|

시장보고서

상품코드

1993560

수용성 비료 시장 : 유형별, 시용법별, 형태별, 작물 유형별, 지역별 - 세계 예측(-2031년)Water-soluble Fertilizers Market by Type, Mode of Application, Form, Crop Type, and Region - Global Forecast to 2031 |

||||||

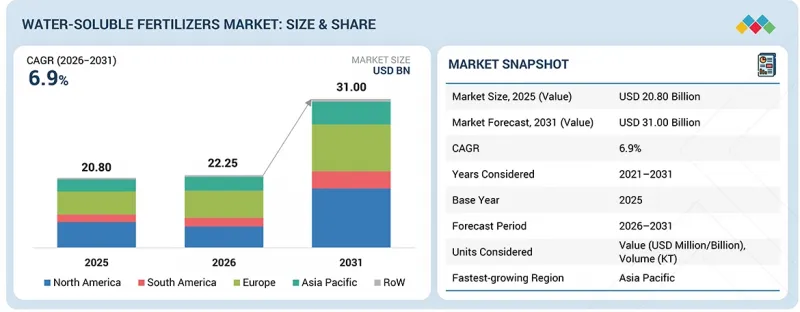

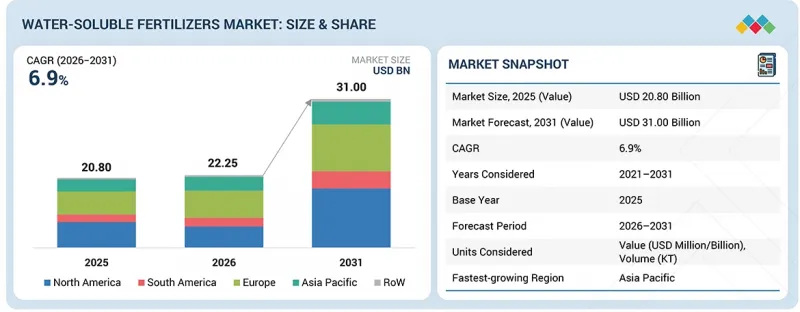

세계의 수용성 비료 시장 규모는 2026년에 추정 222억 5,000만 달러이며, 2031년까지 310억 달러에 달할 것으로 예측되며, CAGR로 6.9%의 성장이 전망됩니다.

디지털 농업 도구, 정밀 시비 시스템, 데이터 기반 영양 관리 플랫폼의 통합으로 WSF 업계의 제품 개발 및 현장 성능은 변화를 보이고 있습니다. 야라 인터내셔널(Yara International)과 같은 주요 기업들은 디지털 농업 솔루션을 활용하여 시비 추천 최적화, 영양분 이용 효율(NUE) 향상, 작물 수확량 증가를 위해 노력하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 달러, 톤 |

| 부문 | 유형, 작물 유형, 시용법, 형태, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

2023년 3월, 하이파 그룹은 관개 및 엽면 살포용으로 설계된 고효율 수용성 비료 제품군인 하이파 보너스(Haifa Bonus)를 출시하였습니다. 본 제품은 용해성 향상과 작물별 영양 밸런스를 실현하였습니다. 이러한 제품 혁신은 정밀농업 및 제어 영양 공급 시스템의 발전과 함께 세계 수용성 비료(WSF) 시장의 지속가능한 성장, 지속가능성 향상, 고부가가치 작물 생산성 실현을 촉진하고 있습니다.

수용성 비료 시장의 기회와 변화는 정밀농업과 고효율 영양소 관리로의 전환 가속화와 밀접한 관련이 있습니다. 수용성 비료는 작물 생산성 향상, 우수한 품질, 투입물 최적화에 대한 수요 증가에 힘입어 농업인과 제조업체 모두에게 큰 상업적 잠재력을 가지고 있습니다. 농가의 경우, 시비 관개 및 엽면 살포를 통한 수용성 비료의 사용은 특히 원예 및 고부가가치 작물에서 양분 이용 효율을 높이고 침출 및 휘발로 인한 손실을 줄여 헥타르당 수익 향상에 기여할 수 있습니다. 특수 비료에 대한 수요 증가는 제조업체들에게 제품 포트폴리오의 다양화, 특정 작물을 위한 미량영양소 강화 제제 개발, 첨단 용해 기술에 대한 투자, 전략적 유통 파트너십 구축과 같은 기회를 창출하고 있습니다. 동시에 시장은 디지털 농업 플랫폼, 관개 시스템 자동화, 영양염류 유출에 대한 환경 규제 강화, 지속가능하고 잔류물을 최소화하는 농법에 대한 관심 증가로 인해 변화의 소용돌이에 휩싸여 경쟁 역학 및 장기적인 성장 궤도를 재구성하고 있습니다.

AI를 활용한 영양소 최적화 : 수용성 비료(WSF) 시장에서 AI와 머신러닝은 특정 작물용 영양제 개발, NPK 비율 최적화, 토양 및 기후 데이터에 기반한 결핍 패턴 예측에 점점 더 많이 활용되고 있습니다. 이러한 기술은 데이터에 기반한 추천을 통해 제품 개발 주기를 단축하고, 영양소 이용 효율(NUE)을 향상시킵니다.

첨단 제형 기술 : 완전 킬레이트화 미량영양소, 초고용해성 등급, 저나트륨 제형, 방출 제어 영양소 블렌딩과 같은 혁신은 시비 관개 및 수경재배 시스템에서 수용성 비료 제품의 성능과 적합성을 향상시킵니다. 이러한 발전은 영양소의 안정성, 흡수 효율, 작물 반응의 일관성을 향상시킵니다.

정밀 시비 시스템 : 자동 관개 컨트롤러, 토양 수분 센서, IoT 지원 시비 장치, GPS 기반 농장 관리 플랫폼을 통합하여 정확하고 균일한 영양분 공급을 가능하게 합니다. 이를 통해 영양분 손실을 줄이고, 환경에 미치는 영향을 최소화하며, 표적화 된 적용 전략을 통해 수확 가능성을 극대화합니다.

"수용성 비료 시장의 형태 부문에서는 건조가 주요 부문입니다."

수용성 비료(WSF) 시장에서 건조 제제는 다양한 유형의 비료 제품을 포함하는 형태 부문 중 가장 큰 비중을 차지하고 있습니다. 건조 제품이 시장을 독점하고 있는 이유는 장기간 품질을 유지할 수 있고, 보관 및 운송이 용이하며, 영양소 함량이 액체 제품을 능가하기 때문입니다. 결정 또는 분말 형태의 건조 수용성 비료는 용해도가 높고, 시비 관개 및 엽면 살포 시스템과의 호환성이 좋기 때문에 다양한 유형의 작물에 적합합니다. 이 시스템을 통해 제조업체는 영양분을 유연하게 조정할 수 있어 작물의 요구 사항과 생육 단계에 맞는 정확한 영양액을 만들 수 있습니다. 건식 비료의 비용 효율성, 경량 포장, 유출 방지 특성으로 인해 선진국과 신흥국 농업 시장 모두에서 건식 비료의 사용이 증가하고 있으며, 그 결과 건식 비료는 전체 수용성 비료(WSF) 시장에서 주요 부문으로 자리 잡고 있습니다.

세계의 수용성 비료 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 수용성 비료 시장 : 유형별

제10장 수용성 비료 시장 : 작물 유형별

제11장 수용성 비료 시장 : 시용법별

제12장 수용성 비료 시장 : 형태별

제13장 수용성 비료 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 인접 시장과 관련 시장

제18장 부록

KSM 26.04.15The market is estimated at USD 22.25 billion in 2026 and is projected to reach USD 31.00 billion by 2031, at a CAGR of 6.9%. The integration of digital agronomy tools, precision fertigation systems, and data-driven nutrient management platforms is transforming product development and on-field performance in the WSF industry. Leading companies such as Yara International are leveraging digital farming solutions to optimize nutrient recommendations, enhance nutrient use efficiency (NUE), and improve crop yield outcomes.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD) and Volume (Tons) |

| Segments | By Type, Crop Type, Mode of Application, Form, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

In March 2023, Haifa Group launched Haifa Bonus, a high-efficiency water-soluble fertilizer range designed for fertigation and foliar application, offering enhanced solubility and crop-specific nutrient balance. Such product innovations, combined with advancements in precision agriculture and controlled nutrient delivery systems, are positioning the WSF market for sustained growth, improved sustainability, and higher-value crop productivity worldwide.

Opportunities and disruption in the water-soluble fertilizer market are closely linked to the accelerating transition toward precision agriculture and high-efficiency nutrient management. WSF presents substantial commercial potential for both growers and manufacturers, supported by the rising demand for improved crop productivity, superior produce quality, and optimized input utilization. For farmers, the adoption of WSF through fertigation and foliar application enhances nutrient use efficiency, reduces losses from leaching and volatilization, and supports higher returns per hectare, particularly in horticulture and high-value crops. For manufacturers, expanding demand for specialty fertilizers creates opportunities to diversify product portfolios, develop crop-specific and micronutrient-enriched formulations, invest in advanced solubility technologies, and establish strategic distribution partnerships. At the same time, the market is undergoing disruption driven by digital agronomy platforms, automation in irrigation systems, tightening environmental regulations on nutrient runoff, and increasing preference for sustainable and residue-minimizing farming practices, collectively reshaping competitive dynamics and long-term growth trajectories:

AI-driven nutrient optimization: Artificial intelligence (AI) and machine learning are increasingly being utilized in the water-soluble fertilizer (WSF) market to develop crop-specific nutrient formulations, optimize NPK ratios, and predict deficiency patterns based on soil and climatic data. These technologies accelerate product development cycles and enhance nutrient use efficiency (NUE) through data-driven recommendations.

Advanced formulation technologies: Innovations such as fully chelated micronutrients, ultra-high solubility grades, low-sodium formulations, and controlled nutrient-release blends improve the performance and compatibility of WSF products in fertigation and hydroponic systems. These advancements enhance nutrient stability, absorption efficiency, and crop response consistency.

Precision fertigation systems: Integration of automated irrigation controllers, soil moisture sensors, IoT-enabled fertigation units, and GPS-based farm management platforms enables accurate and uniform nutrient delivery. This reduces nutrient losses, minimizes environmental impact, and maximizes yield potential through targeted application strategies.

"Dry stood as the major segment within the form segment of the water-soluble fertilizer market."

The water-soluble fertilizer (WSF) market shows that dry formulations take up the largest part of its form segment, which includes various types of fertilizer products. The market dominance of dry products occurs because these products maintain their quality for extended periods, while they remain easier to store and transport, and their nutrient content exceeds that of liquid products. The dry water-soluble fertilizers, which come in crystalline or powder form, provide better solubility and compatibility with fertigation and foliar systems, which make them suitable for various crop types. The system enables growers to create precise nutrient solutions that match crop requirements and growth stages because it provides them with flexible options to customize nutrients. The cost-effective nature of dry formulations, together with their lightweight packaging and their ability to prevent spills, has led to their increased use in both developed and emerging agricultural markets, which results in dry formulations maintaining their status as the top segment in the complete WSF market.

"Within the mode of application segment, fertigation is estimated to account for the largest share."

The water-soluble fertilizer (WSF) market shows its highest application mode share through fertigation. The method exists as the dominant choice because it enables irrigation systems to deliver nutrients directly to crops while achieving equal nutrient distribution and exact delivery of required nutrients. The method enhances nutrient usage efficiency through its practice of applying nutrients according to the specific growth periods of crops, which helps prevent nutrient loss through leaching or volatilization. The method finds common use in horticulture and greenhouse farming and high-value field crop production in areas that possess developed drip and sprinkler irrigation systems. The method of fertigation helps farmers by decreasing their labor expenses while allowing them to save water and establish environmentally friendly farming systems. The worldwide adoption of micro-irrigation systems establishes fertigation as the primary application method for WSF products in the market.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the water-soluble fertilizer market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) - 10%

Prominent companies in the market include Nutrien (Canada), Yara International (Norway), The Mosaic Company (US), ICL Group (Israel), PhosAgro (Russia), Incitec Pivot Limited (Australia), SQM (Chile), K+S Aktiengesellschaft (Germany), Grupa Azoty (Poland), Coromandel International Limited (India), Gujarat State Fertilizers & Chemicals Limited (India), Deepak Fertilisers and Petrochemicals Corporation Limited (India), Katyayani Organics (India), Zuari FarmHub Limited (India), and Aeries Agro Limited (India).

Research Coverage:

This research report categorizes the water-soluble fertilizers market by type (nitrogenous, phosphatic, potassic, and micronutrients), mode of application (foliar and fertigation), form, by crop type (field crop, horticulture crop, turf & ornaments, others), and region. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the global water-soluble fertilizer market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. New product & service launches, mergers and acquisitions, and recent developments associated with the global water-soluble fertilizer market. Competitive analysis of upcoming startups in the global water-soluble fertilizer market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall water-soluble fertilizer market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. In-depth Segmentation across Type, Source, Formulation, Mode of Application, and Crop Type: Comprehensive analysis across nitrogenous, phosphatic, potassic, and micronutrient-based water-soluble fertilizers; evaluation by synthetic/mineral sources and specialty chelated nutrients; and assessment across dry and liquid formulations, fertigation and foliar modes, and major crop categories. The study examines key drivers (expansion of horticulture and protected cultivation, rising micro-irrigation adoption, and increasing focus on nutrient use efficiency), restraints (price volatility of raw materials and infrastructure dependency on irrigation systems), opportunities (advancements in specialty chelation technologies, customized crop-specific blends, and precision fertigation integration), and challenges (intense price competition and limited technical awareness among smallholder farmers).

2. Region-specific Insights with Focus on Emerging Markets: The report provides detailed country- and region-level analysis, highlighting growth opportunities across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. It evaluates regional demand patterns, irrigation penetration, regulatory policies related to nutrient management, and investment trends in precision agriculture, offering strategic guidance for expansion and localization initiatives.

3. Competitive Intelligence and Innovation Landscape: Leading market participants, including Yara International (Norway), Nutrien (Canada), ICL Group (Israel), Haifa Group (Israel), and Coromandel International Limited (India), are profiled in detail. The report covers recent product launches, capacity expansions, strategic partnerships, and investments in specialty nutrient technologies shaping the competitive dynamics of the global WSF market.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for investment planning and market opportunity assessment in the global water-soluble fertilizer sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.5.1 CURRENCY UNIT

- 1.5.2 VOLUME UNIT

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN WATER-SOLUBLE FERTILIZERS MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN WATER-SOLUBLE FERTILIZERS MARKET

- 3.2 WATER-SOLUBLE FERTILIZERS MARKET, BY CROP TYPE

- 3.3 WATER-SOLUBLE FERTILIZERS MARKET, BY MODE OF APPLICATION

- 3.4 WATER-SOLUBLE FERTILIZERS MARKET, BY FORM

- 3.5 WATER-SOLUBLE FERTILIZERS MARKET, BY OFFERING AND REGION

- 3.6 WATER-SOLUBLE FERTILIZERS MARKET, BY COUNTRY/REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing popularity of precision nutrient management and fertigation

- 4.2.1.2 Rising nutrient output and moderate utilization

- 4.2.1.3 Focus on higher nutrient efficiency and fertilizer price volatility

- 4.2.1.4 Shift toward specialty and value-added fertilizer products

- 4.2.1.5 Strong demand from high-value crops requiring rapid nutrient uptake

- 4.2.2 RESTRAINTS

- 4.2.2.1 Growth in organic fertilizers industry

- 4.2.2.2 Limited pricing flexibility due to concentrated potash and phosphate supply

- 4.2.2.3 Limited contribution toward GHG emission reduction targets

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Government initiatives to increase awareness of agricultural technologies in emerging markets

- 4.2.3.2 Rising adoption of customized fertigation and digital agronomy solutions

- 4.2.3.3 Growth in demand for water-soluble nutrients

- 4.2.4 CHALLENGES

- 4.2.4.1 Margin pressure from higher energy, logistics, and regulatory costs

- 4.2.4.2 Intensifying competition in standard water-soluble NPK products

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN WATER-SOLUBLE FERTILIZERS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 RISING NUTRIENT INTENSITY REFLECTS STRUCTURAL GROWTH DRIVERS FOR WSF MARKET

- 5.2.2 HIGH FERTILIZER INTENSITY MARKETS SIGNAL STRONG STRUCTURAL DEMAND FOR WSF ADOPTION

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 FERTILIZER MANUFACTURERS & FORMULATORS

- 5.3.3 SPECIALTY & SYSTEM-ORIENTED SOLUTION PROVIDERS

- 5.3.4 SERVICE PROVIDERS

- 5.3.5 END USERS

- 5.3.6 POST-SALES SERVICES

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.3 AVERAGE SELLING PRICE, BY TYPE

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO OF HS CODE 3105

- 5.6.2 IMPORT SCENARIO OF HS CODE 3105

- 5.7 KEY CONFERENCES AND EVENTS IN 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 YARA INTERNATIONAL ENHANCES FERTILIZER PRECISION WITH AGRIBLE AI ACQUISITION

- 5.10.2 ICL GROWING SOLUTIONS LEVERAGES AGREMATCH AI4AI TO INNOVATE WATER-SOLUBLE FERTILIZERS

- 5.10.3 MOSAIC LEVERAGES AGWORLD AI FOR PRECISION WATER-SOLUBLE FERTILIZER MANAGEMENT

- 5.11 IMPACT OF 2025 US TARIFF - WATER-SOLUBLE FERTILIZERS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 Morocco (North Africa)

- 5.11.4.2 Saudi Arabia & Jordan (Middle East)

- 5.11.4.3 Tunisia (North Africa)

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI-DRIVEN PRECISION FERTIGATION & NUTRIENT PRESCRIPTION SYSTEMS

- 6.1.2 NANO-ENABLED & CONTROLLED-RELEASE WATER-SOLUBLE FERTILIZERS

- 6.1.3 DIGITAL TWIN & PREDICTIVE CROP MODELING PLATFORMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SMART IRRIGATION & IOT-ENABLED DRIP SYSTEMS

- 6.2.2 SOIL & PLANT DIAGNOSTIC TECHNOLOGIES (SENSORS AND SPECTRAL IMAGING)

- 6.2.3 PROTECTED CULTIVATION & HYDROPONIC SYSTEMS

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2031) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2032-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 NANO-ENABLED AND CHELATED HIGH-EFFICIENCY WSF FORMULATIONS

- 6.5.2 AI-INTEGRATED PRECISION FERTIGATION AND SMART NUTRIENT DOSING

- 6.5.3 CROP-SPECIFIC AND CLIMATE-RESILIENT SPECIALTY WSF BLENDS

- 6.5.4 BIO-ENHANCED AND HYBRID NUTRIENT FORMULATIONS

- 6.5.5 CONTROLLED-RELEASE AND STABILIZED SOLUBLE NUTRIENT SYSTEMS

- 6.6 IMPACT OF GENERATIVE AI ON WATER-SOLUBLE FERTILIZERS MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 USE OF GENERATIVE AI ON WATER-SOLUBLE FERTILIZERS MARKET

- 6.6.3 TOP USE CASES AND MARKET POTENTIAL

- 6.6.4 BEST PRACTICES IN WATER-SOLUBLE FERTILIZERS INDUSTRY

- 6.7 CASE STUDIES OF AI IMPLEMENTATION IN WATER-SOLUBLE FERTILIZERS MARKET

- 6.8 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.9 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN WATER-SOLUBLE FERTILIZERS MARKET

- 6.10 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2 INDUSTRY STANDARDS

- 7.2.1 SUSTAINABILITY INITIATIVES

- 7.2.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.2.3 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 7.2.4 REGION-WISE LABELING STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.2.3 ADOPTION BARRIER AND INTERNAL CHALLENGES

- 8.2.4 UNMET NEEDS OF VARIOUS END-USERS/END-USE INDUSTRIES

- 8.2.4.1 Horticulture and high-value crops

- 8.2.4.2 Field crops and cereals

- 8.2.4.3 Specialty crops and plantation agriculture

- 8.2.5 MARKET PROFITABILITY

9 WATER-SOLUBLE FERTILIZERS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 NITROGENOUS

- 9.2.1 VARYING QUANTITIES AND TYPES OF NITROGENOUS FERTILIZERS REQUIRED AT DIFFERENT CROP GROWTH STAGES

- 9.2.2 TYPES OF NITROGENOUS FERTILIZERS

- 9.2.2.1 Calcium nitrate

- 9.2.2.2 Potassium nitrate

- 9.2.2.3 Urea

- 9.2.2.4 Urea-ammonia nitrate & others

- 9.3 PHOSPHATIC

- 9.3.1 SUPPORTS ROOT DEVELOPMENT, ENERGY TRANSFER, AND EARLY CROP ESTABLISHMENT

- 9.3.2 TYPES OF PHOSPHATIC FERTILIZERS

- 9.3.2.1 Monoammonium phosphate (MAP)

- 9.3.2.2 Monopotassium phosphate (MKP)

- 9.3.2.3 Urea phosphate and polyphosphate

- 9.3.2.4 Diammonium phosphate (DAP)

- 9.3.2.5 Other phosphatic fertilizers (phosphoric acid-based blends)

- 9.4 POTASSIC

- 9.4.1 HIGH REQUIREMENT OF POTASSIUM FOR PROPER NUTRIENT UPTAKE

- 9.4.2 TYPES OF POTASSIC FERTILIZERS

- 9.4.2.1 Potassium sulfate

- 9.4.2.2 Others (potassium thiosulfate and other potash-based soluble blends)

- 9.5 MICRONUTRIENTS

- 9.5.1 MICRONUTRIENT DEFICIENCY LEADS TO STUNTED PLANT GROWTH

- 9.5.2 TYPES OF MICRONUTRIENTS

- 9.5.2.1 Iron (Fe)

- 9.5.2.2 Zinc (Zn)

- 9.5.2.3 Manganese(Mn)

- 9.5.2.4 Boron (B)

- 9.5.2.5 Copper (Cu)

- 9.5.2.6 Molybdenum (Mo)

- 9.5.2.7 Other/Multi-micronutrient blends

10 WATER-SOLUBLE FERTILIZERS MARKET, BY CROP TYPE

- 10.1 INTRODUCTION

- 10.2 FIELD CROPS

- 10.2.1 HIGHEST DEMAND AMONG CROP TYPES ACROSS REGIONS

- 10.3 HORTICULTURAL CROPS

- 10.3.1 RISING HEALTH AWARENESS, NUTRITIONAL TRENDS, AND AESTHETIC APPEAL TO DRIVE DEMAND

- 10.3.2 ORCHARD CROPS

- 10.3.3 VEGETABLE & FLOWER CROPS

- 10.4 TURFS & ORNAMENTALS

- 10.4.1 VARYING NUTRIENT REQUIREMENTS DEMAND OPTIMUM WATER-SOLUBLE FERTILIZERS

- 10.5 OTHER CROP TYPES

11 WATER-SOLUBLE FERTILIZERS MARKET, BY MODE OF APPLICATION

- 11.1 INTRODUCTION

- 11.2 FOLIAR

- 11.2.1 EFFICIENT NUTRIENT ABSORPTION ALONG WITH HIGH PEST RESISTANCE

- 11.3 FERTIGATION

- 11.3.1 COST-EFFECTIVE AND EASY APPLICATION

12 WATER-SOLUBLE FERTILIZERS MARKET, BY FORM

- 12.1 INTRODUCTION

- 12.2 DRY

- 12.2.1 EASE OF USE AND LONGER SHELF LIFE

- 12.2.2 POWDER

- 12.2.2.1 Fine powders

- 12.2.2.2 low-dust/agglomerated powder

- 12.2.3 GRANULAR/CRYSTALLINE

- 12.2.3.1 Prillled granules

- 12.2.3.2 High-purity crystalline granules

- 12.2.4 SPECIALTY DRY FORMULATIONS

- 12.2.4.1 Chelated Micronutrient Powders

- 12.2.4.2 Multi-Nutrient and Customized Dry Blends

- 12.3 LIQUID

- 12.3.1 UNIFORM NUTRIENT AVAILABILITY AND CONVENIENCE IN APPLICATION

- 12.3.2 LIQUID CONCENTRATES

- 12.3.3 SUSPENSION CONCENTRATES

- 12.3.4 LIQUID CHELATED MICRONUTRIENTS AND SPECIALTY FORMULATIONS

13 WATER-SOLUBLE FERTILIZERS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Advancements in precision farming techniques to drive market

- 13.2.2 CANADA

- 13.2.2.1 Rising demand for food and government support to drive market

- 13.2.3 MEXICO

- 13.2.3.1 Demand for sustainable agriculture practices to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Increasing demand from agricultural industry and potential for crop-specific fertilizers to drive market

- 13.3.2 UK

- 13.3.2.1 Growing consumer awareness and government support to drive market

- 13.3.3 FRANCE

- 13.3.3.1 Adoption of sustainable agriculture to drive market

- 13.3.4 ITALY

- 13.3.4.1 Demand for high-quality crops and government initiatives to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Increasing farmer awareness and government initiatives to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 High agricultural potential with vast arable land to drive market

- 13.4.2 INDIA

- 13.4.2.1 Government initiatives toward drip irrigation and fertilizer subsidies to drive market

- 13.4.3 JAPAN

- 13.4.3.1 Need to improve production yield and quality to drive market

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Demand for high-quality crops to drive market

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Growth in precision agriculture and specialty fertilizer demand to drive market

- 13.5.2 ARGENTINA

- 13.5.2.1 Expansion of precision nutrient management and public-private initiatives to drive market

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD (ROW)

- 13.6.1 MIDDLE EAST

- 13.6.1.1 Adoption of National Fertilizer Plan to drive market

- 13.6.2 AFRICA

- 13.6.2.1 Growing acceptance of water-soluble fertilizers to drive market

- 13.6.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 14.3 REVENUE ANALYSIS, 2020-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 YARA INTERNATIONAL

- 14.4.2 COROMANDEL INTERNATIONAL LIMITED

- 14.4.3 NUTRIEN LTD.

- 14.4.4 GUJARAT STATE FERTILIZERS & CHEMICALS LIMITED

- 14.4.5 K+S AKTIENGESELLSCHAFT

- 14.5 PRODUCT COMPARISON

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Type footprint

- 14.6.5.3 Mode of application footprint

- 14.6.5.4 Form footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPETITIVE SCENARIO

- 14.8.1 PRODUCT LAUNCHES

- 14.8.2 DEALS

- 14.8.3 EXPANSIONS

- 14.8.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 NUTRIEN

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices made

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 YARA INTERNATIONAL

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 MnM view

- 15.1.2.3.1 Right to win

- 15.1.2.3.2 Strategic choices made

- 15.1.2.3.3 Weaknesses and competitive threats

- 15.1.3 THE MOSAIC COMPANY

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices made

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 ICL

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices made

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 PHOSAGRO

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices made

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 INCITEC PIVOT LTD.

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 MnM view

- 15.1.7 SOCIEDAD QUIMICA Y MINERA DE CHILE (SQM)

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 MnM view

- 15.1.8 K+S AKTIENGESELLSCHAFT

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.4 MnM view

- 15.1.9 GRUPA AZOTY

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Expansions

- 15.1.9.3.2 Other developments

- 15.1.9.4 MnM view

- 15.1.10 COROMANDEL INTERNATIONAL LIMITED

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Expansions

- 15.1.10.4 MnM view

- 15.1.1 NUTRIEN

- 15.2 OTHER PLAYERS

- 15.2.1 GUJARAT STATE FERTILIZERS & CHEMICALS (GSFC)

- 15.2.1.1 Business overview

- 15.2.1.2 Products offered

- 15.2.1.3 MnM view

- 15.2.2 DFPCL

- 15.2.2.1 Business overview

- 15.2.2.2 Products offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Deals

- 15.2.2.4 MnM view

- 15.2.3 KATYAYANI ORGANICS

- 15.2.3.1 Business overview

- 15.2.3.2 Products offered

- 15.2.3.3 MnM view

- 15.2.4 ZUARI FARMHUB

- 15.2.4.1 Business overview

- 15.2.4.2 Products offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches

- 15.2.4.3.2 Deals

- 15.2.4.4 MnM view

- 15.2.5 ARIES AGRO LIMITED

- 15.2.5.1 Business overview

- 15.2.5.2 Products offered

- 15.2.5.3 MnM view

- 15.2.6 HEBEI MONBAND WATER SOLUBLE FERTILIZER CO., LTD.

- 15.2.6.1 Business overview

- 15.2.6.2 Products offered

- 15.2.6.3 MnM view

- 15.2.7 HAIFA GROUP

- 15.2.7.1 Business overview

- 15.2.7.2 Products offered

- 15.2.7.3 Recent developments

- 15.2.7.3.1 Product launches

- 15.2.7.3.2 Deals

- 15.2.7.3.3 Expansions

- 15.2.7.4 MnM view

- 15.2.8 PRAYON

- 15.2.8.1 Business overview

- 15.2.8.2 Products offered

- 15.2.8.3 Recent developments

- 15.2.8.3.1 Deals

- 15.2.8.4 MnM view

- 15.2.9 SPIC

- 15.2.9.1 Business overview

- 15.2.9.2 Products offered

- 15.2.9.3 MnM view

- 15.2.10 EUROCHEM GROUP

- 15.2.10.1 Business overview

- 15.2.10.2 Products offered

- 15.2.10.3 Recent developments

- 15.2.10.4 MnM view

- 15.2.11 VAKI-CHIM

- 15.2.12 KING QUENSON

- 15.2.13 AGAFERT SRL

- 15.2.14 SHANDONG HUAYI HANZHONG BIOTECHNOLOGY CO., LTD.

- 15.2.15 GREEN VISION TECHNICAL SERVICES

- 15.2.1 GUJARAT STATE FERTILIZERS & CHEMICALS (GSFC)

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of major secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.2.3 Breakdown of primaries

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.2.2.1 Approach to estimate market size using top-down analysis

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 ADJACENT AND RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 LIMITATIONS

- 17.3 FERTILIZERS MARKET

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.4 SPECIALTY FERTILIZERS MARKET

- 17.4.1 MARKET DEFINITION

- 17.4.2 MARKET OVERVIEW

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS