|

시장보고서

상품코드

2011926

관성 항법 시스템 시장 예측(-2030년) : 용도별, 등급별, 기술별, 솔루션별, 지역별Inertial Navigation Systems Market by Application, Grade, Technology, Solution, Region - Global Forecast To 2030 |

||||||

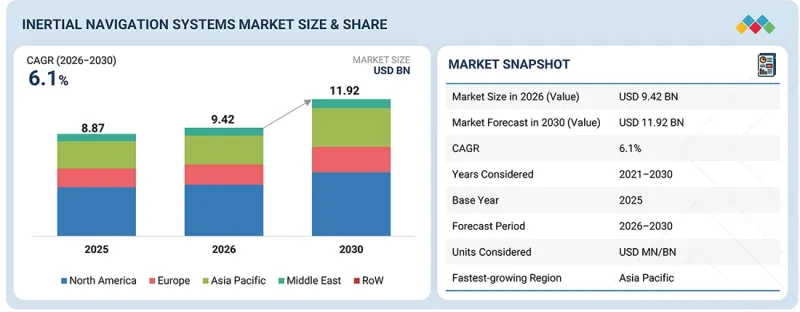

세계의 관성 항법 시스템 시장 규모는 2026년에 추정 94억 2,000만 달러로, 2030년까지 119억 2,000만 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 6.1%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2030년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2030년 |

| 단위 | 10억 달러 |

| 부문 | 용도, 기술, 솔루션, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

이 시장은 방위 및 상업용 플랫폼에서 정확하고 신뢰할 수 있는 항법에 대한 수요가 증가함에 따라 주도되고 있습니다. 미사일, 항공기, 선박, 자율주행차 등 최신 시스템에서는 특히 GPS 신호를 사용할 수 없는 상황에서 지속적인 측위 및 유도가 요구됩니다. 이에 따라 외부의 입력 없이 자율적으로 작동할 수 있는 관성항법시스템의 중요성이 커지고 있습니다.

동시에 국방 기관은 차세대 플랫폼과 정밀 작전을 위해 첨단 항법 기술에 대한 투자를 확대하고 있습니다. 광섬유 및 MEMS 기반 시스템을 포함한 센서 기술의 발전으로 이러한 솔루션은 더욱 컴팩트하고 효율적입니다. 또한 시스템 통합 및 처리 능력의 지속적인 개발로 육상, 해상, 항공, 우주 플랫폼에 INS를 쉽게 배치할 수 있게 되었습니다.

"기술별로는 통합 GNSS/INS 부문이 예측 기간 중 가장 큰 점유율을 차지할 것으로 예상됩니다. "

관성항법 및 위성측위 두 가지의 강점을 모두 갖춘 통합 GNSS/INS 부문이 관성항법 시스템 시장을 주도할 것으로 예상됩니다. 이 통합은 특히 GNSS 신호가 약하거나 일시적으로 사용할 수 없는 경우 전반적인 정확도와 신뢰성을 향상시킵니다. 또한 큰 중단 없이 지속적인 항해가 가능하며, 이는 국방 및 상업적 용도에 있으며, 중요한 요소입니다. 플랫폼의 고도화에 따라 다양한 운영 조건에서 안정적이고 고정밀도의 측위를 실현할 수 있는 통합 시스템에 대한 수요가 증가하고 있습니다. 따라서 현재 많은 최신 시스템들은 처음부터 GNSS/INS 통합을 전제로 설계되고 있습니다.

"솔루션별로는 가속도계 부문이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

가속도계 부문은 운동 측정 및 속도 변화 감지에 중요한 역할을 하므로 관성 항법 시스템 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이러한 구성 요소는 모든 관성 시스템에서 위치와 움직임을 계산하는 데 필수적인 요소입니다. 항공기, 미사일, 선박, 자율시스템의 항법 수요가 증가함에 따라 가속도계의 활용은 계속 확대되고 있습니다. 가속도계는 하이엔드부터 비용 중심의 애플리케이션까지 폭넓게 사용되고 있으며, 대부분의 INS 솔루션에 필수적인 요소로 자리 잡고 있습니다. 센서 성능의 지속적인 향상과 소형화도 그 보급을 촉진하고 있습니다.

"북미 지역이 예측 기간 중 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. "

북미는 강력한 국방 지출과 첨단 항법 기술의 조기 채택으로 인해 관성항법시스템(INS) 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이 지역에는 항공우주 및 방위산업이 발달해 있으며, 미국을 비롯한 여러 국가들이 차세대 항공기, 미사일 시스템, 해군 플랫폼, 우주 프로그램에 많은 투자를 하고 있습니다. 이러한 플랫폼에는 고정밀하고 신뢰할 수 있는 항법 시스템이 필요하며, 이는 INS에 대한 안정적인 수요를 촉진하고 있습니다. 또한 GPS를 사용할 수 없거나 사용이 제한되는 환경에서의 운용에 대한 관심이 높아지고 있으며, 이에 따라 독립적인 항법 시스템에 대한 요구가 증가하고 있습니다. 또한 R&D에 대한 지속적인 투자와 업계 주요 기업의 존재는 첨단 관성 시스템의 혁신과 대규모 배포를 지원하고 있습니다. 이러한 수요는 지역 전반의 자율 시스템 활용 확대와 기존 국방 인프라의 현대화로 더욱 강화되고 있습니다.

세계의 관성항법시스템(Inertial Navigation Systems) 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제8장 지속가능성과 규제 상황

제9장 관성 항법 시스템 시장 : 용도별

제10장 관성 항법 시스템 시장 : 등급별

제11장 관성 항법 시스템 시장 : 기술별

제12장 관성 항법 시스템 시장 : 솔루션별

제13장 관성 항법 시스템 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

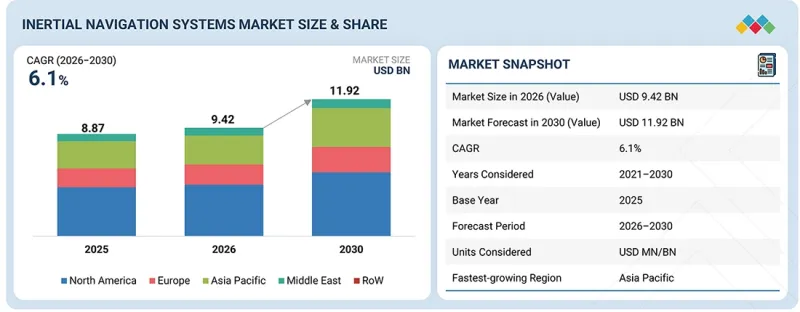

KSA 26.05.04The inertial navigation systems market is estimated at USD 9.42 billion in 2026 and is projected to reach USD 11.92 billion by 2030 at a CAGR of 6.1% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2025 |

| Forecast Period | 2026-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Application, Technology, Solution and Region |

| Regions covered | North America, Europe, APAC, RoW |

The market is driven by the rising need for accurate and reliable navigation across defense and commercial platforms. Modern systems such as missiles, aircraft, ships and autonomous vehicles require continuous positioning and guidance, especially in situations where GPS signals may not be available. This has increased the importance of inertial navigation systems that can operate independently without external inputs.

At the same time, defense forces are investing more in advanced navigation technologies to support next-generation platforms and precision operations. Improvements in sensor technologies, including fiber optic and MEMS-based systems, are helping make these solutions more compact and efficient. Ongoing developments in system integration and processing capabilities are also making it easier to deploy INS across land, naval, airborne, and space platforms.

"By technology, the Integrated GNSS/INS segment is projected to be the most dominant during the forecast period."

The integrated GNSS/INS segment is expected to lead the inertial navigation systems market as it combines the strengths of both inertial navigation and satellite-based positioning. This integration helps improve overall accuracy and reliability, especially in cases where GNSS signals are weak or temporarily unavailable. It also allows continuous navigation without major interruptions, which is important for defense and commercial applications. As platforms become more advanced, there is a growing preference for integrated systems that can deliver stable and precise positioning across different operating conditions. This is why many modern systems are now being designed with GNSS/INS integration from the beginning.

"By solution, the accelerometer segment is projected to account for the largest market share during the forecast period."

The accelerometer segment is expected to hold the largest share of the inertial navigation systems market since it plays a key role in measuring motion and detecting changes in velocity. These components are essential for calculating position and movement in any inertial system. With increasing demand for navigation across aircraft, missiles, marine vessels, and autonomous systems, the use of accelerometers continues to grow. They are widely used across both high-end and cost-sensitive applications, making them a fundamental part of most INS solutions. Continuous improvements in sensor performance and miniaturization are also supporting their widespread adoption.

"North America is projected to have the largest market share during the forecast period."

North America is expected to hold the largest share of the inertial navigation systems (INS) market, mainly due to strong defense spending and early adoption of advanced navigation technologies. The region has a well-established aerospace and defense industry, with countries like the US investing heavily in next-generation aircraft, missile systems, naval platforms, and space programs. These platforms require highly accurate and reliable navigation systems, which is driving consistent demand for INS. There is also a growing focus on operating in GPS denied or contested environments, which is increasing the need for independent navigation systems. In addition, continuous investments in R&D and the presence of major industry players are supporting innovation and large-scale deployment of advanced inertial systems. The demand is further supported by the increasing use of autonomous systems and modernization of existing defense infrastructure across the region.

The breakdown of profiles for primary participants in the inertial navigation systems market is provided below:

- By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

- By Designation: Directors - 25%, Managers - 30%, and Others - 45%

- By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, Middle East - 10% , and Rest of the World - 5%

Research Coverage:

This market study covers the inertial navigation systems market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different parts and regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to buy this report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall inertial navigation systems market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

- Market Drivers (Rising emphasis on assured and resilient navigation architectures, expansion of autonomous and unmanned platform deployments, sustained growth in aerospace and space missions, advancements in high-performance sensor technologies),

Restraints (High cost of navigation-grade inertial systems, cumulative drift and dependence on external aiding for long-duration missions, supply chain concentration in precision sensor manufacturing), Opportunities (Integration with low Earth Orbit satellite constellations and hybrid navigation architectures, growth of urban air mobility and advanced air mobility platforms, expansion of precision agriculture and industrial automation, increasing space exploration and deep space mission activity),

Challenges (Maintaining long-term accuracy under extended mission durations, environmental sensitivity and performance stability, increasing competition from alternative navigation technologies, export controls and regulatory compliance constraints)

- Market Penetration: Comprehensive information on inertial navigation systems market offered by the top players in the market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INERTIAL NAVIGATION SYSTEMS MARKET

- 3.2 INERTIAL NAVIGATION SYSTEMS MARKET, BY APPLICATION

- 3.3 INERTIAL NAVIGATION SYSTEMS MARKET, BY GRADE

- 3.4 INERTIAL NAVIGATION SYSTEMS MARKET, BY TECHNOLOGY

- 3.5 INERTIAL NAVIGATION SYSTEMS MARKET, BY SOLUTION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Emphasis on assured navigation architectures

- 4.2.1.2 Expansion of autonomous and unmanned systems

- 4.2.1.3 Growth in aerospace and space missions

- 4.2.1.4 Advancements in high-performance sensor technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Cumulative drift and dependence on external aiding for long- duration missions

- 4.2.2.2 Supply chain concentration in precision sensor manufacturing

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration with LEO satellite constellations and hybrid navigation architectures

- 4.2.3.2 Development of urban air mobility and advanced air mobility platforms

- 4.2.3.3 Rise of precision agriculture and industrial automation

- 4.2.4 CHALLENGES

- 4.2.4.1 Maintaining long-term accuracy under extended mission durations

- 4.2.4.2 Environmental sensitivity and performance stability

- 4.2.4.3 Increased competition from alternative navigation technologies

- 4.2.4.4 Export controls and regulatory compliance constraints

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 LIMITED MODULARITY AND UPGRADE FLEXIBILITY

- 4.3.2 INDUSTRIAL SCALABILITY AND SURGE PRODUCTION CAPABILITY

- 4.3.3 LIFECYCLE VISIBILITY AND PREDICTIVE SUSTAINMENT INTEGRATION

- 4.3.4 CROSS-PLATFORM INTEROPERABILITY AND STANDARDIZATION GAPS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6 TOTAL COST OF OWNERSHIP

- 4.7 BUSINESS MODELS

- 4.7.1 DIRECT SALES AND GOVERNMENT CONTRACT MODEL

- 4.7.2 OEM INTEGRATION AND PLATFORM-EMBEDDED MODEL

- 4.7.3 AFTERMARKET AND LIFECYCLE SUPPORT MODEL

- 4.7.4 MODULAR AND SOFTWARE-ENABLED NAVIGATION PLATFORM MODEL

- 4.8 BILL OF MATERIALS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC OUTLOOK

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL INERTIAL NAVIGATION SYSTEM INDUSTRY

- 5.1.4 TRENDS IN GLOBAL INERTIAL NAVIGATION SYSTEM COMPONENT INDUSTRY

- 5.2 VALUE CHAIN ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.3.1 PROMINENT COMPANIES

- 5.3.2 PRIVATE AND SMALL ENTERPRISES

- 5.3.3 END USERS

- 5.4 PRICING ANALYSIS

- 5.5 TRADE ANALYSIS

- 5.5.1 INERTIAL NAVIGATION SYSTEMS: IMPORT SCENARIO (HS CODE 901420 + 901480)

- 5.5.2 INERTIAL NAVIGATION SYSTEMS MARKET: EXPORT SCENARIO (HS CODE: 901420 + 901480)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 NORTHROP GRUMMAN: LGM-35 SENTINEL ICBM NAVIGATION MODERNIZATION

- 5.8.2 SAFRAN ELECTRONICS: DASSAULT RAFALE FIGHTER NAVIGATION SYSTEM

- 5.8.3 HONEYWELL: INERTIAL REFERENCE UNIT DEPLOYMENT IN COMMERCIAL NARROW-BODY AIRCRAFT PLATFORMS

- 5.8.4 SPACEX: FALCON 9 & DRAGON NAVIGATION SYSTEMS

- 5.8.5 BLUE ORIGIN: LUNAR LANDER NAVIGATION

- 5.9 IMPACT OF 2025 US TARIFFS

- 5.9.1 INTRODUCTION

- 5.9.2 KEY TARIFF RATES

- 5.9.3 PRICE IMPACT ANALYSIS

- 5.9.4 IMPACT ON COUNTRY/REGION

- 5.9.4.1 US

- 5.9.4.2 Europe

- 5.9.4.3 Asia Pacific

- 5.9.5 IMPACT ON APPLICATIONS

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS

- 6.2.2 KEY BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS OF END-USE INDUSTRIES

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 KEY TECHNOLOGIES

- 7.1.1 MICRO-ELECTROMECHANICAL SYSTEMS (MEMS)-BASED INERTIAL SENSORS

- 7.1.2 FIBER-OPTIC AND RING LASER GYROSCOPES

- 7.1.3 AI-ENABLED SENSOR FUSION AND NAVIGATION ALGORITHMS

- 7.1.4 QUANTUM INERTIAL SENSING AND NEXT-GENERATION NAVIGATION

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 GNSS INTEGRATION AND HYBRID NAVIGATION SYSTEMS

- 7.2.2 SENSOR CALIBRATION, ERROR COMPENSATION, AND SIGNAL PROCESSING

- 7.2.3 SIMULTANEOUS LOCALIZATION AND MAPPING (SLAM) AND VISION-AIDED NAVIGATION

- 7.3 TECHNOLOGY ROADMAP

- 7.4 PATENT ANALYSIS

- 7.5 FUTURE APPLICATIONS

- 7.6 IMPACT OF AI/GENERATIVE AI

- 7.6.1 TOP USE CASES AND MARKET POTENTIAL

- 7.6.2 CASE STUDIES OF AI IMPLEMENTATION

- 7.6.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.6.4 CLIENTS' READINESS TO ADOPT AI/GENERATIVE AI

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 REGIONAL REGULATIONS AND COMPLIANCE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS

- 8.2 SUSTAINABILITY INITIATIVES

- 8.2.1 CARBON IMPACT REDUCTION

- 8.2.2 ECO-APPLICATIONS

- 8.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

9 INERTIAL NAVIGATION SYSTEMS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 COMPARISON OF INERTIAL NAVIGATION SYSTEMS BASED ON AUTONOMY LEVEL

- 9.2.1 FULLY AUTONOMOUS

- 9.2.2 SEMI-AUTONOMOUS

- 9.2.3 REMOTELY OPERATED

- 9.2.4 CREW-OPERATED

- 9.3 MISSILE & MUNITION

- 9.3.1 NEED FOR PRECISION STRIKE CAPABILITIES IN MODERN DEFENSE

- 9.3.2 MISSILE

- 9.3.2.1 Ballistic missile

- 9.3.2.2 Cruise missile

- 9.3.2.3 Interceptor missile

- 9.3.3 GUIDED ROCKET

- 9.3.4 GUIDED AMMUNITION

- 9.3.4.1 Mortar ammunition

- 9.3.4.2 Tank ammunition

- 9.3.4.3 Artillery ammunition

- 9.3.4.4 Naval ammunition

- 9.3.5 LOITERING MUNITION

- 9.3.6 TORPEDO

- 9.4 AIRBORNE PLATFORM

- 9.4.1 INCREASING DEMAND FOR ADVANCED NAVIGATION CAPABILITIES IN COMMERCIAL AND MILITARY AVIATION

- 9.4.2 COMMERCIAL AIRCRAFT

- 9.4.2.1 Narrow-body aircraft

- 9.4.2.2 Wide-body aircraft

- 9.4.2.3 Regional jet

- 9.4.2.4 Business jet

- 9.4.2.5 Commercial helicopter

- 9.4.2.6 Light aircraft

- 9.4.3 MILITARY AIRCRAFT

- 9.4.3.1 Fighter jet

- 9.4.3.2 Transport aircraft

- 9.4.3.3 Special mission aircraft

- 9.4.3.4 Military helicopter

- 9.5 SPACE PLATFORM

- 9.5.1 RISING SPACE LAUNCH ACTIVITIES AND EXPANDING SATELLITE CONSTELLATIONS

- 9.5.2 SPACE LAUNCH VEHICLE

- 9.5.3 SATELLITE

- 9.6 MARINE PLATFORM

- 9.6.1 GROWING DEMAND FOR RELIABLE NAVIGATION IN COMMERCIAL SHIPPING AND NAVAL OPERATIONS

- 9.6.2 COMMERCIAL SURFACE VESSEL

- 9.6.3 MILITARY SURFACE VESSEL

- 9.6.4 OFFSHORE PLATFORM

- 9.6.5 SUBMARINE

- 9.7 LAND APPLICATION

- 9.7.1 IMPROVED FOCUS ON DEFENSE MODERNIZATION AND NETWORK-CENTRIC WARFARE

- 9.7.2 MILITARY VEHICLE

- 9.7.2.1 Combat vehicle

- 9.7.2.1.1 Main battle tank

- 9.7.2.1.2 Infantry fighting vehicle

- 9.7.2.1.3 Armored personnel carrier

- 9.7.2.1.4 Mine-resistant ambush-protected vehicle

- 9.7.2.1.5 Light armored vehicle

- 9.7.2.2 Combat support vehicle

- 9.7.2.2.1 Armored supply truck

- 9.7.2.2.2 Armored command & control vehicle

- 9.7.2.2.3 Repair & recovery vehicle

- 9.7.2.2.4 Bridge-laying tank

- 9.7.2.2.5 Mine clearance vehicle

- 9.7.2.3 Fire support & air defense vehicle

- 9.7.2.3.1 Self-propelled artillery vehicle

- 9.7.2.3.2 Air defense vehicle

- 9.7.2.1 Combat vehicle

- 9.7.3 CIVIL & INDUSTRIAL MOBILE PLATFORM

- 9.7.3.1 On-road autonomous vehicle

- 9.7.3.1.1 Autonomous passenger vehicle

- 9.7.3.1.2 Autonomous passenger shuttle

- 9.7.3.1.3 Autonomous freight vehicle

- 9.7.3.2 Off-road industrial mobile platform

- 9.7.3.2.1 Construction machinery

- 9.7.3.2.2 Mining machinery

- 9.7.3.2.3 Agricultural machinery

- 9.7.3.3 Rail system

- 9.7.3.3.1 Passenger rail

- 9.7.3.3.2 Freight rail

- 9.7.3.3.3 Rail track inspection & measurement platform

- 9.7.3.3.4 Rail maintenance-of-way platform

- 9.7.3.1 On-road autonomous vehicle

- 9.7.4 INDUSTRIAL & MOBILE ROBOTIC PLATFORM

- 9.7.4.1 Fixed industrial robot

- 9.7.4.2 Automated guided vehicle

- 9.7.4.3 Autonomous mobile robot

- 9.7.4.4 Industrial mobile robot

- 9.8 UNMANNED VEHICLE

- 9.8.1 ESCALATING USE OF UNMANNED SYSTEMS IN DEFENSE APPLICATIONS

- 9.8.2 UNMANNED AERIAL VEHICLE

- 9.8.3 UNMANNED GROUND VEHICLE

- 9.8.4 UNMANNED MARITIME VEHICLE

- 9.8.4.1 Unmanned underwater vehicle

- 9.8.4.2 Unmanned surface vehicle

- 9.9 DISMOUNTED & PORTABLE SYSTEM

- 9.9.1 HEIGHTENED EMPHASIS ON SOLDIER MODERNIZATION PROGRAMS

- 9.9.2 SOLDIER NAVIGATION & WEARABLE SYSTEM

- 9.9.3 HANDHELD & MANPACK POSITIONING UNIT

10 INERTIAL NAVIGATION SYSTEMS MARKET, BY GRADE

- 10.1 INTRODUCTION

- 10.2 COMPARISON OF INERTIAL NAVIGATION SYSTEMS BASED ON DEPLOYMENT ARCHITECTURE

- 10.2.1 GIMBALED

- 10.2.2 STRAPDOWN

- 10.3 CONSUMER-GRADE

- 10.3.1 IMPROVED PERFORMANCE WITH ADVANCEMENTS IN MEMS TECHNOLOGY AND SENSOR FUSION ALGORITHMS

- 10.4 INDUSTRIAL-GRADE

- 10.4.1 INCREASED ADOPTION OF AUTOMATION AND DIGITAL TECHNOLOGIES ACROSS INDUSTRIES

- 10.5 TACTICAL-GRADE

- 10.5.1 NEED FOR RELIABLE NAVIGATION IN ELECTRONIC WARFARE

- 10.6 NAVIGATION-GRADE

- 10.6.1 CONTINUOUS ADVANCES IN SENSOR TECHNOLOGY AND SYSTEM INTEGRATION

11 INERTIAL NAVIGATION SYSTEMS MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 STANDALONE

- 11.2.1 SELF-CONTAINED NAVIGATION FOR GNSS-DENIED AND HIGH-INTEGRITY APPLICATIONS

- 11.2.1.1 Use case: Standalone inertial navigation system in Trident II (D5) submarine-launched ballistic missile

- 11.2.1 SELF-CONTAINED NAVIGATION FOR GNSS-DENIED AND HIGH-INTEGRITY APPLICATIONS

- 11.3 INTEGRATED GNSS/INS OR GNSS-AIDED

- 11.3.1 ENHANCED ACCURACY AND DRIFT CORRECTION THROUGH GNSS INTEGRATION

- 11.3.1.1 Use case: Integrated GNSS/INS in Boeing 787 Dreamliner

- 11.3.1 ENHANCED ACCURACY AND DRIFT CORRECTION THROUGH GNSS INTEGRATION

- 11.4 HYBRID/MULTISENSOR-BASED

- 11.4.1 ADVANCED SENSOR FUSION FOR RESILIENT AND HIGH-PRECISION NAVIGATION

- 11.4.1.1 Use case: Hybrid inertial navigation system in autonomous vehicle platform

- 11.4.1 ADVANCED SENSOR FUSION FOR RESILIENT AND HIGH-PRECISION NAVIGATION

12 INERTIAL NAVIGATION SYSTEMS MARKET, BY SOLUTION

- 12.1 INTRODUCTION

- 12.2 ACCELEROMETER

- 12.2.1 SURGE IN DEMAND DUE TO EVOLVING NAVIGATION REQUIREMENTS

- 12.3 GYROSCOPE

- 12.3.1 RAPID INTEGRATION OF ADVANCED ALGORITHMS AND SENSOR FUSION SYSTEMS

- 12.3.2 RING LASER GYRO

- 12.3.3 FIBER OPTIC GYRO

- 12.3.4 MICROELECTROMECHANICAL SYSTEM (MEMS) GYRO

- 12.3.5 OTHERS

- 12.4 ALGORITHM & PROCESSOR

- 12.4.1 REAL-TIME DATA PROCESSING AND SENSOR FUSION FOR NAVIGATION COMPUTATION

- 12.5 OTHER SOLUTIONS

13 INERTIAL NAVIGATION SYSTEMS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Large-scale defense programs and autonomous platform expansion to drive market

- 13.2.2 CANADA

- 13.2.2.1 Growing autonomous system adoption to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Advancements in resilient navigation and next-generation defense programs to drive market

- 13.3.2 GERMANY

- 13.3.2.1 Strong industrial base and advanced sensor engineering to drive growth

- 13.3.3 ITALY

- 13.3.3.1 Increasing emphasis on integrated navigation solutions and advanced sensor technologies to drive market

- 13.3.4 FRANCE

- 13.3.4.1 Industrial expertise in aerospace, defense, and navigation technologies to drive market

- 13.3.5 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rapid expansion of unmanned systems, missile programs, and satellite constellations to drive market

- 13.4.2 INDIA

- 13.4.2.1 National programs focused on navigation, communication, Earth observation, and scientific missions to drive market

- 13.4.3 JAPAN

- 13.4.3.1 Strong capabilities in precision manufacturing, advanced materials, and sensor engineering to drive market

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Transition toward autonomous systems and advanced defense platforms to drive market

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST

- 13.5.1 GCC

- 13.5.1.1 UAE

- 13.5.1.1.1 Transition toward advanced aerospace systems to drive market

- 13.5.1.2 Saudi Arabia

- 13.5.1.2.1 National aerospace expansion initiatives to drive market

- 13.5.1.1 UAE

- 13.5.2 REST OF MIDDLE EAST

- 13.5.1 GCC

- 13.6 REST OF THE WORLD

- 13.6.1 LATIN AMERICA

- 13.6.1.1 Gradual expansion of space and defense programs to drive market

- 13.6.2 AFRICA

- 13.6.2.1 Expanding aerospace and defense initiatives to drive market

- 13.6.1 LATIN AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2026

- 14.3 REVENUE ANALYSIS, 2021-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Technology footprint

- 14.7.5.4 Solution footprint

- 14.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.8.5.1 List of start-ups/SMEs

- 14.8.5.2 Competitive benchmarking of start-ups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 HONEYWELL INTERNATIONAL INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches/developments

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 NORTHROP GRUMMAN

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches/developments

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 SAFRAN ELECTRONICS & DEFENSE

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches/developments

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 COLLINS AEROSPACE

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches/developments

- 15.1.4.3.2 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Competitive threats and weaknesses

- 15.1.5 TELEDYNE TECHNOLOGIES INCORPORATED

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches/developments

- 15.1.5.3.2 Other developments

- 15.1.5.4 MnM View

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Competitive threats and weaknesses

- 15.1.6 THALES

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.3.2 Other developments

- 15.1.7 HEXAGON AB

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.8 TRIMBLE INC.

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches/developments

- 15.1.8.3.2 Deals

- 15.1.9 GENERAL ELECTRIC COMPANY

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.10 LEONARDO S.P.A.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.11 ISRAEL AEROSPACE INDUSTRIES LTD.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 BHARAT ELECTRONICS LIMITED

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Other developments

- 15.1.13 ASELSAN A.S.

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Other developments

- 15.1.14 KONGSBERG DEFENCE & AEROSPACE

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.15 EXAIL TECHNOLOGIES

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.15.3.2 Other developments

- 15.1.1 HONEYWELL INTERNATIONAL INC.

- 15.2 OTHER PLAYERS

- 15.2.1 VECTORNAV TECHNOLOGIES

- 15.2.2 SBG SYSTEMS

- 15.2.3 INERTIAL LABS, INC.

- 15.2.4 IMAR NAVIGATION GMBH

- 15.2.5 INNALABS

- 15.2.6 MICROSTRAIN BY HBK

- 15.2.7 SILICON SENSING

- 15.2.8 SILICON DESIGN, INC.

- 15.2.9 XSENS

- 15.2.10 SPARTON NAVIGATION AND EXPLORATION LTD.

- 15.2.11 ADVANCED NAVIGATION

- 15.2.12 GUIDENAV

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Primary sources

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of primary interviews

- 16.1.2.4 Key industry insights

- 16.1.1 SECONDARY DATA

- 16.2 FACTOR ANALYSIS

- 16.2.1 DEMAND-SIDE INDICATORS

- 16.2.2 SUPPLY-SIDE INDICATORS

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 BOTTOM-UP APPROACH

- 16.3.2 TOP-DOWN APPROACH

- 16.4 DATA TRIANGULATION

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS