|

시장보고서

상품코드

1963145

의약품 제조 장비 시장 : 장비 유형별, 최종 제품별, 기술별 - 세계 예측(-2032년)Pharmaceutical Manufacturing Equipment Market by Equipment Type (Packaging, Filling, Spray Drying, Mixing & Blending, Milling, Tablet Compression, Inspection, Granulation, Sterilization), End Product (Solid, Liquid), Technology - Global Forecast to 2032 |

||||||

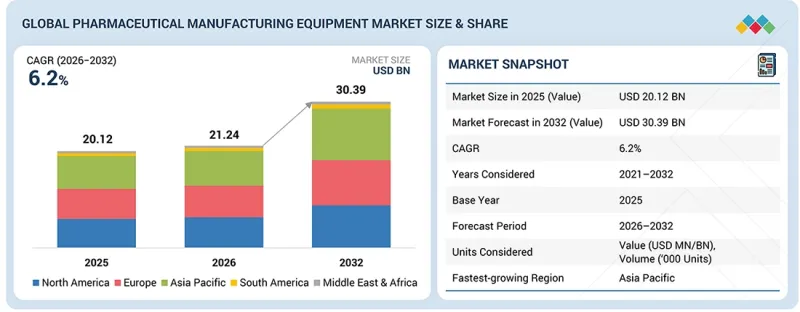

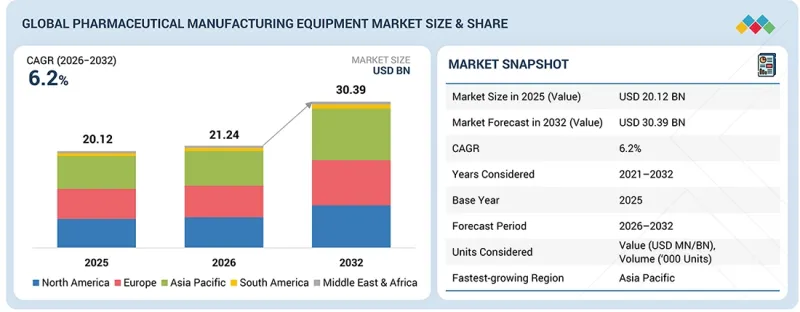

세계의 의약품 제조 장비 시장 규모는 2026년에 212억 4,000만 달러, 2032년까지 303억 9,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 6.2%의 성장이 전망됩니다.

효율적이고 규정을 준수하는 의약품 생산 시스템에 대한 수요가 증가함에 따라 시장은 꾸준히 발전하고 있습니다. 제약사들은 늘어나는 의약품 수요에 대응하기 위해 생산능력 확충을 추진하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2026-2032년 |

| 단위 | 10억 달러 |

| 부문 | 장비 유형, 기술, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

가공 정밀도와 제품 품질은 여전히 중요한 우선순위입니다. 규제 준수 요구 사항은 생산 라인의 현대화를 촉진하고 있습니다. 제네릭 의약품과 바이오의약품에 대한 수요 증가는 확장 가능한 제조 솔루션을 뒷받침하고 있습니다. 엄격한 품질 기준은 검증되고 신뢰할 수 있는 장비를 요구합니다. 제약 인프라에 대한 투자는 계속 증가하고 있습니다. 이러한 요인들은 전 세계 제약 시설에서 첨단 제조 장비의 채택을 촉진하고 있습니다.

"포장기계 부문은 2026-2032년 가장 높은 CAGR로 성장할 것으로 예상됩니다."

안전하고 규정을 준수하는 의약품 포장에 대한 관심이 높아짐에 따라 포장기계는 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다. 제약회사는 제품 보호와 유통기한 연장을 우선순위로 삼고 있습니다. 엄격한 규제 요건으로 인해 첨단 포장 시스템에 대한 투자가 증가하고 있습니다. 정제 및 캡슐 생산이 증가함에 따라 포장 수 또한 증가하고 있습니다. 주사제 역시 안전한 취급이 필요합니다. 변조 방지 포장에 대한 수요가 증가하고 있습니다. 또한, 추적성 확보와 위조 위험 감소를 위한 자동화 및 직렬화 기술의 채택이 확대되면서 의약품 제조 시설 전반에 걸쳐 첨단 포장기계에 대한 수요가 더욱 가속화되고 있습니다.

"액체 부문은 예측 기간 동안 제약 제조 장비 시장에서 우위를 점할 것으로 예상됩니다."

주사제 및 생물학적 제제에 대한 수요 증가로 인해 액체 부문은 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 백신과 경구용 액체도 생산량 증가를 촉진하고 있습니다. 만성질환의 유병률 증가는 무균 제제의 생산 증가를 뒷받침하고 있습니다. 예방접종 프로그램의 확대는 지역을 불문하고 수요를 강화하고 있습니다. 제약회사들은 첨단 충진 및 밀봉 시스템에 대한 투자를 진행하고 있습니다. 수탁 제조의 성장은 생산능력의 확장을 촉진하고 있습니다. 투약 편의성에 대한 환자들의 선호도가 높아지면서 액상 제제의 채택이 증가하고 있습니다. 이러한 변화는 전 세계적으로 액제 제조 인프라에 대한 자본 투자 확대를 뒷받침하고 있습니다.

"중국은 2025년 아시아태평양 의약품 제조 장비 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다."

중국은 대규모 생산능력으로 인해 예측 기간 동안 의약품 제조 장비 시장에서 가장 큰 점유율을 차지할 것입니다. 중국은 원료의약품(API) 및 제네릭 의약품 제조 분야에서 탄탄한 입지를 유지하고 있습니다. 소규모 국내 제조업체부터 수출 지향적 기업까지 다양한 시설기반을 보유하고 있습니다. 많은 공장에서 첨단 자동화 생산 라인을 가동하고 있습니다. 바이오의약품과 백신에 대한 투자가 장비 수요를 증가시키고 있습니다. 무균 제조의 확대가 국내 공정 시스템 업데이트를 뒷받침하고 있습니다. 위탁생산의 성장이 추가적인 생산능력 증설을 촉진하는 한편, 국제 규제 기준을 충족하기 위한 시설 현대화가 수요를 강화시키고 있습니다. 이러한 컴플라이언스 요구사항은 검증된 시스템의 채택을 촉진하고 있습니다. 이러한 요인들로 인해 중국은 의약품 제조 장비의 주요 시장으로 부상하고 있습니다.

세계의 의약품 제조 장비 시장에 대해 조사 분석했으며, 주요 촉진요인 및 억제요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 의약품 제조 장비 최종사용자

제10장 의약품 장비 제조 공정

제11장 의약품 제조 장비 시장 : 장비 유형별

제12장 의약품 제조 장비 시장 : 최종 제품 유형별

제13장 의약품 제조 장비 시장 : 기술별

제14장 의약품 제조 장비 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.03.20The global pharmaceutical manufacturing equipment market size is projected to be USD 21.24 billion in 2026 and USD 30.39 billion by 2032, registering a CAGR of 6.2% during the forecast period. The market is progressing steadily due to the rising demand for efficient and compliant drug production systems. Pharmaceutical companies are expanding production capacity to meet growing medicine demand.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Equipment Type, Technology and Region |

| Regions covered | North America, Europe, APAC, RoW |

Process accuracy and product quality remain key priorities. Regulatory compliance requirements drive the modernization of production lines. Increasing demand for generic drugs and biologics supports scalable manufacturing solutions. Strict quality standards require validated and reliable equipment. Investment in pharmaceutical infrastructure continues to rise. These factors support the adoption of advanced manufacturing equipment across global pharmaceutical facilities.

"Packaging machines segment is anticipated to grow at the fastest CAGR from 2026 to 2032"

Packing machines are expected to record the highest CAGR during the forecast period due to the growing emphasis on safe and compliant pharmaceutical packaging. Pharmaceutical companies are prioritizing product protection and shelf life extension. Strict regulatory requirements are increasing investment in advanced packaging systems. The growing production of tablets and capsules is raising packaging volumes. Injectable drugs also require secure handling. Demand for tamper-proof packaging is increasing. Additionally, the increasing adoption of automation and serialization technologies to ensure traceability and reduce counterfeiting risks is further accelerating the demand for advanced packaging machines across pharmaceutical manufacturing facilities.

"Liquid segment is expected to dominate the pharmaceutical manufacturing equipment market during the forecast period"

The liquid segment is expected to account for the largest market share during the forecast period due to the mounting demand for injectables and biologics. Vaccines and oral liquid medicines are also driving production growth. The increasing prevalence of chronic diseases supports the higher output of sterile formulations. Expansion of immunization programs strengthens demand across regions. Pharmaceutical companies are investing in advanced filling and sealing systems. Growth in contract manufacturing supports capacity expansion. Patient preference for easy administration is increasing the adoption of liquid forms. This shift supports higher capital investment in liquid manufacturing infrastructure globally.

"China held the largest share of the Asia Pacific pharmaceutical manufacturing equipment market in 2025"

China accounted for the largest share of the pharmaceutical manufacturing equipment market during the forecast period due to its large-scale production capacity. The country maintains a strong position in active pharmaceutical ingredient (API) and generic drug manufacturing. A wide base of facilities ranges from small domestic producers to export-focused companies. Many plants operate advanced automated production lines. Investment in biologics and vaccines is increasing equipment demand. Sterile manufacturing expansion supports process system upgrades in the country. Contract manufacturing growth drives additional capacity additions, while facility modernization to meet international regulatory standards strengthens demand. These compliance requirements encourage the adoption of validated systems. These factors position it as the leading market for pharmaceutical manufacturing equipment.

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: Directors - 40%, C-level Executives - 45%, and Others - 15%

- By Region: North America - 26%, Europe - 28%, Asia Pacific - 41%, and RoW - 5%

Prominent players profiled in this report include GEA Group Aktiengesellschaft (Germany), IMA Industria Macchine Automatiche S.p.A (Italy), Syntegon Technology GmbH (Germany), ACG (India), Thermo Fisher Scientific Inc (US), Korber AG (Germany), Coperion GmbH (Germany), Romaco Group (Germany), Marchesini Group S.p.A (Italy), and Bausch+Strobel SE + Co. KG (Germany).

Research Coverage

The report defines, describes, and forecasts the pharmaceutical manufacturing equipment market based on equipment type (packaging machines, filling machines, spray drying equipment, mixing & blending machines, milling equipment, extrusion equipment, tablet compression presses, inspection equipment, granulation equipment, and sterilization equipment), end-product type (solid and liquid), and technology (semi-automatic and automatic). It also analyzes the market across key regions, including North America, Europe, Asia Pacific, and RoW. The report provides detailed insights into the major drivers, restraints, opportunities, and challenges influencing market growth. In addition, it evaluates competitive developments, such as product launches, expansions, partnerships, acquisitions, and strategic initiatives undertaken by leading companies to strengthen their market position.

Reasons to Buy This Report

The report will help market leaders/new entrants with information on the closest approximations of the revenue for the overall pharmaceutical manufacturing equipment market and its subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following points:

- Analysis of Key Drivers (Increasing commercialization of biologics and complex formulations, Growing preference for personalized medicines and targeted therapies, Rapid advances in automation, digital monitoring, and Industry 4.0 technologies, Escalating generic drug production), restraints (High capital expenditure requirements, Issues related to integration with existing systems, Implementation of stringent regulatory compliance standards), opportunities (Expansion of contract development and manufacturing organizations, Mounting demand for sterile and aseptic injectable drugs, Rising integration of advanced inspection and serialization technologies), and challenges (Requirement for frequent technological upgrades, Complex validation and revalidation cycles, Technical and operational challenges related to small-batch production) of the pharmaceutical manufacturing equipment market.

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the pharmaceutical manufacturing equipment market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the pharmaceutical manufacturing equipment market across various regions)

- Market Diversification: Exhaustive information about new product launches, untapped geographies, recent developments, and investments in the pharmaceutical manufacturing equipment market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and offering of leading players, including GEA Group Aktiengesellschaft (Germany), IMA Industria Macchine Automatiche S.p.A (Italy), Syntegon Technology GmbH (Germany), ACG (India), and Thermo Fisher Scientific Inc (US) in the pharmaceutical manufacturing equipment market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET

- 3.2 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 3.3 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY END-PRODUCT TYPE

- 3.4 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY TECHNOLOGY

- 3.5 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET IN NORTH AMERICA, BY EQUIPMENT TYPE AND COUNTRY

- 3.6 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY GEOGRAPHY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing commercialization of biologics and complex formulations

- 4.2.1.2 Growing preference for personalized medicines and targeted therapies

- 4.2.1.3 Rapid advances in automation, digital monitoring, and Industry 4.0 technologies

- 4.2.1.4 Escalating generic drug production

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital expenditure requirements

- 4.2.2.2 Issues related to integration with existing systems

- 4.2.2.3 Implementation of stringent regulatory compliance standards

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of contract development and manufacturing organizations

- 4.2.3.2 Mounting demand for sterile and aseptic injectable drugs

- 4.2.3.3 Rising deployment of advanced inspection and serialization technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Requirement for frequent technological upgrades

- 4.2.4.2 Complex validation and revalidation cycles

- 4.2.4.3 Technical and operational challenges related to small-batch production

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL BIOPHARMACEUTICAL & VACCINE MANUFACTURING INDUSTRY

- 5.2.4 TRENDS IN GLOBAL GENERIC DRUG & ORAL SOLID DOSAGE MANUFACTURING INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF PHARMACEUTICAL MANUFACTURING EQUIPMENT OFFERED BY KEY PLAYERS, BY EQUIPMENT TYPE, 2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF PACKAGING MACHINES, 2022-2025

- 5.5.3 AVERAGE SELLING PRICE TREND OF PACKAGING MACHINES, BY REGION, 2022-2025

- 5.6 INVESTMENT AND FUNDING SCENARIO

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 8479)

- 5.7.2 EXPORT SCENARIO (HS CODE 8479)

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 KEY CONFERENCES AND EVENTS, 2026

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 INOXPA STRENGTHENS AVVA PHARMACEUTICALS' MANUFACTURING CAPABILITIES THROUGH MODULAR PHARMACEUTICAL PROCESSING SYSTEM

- 5.10.2 GEA GROUP INSTALLS PSD-3 PHARMACEUTICAL SPRAY DRYER AT CHUGAI PHARMACEUTICAL'S FJ3 FACILITY TO PROCESS PHARMACEUTICAL COMPOUNDS

- 5.10.3 ZAMBON COMPANY AND IMA ACTIVE COLLABORATE ON PROCESS OPTIMIZATION PROJECT TO ENHANCE BATCH CONSISTENCY AND QUALITY

- 5.10.4 ACG HELPS INDIAN PHARMACEUTICAL COMPANY RETROFIT B MAX MACHINE WITH NITROGEN-ENHANCED PURGING SYSTEM TO IMPROVE STABILITY AND SHELF LIFE

- 5.10.5 SYNTEGON PROVIDES AIM 5022S PLATFORM TO JIANGSU JINDIKE PHARMACEUTICAL TO ENHANCE INSPECTION EFFICIENCY AND ACCURACY

- 5.11 IMPACT OF 2025 US TARIFF - PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON EQUIPMENT TYPES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACTS, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 CONTINUOUS MANUFACTURING

- 6.1.2 DIGITAL TWIN

- 6.1.3 STERILE AND ASEPTIC PROCESSING

- 6.1.4 SOLID DOSAGE MANUFACTURING

- 6.1.5 AUTOMATION AND ROBOTICS

- 6.1.6 INTERNET OF THINGS (IOT) AND SMART SENSORS

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 COMPUTER-AIDED DESIGN (CAD) AND COMPUTER-AIDED MANUFACTURING (CAM)

- 6.2.2 ADVANCED CNC MACHINING AND PRECISION MANUFACTURING

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 3D PRINTING

- 6.3.2 INDUSTRIAL AUTOMATION SYSTEMS

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED PHARMACEUTICAL MANUFACTURING EQUIPMENT

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 REGULATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF EQUIPMENT TYPES

9 END USERS OF PHARMACEUTICAL MANUFACTURING EQUIPMENT

- 9.1 INTRODUCTION

- 9.2 PHARMACEUTICAL MANUFACTURING COMPANIES

- 9.3 CONTRACT MANUFACTURING ORGANIZATIONS

10 MANUFACTURING PROCESSES OF PHARMACEUTICAL EQUIPMENT

- 10.1 INTRODUCTION

- 10.2 FORMULATION PROCESS

- 10.3 TABLETING & ENCAPSULATION PROCESS

- 10.4 ASEPTIC PROCESS

- 10.5 PACKAGING PROCESS

- 10.6 QUALITY CONTROL PROCESS

11 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 11.1 INTRODUCTION

- 11.2 PACKAGING MACHINES

- 11.2.1 INCREASING PRODUCT AND STOCK KEEPING UNIT PROLIFERATION TO BOOST SEGMENTAL GROWTH

- 11.3 FILLING MACHINES

- 11.3.1 RISING STERILE AND ASEPTIC MANUFACTURING TO CONTRIBUTE TO SEGMENTAL GROWTH

- 11.4 SPRAY DRYING EQUIPMENT

- 11.4.1 ESCALATING NUMBER OF POORLY SOLUBLE DRUG MOLECULES TO FOSTER SEGMENTAL GROWTH

- 11.5 MIXING & BLENDING MACHINES

- 11.5.1 MOUNTING CONSUMPTION OF SOLID ORAL DOSAGE FORMS TO BOLSTER SEGMENTAL GROWTH

- 11.6 MILLING EQUIPMENT

- 11.6.1 RISING NEED FOR TIGHT PARTICLE SIZE CONTROL TO ACCELERATE SEGMENTAL GROWTH

- 11.7 EXTRUSION EQUIPMENT

- 11.7.1 GROWING EMPHASIS ON IMPROVING BIOAVAILABILITY OF POORLY SOLUBLE DRUGS TO SPUR DEMAND

- 11.8 TABLET COMPRESSION PRESSES

- 11.8.1 LARGE-SCALE PRODUCTION OF TABLETS AND HIGH-VOLUME PRODUCTION REQUIREMENTS TO FUEL SEGMENTAL GROWTH

- 11.9 INSPECTION EQUIPMENT

- 11.9.1 HEIGHTENED FOCUS ON QUALITY ASSURANCE AND RISK REDUCTION TO EXPEDITE SEGMENTAL GROWTH

- 11.10 GRANULATION EQUIPMENT

- 11.10.1 REQUIREMENT FOR CONSISTENT AND REPRODUCIBLE MANUFACTURING PROCESSES TO BOOST SEGMENTAL GROWTH

- 11.11 STERILIZATION EQUIPMENT

- 11.11.1 INCREASING PRODUCTION OF STERILE DRUGS AND REGULATORY SCRUTINY TO FOSTER SEGMENTAL GROWTH

12 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY END-PRODUCT TYPE

- 12.1 INTRODUCTION

- 12.2 SOLID

- 12.2.1 STABILITY, EASE OF STORAGE AND TRANSPORT, AND LOW MANUFACTURING COSTS TO AUGMENT SEGMENTAL GROWTH

- 12.3 LIQUID

- 12.3.1 HIGH PREFERENCE FOR BIOLOGICS, VACCINES, AND INJECTABLE THERAPIES TO EXPEDITE SEGMENTAL GROWTH

13 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY TECHNOLOGY

- 13.1 INTRODUCTION

- 13.2 SEMI-AUTOMATIC

- 13.2.1 MOUNTING DEMAND FOR SMALL-SCALE AND FLEXIBLE PHARMACEUTICAL MANUFACTURING TO FUEL SEGMENTAL GROWTH

- 13.3 AUTOMATIC

- 13.3.1 RISING NEED FOR HIGH PRODUCTIVITY AND STRINGENT REGULATORY REQUIREMENTS TO AUGMENT SEGMENTAL GROWTH

14 PHARMACEUTICAL MANUFACTURING EQUIPMENT MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Increasing investment in compliance-ready equipment to strengthen healthcare production capabilities to drive market

- 14.2.2 CANADA

- 14.2.2.1 Mounting adoption of automation and regulatory frameworks to foster market growth

- 14.2.3 MEXICO

- 14.2.3.1 Rising domestic track-and-trace requirements and export compliance to support market growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Government support for life sciences sector and strong regulatory standards to boost market growth

- 14.3.2 GERMANY

- 14.3.2.1 Strong engineering capabilities, advanced automation, and early adoption of digital manufacturing practices to drive market

- 14.3.3 FRANCE

- 14.3.3.1 High investment in validated manufacturing, filling, inspection, and packaging equipment to fuel market growth

- 14.3.4 ITALY

- 14.3.4.1 Growing focus on sterile and high-value manufacturing to contribute to market growth

- 14.3.5 REST OF EUROPE

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Rising emphasis on innovative drug development and automated manufacturing technologies to expedite market growth

- 14.4.2 JAPAN

- 14.4.2.1 Strong focus on manufacturing process control, accuracy, and reliability to accelerate market growth

- 14.4.3 INDIA

- 14.4.3.1 Large-scale generic drug manufacturing base to drive market

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Advanced technological capabilities and strong regulatory framework to foster market growth

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 ROW

- 14.5.1 MIDDLE EAST & AFRICA

- 14.5.1.1 GCC

- 14.5.1.1.1 Rising adoption of healthcare localization and economic diversification strategies to bolster market growth

- 14.5.1.2 South Africa

- 14.5.1.2.1 Increasing vaccine and biologics manufacturing capabilities to augment market growth

- 14.5.1.3 Rest of Middle East & Africa

- 14.5.1.1 GCC

- 14.5.2 SOUTH AMERICA

- 14.5.2.1 Brazil

- 14.5.2.1.1 Strong focus on compliance with track-and-trace regulations to contribute to market growth

- 14.5.2.2 Argentina

- 14.5.2.2.1 Mounting demand for tablet compression, capsule filling, granulation, and coating equipment to support market growth

- 14.5.2.3 Rest of South America

- 14.5.2.1 Brazil

- 14.5.1 MIDDLE EAST & AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2O25

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.6 BRAND COMPARISON

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Equipment type footprint

- 15.7.5.4 End-product type footprint

- 15.7.5.5 Technology footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 GEA GROUP AKTIENGESELLSCHAFT

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses/Competitive threats

- 16.1.2 KORBER AG

- 16.1.2.1 Business overview

- 16.1.2.2 Products/Solutions/Services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.3.2 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses/Competitive threats

- 16.1.3 IMA INDUSTRIA MACCHINE AUTOMATICHE SPA

- 16.1.3.1 Business overview

- 16.1.3.2 Products/Solutions/Services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses/Competitive threats

- 16.1.4 SYNTEGON TECHNOLOGY GMBH

- 16.1.4.1 Business overview

- 16.1.4.2 Products/Solutions/Services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.3.2 Deals

- 16.1.4.3.3 Expansions

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses/Competitive threats

- 16.1.5 ACG

- 16.1.5.1 Business overview

- 16.1.5.2 Products/Solutions/Services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Deals

- 16.1.5.3.2 Expansions

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses/Competitive threats

- 16.1.6 THERMO FISHER SCIENTIFIC INC.

- 16.1.6.1 Business overview

- 16.1.6.2 Products/Solutions/Services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.6.3.2 Expansions

- 16.1.7 ROMACO GROUP

- 16.1.7.1 Business overview

- 16.1.7.2 Products/Solutions/Services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches

- 16.1.7.3.2 Deals

- 16.1.8 MARCHESINI GROUP S.P.A.

- 16.1.8.1 Business overview

- 16.1.8.2 Products/Solutions/Services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.8.3.2 Deals

- 16.1.9 MG2 S.R.L.

- 16.1.9.1 Business overview

- 16.1.9.2 Products/Solutions/Services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.10 GLATT GMBH

- 16.1.10.1 Business overview

- 16.1.10.2 Products/Solutions/Services offered

- 16.1.1 GEA GROUP AKTIENGESELLSCHAFT

- 16.2 OTHER PLAYERS

- 16.2.1 BAUSCH+STROBEL SE + CO. KG

- 16.2.2 COPERION GMBH

- 16.2.3 ELIZABETH COMPANIES

- 16.2.4 FETTE COMPACTING

- 16.2.5 FREUND

- 16.2.6 KORSCH AG

- 16.2.7 L.B. BOHLE MASCHINEN UND VERFAHREN GMBH

- 16.2.8 LFA MACHINES

- 16.2.9 CVC TECHNOLOGIES, INC.

- 16.2.10 OHARA TECHNOLOGIES

- 16.2.11 PRISM PHARMA MACHINERY

- 16.2.12 SAINTYCO

- 16.2.13 SILVERSON

- 16.2.14 YENCHEN MACHINERY CO., LTD.

- 16.2.15 QUALICAPS

- 16.2.16 COESIA S.P.A.

- 16.2.17 UHLMANN

- 16.2.18 AST, LLC

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY AND PRIMARY RESEARCH

- 17.1.2 SECONDARY DATA

- 17.1.2.1 List of key secondary sources

- 17.1.2.2 Key data from secondary sources

- 17.1.3 PRIMARY DATA

- 17.1.3.1 List of primary interview participants

- 17.1.3.2 Key data from primary sources

- 17.1.3.3 Key industry insights

- 17.1.3.4 Breakdown of primaries

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 17.3 MARKET FORECAST APPROACH

- 17.3.1 SUPPLY SIDE

- 17.3.2 DEMAND SIDE

- 17.4 FACTOR ANALYSIS

- 17.5 DATA TRIANGULATION

- 17.6 RESEARCH ASSUMPTIONS

- 17.7 RESEARCH LIMITATIONS

- 17.8 RISK ANALYSIS

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS