|

시장보고서

상품코드

1964921

데이터센터용 냉각액 시장 : 액체 유형별(물 글리콜 혼합액, 합성 탄화수소, 불소계 냉각액), 냉각 방식별(단상 냉각, 2상 냉각), 데이터센터 유형별, 냉각 기술별, 지역별 - 세계 예측 (-2032년)Data Center Liquid Cooling Fluids Market by Fluid Type (Water Glycol Mixtures, Synthetic Hydrocarbons, Fluorocarbon-Based Fluids), Cooling Method (Single Phase, Two Phase), Data Center Type, Cooling Technology, and Region - Global Forecast to 2032 |

||||||

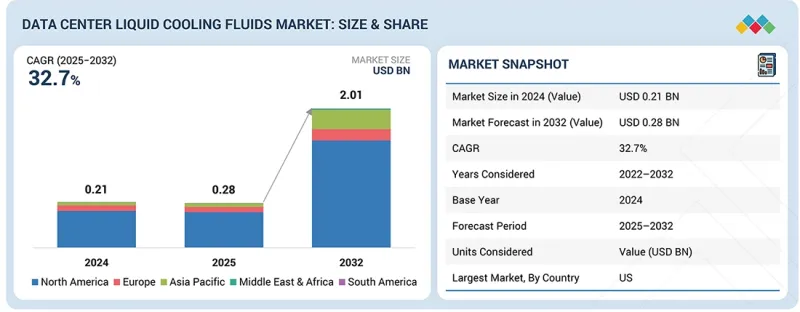

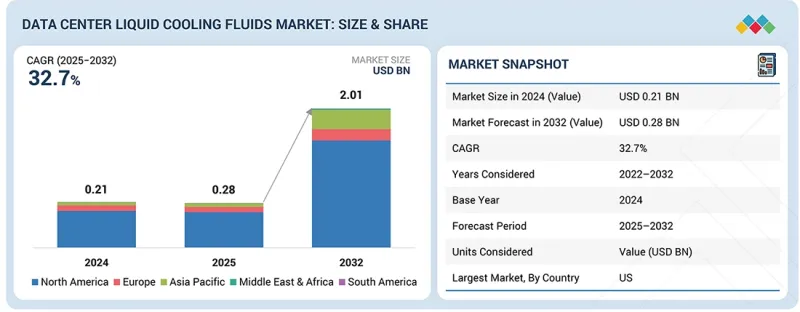

데이터센터용 냉각액 시장 규모는 예측 기간 동안 CAGR 32.7%로 성장하여 2025년 2억 8,000만 달러에서 2032년에는 20억 1,000만 달러에 달할 것으로 전망됩니다.

클라우드 컴퓨팅, AI, 고성능 애플리케이션으로 인한 컴퓨팅 밀도의 현저한 증가는 데이터센터 냉각수 시장을 주도하는 주요 요인입니다. 이러한 증가는 기존의 공랭식 냉각 방식으로는 대응할 수 없는 수준에 이르렀습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2032년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2032년 |

| 단위 | 금액(달러)·양(리터) |

| 부문 | 액체 유형, 데이터센터 유형, 냉각 기술, 냉각 방식, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

현대의 데이터센터에서는 고성능 GPU, 가속기, 프로세서가 사용되고 있으며, 이는 칩 레벨과 랙 레벨에서 집중적인 열을 발생시킵니다. 이로 인해 공기 냉각 시스템으로는 관리할 수 없는 열 문제가 발생합니다. 냉각수는 더 나은 열 전달을 제공하고 중요한 구성요소에서 직접 열을 제거할 수 있습니다. 이를 통해 매우 높은 전력 밀도에서도 안정적인 동작 온도를 유지할 수 있습니다. 공간 활용도 향상, 에너지 소비 감소, 운영 안정성 향상에 대한 요구도 고밀도 컴퓨팅으로의 전환을 촉진하는 요인 중 하나입니다.

"데이터센터 유형별로는 하이퍼스케일 부문이 예측 기간 동안 수량 기준으로 가장 큰 점유율을 차지할 것으로 예상됩니다."

이는 하이퍼스케일 데이터센터가 매우 높은 연산 능력으로 운영되고, 시설 규모가 빠르게 확장되고 있기 때문입니다. 하이퍼스케일 사업자들은 세계 클라우드 및 기술 기업들이 클라우드 서비스를 제공하기 위한 거대한 시설을 구축하고 있으며, AI, 머신러닝, 고성능 컴퓨팅 등 지속적으로 엄청난 열을 발생시키는 워크로드를 지원하고 있습니다. 데이터센터는 많은 서버를 운영하면서 랙 전력 밀도가 계속 증가함에 따라 수랭식 냉각 솔루션이 필요합니다. 하이퍼스케일 시설의 설계는 장기적인 확장성을 염두에 두고 설계되어, 코로케이션이나 엔터프라이즈 데이터센터와 비교하여 냉각수 총 소비량이 더 많이 소모됩니다. 또한 하이퍼스케일은 에너지 소비량 감소, 전력 사용 효율 향상, 운영 비용 절감을 실현하기 위해 보다 일찍 대규모로 액체 냉각을 채택하고 있습니다. 거대한 물리적 공간, 고밀도 컴퓨팅 환경, 표준화된 액체 냉각 아키텍처가 결합되어 하이퍼스케일 데이터센터의 라이프사이클 전반에 걸쳐 냉각수 사용량이 크게 증가하여 시장 규모에서 우위를 점할 수 있게 되었습니다.

"냉각 기술별로는 DTC(Direct-to-Chip) 기술이 예측 기간 동안 사용량 기준으로 가장 큰 점유율을 차지할 것으로 예상됩니다."

DTC 냉각수는 현대 데이터센터에서 프로세서가 생성하는 증가하는 열을 제어하는 가장 효과적이고 확장성이 높은 방법이기 때문에 사용량 기준으로 가장 큰 점유율을 차지하는 것으로 추정됩니다. DTC 냉각 시스템은 CPU와 GPU에서 효과적인 방열을 실현하여 AI, 고성능 컴퓨팅, 클라우드 워크로드의 전력 수요 증가에 따라 시스템 전체의 액침 냉각이 필요하지 않도록 합니다. 이 방식은 기존 서버 시스템과 연동이 가능하기 때문에 신규 시설 및 설비 업데이트를 하는 기존 시설 모두에서 액체 냉각을 도입할 수 있습니다. DTC 시스템은 여러 프로세서 전체에 걸쳐 냉각수 유량을 일정하게 유지해야 하기 때문에 전용 냉각 시스템이나 국소 냉각 시스템에 비해 총 소비량이 많아집니다. 또한, 운영의 유연성을 확보하면서 에너지 효율을 크게 향상시켜 고밀도 랙을 사용하는 하이퍼스케일 사업자와 코로케이션 사업자에게 최적의 선택이 될 수 있습니다. 우수한 성능과 신뢰성 높은 서비스, 간편한 도입으로 널리 채택되어 냉각액에 대한 지속적인 수요를 창출하고 있습니다.

"냉각 방식별로는 단상 냉각 부문이 예측 기간 동안 수량 기준으로 가장 큰 점유율을 차지할 것으로 예상됩니다."

단상 냉각 부문은 현대 데이터센터에서 가장 안정적이고 신뢰할 수 있으며 널리 채택된 액체 냉각 솔루션이기 때문에 가장 큰 비중을 차지할 것으로 예상됩니다. 단상 시스템의 설계는 냉각 공정 전체에 걸쳐 냉각액이 일정한 물리적 상태를 유지하기 때문에 관리 및 유지보수가 용이하며, 이중상 시스템에 비해 운영 효율이 향상됩니다. 단상 냉각의 운영 안정성과 높은 시스템 이해도는 액체 냉각 시스템을 도입하는 하이퍼스케일 데이터센터, 코로케이션 시설, 대규모 기업 데이터센터에서 이 기술에 대한 강한 선호를 불러일으키고 있습니다. 단상 냉각의 도입으로 CPU 및 GPU의 발열 증가를 관리하는 표준 솔루션이 된 DTC 시스템 및 콜드 플레이트 시스템과의 원활한 운영이 가능해졌습니다. 이러한 시스템에서는 여러 서버와 랙을 통해 액체가 지속적으로 흐르기 때문에 냉각수의 총 소비량이 증가합니다. 기존 냉각 시스템 및 물 순환 루프는 단상 냉각 시스템과 통합할 수 있어 운영상의 이점을 제공합니다. 이는 보다 안전하고 경제적인 도입을 가능하게 하여 사용량 증가를 촉진하고, 예측 기간 동안 단상 냉각이 시장을 선도하는 위치를 차지할 것으로 예상됩니다.

"액체 유형별로는 물-글리콜 혼합물 부문이 예측 기간 동안 부피 기준으로 가장 큰 점유율을 차지할 것으로 예상됩니다."

물-글리콜 혼합물 부문은 최적의 열 성능과 비용 효율성, 데이터센터 냉각 시스템에 대한 안정적인 냉각 성능을 제공하기 때문에 예측 기간 동안 가장 큰 점유율을 차지할 것으로 추정됩니다. 수성 냉각제는 뛰어난 열전달 성능을 발휘하며, 여기에 글리콜을 첨가하여 동결 방지, 내식성, 시스템 내구성을 향상시켜 다양한 기후 및 운영 환경에서 사용할 수 있습니다. 물-글리콜 혼합물은 하이퍼스케일, 코로케이션 및 엔터프라이즈 데이터센터에서 가장 널리 채택된 액체 냉각 시스템인 D2C 냉각 시스템 및 단상 냉각 시스템의 주요 냉각제 역할을 합니다. 본 시스템은 기존 냉수 시스템 및 열교환기 인프라에 연결이 가능하며, 기존 시스템을 크게 변경하지 않아도 되기 때문에 대규모 도입이 가능합니다. 데이터센터 운영자들은 특수한 취급이 필요한 전용 유전체 유체와 달리 저렴하고 유지보수가 용이하여 물-글리콜 혼합액을 선호하고 있습니다. 성능, 유연성, 경제적 이점이 결합되어 예측 기간 동안 시장 점유율을 유지하는 데 성공할 수 있는 기반이 될 것입니다.

세계의 데이터센터용 냉각액 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정 및 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 분석

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 데이터센터용 냉각액 시장 : 액체 유형별

제10장 데이터센터용 냉각액 시장 : 냉각 기술별

제11장 데이터센터용 냉각액 시장 : 데이터센터 유형별

제12장 데이터센터용 냉각액 시장 : 냉각 방식별

제13장 데이터센터용 냉각액 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSM 26.03.26The data center liquid cooling fluids market is projected to grow from USD 0.28 billion in 2025 to USD 2.01 billion in 2032, at a CAGR of 32.7% during the forecast period. The significant increase in computing density driven by cloud computing, artificial intelligence, and high-performance applications is the primary factor propelling the data center liquid-cooling fluids market. This increase is beyond the capacity of conventional air cooling to handle.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Value (USD Million/Billion) Volume (Thousand Liters) |

| Segments | Fluid Type, Data Center Type, Cooling Technology, Cooling Method, And Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

Modern data centers use high-performance GPUs, accelerators, and processors that generate concentrated heat at the chip and rack levels. This leads to heat problems that air-based systems cannot manage. Better heat transfer is provided by liquid cooling fluids, which enable direct heat removal from vital components. Even with extremely high-power densities, this helps maintain steady operating temperatures. The demand for improved space utilization, lower energy consumption, and greater operational reliability is another factor driving the move toward high-density computing.

"By data center type, the hyperscale segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The hyperscale segment is estimated to hold the largest share in terms of volume of the data center liquid cooling fluids market during the forecast period, as hyperscale data centers operate at high computing power and experience rapid facility growth. Hyperscale operators build massive facilities that global cloud and technology providers use to deliver cloud services while supporting artificial intelligence, machine learning, and high-performance computing workloads that generate continuous, extreme heat. Data centers need liquid-cooling solutions because they operate at very high server counts while rack power densities continue to rise. The design of hyperscale facilities includes long-term scalability features, leading to greater total cooling fluid consumption than in colocation or enterprise data centers. Hyperscale also adopts liquid cooling earlier and on a larger scale to achieve lower energy consumption, improved power usage effectiveness, and reduced operational costs. The combination of large physical footprints, dense compute deployments, and standardized liquid-cooling architectures results in significantly higher volumes of cooling fluids used over the lifecycle of hyperscale data centers, driving their dominance in market volume.

"By cooling technology, the direct-to-chip cooling fluids segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The direct-to-chip cooling fluids segment is estimated to hold the largest share in terms of volume during the forecast period, as it is the most effective and scalable method for controlling the increasing heat generated by processors in contemporary data centers. A direct-to-chip cooling system provides effective heat dissipation at the CPU and GPU, eliminating the need for complete system immersion, as AI, high-performance computing, and cloud workloads increase power requirements. The approach enables server operators to use liquid cooling in both newly constructed and existing facilities that undergo equipment updates, as it works with their current server systems. Direct-to-chip systems must maintain constant cooling fluid flow across multiple processors, resulting in higher total fluid consumption than specialized or localized cooling systems. Direct-to-chip cooling provides substantial energy-efficiency improvements while enabling operational flexibility, making it the top choice for hyperscale and colocation operators that use high-density racks. The solution achieves widespread adoption by combining excellent performance with dependable service and simple implementation, thereby creating ongoing demand for cooling fluids.

"By cooling method, the single-phase cooling segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The single-phase cooling segment is expected to hold the largest share, as it is the most established, reliable, and widely used liquid-cooling solution for contemporary data centers. The design of single-phase systems is easier to manage and maintain because their liquid coolants maintain a constant physical state throughout the cooling process, thereby improving operational efficiency compared to two-phase systems. The operational dependability and system understanding of single-phase cooling create a strong preference for this technology among hyperscale data centers, colocation facilities, and large-scale enterprise data centers that implement liquid-cooling systems. The implementation of single-phase cooling enables seamless operation with direct-to-chip and cold plate systems, which have become standard solutions for managing increased CPU and GPU thermal output. The systems require constant liquid flow through their multiple servers and racks, leading to increased total cooling fluid consumption. The existing cooling systems and water loops can be integrated with single-phase cooling systems, delivering operational advantages that make deployment safer and more affordable, thereby driving increased usage and establishing single-phase cooling as the market leader during the forecast period.

"By fluid type, the water glycol mixtures segment is estimated to hold the largest share, in terms of volume, during the forecast period."

The water-glycol mixtures segment is estimated to hold the largest share, in terms of volume, during the forecast period because it delivers optimal thermal performance and cost efficiency, as well as dependable cooling performance for data center cooling systems. Water-based coolants deliver exceptional heat transfer performance, which glycol addition enhances by providing freeze protection, corrosion resistance, and system durability for use in various climate and operational environments. Water-glycol mixtures serve as the primary coolant for direct-to-chip and single-phase cooling systems, which are the most widely used liquid-cooling systems in hyperscale, colocation, and enterprise data centers. The system enables large-scale implementation by connecting to existing chilled water systems and heat exchanger infrastructure, requiring no major changes to current systems. Data center operators prefer water-glycol mixtures because they are inexpensive and easy to maintain, unlike specialized dielectric fluids, which require specialized handling. The combination of their performance, flexibility, and economic benefits provides the basis for their success in maintaining market share during the forecast period.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 45%, Tier 2 - 22%, and Tier 3 - 33%

- By Designation: C-Level Executives- 50%, Directors- 10%, and Others - 40%

- By Region: North America - 17%, Asia Pacific - 17%, Europe - 33%, Middle East & Africa - 25%, and South America - 8%

Shell plc (UK), The Chemours Company (US), Dow Inc. (US), Valvoline Global Operations (US), Exxon Mobil Corporation (US), and others are the key players in the data center liquid cooling fluids market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage:

The report defines segments and projects the size of the data center liquid cooling fluids market based on fluid type, data center type, cooling technology, cooling method, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help market leaders/new entrants by providing the closest approximations of revenue for the data center liquid cooling fluids market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (Growth in data center market, Rise in use of liquid cooling technology in data centers boosts demand for Liquid cooling fluids, and Increase in server rack density), restraints (Technology under development for two-phase PFAS-free fluids for immersion cooling, Lack of widely accepted industry standards, and High initial investment cost), opportunities (Growing installation of AI-based mega data centers, Growing demand for energy efficient cooling solutions, Data center owners and operators face growing pressure to lower carbon footprint, Increasing demand for environment friendly fluid technology, such as PFAS free and bio-based fluids, and Growth in DTC liquid cooling technology) and challenges (Fluid contamination risk increases maintenance burden, and Maintenance challenges and cost burden in immersion cooling for data centers) influencing the growth of the data center liquid cooling fluids market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the data center liquid cooling fluids market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the data center liquid cooling fluids market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the data center liquid cooling fluids market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Shell plc (UK), The Chemours Company (US), Dow Inc. (US), Valvoline Global Operations (US), and Exxon Mobil Corporation (US), and others are the key players in the data center liquid cooling fluids market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.4 INCLUSIONS & EXCLUSIONS

- 1.4.1 YEARS CONSIDERED

- 1.4.2 CURRENCY CONSIDERED

- 1.4.3 UNIT CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER LIQUID COOLING FLUIDS MARKET

- 3.2 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY FLUID TYPE AND REGION

- 3.3 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY COOLING METHOD

- 3.4 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY COOLING TECHNOLOGY

- 3.5 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in data center market

- 4.2.1.2 Rise in use of liquid cooling technology in data centers

- 4.2.1.3 Increase in server rack density

- 4.2.2 RESTRAINTS

- 4.2.2.1 Technology under development for two-phase PFAS-free fluids for immersion cooling

- 4.2.2.2 Lack of widely accepted industry standards

- 4.2.2.3 High initial investment cost

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing installation of AI-based mega data centers

- 4.2.3.2 Growing demand for energy-efficient cooling solutions

- 4.2.3.3 Data center owners and operators face growing pressure to lower carbon footprint

- 4.2.3.4 Increasing demand for environmentally friendly fluid technology and growth in DTC liquid cooling technology

- 4.2.4 CHALLENGES

- 4.2.4.1 Fluid contamination risk increases maintenance burden

- 4.2.4.2 Maintenance challenges and cost burden in immersion cooling for data centers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER LIQUID COOLING FLUIDS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.3 EMERGING BUSINESS MODELS

- 4.4.4 ECOSYSTEM SHIFTS

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ELECTRONICS INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ARTIFICIAL INTELLIGENCE INDUSTRY

- 5.2.5 RESEARCH & DEVELOPMENT (R&D) EXPENDITURE

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.2 AVERAGE SELLING PRICE OF DATA CENTER TYPE AMONG KEY PLAYERS, BY COOLING TECHNOLOGY, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 2710)

- 5.6.2 EXPORT SCENARIO (HS CODE 2710)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 DIRECT LIQUID COOLING AT HLRS HAWK SUPERCOMPUTER ENABLES DATA-CENTER-LEVEL ENERGY OPTIMIZATION

- 5.10.2 LIQUID COOLING ENABLES ENERGY-EFFICIENT SCALING OF HIGH-DENSITY, AI-DRIVEN DATA CENTER INFRASTRUCTURE

- 5.10.3 DOWNUNDER GEOSOLUTIONS ADOPTS IMMERSION COOLING TECHNOLOGY BY GREEN REVOLUTION COOLING

- 5.10.4 GREEN REVOLUTION COOLING AND TEXAS ADVANCED COMPUTING CENTER COLLABORATE TO ENHANCE SUPERCOMPUTER PERFORMANCE

- 5.11 IMPACT OF 2025 US TARIFF ON DATA CENTER LIQUID COOLING FLUIDS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON DATA CENTER INDUSTRY

- 5.11.5.1 Hyperscale data centers

- 5.11.5.2 AI/ML data centers

- 5.11.5.3 Cryptocurrency mining data centers

- 5.11.5.4 Others (Edge data centers and colocation data centers)

6 TECHNOLOGY ANALYSIS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ETHYLENE GLYCOL: HEAT TRANSFER PERFORMANCE OPTIMIZATION FOR DATA CENTER COOLING

- 6.1.2 PROPYLENE GLYCOL: SUSTAINABLE MANUFACTURING ROUTES AND SAFETY-DRIVEN COOLING FLUID TECHNOLOGY

- 6.1.3 DE-IONIZED (DI) WATER: ADVANCED PURIFICATION TECHNOLOGIES AND HIGH-EFFICIENCY THERMAL MANAGEMENT

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 IMMERSION COOLING TANK AND ENCLOSURE DESIGN

- 6.2.2 THERMAL INTERFACE OPTIMIZATION AND HARDWARE CONFIGURATION

- 6.2.3 DATA CENTER INFRASTRUCTURE MANAGEMENT

- 6.2.4 IMMERSION-COMPATIBLE HARDWARE DESIGN

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT TERM (2026-2027)| QUALIFICATION & EARLY SCALING

- 6.3.2 MEDIUM-TERM (2027-2030) | ADVANCED FLUIDS & SYSTEM INTEGRATION

- 6.3.3 LONG-TERM (2030-2035) | FLUID FIRST ARCHITECTURES & SUSTAINABILITY INTEGRATION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPE

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS OF PATENTS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 LIST OF MAJOR PATENTS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 DIRECT-TO-CHIP COOLING FOR AI AND HIGH POWER COMPUTING: NEXT GENERATION GPUS, CPUS, AND AI ACCELERATORS

- 6.5.2 SINGLE PHASE IMMERSION COOLING OF IT HARDWARE: HIGH-DENSITY AI TRAINING AND INFERENCE DATA CENTERS

- 6.5.3 TWO-PHASE IMMERSION COOLING FOR EXTREME RACK DENSITY: SPACE CONSTRAINED, ENERGY OPTIMIZED DATA CENTERS

- 6.5.4 HIGH-TEMPERATURE LIQUID COOLING FOR HEAT REUSE: ENERGY RECOVERY AND SUSTAINABLE DATA CENTER OPERATION

- 6.5.5 EDGE, MODULAR & RETROFIT DATA CENTER COOLING: DISTRIBUTED, SPACE LIMITED, AND LEGACY INFRASTRUCTURE

- 6.6 IMPACT OF AI/GEN AI ON DATA CENTER LIQUID COOLING FLUIDS MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES: COMPANIES/INSTITUTIONS USE CASES

- 6.6.3 CASE STUDIES OF DATA CENTER LIQUID COOLING FLUIDS MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DATA CENTER LIQUID COOLING FLUIDS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 PFAS PHASE-OUT AND TRANSITION TO PFAS-FREE FLUIDS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS OF VARIOUS DATA CENTER TYPES

- 8.6 MARKET PROFITABILITY

- 8.6.1 REVENUE POTENTIAL

- 8.6.2 COST DYNAMICS

- 8.6.3 MARGIN OPPORTUNITIES IN VARIOUS DATA CENTERS

9 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY FLUID TYPE

- 9.1 INTRODUCTION

- 9.2 WATER GLYCOL MIXTURES (ETHYLENE GLYCOL & PROPYLENE GLYCOL)

- 9.2.1 RELIABILITY AND SCALABILITY TO DRIVE MARKET

- 9.3 SYNTHETIC HYDROCARBONS

- 9.3.1 SUPERIOR CHEMICAL STABILITY, LOW VOLATILITY, AND STRONG COMPATIBILITY TO DRIVE MARKET

- 9.4 FLUOROCARBON-BASED FLUIDS

- 9.4.1 INCREASING DEMAND FOR COMPACT AND ENERGY-EFFICIENT DATA CENTER INFRASTRUCTURE TO DRIVE MARKET

- 9.5 OTHER FLUID TYPES

10 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY COOLING TECHNOLOGY

- 10.1 INTRODUCTION

- 10.2 DIRECT TO CHIP COOLING FLUIDS

- 10.2.1 GROWING ADOPTION OF HIGH-PERFORMANCE COMPUTING AND ADVANCED PROCESSOR TECHNOLOGIES TO DRIVE MARKET

- 10.3 IMMERSION COOLING FLUIDS

- 10.3.1 GROWING INVESTMENTS IN HYPERSCALE DATA CENTERS AND EDGE COMPUTING FACILITIES TO DRIVE MARKET

11 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY DATA CENTER TYPE

- 11.1 INTRODUCTION

- 11.2 HYPERSCALE

- 11.2.1 MAJOR DEMAND FOR ADVANCED COOLING SOLUTIONS TO DRIVE MARKET

- 11.3 COLOCATION

- 11.3.1 HIGH-DENSITY WORKLOADS WHILE IMPROVING OPERATIONAL EFFICIENCY AND REDUCING ENERGY CONSUMPTION TO DRIVE DEMAND

- 11.4 ENTERPRISE

- 11.4.1 SHIFT TOWARD HYBRID CLOUD AND PRIVATE CLOUD ENVIRONMENTS TO DRIVE MARKET

12 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY COOLING METHOD

- 12.1 INTRODUCTION

- 12.2 SINGLE PHASE COOLING

- 12.2.1 EFFICIENT COOLING OF HIGH-DENSITY SERVER RACKS TO DRIVE MARKET

- 12.3 TWO-PHASE COOLING

- 12.3.1 SUPERIOR HEAT TRANSFER EFFICIENCY TO DRIVE MARKET

13 DATA CENTER LIQUID COOLING FLUIDS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Rapid scaling of artificial intelligence, machine learning, and high-performance computing workloads

- 13.2.2 CANADA

- 13.2.2.1 Advanced adoption as AI and high-performance computing deployments

- 13.2.3 MEXICO

- 13.2.3.1 Adoption of advanced thermal management systems, including direct-to-chip and immersion cooling fluids

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Adoption of direct-to-chip and immersion cooling to drive market

- 13.3.2 GERMANY

- 13.3.2.1 Increased adoption of direct-to-chip and immersion cooling to improve energy efficiency

- 13.3.3 SPAIN

- 13.3.3.1 Rise in demand from niche HPC applications toward mainstream hyperscale and AI workloads

- 13.3.4 FRANCE

- 13.3.4.1 Deployment of high-density data center infrastructure to support cloud, AI, and sovereign data workloads

- 13.3.5 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 AI infrastructure expansion and high-density computing driving liquid cooling adoption

- 13.4.2 SOUTH KOREA

- 13.4.2.1 Investment in AI and cloud infrastructure to drive market

- 13.4.3 JAPAN

- 13.4.3.1 Rising rack densities and high electricity costs pushing operators toward liquid and immersion cooling solutions

- 13.4.4 INDIA

- 13.4.4.1 Rapid hyperscale growth and AI readiness to increase demand

- 13.4.5 MALAYSIA

- 13.4.5.1 Growing adoption in hyperscale and AI-ready data centers to boost market

- 13.4.6 AUSTRALIA

- 13.4.6.1 Rising AI workloads, energy efficiency mandates, and high-density data center expansion to drive demand

- 13.4.7 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Regional hub for AI, cloud, and high-performance computing

- 13.5.1.2 UAE

- 13.5.1.2.1 Continued hyperscale investment, AI localization requirements, and sovereign cloud initiatives to drive market

- 13.5.1.3 Rest of GCC

- 13.5.1.1 Saudi Arabia

- 13.5.2 SOUTH AFRICA

- 13.5.2.1 National data infrastructure rapidly evolves to support AI, cloud expansion, and high-performance computing

- 13.5.3 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Largest digital infrastructure hub to increase demand

- 13.6.2 ARGENTINA

- 13.6.2.1 Rising hyperscale developments and power-cost sensitivity to drive market

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2024

- 14.3.1 TOP 5 PLAYERS' REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Fluid type footprint

- 14.7.5.4 Data center type footprint

- 14.7.5.5 Cooling technology footprint

- 14.7.5.6 Cooling method footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 MAJOR PLAYERS

- 15.1.1 SHELL PLC

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 THE CHEMOURS COMPANY

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 VALVOLINE GLOBAL OPERATIONS

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 DOW INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 EXXON MOBIL CORPORATION

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 LUBRIZOL

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 CASTROL LIMITED

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.8 FUCHS SE

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.9 SUBMER

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.9.3.3 Other developments

- 15.1.10 INVENTEC PERFORMANCE CHEMICALS

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.11 GREEN REVOLUTION COOLING

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 ENGINEERED FLUIDS

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Deals

- 15.1.13 CARGILL, INCORPORATED

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.14 ENEOS CORPORATION

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 TOTALENERGIES

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.16 DYNALENE, INC.

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.16.3 Recent developments

- 15.1.17 DCX LIQUID COOLING SYSTEMS

- 15.1.17.1 Business overview

- 15.1.17.2 Products/Solutions/Services offered

- 15.1.17.3 Recent developments

- 15.1.18 HONEYWELL INTERNATIONAL INC.

- 15.1.18.1 Business overview

- 15.1.18.2 Products/Solutions/Services offered

- 15.1.18.3 Recent developments

- 15.1.19 PETRONAS LUBRICANTS INTERNATIONAL

- 15.1.19.1 Business overview

- 15.1.19.2 Products/Solutions/Services offered

- 15.1.19.3 Recent developments

- 15.1.19.3.1 Deals

- 15.1.20 OLEON NV

- 15.1.20.1 Business overview

- 15.1.20.2 Products/Solutions/Services offered

- 15.1.20.3 Recent developments

- 15.1.20.3.1 Product launches

- 15.1.20.3.2 Deals

- 15.1.21 CHEVRON PHILLIPS CHEMICAL COMPANY LLC. (CHEVRON CORPORATION)

- 15.1.21.1 Business overview

- 15.1.21.2 Products/Solutions/Services offered

- 15.1.21.3 Recent developments

- 15.1.21.3.1 Expansion

- 15.1.22 RECOCHEM CORPORATION

- 15.1.22.1 Business overview

- 15.1.22.2 Products/Solutions/Services offered

- 15.1.22.3 Recent developments

- 15.1.23 ARTECO

- 15.1.23.1 Business overview

- 15.1.23.2 Products/Solutions/Services offered

- 15.1.23.3 Recent developments

- 15.1.24 LIQUITHERM TECHNOLOGIES GROUP LTD

- 15.1.24.1 Business overview

- 15.1.24.2 Products/Solutions/Services offered

- 15.1.24.3 Recent developments

- 15.1.1 SHELL PLC

- 15.2 OTHER PLAYERS

- 15.2.1 SANMING HEXAFLUO CHEMICALS CO., LTD.

- 15.2.2 GUANGDONG GIANT FLUORINE ENERGY SAVING TECHNOLOGY CO., LTD.

- 15.2.3 ZHEJIANG NOAH FLUOROCHEMICAL CO., LTD

- 15.2.4 FLUOREZ TECHNOLOGY INC.

- 15.2.5 SHENZHEN HUAYI BROTHER TECHNOLOGY CO., LTD.

- 15.2.6 AMER TECHNOLOGY CO., LTD.

- 15.2.7 NOVVI, LLC.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 List of participating companies for primary research

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.3 BASE NUMBER CALCULATION

- 16.3.1 DEMAND-SIDE APPROACH

- 16.3.2 SUPPLY-SIDE APPROACH

- 16.4 MARKET FORECAST APPROACH

- 16.4.1 SUPPLY SIDE

- 16.4.2 DEMAND SIDE

- 16.5 DATA TRIANGULATION

- 16.6 FACTOR ANALYSIS

- 16.7 RESEARCH ASSUMPTIONS

- 16.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS