 전망됩니다. 이러한 성장은 농업의 급속한 현대화, 고효율 비료 사용 확대, 그리고 증가하는 인구 수요를 충족시키기 위한 작물 수확량 증대의 필요성에 의해 주도되고 있습니다. 해당 지역 전체에서 정밀 농업, 온실 재배 및 영양 관리 기법의 개선에 대한 투자가 분말 및 액상 형태의 포타슘 휴메이트 제품에 대한 수요 증가를 이끌고 있습니다.

북미에서는 탄소 크레딧 지급, 온실 재배 면적 확대, 그리고 HumiK ONE과 같은 특허 보호 제품의 인기에 힘입어 견고한 수요 기반이 형성되어, 이 지역에서 상당한 성장이 예상됩니다. 남미에서는 브라질의 수입 비료에 대한 의존도와 아르헨티나의 바이오 투입재 생산 현지화 노력에 힘입어 시장이 확대되고 있습니다. 채굴부터 배합까지를 통합하는 국내 부식산염 공급업체는 완비료에 대한 수입 관세 인상을 기회로 삼을 수 있습니다. 아프리카는 남아프리카공화국, 케냐, 이집트에서 새롭게 부상하고 있는 온실 클러스터와 정부의 점적 관개 인프라 지원에 힘입어 낮은 수준에서 성장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the potassium humate market size was valued at USD 0.9 billion in 2025 and is estimated to grow from USD 1.0 billion in 2026 to USD 1.3 billion by 2031, at a CAGR of 6.0% during the forecast period (2026-2031).

This report is Segmented by Form (Powder, Granules/Flakes, Liquid Concentrate), by Application (Field Crops, Horticulture and Fruits, and Hydroponics and Greenhouse), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Potassium Humate Market Trends and Insights

Rising Demand for Sustainable Agricultural Inputs

Corporate sustainability mandates are shifting procurement budgets away from synthetic-only fertilizers toward soil conditioners that reduce nitrogen dependence. The European Farm to Fork strategy aims for a 20% reduction in fertilizer use by 2030, a target that is pushing growers toward humate blends, which improve nutrient-use efficiency without harming yields. Potassium humate aids carbon sequestration by enhancing soil organic matter and promoting microbial activity, aligning with corporate Scope 3 emission-reduction goals. Major agribusinesses and food companies are increasingly adopting regenerative agriculture inputs, thereby increasing the appeal of humate-based products in sustainable sourcing initiatives.

Increasing Global Organic-Farming Acreage

According to FiBL statistics, certified organic cropland reached 98.9 million hectares in 2023, adding 2.6% year on year. Europe leads by land area, but Asia-Pacific adds producers the fastest, reflecting smallholder conversions in India, China, and Indonesia. Spain alone manages 2.99 million hectares under organic rules, although humate uptake is still higher in intensive vegetable systems than in broad-acre cereals. Because potassium humate is mined from naturally occurring leonardite and undergoes minimal processing, it qualifies for organic input lists worldwide. Its main competition is on-farm compost, where feedstocks are abundant, and labor is cheap, yet humate wins where clean drip systems and fast nutrient release are critical.

Competition from Microbial Biostimulants

Microbial biostimulants are increasingly influencing the potassium humate market by providing farmers with alternative solutions that improve soil fertility, nutrient uptake, and plant growth, often marketed with eco-friendly or bio-based attributes. This trend introduces substitution pressure, potentially decreasing the demand for potassium humate while also creating pricing challenges for producers. Some microbial blends achieve higher yields at lower application rates compared to humates, further intensifying price competition. Microbial products face limitations such as shorter shelf life and sensitivity to pH variations, issues that chemically stable humates do not encounter. To address this, suppliers are co-formulating humic acids with microbial products to retain customers. While this strategy may mitigate some of the competitive pressures, it does not fully eliminate the challenges faced by the potassium humate market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push to Reduce Chemical-Fertilizer Use

- Growing Use of Water-Soluble Fertilizers in Drip Irrigation

- Environmental, Social, and Governance (ESG) Scrutiny of Leonardite Strip-Mining in Sensitive Peatlands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder held the largest segment, 47% of the potassium humate market share in 2025, reflecting its fit with automated fertigation that now commands protected-crop production. This dominance is attributed to its versatility, extended shelf life, and ease of transportation. Farmers often prefer powdered potassium humate for large-scale field applications due to its ability to blend with other solid fertilizers and ensure uniform distribution across extensive farmland. Additionally, powdered forms are generally more cost-effective per metric ton, making them a practical choice for traditional soil amendment practices in key agricultural regions.

Liquid concentrate is the fastest-growing, forecast to expand at a 12.4% CAGR through 2026-2031. This growth is driven by the increasing adoption of precision agriculture techniques, such as fertigation and foliar spraying, which enable more targeted and efficient nutrient delivery. Liquid concentrates are particularly favored for high-value crops, greenhouse systems, and hydroponic setups due to their compatibility with automated irrigation systems and their ability to facilitate faster nutrient uptake.

Geography Analysis

Europe led the potassium humate market size with 34% in 2025, this regional leadership is supported by a well-established agricultural infrastructure, high awareness of sustainable soil management practices, and regulatory frameworks that encourage the use of soil conditioners and specialty fertilizers. European farmers increasingly utilize potassium humate to improve soil fertility, boost crop productivity, and comply with soil health standards, ensuring steady demand in the region.

Asia-Pacific is the fastest-growing, projected to grow at a 11.9% CAGR through 2026-2031, this growth is driven by the rapid modernization of agriculture, increased adoption of high-efficiency fertilizers, and the need to enhance crop yields to meet the demands of growing populations. Investments in precision agriculture, greenhouse farming, and improved nutrient management practices across the region are driving rising demand for both powdered and liquid potassium humate products.

North America delivers the significant regional growth driven by carbon-credit payments, expanding greenhouse acreage, and patent-protected products such as HumiK ONE, creating a robust demand stack. South America expands, driven by Brazil's dependency on imported nutrients and Argentina's efforts to localize bioinput production. Domestic humate suppliers that integrate mining into blending can tap into rising import duties on finished fertilizers. Africa grows from a low base, powered by nascent greenhouse clusters in South Africa, Kenya and Egypt along with drip infrastructure subsidized by governments.

- HGS BioScience (Paine Schwartz Partners, LLC)

- Humintech GmbH

- Nutri-Tech Solutions Pty Ltd

- Omnia Specialities

- Jing Feng Humic Acid

- FMC Corporation

- Criyagen

- Zhengzhou Shengda Khumic Biotechnology Co

- Humico Minerals

- Hebei Shuanglian Biotechnology Co.Ltd.

- Huma, Inc.

- Black Earth Humic LP

- The Andersons Plant Nutrient

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for sustainable agricultural inputs

- 4.2.2 Increasing global organic-farming acreage

- 4.2.3 Regulatory push to reduce chemical-fertilizer use

- 4.2.4 Growing use of water-soluble fertilizers in drip irrigation

- 4.2.5 Carbon-credit monetization for humate-amended soils

- 4.2.6 Patent cliff for polymer-coated urea enabling humate integration

- 4.3 Market Restraints

- 4.3.1 Price volatility of high-grade humic substances

- 4.3.2 Competition from microbial biostimulants

- 4.3.3 Stringent heavy-metal limits on leonardite-derived inputs

- 4.3.4 Environmental, Social, and Governance (ESG) scrutiny of leonardite strip-mining in sensitive peatlands

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Form

- 5.1.1 Powder

- 5.1.2 Granules/Flakes

- 5.1.3 Liquid Concentrate

- 5.2 By Application

- 5.2.1 Field Crops

- 5.2.2 Horticulture and Fruits

- 5.2.3 Hydroponics and Greenhouse

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Russia

- 5.3.3.4 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products And Services, And Recent Developments)

- 6.4.1 HGS BioScience (Paine Schwartz Partners, LLC)

- 6.4.2 Humintech GmbH

- 6.4.3 Nutri-Tech Solutions Pty Ltd

- 6.4.4 Omnia Specialities

- 6.4.5 Jing Feng Humic Acid

- 6.4.6 FMC Corporation

- 6.4.7 Criyagen

- 6.4.8 Zhengzhou Shengda Khumic Biotechnology Co

- 6.4.9 Humico Minerals

- 6.4.10 Hebei Shuanglian Biotechnology Co.Ltd.

- 6.4.11 Huma, Inc.

- 6.4.12 Black Earth Humic LP

- 6.4.13 The Andersons Plant Nutrient