|

시장보고서

상품코드

1993566

자동차 통신 프로토콜 시장(-2033년) : 차량 유형(이코노미, 미드사이즈, 럭셔리), 프로토콜(LIN, CAN, FlexRay, 이더넷, 기타), 용도(파워트레인, 안전&ADAS, 기타), 추진 방식(ICE, EV), 지역별Automotive Communication Protocol Market by Vehicle Class (Economy, Mid-size, Luxury), Protocol (LIN, CAN, FlexRay, Ethernet, Others), Application (Powertrain, Safety & ADAS, Others), Propulsion (ICE, EV), and Region - Global Forecast to 2033 |

||||||

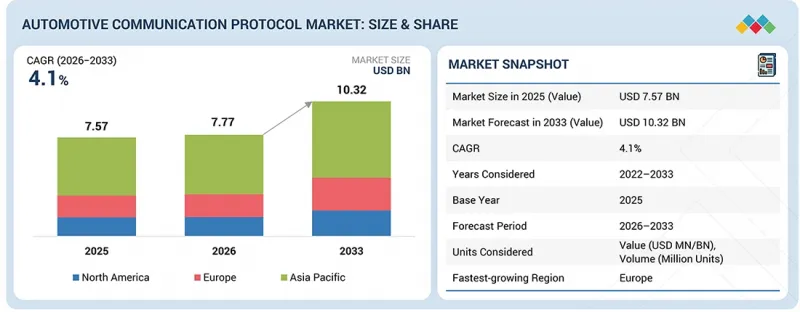

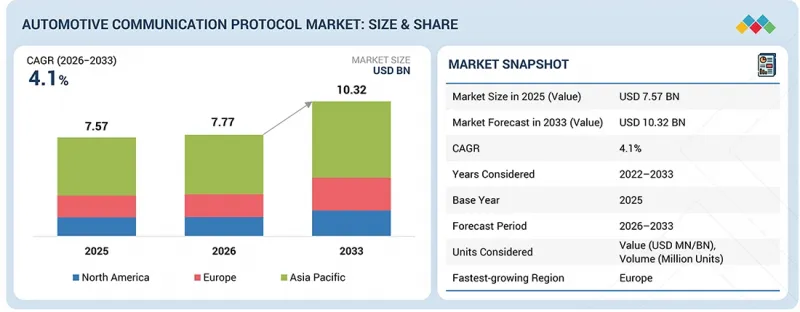

자동차 통신 프로토콜 시장 규모는 2026년 77억 7,000만 달러에서 2033년에는 103억 2,000만 달러에 이를 것으로 예측되며, CAGR은 4.1%를 보일ㄴ 전망입니다.

이러한 성장은 주로 차체, 섀시, 인포테인먼트, 파워트레인 등 다양한 영역에서 여러 네트워크 노드, 센서, 컨트롤러가 동시에 상호 작용하여 승용차 내 통신 밀도가 높아짐에 따라 차량 내 데이터 교환 요구사항이 증가함에 따라 주도되고 있습니다. 에 의해 형성되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | Million Units 및 금액(달러) |

| 부문 | 프로토콜, 용도, 차량 유형, 추진 방식, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미 |

OEM 업체들은 메시지 트래픽 증가에 대응하고, 더 빠른 진단을 가능하게 하며, 하드웨어 재설계 없이 향후 기능 확장을 위해 확장성이 높은 차량용 네트워크에 투자하고 있습니다. 또한, 플랫폼의 라이프사이클이 길어지고 있는 것도 시장 성장 요인으로 작용하고 있으며, 여러 모델 세대에 걸쳐 프로토콜이 안정적으로 도입되면서 통신용 IC 및 소프트웨어 스택에 대한 지속적인 수요가 유지되고 있습니다.

예측 기간 동안 이더넷이 가장 빠르게 성장하는 프로토콜이 될 것으로 예측됩니다.

차량용 이더넷은 100Mbps에서 멀티 기가비트 속도까지 높은 대역폭의 데이터 전송을 가능하게 합니다. 이는 고해상도 카메라, 레이더 시스템, 차량용 인포테인먼트, 중앙 게이트웨이, 도메인 컨트롤러, 존 아키텍처, ADAS, 현대 ICE 차량의 고도의 자동화에서 점점 더 많이 요구되고 있습니다. 카메라 및 레이더 기반 안전 시스템의 보급에 따라 기존 CAN의 처리 능력을 넘어서는 방대한 양의 데이터가 발생하고 있으며, 백본 네트워크로서 이더넷의 채택이 가속화되고 있습니다. Volkswagen, BMW, Mercedes-Benz, General Motors, Toyota와 같은 OEM 업체들은 이더넷이 핵심 통신 기술로 기능하고 소프트웨어 정의 차량(SDV) 전략을 지원하는 확장 가능한 네트워크 토폴로지를 지원하는 도메인 및 존 기반 E/E 아키텍처로 전환하고 있습니다. SDV) 전략에 따라 확장 가능한 네트워크 토폴로지를 지원하고 있습니다. 또한, TSN(Time Scalable Network)과 같은 결정론적 기능 강화로 지연에 대한 우려가 해소되어 이더넷은 안전 관련 용도에 적합합니다. 차량 1대당 전자 컨텐츠가 지속적으로 증가하는 가운데, OEM 업체들은 분산형 CAN 네트워크에서 이더넷을 중심으로 한 게이트웨이 아키텍처로 전환하고 있으며, ADAS 데이터 융합을 위한 기가비트 이더넷의 도입 확대도 포함됩니다. 마찬가지로 자동차 통신 프로토콜 공급업체들도 이더넷 PHY, 스위치, TSN 기능, 사이버 보안 대응 솔루션 등을 도입하여 제품 포트폴리오를 다양화하고 있습니다.

"북미 시장이 예측 기간 동안 상당한 성장률을 보일 것으로 예상"

미국은 북미 최대의 승용차 시장으로 첨단 안전, 파워트레인, 인포테인먼트의 네트워크 노드가 널리 채택되어 CAN, CAN FD, LIN, 차량용 이더넷에 대한 수요가 증가하고 있습니다. 미국 및 캐나다 전역의 차량에서 ADAS 및 안전 기능의 보급이 이더넷 채택 확대를 주도하고 있지만, 하위 시스템 수준에서는 여전히 CAN과 LIN이 주류를 이루고 있습니다. 양국의 OEM들은 중앙집중형 및 도메인 기반 E/E 아키텍처로의 전환을 가속화하고 있으며, 이로 인해 게이트웨이의 복잡성과 프로토콜 밀도가 증가하고 있습니다. 반도체 공급업체와 1등급 자동차 전장업체가 다수 존재한다는 점도 첨단 통신 표준의 빠른 도입을 더욱 촉진하고 있습니다. 북미에는 TEXAS INSTRUMENTS INCORPORATED, Analog Devices, Inc. 및 Microchip Technology와 같은 주요 자동차 통신 프로토콜 제공업체가 있습니다. 예를 들어, 2026년 1월 TEXAS INSTRUMENTS는 CES 2026에서 자동차용 10BASE-T1S PHY 제품 포트폴리오를 선보였습니다. 이를 통해 센서 네트워크, 구역형 또는 엣지 노드 아키텍처를 위한 멀티 드롭 및 포인트-투-포인트 10Mb/s 싱글 페이 이더넷이 가능해집니다.

세계의 자동차 통신 프로토콜(Automotive Communication Protocol) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 OEM 분석 : 제조, 생산, E/E 아키텍처 전략

제7장 기술 진보, AI의 영향, 특허, 혁신

제8장 고객 현황과 구매 행동

제9장 규제 상황과 지속가능성 이니셔티브

제10장 OEM와 Tier 1 공급망 전략 전환

제11장 자동차 통신 프로토콜 시장 : 프로토콜 유형별

제12장 자동차 통신 프로토콜 시장 : 차량 유형별

제13장 자동차 통신 프로토콜 시장 : 용도별

제14장 자동차 통신 프로토콜 시장 : 추진 방식별

제15장 자동차 통신 프로토콜 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

LSH 26.04.17The automotive communication protocol market is expected to reach USD 10.32 billion by 2033, from USD 7.77 billion in 2026, with a CAGR of 4.1%. This growth is mainly driven by increasing in-vehicle data exchange requirements, which are shaped by greater communication density within passenger cars, as multiple network nodes, sensors, and controllers interact simultaneously across body, chassis, infotainment, and powertrain domains.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | Volume (Million Units) and Value (USD MN/BN) |

| Segments | Protocol, Application, Vehicle Class, Propulsion, and Region |

| Regions covered | Asia Pacific, Europe, and North America |

OEMs are investing in scalable in-vehicle networks to handle higher message traffic, enable faster diagnostics, and allow for future feature expansion without repeated hardware redesigns. The market is also driven by longer platform lifecycles, where stable protocol deployment across multiple model generations maintains recurring demand for communication ICs and software stacks.

Ethernet is expected to be the fastest-growing protocol during the forecast period.

Automotive Ethernet enables high-bandwidth data transmission from 100 Mbps to multi-gigabit speeds, which is increasingly required for high-resolution cameras, radar systems, in-vehicle infotainment, central gateways, domain controllers, zonal architectures, ADAS, and higher levels of automation in modern ICE vehicles. The growing use of camera- and radar-based safety systems generates large data volumes that exceed the capabilities of Classical CAN, accelerating the adoption of Ethernet as a backbone network. OEMs such as Volkswagen, BMW, Mercedes-Benz, General Motors, and Toyota are moving toward domain- and zonal-based E/E architectures, where Ethernet functions as the core communication technology and supports scalable network topologies aligned with software-defined vehicle strategies. Deterministic enhancements such as TSN address latency concerns, making Ethernet suitable for safety-related applications. As electronic content per ICE vehicle continues to increase, OEMs are shifting from distributed CAN networks to Ethernet-centric gateway architectures, including wider deployment of gigabit Ethernet for ADAS data fusion. Similarly, automotive communication protocol suppliers are diversifying their portfolios to include Ethernet PHYs, switches, TSN capabilities, and cybersecurity-ready solutions.

Mid-size passenger cars are expected to be the largest vehicle class during the forecast period.

Mid-size passenger cars account for the highest global production and sales volumes, particularly in North America, Europe, and parts of Asia, which drives demand for automotive communication protocols. This vehicle segment balances cost and feature content by integrating ADAS, infotainment, and connectivity solutions, resulting in higher network node counts per vehicle. Compared to entry-level vehicles, mid-size models adopt CAN FD and Ethernet-enabled gateways more rapidly to support enhanced safety, comfort, and data throughput requirements. LIN and CAN are universally used in mid-size vehicles for body electronics such as door modules, lighting, climate control, seat control, and core powertrain and chassis functions. Ethernet penetration is significant due to the need to handle high data volumes from cameras, radar, infotainment, and centralized gateways, while FlexRay remains present in legacy architectures because of its deterministic and fault-tolerant performance for safety-critical applications. OEMs often prioritize mid-size models for early technology deployment, making this segment the first ICE category to adopt upgraded network architectures.

"North America is expected to grow at a significant rate during the forecast period."

The US represents the largest passenger car market in North America, with extensive use of advanced safety, powertrain, and infotainment network nodes, which boosts demand for CAN, CAN FD, LIN, and automotive Ethernet. Widespread deployment of ADAS and safety features in vehicles across the US and Canada is driving increased Ethernet adoption, while CAN and LIN continue to dominate at the subsystem level. OEMs in both countries are accelerating the transition toward centralized and domain-based E/E architectures, leading to higher gateway complexity and greater protocol density. The significant presence of semiconductor suppliers and Tier-1 automotive electronics manufacturers further supports the rapid incorporation of advanced communication standards. North America is home to major automotive communication protocol providers such as TEXAS INSTRUMENTS INCORPORATED, Analog Devices, Inc., and Microchip Technology. For instance, in January 2026, TEXAS INSTRUMENTS showcased its automotive 10BASE-T1S PHY product portfolio at CES 2026, enabling multidrop and point-to-point 10 Mb/s single-pair Ethernet for sensor networks and zonal or edge-node architectures.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 25%, Tier 1 - 60%, and Tier 2 - 15%

- By Designation: CXOs - 29%, Managers - 58%, and Executives - 13%

- By Region: North America - 29%, Europe - 23%, and Asia Pacific - 48%

The automotive communication protocol market is dominated by major players, such as NXP Semiconductors (Netherlands), Robert Bosch GmbH (Germany), Infineon Technologies AG (Germany), STMicroelectronics (Switzerland), and TEXAS INSTRUMENTS INCORPORATED (US).

Research Coverage:

This research report categorizes the automotive communication protocol market by vehicle class (economy, mid-size, luxury), protocol (LIN, CAN, FlexRay, Ethernet, others), application (powertrain, safety & ADAS, others), propulsion type (ICE, EV), and region. It covers the competitive landscape and profiles of the major players of the automotive communication protocol market. The study also includes an in-depth competitive analysis of the key market players, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall automotive communication protocol market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will also help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (bandwidth escalation from ADAS sensor proliferation, growth of high-resolution displays and digital cockpit architectures, electrification and high-voltage powertrain communication complexity), restraints (legacy network entrenchment and backward compatibility constraints, functional safety certification burden), opportunities (multi-gigabit sensor connectivity for ADAS and autonomous architectures, in-vehicle high-bandwidth infotainment and display networking), and challenges (multi-protocol coexistence and network integration complexity, growing cybersecurity threats in modern vehicle networks)

- Product Development/Innovation: Detailed insights into upcoming technologies and R&D activities in the automotive communication protocol market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the automotive communication protocol market across varied regions)

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the automotive communication protocol market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players such as NXP Semiconductors (Netherlands), Robert Bosch GmbH (Germany), Infineon Technologies AG (Germany), STMicroelectronics (Switzerland), and TEXAS INSTRUMENTS INCORPORATED (US) in the automotive communication protocol market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING AUTOMOTIVE COMMUNICATION PROTOCOL MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE COMMUNICATION PROTOCOL MARKET

- 3.2 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY REGION

- 3.3 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY PROTOCOL TYPE

- 3.4 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY APPLICATION

- 3.5 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY VEHICLE CLASS

- 3.6 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY PROPULSION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased bandwidth requirements due to ADAS sensor proliferation

- 4.2.1.2 Expansion of high-resolution displays and digital cockpit architectures

- 4.2.1.3 Need for advanced communication in high-voltage electrified powertrains

- 4.2.2 RESTRAINTS

- 4.2.2.1 Legacy network entrenchment and backward compatibility constraints

- 4.2.2.2 Functional safety certification burden

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Multi-gigabit sensor connectivity for ADAS and autonomous architectures

- 4.2.3.2 Rise of high-bandwidth in-vehicle infotainment networking

- 4.2.4 CHALLENGES

- 4.2.4.1 Multi-protocol coexistence and network integration complexity

- 4.2.4.2 Heightened cybersecurity threats in modern vehicle networks

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN AUTOMOTIVE COMMUNICATION PROTOCOL MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL PASSENGER CAR MARKET

- 5.1.3 TRENDS IN GLOBAL CONNECTED VEHICLE INDUSTRY

- 5.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3 PRICING ANALYSIS

- 5.3.1 AVERAGE SELLING PRICE TREND, BY PROTOCOL, 2024-2026

- 5.3.2 AVERAGE SELLING PRICE TREND OF PROTOCOL, BY REGION, 2024-2026

- 5.3.2.1 Average selling price trend of LIN, by region, 2024-2026

- 5.3.2.2 Average selling price trend of CAN, by region, 2024-2026

- 5.3.2.3 Average selling price trend of FlexRay, by region, 2024-2026

- 5.3.2.4 Average selling price trend of Ethernet, by region, 2024-2026

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 ACCELERATING AUTOMOTIVE ETHERNET ADOPTION THROUGH END-TO-END VALIDATION STRATEGY

- 5.6.2 ENHANCING HIGH-SPEED AUTOMOTIVE ETHERNET VALIDATION FOR ADVANCED VEHICLE SYSTEMS

- 5.6.3 MODERNIZING SUPER CRUISE THROUGH AUTOMOTIVE ETHERNET INTEGRATION

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT SCENARIO (HS CODE 8542)

- 5.8.2 EXPORT SCENARIO (HS CODE 8542)

- 5.9 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.10 UPCOMING AUTOMOTIVE ETHERNET STANDARDS AND THEIR USE CASES

- 5.10.1 TIMELINE OF IEEE AND OPEN ALLIANCE DEVELOPMENTS

- 5.10.2 TECHNICAL SPECIFICATIONS OF 10G+ AUTOMOTIVE ETHERNET

- 5.10.3 VEHICLE USE CASES

- 5.10.3.1 ADAS/Autonomous driving

- 5.10.3.2 Infotainment/Digital cockpit

- 5.10.3.3 Zonal/Electrical architecture

- 5.10.3.4 V2X and OTA

- 5.10.4 COPPER VS. FIBER FOR HIGH-SPEED LINKS

- 5.10.4.1 Copper

- 5.10.4.2 Fiber optics

6 OEM ANALYSIS - MANUFACTURING, PRODUCTION, AND E/E ARCHITECTURE STRATEGY

- 6.1 OEM MANUFACTURING FOOTPRINT AND PRODUCTION CAPACITY

- 6.2 E/E ARCHITECTURE EVOLUTION STRATEGY

- 6.2.1 NEW GENERATION OEMS

- 6.2.1.1 BYD

- 6.2.1.2 XPENG

- 6.2.1.3 NIO

- 6.2.1.4 Li Auto

- 6.2.1.5 Tesla

- 6.2.1.6 Rivian

- 6.2.1.7 Lucid Motors

- 6.2.1.8 Polestar

- 6.2.1.9 Leapmotor

- 6.2.1.10 Faraday Future

- 6.2.2 LEGACY OEMS

- 6.2.2.1 Toyota Motor Corporation

- 6.2.2.2 Volkswagen Group

- 6.2.2.3 Hyundai Motor Company

- 6.2.2.4 Honda Motor Co., Ltd.

- 6.2.2.5 Mahindra & Mahindra

- 6.2.2.6 Tata Motors

- 6.2.2.7 Audi AG

- 6.2.2.8 Mercedes-Benz AG

- 6.2.2.9 BMW Group

- 6.2.2.10 General Motors

- 6.2.3 OEM COLLABORATIONS AND STANDARDIZATION LANDSCAPE

- 6.2.1 NEW GENERATION OEMS

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 7.1 KEY TECHNOLOGIES

- 7.1.1 AUTOMOTIVE ETHERNET

- 7.1.2 AUTOMOTIVE SERDES/CAMERA CONNECTIVITY

- 7.1.3 SOFTWARE-DEFINED NETWORKING

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 CAN FD AND CAN XL

- 7.2.2 IN-VEHICLE CYBERSECURITY

- 7.3 TECHNOLOGY/PRODUCT ROADMAP

- 7.3.1 SHORT-TERM (2026-2027): FOUNDATION AND EARLY COMMERCIALIZATION

- 7.3.2 MID-TERM (2028-2030): EXPANSION AND STANDARDIZATION

- 7.3.3 LONG-TERM (2031-2035+): MASS COMMERCIALIZATION AND DISRUPTION

- 7.4 PATENT ANALYSIS

- 7.5 IMPACT OF AI/GEN AI

- 7.5.1 TOP USE CASES AND MARKET POTENTIAL

- 7.5.1.1 Security and anomaly detection

- 7.5.1.2 Network design and optimization

- 7.5.1.3 Testing and virtualization

- 7.5.1.4 Data compression and semantic streaming

- 7.5.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS

- 7.5.2.1 Model-based designs and standards compliance

- 7.5.2.2 Integrated development environments

- 7.5.2.3 Cybersecurity focus

- 7.5.2.4 Simulation and continuous testing

- 7.5.2.5 Zonal architectures and gateway designs

- 7.5.2.6 Data-driven calibration

- 7.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION

- 7.5.3.1 Transforming vehicle cybersecurity with edge-based intrusion detection

- 7.5.3.2 Accelerating automotive software validation with Gen AI

- 7.5.3.3 Enhancing in-vehicle voice interaction with GPT-powered assistants

- 7.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT OF MARKET PLAYERS

- 7.5.4.1 Semiconductor

- 7.5.4.2 Telecom and cloud

- 7.5.4.3 IoT and V2X

- 7.5.4.4 Standards bodies and consortia

- 7.5.4.5 Software platforms

- 7.5.5 CLIENTS' READINESS TO ADOPT AI

- 7.5.1 TOP USE CASES AND MARKET POTENTIAL

- 7.6 INSIGHTS ON TECHNOLOGY ANALYSIS AND WHO WORKS WITH WHOM

- 7.6.1 BROADCOM

- 7.6.2 TEXAS INSTRUMENTS INCORPORATED

- 7.6.3 NXP SEMICONDUCTORS

- 7.6.4 STMICROELECTRONICS

- 7.6.5 INFINION TECHNOLOGIES AG

- 7.6.6 RENESAS ELECTRONICS CORPORATION

- 7.6.7 XILINX

- 7.6.8 QUALCOMM TECHNOLOGIES, INC.

- 7.6.9 NVIDIA CORPORATION

- 7.6.10 ANALOG DEVICES INC.

- 7.6.11 MICROCHIP TECHNOLOGY

- 7.6.12 MARVELL TECHNOLOGY

- 7.6.13 ROHM CO., LTD.

- 7.6.14 MELEXIS

- 7.6.15 VALENS SEMICONDUCTOR

- 7.6.16 SONY GROUP CORPORATION

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

9 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 9.1 REGIONAL REGULATIONS AND COMPLIANCE

- 9.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 9.1.2 INDUSTRY STANDARDS

- 9.1.2.1 OpenGMSL (Open Gigabit Multimedia Serial Link)

- 9.1.2.2 FPD-Link (Flat Panel Display Link)

- 9.1.2.3 MIPI A-PHY (Automotive Physical Layer)

- 9.1.2.4 GVIF (Gigabit Video Interface)

- 9.1.2.5 HSMT (High-Speed Media Transmission)

- 9.1.2.6 A2B (Audio to Bus)

- 9.1.2.7 ASA-ML (Automotive SerDes Alliance - Motion Link)

- 9.1.2.8 CAN (Controller Area Network)

- 9.1.2.9 LIN (Local Interconnect Network)

- 9.1.2.10 FlexRay

- 9.1.2.11 Automotive Ethernet

- 9.1.2.12 APIX (Automotive Pixel Link)

- 9.1.2.13 MOST (Media Oriented Systems Transport)

- 9.2 SUSTAINABILITY INITIATIVES

- 9.2.1 CARBON IMPACT AND ECO-APPLICATIONS

- 9.2.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 9.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

10 OEM AND TIER-1 SUPPLY CHAIN STRATEGY SHIFT

- 10.1 OVERVIEW OF TARIFF AND TRADE CONFLICTS

- 10.1.1 US-CHINA

- 10.1.2 US-EU

- 10.1.3 EU-CHINA

- 10.1.4 INDIA-CHINA

- 10.2 IMPACT ON GLOBAL AUTOMOTIVE PRODUCTION AND LOCALIZATION

- 10.3 OEM SUPPLY CHAIN, PRODUCTION, AND LOCALIZATION STRATEGY

- 10.4 TIER-1 SUPPLIER SUPPLY CHAIN ADAPTATION AND LOCALIZATION STRATEGY

- 10.5 IMPACT OF EUROPE-INDIA TRADE DEALS

- 10.5.1 EU TARIFFS

- 10.5.2 IMPORTS TO INDIA

- 10.5.3 EXPORTS FROM INDIA

11 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY PROTOCOL TYPE

- 11.1 INTRODUCTION

- 11.2 LIN

- 11.2.1 DEMAND FOR LOW-COST BODY CONTROL APPLICATIONS IN VEHICLES TO DRIVE MARKET

- 11.3 CAN

- 11.3.1 RAPID INTEGRATION OF REAL-TIME POWERTRAIN, CHASSIS, AND SAFETY CONTROL SYSTEMS INTO VEHICLES TO DRIVE MARKET

- 11.4 FLEXRAY

- 11.4.1 ADVANCED POWERTRAIN APPLICATIONS IN LUXURY VEHICLES TO DRIVE MARKET

- 11.5 ETHERNET

- 11.5.1 SURGE IN DEMAND FOR HIGH-BANDWIDTH ADAS, INFOTAINMENT, AND ZONAL VEHICLE ARCHITECTURES TO DRIVE MARKET

- 11.6 OEPNGMSL

- 11.7 FPD LINK

- 11.8 MIPI A-PHY

- 11.9 GVIF

- 11.10 HSMT

- 11.11 A2B

- 11.12 ASA-ML

- 11.13 APIX

- 11.14 MOST

- 11.15 PRIMARY INSIGHTS

12 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY VEHICLE CLASS

- 12.1 INTRODUCTION

- 12.2 ECONOMY

- 12.2.1 INCORPORATION OF MANDATORY SAFETY SYSTEMS AND BASIC INFOTAINMENT TO DRIVE MARKET

- 12.3 MID-SIZE

- 12.3.1 INTRODUCTION OF NEW NETWORKING TECHNOLOGIES BY OEMS TO DRIVE MARKET

- 12.4 LUXURY

- 12.4.1 ADVANCED INFOTAINMENT SYSTEMS, LARGE DIGITAL COCKPITS, AND IMMERSIVE DISPLAYS REQUIREMENTS TO DRIVE MARKET

- 12.5 PRIMARY INSIGHTS

13 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 POWERTRAIN

- 13.2.1 INCREASING CONTROL COMPLEXITY AND REGULATORY PRESSURE TO DRIVE MARKET

- 13.3 BODY CONTROL & COMFORT

- 13.3.1 RISING FEATURE PENETRATION IN ECONOMY AND MID-SIZE VEHICLES TO DRIVE MARKET

- 13.4 INFOTAINMENT & COMMUNICATION

- 13.4.1 EXPANDING DIGITAL COCKPIT SYSTEMS AND CONNECTED VEHICLE SERVICES TO DRIVE MARKET

- 13.5 SAFETY & ADAS

- 13.5.1 RISING INTEGRATION OF LEVEL 2 AND LEVEL 2+ ADAS FEATURES IN MID-SIZE VEHICLES TO DRIVE MARKET

- 13.6 TELEMATICS

- 13.6.1 REGULATORY REQUIREMENTS FOR EMERGENCY CALL SYSTEMS TO DRIVE MARKET

- 13.7 CENTRAL COMPUTING UNITS

- 13.8 AUDIO AMPLIFIERS

- 13.9 ZONAL CONTROLLERS

- 13.10 DISPLAYS

- 13.11 PRIMARY INSIGHTS

14 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY PROPULSION

- 14.1 INTRODUCTION

- 14.2 ICE

- 14.2.1 HEIGHTENED DEMAND FOR ADVANCED POWERTRAIN SOLUTIONS TO DRIVE MARKET

- 14.3 ELECTRIC

- 14.3.1 SHIFT FROM DISTRIBUTED ECUS TO CENTRALIZED AND ZONAL ARCHITECTURES TO DRIVE MARKET

- 14.4 PRIMARY INSIGHTS

15 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 ASIA PACIFIC

- 15.2.1 CHINA

- 15.2.1.1 Level 2 ADAS and advanced emission control system mandates to drive market

- 15.2.2 INDIA

- 15.2.2.1 Mandatory safety requirements like dual airbags and electronic stability control to drive market

- 15.2.3 JAPAN

- 15.2.3.1 High integration of advanced powertrain control systems to drive market

- 15.2.4 SOUTH KOREA

- 15.2.4.1 Tighter emission regulations to drive market

- 15.2.5 REST OF ASIA PACIFIC

- 15.2.1 CHINA

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 High ECU density in mid-size and luxury ICE vehicles to drive market

- 15.3.2 FRANCE

- 15.3.2.1 ADAS integration into mainstream ICE hatchbacks and crossovers to drive market

- 15.3.3 UK

- 15.3.3.1 High penetration of ADAS, digital instrument clusters, and connected infotainment to drive market

- 15.3.4 SPAIN

- 15.3.4.1 Strong base of compact and mid-size vehicle manufacturing to drive market

- 15.3.5 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 NORTH AMERICA

- 15.4.1 US

- 15.4.1.1 Early software-defined architecture adoption and connected vehicle integration to drive market

- 15.4.2 CANADA

- 15.4.2.1 Advanced safety integration in mainstream ICE sedans and compact SUVs to drive market

- 15.4.1 US

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 16.3 MARKET SHARE ANALYSIS, 2025

- 16.4 REVENUE ANALYSIS, 2021-2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Protocol type footprint

- 16.7.5.4 Application footprint

- 16.7.5.5 Vehicle class footprint

- 16.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING

- 16.8.5.1 List of start-ups/SMEs

- 16.8.5.2 Competitive benchmarking of start-ups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 16.9.2 DEALS

- 16.9.3 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 NXP SEMICONDUCTORS

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches/developments

- 17.1.1.3.2 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 ROBERT BOSCH GMBH

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches/developments

- 17.1.2.3.2 Other developments

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 INFINEON TECHNOLOGIES AG

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 STMICROELECTRONICS

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 MnM view

- 17.1.4.3.1 Key strengths

- 17.1.4.3.2 Strategic choices

- 17.1.4.3.3 Weaknesses and competitive threats

- 17.1.5 TEXAS INSTRUMENTS INCORPORATED

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Other developments

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 VECTOR INFORMATIK GMBH

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches/developments

- 17.1.6.3.2 Deals

- 17.1.7 RENESAS ELECTRONICS CORPORATION

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.8 MICROCHIP TECHNOLOGY INC.

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Deals

- 17.1.9 ELMOS SEMICONDUCTOR SE

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Other developments

- 17.1.10 BROADCOM

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.11 ANALOG DEVICES, INC.

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.12 ALPS ALPINE CO., LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Deals

- 17.1.1 NXP SEMICONDUCTORS

- 17.2 KEY ZONE CONTROLLER PLAYERS

- 17.2.1 AUMOVIO SE

- 17.2.1.1 Business overview

- 17.2.1.2 Products offered

- 17.2.1.3 Recent developments

- 17.2.1.3.1 Product launches/developments

- 17.2.1.3.2 Deals

- 17.2.1.3.3 Expansions

- 17.2.1.3.4 Other developments

- 17.2.2 VALEO

- 17.2.2.1 Business overview

- 17.2.2.2 Products offered

- 17.2.2.3 Recent developments

- 17.2.2.3.1 Deals

- 17.2.2.3.2 Other developments

- 17.2.3 APTIV

- 17.2.3.1 Business overview

- 17.2.3.2 Products offered

- 17.2.3.3 Recent developments

- 17.2.3.3.1 Deals

- 17.2.3.3.2 Other developments

- 17.2.4 SCHAEFFLER AG

- 17.2.4.1 Business overview

- 17.2.4.2 Products offered

- 17.2.4.3 Recent developments

- 17.2.4.3.1 Deals

- 17.2.4.3.2 Other developments

- 17.2.5 MARELLI HOLDINGS CO., LTD.

- 17.2.5.1 Business overview

- 17.2.5.2 Products offered

- 17.2.5.3 Recent developments

- 17.2.5.3.1 Product launches/developments

- 17.2.5.3.2 Deals

- 17.2.5.3.3 Other developments

- 17.2.1 AUMOVIO SE

- 17.3 OTHER PLAYERS

- 17.3.1 DSPACE

- 17.3.2 EXCELFORE

- 17.3.3 TE CONNECTIVITY

- 17.3.4 TECHNICA ENGINEERING GMBH

- 17.3.5 REALTEK SEMICONDUCTOR CORP

- 17.3.6 KNOWLEDGE DEVELOPMENT FOR POF S.L.

- 17.3.7 INTREPID CONTROL SYSTEMS

- 17.3.8 VALENS SEMICONDUCTOR

- 17.3.9 CADENCE DESIGN SYSTEMS, INC.

- 17.3.10 SYNOPSYS, INC.

- 17.3.11 NOVOSENSE

- 17.3.12 ROHM CO., LTD.

- 17.3.13 MELEXIS

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Primary interviewees from demand and supply sides

- 18.1.2.2 Breakdown of primary interviews

- 18.1.2.3 List of primary interview participants

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 DATA TRIANGULATION

- 18.4 FACTOR ANALYSIS

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.3.1 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY APPLICATION, AT COUNTRY LEVEL

- 19.3.2 AUTOMOTIVE COMMUNICATION PROTOCOL MARKET, BY PROTOCOL, AT COUNTRY LEVEL

- 19.3.3 COMPANY INFORMATION

- 19.3.3.1 Profiling of additional market players (up to five)

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS